1. What are the major growth drivers for the Vehicle Wrap Film Market market?

Factors such as are projected to boost the Vehicle Wrap Film Market market expansion.

+1 2315155523

Vehicle Wrap Film Market

Vehicle Wrap Film Market

Market Lens IQ is a global market intelligence and strategic consulting firm delivering advanced syndicated research reports, customized industry analysis, competitive intelligence, and data-driven advisory solutions to organizations across international markets. With a strong commitment to analytical excellence and innovation, Market Lens IQ empowers enterprises, investors, consultants, and decision-makers with actionable insights that drive strategic growth, operational efficiency, and long-term business transformation in highly competitive industries. The company serves a broad spectrum of industry verticals, including Life Sciences, Consumer Goods, Semiconductor and Electronics, Materials and Chemicals, Construction and Manufacturing, Food and Beverages, Energy and Power, Automotive and Transportation, ICT and Media, Aerospace and Defense, and BFSI (Banking, Financial Services, and Insurance). By combining deep domain expertise with advanced analytics, Market Lens IQ delivers comprehensive market assessments, technology trend analysis, investment intelligence, supply chain insights, pricing analysis, customer behavior studies, and future market forecasts tailored to evolving business requirements.

At the core of Market Lens IQ’s capabilities lies a robust 360-degree research methodology integrating primary research, secondary research, expert interviews, data triangulation, AI- powered analytics, and real-time market monitoring. Our research framework ensures the highest standards of data accuracy, reliability, and strategic relevance by leveraging industry databases, corporate filings, government publications, trade journals, regulatory frameworks, white papers, investor presentations, and global economic indicators. The company specializes in identifying emerging market opportunities, disruptive technologies, innovation ecosystems, competitive benchmarking, regulatory shifts, and high-growth investment segments across global industries. Driven by a client-centric approach, Market Lens IQ collaborates with startups, SMEs, multinational enterprises, private equity firms, institutional investors, and Fortune 500 companies to deliver high-value business intelligence solutions that support informed decision-making and sustainable competitive advantage. Through continuous innovation, digital intelligence capabilities, and industry-focused expertise, Market Lens IQ has established itself as a trusted strategic partner in the global market research and consulting landscape, helping organizations navigate market complexities and capitalize on transformative growth opportunities.

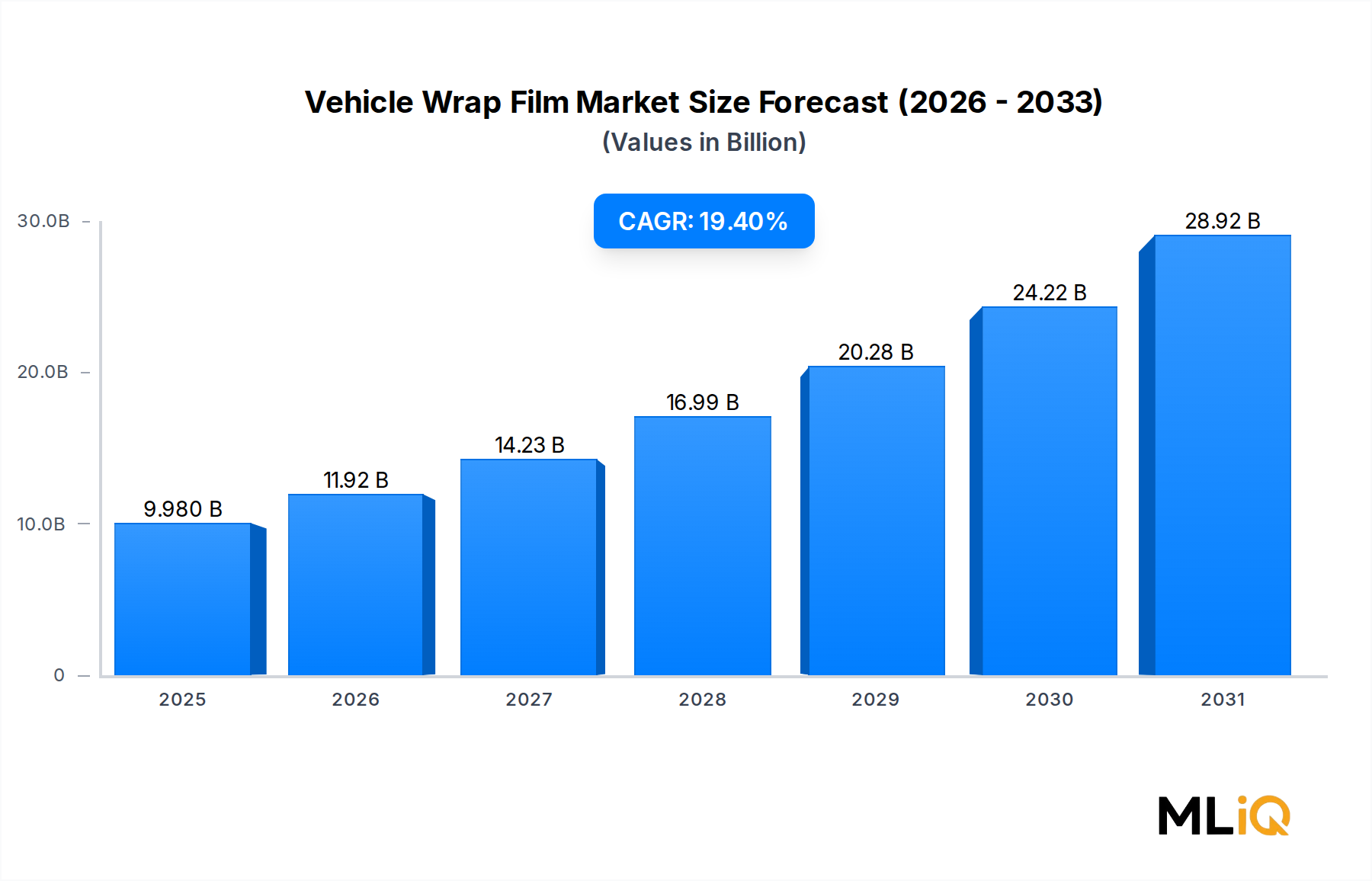

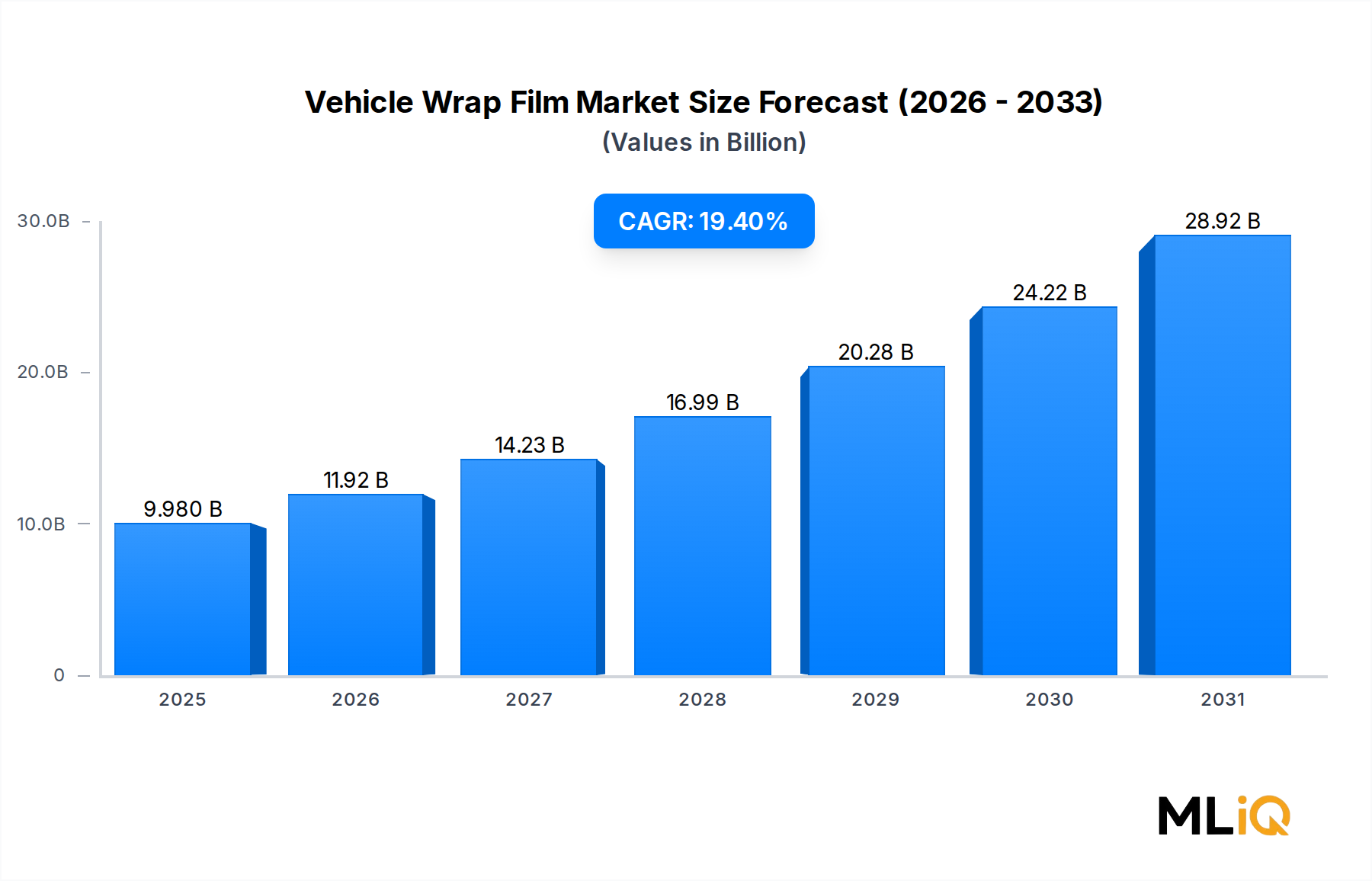

The global Vehicle Wrap Film Market is experiencing a period of exceptional expansion, underpinned by a convergence of advertising innovation, automotive customization trends, and technological advances in film chemistry. As of the base assessment period, the market is valued at $9.98 billion and is projected to scale significantly over the forecast horizon at a compound annual growth rate (CAGR) of 19.4%. This robust trajectory places the Vehicle Wrap Film Market among the fastest-growing segments within the broader automotive accessories and protective coatings universe.

Several macro tailwinds are fueling this momentum. The global proliferation of fleet-based brand advertising has emerged as a primary demand catalyst, with companies across logistics, food delivery, retail, and telecommunications increasingly leveraging vehicle surfaces as mobile billboards. This shift in out-of-home advertising strategy has directly elevated demand for high-performance wrap films across both commercial and passenger vehicle segments. Simultaneously, a burgeoning DIY automotive culture, amplified by social media visibility, has drawn individual vehicle owners into the wrap film ecosystem, driving strong retail-channel volume growth.

From a technology standpoint, advances in cast vinyl formulation, air-release adhesive channels, and conformable film structures have dramatically reduced installation complexity and extended product lifespans. These enhancements are accelerating adoption across both professional installation centers and the growing do-it-yourself segment. The increasing availability of specialty finishes—including matte, chrome, satin, color-shift, and textured surfaces—has broadened the addressable consumer base beyond purely functional applications into the realm of high-end vehicle aesthetics.

Institutionally, rising corporate investment in mobile advertising, particularly among last-mile delivery companies whose fleets have expanded materially post-pandemic, is providing a stable, recurring demand stream. Environmental factors also play a role: compared to conventional repainting, vinyl wrapping generates lower volatile organic compound (VOC) emissions and offers reversibility, aligning with fleet operators' sustainability mandates.

Looking forward, the Vehicle Wrap Film Market is positioned to benefit from continued urbanization, electric vehicle fleet expansion—which often necessitates brand differentiation beyond traditional paint—and digital integration with printed wrap technologies. The Asia Pacific region is expected to contribute disproportionately to incremental growth over the forecast window, while North America and Europe maintain their positions as high-value, mature markets. Innovation pipelines across leading manufacturers suggest that next-generation self-healing and thermochromic films will unlock further premium market segments within the next three to five years.

Within the Vehicle Wrap Film Market, the Wrap Films sub-segment commands the largest revenue share across the Film Type classification, significantly outpacing both Window Films and Paint Protection Films in absolute market volume and dollar value. This dominance is attributable to a multi-layered value proposition that serves both commercial advertisers and individual vehicle owners seeking aesthetic transformation without permanent modification.

Wrap films, primarily composed of calendered or cast polyvinyl chloride substrates with pressure-sensitive adhesive backing, are uniquely positioned at the intersection of functional durability and visual customization. Their application scope spans full-body vehicle wraps for fleet branding, partial wraps for promotional campaigns, and single-panel color changes for personal vehicles. This versatility enables a single product category to serve fundamentally different buyer personas—from chief marketing officers of multinational logistics companies to independent automotive enthusiasts—thereby compressing market fragmentation and concentrating revenue within the segment.

The commercial advertising application is the most significant revenue driver within the Wrap Films sub-segment. Fleet operators deploying hundreds or thousands of vehicles require consistent, large-format, high-opacity films that can be mass-produced to tight color tolerances and installed efficiently across diverse geographic locations. This demand profile supports high average order values, multi-year procurement contracts, and strong customer retention rates for film manufacturers capable of meeting enterprise-grade quality standards.

Key players commanding substantial share within the Wrap Films sub-segment include 3M, Avery Dennison Corporation, ORAFOL Europe GmbH, Hexis S.A.S., and Arlon Graphics LLC. These manufacturers have invested heavily in proprietary adhesive technologies—most notably air-egress channel systems that eliminate installation bubbles—and in premium cast vinyl formulations that offer superior conformability over complex vehicle curves and rivets. Their competitive moats are reinforced by extensive global distribution networks, certified installer programs, and product warranties of five to twelve years depending on film grade.

The sub-segment's revenue share is consolidating rather than fragmenting. While regional and lower-cost manufacturers such as Guangzhou Carbins Film Co. have captured price-sensitive segments in emerging markets, the overall trend in developed markets is toward premiumization. End users are demonstrably willing to pay higher per-square-foot prices for films that offer enhanced UV resistance, longer durability, and expanded color libraries. This premiumization dynamic is compressing the volume advantage of commodity-grade products while expanding the margin profile for technology-differentiated offerings.

From an application standpoint, the Advertisement Purpose segment within the broader market is structurally aligned with Wrap Films, creating a reinforcing demand loop. As digital out-of-home advertising budgets grow and fleet networks expand—particularly in the e-commerce logistics and ride-sharing sectors—Wrap Films are increasingly specified as the preferred substrate for mobile brand communication. Industry estimates suggest that fleet wrap advertising can generate between 30,000 and 70,000 daily visual impressions per vehicle in urban environments, a cost-per-impression metric that competes favorably with static billboard and transit advertising.

The Safety Purpose application sub-segment, while smaller in absolute terms, also predominantly utilizes Wrap Films for high-visibility conspicuity marking on emergency vehicles, construction fleet, and public transit assets. Regulatory mandates in multiple jurisdictions requiring retroreflective markings on heavy commercial vehicles are sustaining a structurally non-cyclical demand base within this niche, further underpinning the Wrap Films segment's overall revenue resilience.

The Vehicle Wrap Film Market is propelled by a distinct set of quantifiable drivers while also navigating several material constraints that shape competitive dynamics and investment calculus.

The primary demand driver is the accelerating adoption of vehicle-based advertising by commercial fleet operators. The global last-mile delivery vehicle fleet is estimated to have grown by over 25% between 2020 and 2024, driven by structural shifts in e-commerce penetration. Each new delivery vehicle represents an incremental wrap film demand unit, and fleet operators' preference for full-body branding wraps over partial decals is pushing average revenue per vehicle installation higher.

The rise of electric vehicles (EVs) constitutes a secondary but increasingly important driver. EV manufacturers and fleet operators frequently seek to differentiate their vehicles through non-standard paint colors and textures that are prohibitively expensive through factory paint processes. Wrap films offer a cost-effective route to visual differentiation, and the rapid growth of EV fleets—global EV sales surpassed 10 million units in 2023 alone—is generating a structurally new demand category.

On the constraints side, raw material price volatility represents the most significant market headwind. Wrap films rely heavily on plasticized PVC resin, polyurethane, and specialty adhesive polymers, all of which are subject to petrochemical commodity cycles. Significant input cost inflation between 2021 and 2023 compressed manufacturer margins and forced selective price increases across product lines, dampening volume growth in price-sensitive segments.

Installer skill scarcity also constrains market velocity. The quality of a wrap installation is critically dependent on technician proficiency, and the global pool of certified wrap installers has not scaled commensurately with market demand. This bottleneck extends project lead times and increases labor cost as a percentage of total installation spend, particularly in North America and Western Europe.

Regulatory fragmentation across jurisdictions—particularly regarding VOC emissions from adhesive outgassing and end-of-life film disposal requirements—adds compliance cost and complexity for manufacturers targeting multi-regional distribution.

The competitive landscape of the Vehicle Wrap Film Market is characterized by a mix of global technology leaders, specialized regional manufacturers, and vertically integrated graphics solutions providers. The following profiles outline the strategic positioning of key participants:

3M: The company occupies a commanding position in the premium wrap film segment, leveraging its proprietary Controltac and Comply adhesive technologies. Its global distribution infrastructure and certified wrap installer network provide sustained competitive advantages across both commercial fleet and retail channels.

Avery Dennison Corporation: A major force in pressure-sensitive materials, Avery Dennison deploys its Supreme Wrapping Film series as a high-performance alternative targeting professional installers. The company's global manufacturing footprint and supply chain integration support consistent quality delivery across diverse geographies.

ORAFOL Europe GmbH: A Germany-headquartered manufacturer renowned for its ORACAL brand, ORAFOL maintains strong penetration in both the European professional and emerging DIY segments. Its calendar and cast vinyl lines are widely specified in fleet graphics and vehicle color change applications.

Hexis S.A.S.: A French specialist manufacturer with a strong European presence, Hexis is recognized for innovative product launches in textured and specialty finishes. The company's focus on installer-centric product design has cultivated strong loyalty among professional wrap studios.

Arlon Graphics LLC: Positioned as a technically differentiated supplier, Arlon focuses on high-performance cast vinyl films for demanding commercial applications including transit vehicles and heavy commercial fleet wraps. Its products are noted for long service life under high-UV and high-abrasion conditions.

KPMF: A UK-based manufacturer specializing in color-shift, matte, and unique-effect wrap films. KPMF has built a strong reputation in the premium vehicle customization segment through regular new finish introductions and a global distribution partnership network.

Vvivid Vinyl: A direct-to-consumer brand that has captured significant share in the DIY vehicle wrap segment, offering accessible pricing and a broad color selection. The company's e-commerce-first distribution model has enabled rapid geographic expansion without traditional distributor overhead.

Guangzhou Carbins Film Co., LTD: A China-based manufacturer providing cost-competitive wrap films for emerging market applications and price-sensitive commercial segments. The company's manufacturing scale in the Pearl River Delta region supports competitive export pricing.

Fedrigoni S.P.A: An Italy-headquartered specialty papers and films group that has extended its materials expertise into self-adhesive films for vehicle applications. Fedrigoni's premium branding and European distribution channels position it in the quality-differentiated commercial wrap segment.

JMR Graphics: A full-service graphics provider bridging design, production, and installation services, JMR Graphics competes at the applied solutions level rather than purely as a film manufacturer, serving large fleet clients with turnkey vehicle branding programs.

March 2023: 3M announced a product line expansion of its 1080 Series wrap film to include additional specialty satin and brushed metallic finishes, targeting the premium vehicle customization segment and responding to documented installer demand for broader texture portfolios.

June 2023: Avery Dennison Corporation launched an updated formulation of its Supreme Wrapping Film featuring enhanced cold-crack resistance, extending the film's operational temperature range and addressing installer feedback from high-latitude markets in Northern Europe and Canada.

September 2023: ORAFOL Europe GmbH introduced a bio-attributed PVC wrap film series as part of its sustainability roadmap, sourcing a portion of its vinyl resin from bio-based feedstocks in response to European regulatory pressure on petrochemical-derived plastics.

January 2024: Hexis S.A.S. announced a strategic distribution partnership with a major Asia Pacific automotive accessories distributor, marking a deliberate expansion push into the high-growth markets of South Korea, Japan, and ASEAN.

April 2024: Vvivid Vinyl expanded its direct-to-consumer platform by launching a proprietary online wrap calculator and installation tutorial library, reducing the experience barrier for first-time DIY installers and broadening its addressable retail customer base.

July 2024: A major European fleet operator publicly reported completing the wrap branding of over 5,000 delivery vehicles using certified wrap film products, citing cost-per-impression efficiency and reversibility as key decision criteria versus traditional livery painting.

November 2024: Industry trade body FESPA published updated installer certification guidelines incorporating digital color management standards, a development expected to raise professional installation quality benchmarks globally and support premium product uptake.

The Vehicle Wrap Film Market exhibits pronounced regional heterogeneity in both growth velocity and demand structure, reflecting divergent levels of advertising market maturity, fleet modernization investment, and consumer customization culture.

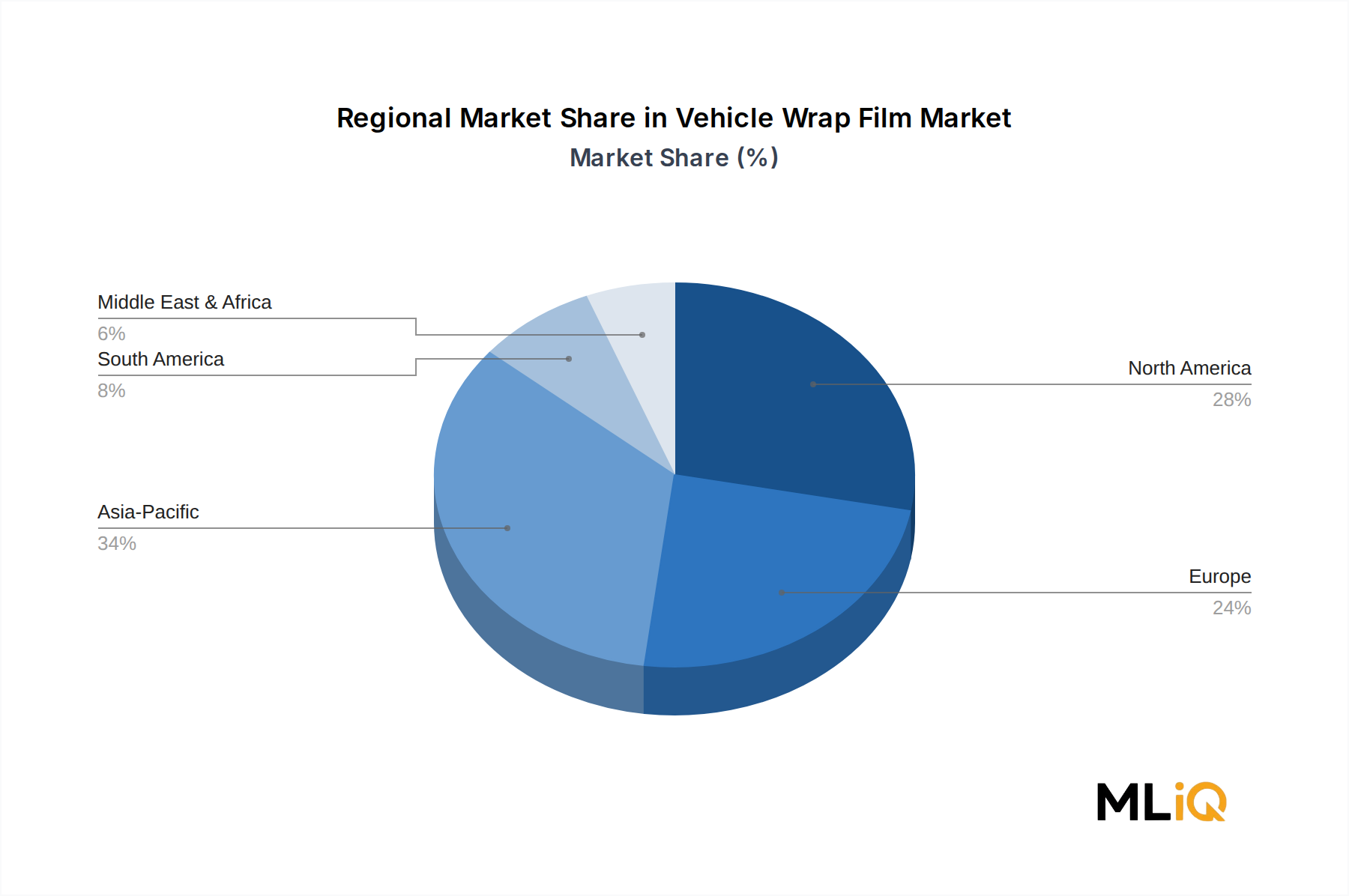

North America represents the largest single regional market by absolute revenue, accounting for an estimated 35% of global market value. The United States anchors this position through a mature fleet graphics industry, a robust DIY customization culture, and a dense network of professional wrap installers. Regulatory certainty and high per-vehicle wrap spending support premium pricing. The region's CAGR over the forecast period is projected at approximately 16%, reflecting relative market maturity but sustained organic growth from EV fleet expansion and e-commerce logistics fleet branding.

Europe constitutes the second-largest regional market, with Germany, the United Kingdom, and France representing the primary national markets. European demand is partly driven by stringent vehicle conspicuity regulations for commercial vehicles, which create a compliance-driven floor for certain wrap film specifications. The region's CAGR is estimated at 15–17%, supported by sustainability-oriented product innovation and the ongoing transition of commercial fleets to electric powertrains.

Asia Pacific is the fastest-growing regional market, with a projected CAGR exceeding 22% over the forecast horizon. China is the dominant market within the region, combining a massive automotive fleet, rapidly growing e-commerce logistics infrastructure, and a burgeoning premium vehicle customization culture in tier-one and tier-two cities. India represents the highest-velocity emerging sub-market, where fleet wrap advertising is gaining traction as a cost-effective alternative to static billboard media. Japan and South Korea contribute premium product demand driven by sophisticated automotive aesthetics culture.

The Middle East and Africa region, while smaller in absolute terms, is exhibiting above-average growth rates—estimated at 18–20% CAGR—supported by Gulf Cooperation Council commercial fleet expansion and rising advertising adoption among regional logistics operators. South America, led by Brazil and Argentina, represents a developing market where price sensitivity constrains premium product penetration but overall volume growth remains positive at an estimated CAGR of 14–16%.

The Vehicle Wrap Film Market is deeply integrated into global trade networks, with manufacturing capacity concentrated in a small number of hub regions and consumption distributed across over one hundred national markets. Understanding trade flow dynamics is essential for assessing supply chain resilience and competitive positioning.

China is the dominant exporting nation for calendered and mid-grade cast vinyl wrap films, with manufacturers in the Guangdong, Zhejiang, and Jiangsu provinces collectively accounting for an estimated 45–50% of global wrap film export volume by weight. These manufacturers serve price-sensitive markets across Southeast Asia, the Middle East, Africa, and Latin America, and increasingly compete in lower-tier segments of the North American and European markets through e-commerce channels. The competitive cost structure of Chinese manufacturers is underpinned by vertically integrated PVC compounding capacity and proximity to plasticizer and adhesive raw material suppliers.

Europe—specifically Germany, France, and the UK—is both a significant manufacturing and re-export hub for premium cast wrap films. European-manufactured products command price premiums in export markets due to perceived quality differentiation and brand heritage. Intra-European trade flows are facilitated by harmonized regulatory standards under EU single market provisions.

The United States imports significant volumes of wrap film from both Asian and European sources, primarily for distribution through professional installer networks and retail channels. U.S. import tariffs on PVC film products from China, which were elevated under Section 301 trade actions and maintained under subsequent trade policy frameworks, have incentivized some procurement diversification toward South Korean, Japanese, and European suppliers, though Chinese-origin products remain price-competitive in volume segments.

In the Asia Pacific region, South Korea and Japan are net exporters of high-performance wrap film components including specialty adhesive layers and UV-stabilized topcoat films, reflecting their advanced materials science ecosystems. ASEAN nations, particularly Malaysia and Thailand, are emerging as secondary manufacturing

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 19.4% from 2020-2034 |

| Segmentation |

|

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Comprehensive validation mechanisms ensuring market intelligence accuracy, reliability, and adherence to international standards.

500+ data sources cross-validated

200+ industry specialists validation

NAICS, SIC, ISIC, TRBC standards

Continuous market tracking updates

Factors such as are projected to boost the Vehicle Wrap Film Market market expansion.

Key companies in the market include Fedrigoni S.P.A, KPMF, Guangzhou Carbins Film Co., LTD, Avery Dennison Corporation, JMR Graphics, Vvivid Vinyl, 3M, Arlon Graphics LLC., Hexis S.A.S., ORAFOL Europe GmbH..

The market segments include Film Type, Vehicle Type, Application.

The market size is estimated to be USD 9.98 billion as of 2022.

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3200, USD 4650, and USD 7789 respectively.

The market size is provided in terms of value, measured in billion and volume, measured in .

Yes, the market keyword associated with the report is "Vehicle Wrap Film Market," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Vehicle Wrap Film Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.