1. What are the major growth drivers for the Automotive Ambient Lighting Market market?

Factors such as are projected to boost the Automotive Ambient Lighting Market market expansion.

+1 2315155523

Automotive Ambient Lighting Market

Automotive Ambient Lighting Market

Market Lens IQ is a global market intelligence and strategic consulting firm delivering advanced syndicated research reports, customized industry analysis, competitive intelligence, and data-driven advisory solutions to organizations across international markets. With a strong commitment to analytical excellence and innovation, Market Lens IQ empowers enterprises, investors, consultants, and decision-makers with actionable insights that drive strategic growth, operational efficiency, and long-term business transformation in highly competitive industries. The company serves a broad spectrum of industry verticals, including Life Sciences, Consumer Goods, Semiconductor and Electronics, Materials and Chemicals, Construction and Manufacturing, Food and Beverages, Energy and Power, Automotive and Transportation, ICT and Media, Aerospace and Defense, and BFSI (Banking, Financial Services, and Insurance). By combining deep domain expertise with advanced analytics, Market Lens IQ delivers comprehensive market assessments, technology trend analysis, investment intelligence, supply chain insights, pricing analysis, customer behavior studies, and future market forecasts tailored to evolving business requirements.

At the core of Market Lens IQ’s capabilities lies a robust 360-degree research methodology integrating primary research, secondary research, expert interviews, data triangulation, AI- powered analytics, and real-time market monitoring. Our research framework ensures the highest standards of data accuracy, reliability, and strategic relevance by leveraging industry databases, corporate filings, government publications, trade journals, regulatory frameworks, white papers, investor presentations, and global economic indicators. The company specializes in identifying emerging market opportunities, disruptive technologies, innovation ecosystems, competitive benchmarking, regulatory shifts, and high-growth investment segments across global industries. Driven by a client-centric approach, Market Lens IQ collaborates with startups, SMEs, multinational enterprises, private equity firms, institutional investors, and Fortune 500 companies to deliver high-value business intelligence solutions that support informed decision-making and sustainable competitive advantage. Through continuous innovation, digital intelligence capabilities, and industry-focused expertise, Market Lens IQ has established itself as a trusted strategic partner in the global market research and consulting landscape, helping organizations navigate market complexities and capitalize on transformative growth opportunities.

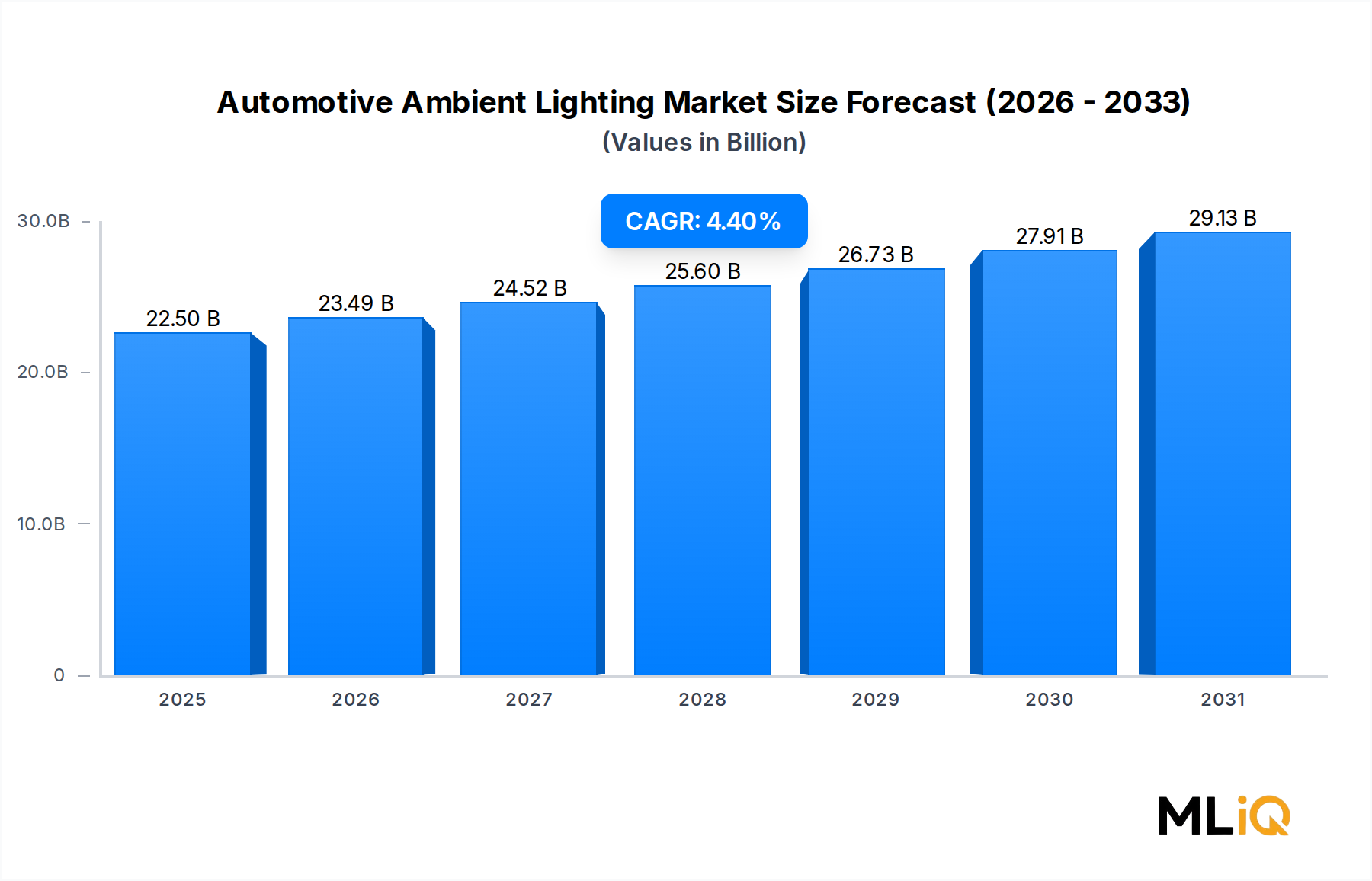

The global Automotive Ambient Lighting Market was valued at $22.5 billion in 2023 and is projected to expand at a compound annual growth rate (CAGR) of 4.4% through the forecast period, reflecting persistent consumer appetite for elevated in-cabin experiences and escalating OEM investment in vehicle personalization. As automakers pivot toward differentiated interior architectures to justify premium pricing, ambient lighting has transitioned from a discretionary luxury feature to a near-standard specification across mid-range and premium vehicle segments worldwide.

Several structural demand catalysts underpin this trajectory. First, the rapid proliferation of battery electric vehicles (BEVs) and hybrid electric vehicles (HEVs) is reshaping interior design philosophy. Without traditional powertrain constraints on cabin packaging, EV manufacturers have dramatically expanded usable interior real estate, making ambient lighting a central aesthetic and functional tool. Second, consumer expectations—shaped heavily by high-definition digital interfaces in smartphones and smart home devices—have migrated into automotive interiors, driving automakers to deploy multi-zone, color-tunable LED strips capable of displaying millions of hues synchronized with infotainment cues, navigation prompts, and safety alerts.

On the technology front, the shift from halogen and xenon-based accent sources toward full-spectrum LED architectures is nearly complete in new vehicle programs. LED-based systems offer superior energy efficiency, a lifespan exceeding 50,000 hours, and the programmability required for dynamic, software-defined lighting experiences. Integration with Advanced Driver-Assistance Systems (ADAS) and heads-up displays further elevates the functional role of ambient lighting beyond mere aesthetics.

Geographically, Asia Pacific leads in volume output—driven predominantly by China's formidable domestic OEM ecosystem and India's rapidly expanding passenger vehicle fleet—while Europe commands the highest revenue intensity per vehicle, reflecting the region's concentration of premium and luxury automotive brands. North America presents a balanced growth profile, with electrification mandates and consumer premiumization trends converging to support sustained market expansion.

Looking ahead, the market's forward outlook is shaped by three converging forces: the deepening integration of ambient lighting within Software-Defined Vehicle (SDV) architectures, the standardization of multi-zone dynamic systems across volume segments (not just luxury tiers), and the increasing use of ambient light as a human-machine interface (HMI) modality for communicating vehicle states—such as charging status, autonomous driving mode engagement, and proximity alerts. Together, these forces suggest the market will sustain above-average growth momentum well beyond the near-term horizon.

Among all technology segments within the Automotive Ambient Lighting Market—halogen, LED, and xenon—LED technology commands by far the largest revenue share and exhibits the strongest forward momentum. This dominance is attributable to a convergence of technical superiority, economic practicality, and regulatory alignment that collectively renders legacy lighting technologies increasingly obsolete for interior ambient applications.

LED systems offer a combination of attributes that halogen and xenon solutions fundamentally cannot replicate at competitive price points. Their compact form factor allows integration into millimeter-thin door panel trims, instrument panel bezels, footwells, and center console profiles without structural compromise. Color rendering capabilities span virtually the entire visible spectrum—enabling OEMs to offer multi-million color palettes through PWM (pulse-width modulation) and RGB mixing—while halogen sources are constrained to a narrow warm-white output and xenon systems remain impractical for low-voltage, high-frequency switching applications characteristic of ambient interior use.

From an energy consumption perspective, LED ambient lighting systems draw between 3W and 15W per vehicle depending on zone count and luminosity settings, compared to equivalent halogen setups that can consume 30–50% more power for comparable lumen output. In the context of BEV range optimization, this efficiency differential has made LED the de facto standard across virtually all new EV platforms entering production after 2020.

The cost trajectory of LED components has further reinforced the segment's dominance. Average LED chip prices declined at roughly 8–10% per annum during the 2015–2022 period, driven by scale efficiencies in Asian semiconductor manufacturing and improvements in epitaxial wafer yields. While price declines have moderated since 2022 due to supply chain normalization and raw material cost pressures, LEDs remain significantly more cost-effective on a total-cost-of-ownership basis when factoring in reduced replacement frequency and lower warranty exposure.

Key players operating prominently within the LED segment include HELLA KGaA Hueck & Co., which has developed proprietary LED ambient lighting modules for several European OEM platforms; Osram Licht AG, a global leader in automotive-grade LED packages supplying both OEM and aftermarket channels; Valeo SA, whose ambient lighting systems integrate directly with its broader HMI product portfolio; and Koito Manufacturing Co. Ltd., which leverages its strong position in Japanese OEM supply chains to drive LED ambient module adoption in Asia Pacific markets.

The LED segment's share is not merely holding steady—it is actively consolidating. As OEMs phase out halogen interior lighting from new model introductions and xenon remains confined to headlamp applications, the competitive battleground within ambient lighting has effectively become an intra-LED competition: who can deliver the most sophisticated, software-integrated, cost-optimized LED ambient system at scale. This dynamic favors vertically integrated suppliers with in-house semiconductor capabilities and robust software engineering teams capable of supporting SDV integration requirements.

Further reinforcing LED dominance, regulatory frameworks in Europe and increasingly in Asia are tightening energy efficiency requirements for vehicle subsystems, effectively creating structural headwinds for less-efficient lighting technologies. The European Union's ongoing vehicle energy management directives and China's New Energy Vehicle (NEV) technical standards both contain provisions that favor low-power, high-efficiency interior lighting architectures—directly benefiting LED-based ambient systems.

The Automotive Ambient Lighting Market is propelled by a set of quantifiable structural drivers while simultaneously navigating a distinct set of supply-side and macro-level constraints that modulate growth velocity.

Drivers:

The electrification of the global vehicle fleet is the single most powerful demand accelerator. Global BEV sales surpassed 10 million units in 2022 and exceeded 14 million units in 2023, according to industry tracking data. EV interiors, freed from combustion powertrain packaging constraints, incorporate significantly more ambient lighting zones—averaging 8–12 zones per vehicle versus 4–6 zones in comparable ICE platforms—directly expanding per-vehicle ambient lighting content value.

Consumer willingness to pay for interior personalization features is measurably increasing. Surveys across North American and European markets indicate that more than 60% of new car buyers under the age of 45 rank interior ambient lighting among their top five desired features, a preference that OEMs have translated into option packages ranging from $300 to $1,200 per vehicle in the premium segment.

The integration of ambient lighting with ADAS and safety alert systems—using color-coded light cues to signal lane departure warnings, forward collision alerts, and autonomous mode status—has elevated ambient lighting from a cosmetic to a functional safety specification, broadening its adoption mandate beyond luxury tiers.

Constraints:

Semiconductor supply volatility remains a material constraint. The 2020–2022 global chip shortage disrupted ambient lighting module production schedules across multiple OEM platforms, delaying vehicle launches and compressing supplier margins. While supply conditions normalized through 2023–2024, structural dependencies on a limited number of LED driver IC fabricators introduce ongoing concentration risk.

Raw material cost inflation—particularly for rare earth phosphors used in LED white-light conversion and copper used in wiring harnesses—has exerted upward cost pressure on ambient lighting system bill-of-materials since 2021, partially offsetting margin gains from volume scale. This dynamic directly connects the Automotive Ambient Lighting Market to broader trends in the Automotive LED Lighting Market and the LED Driver IC Market.

The competitive landscape of the Automotive Ambient Lighting Market is characterized by a mix of diversified automotive lighting specialists, Tier 1 interior systems integrators, and global electronics conglomerates. The following profiles summarize strategic positioning across the key players:

HELLA KGaA Hueck & Co.: A leading Tier 1 automotive lighting and electronics supplier headquartered in Germany, HELLA has developed an integrated ambient lighting portfolio spanning fiber optic, RGB LED, and OLED-based interior solutions, supplying major European OEM programs including Volkswagen Group and BMW platforms.

Grupo Antolin: A global automotive interior systems specialist, Grupo Antolin embeds ambient lighting directly into headliner, door panel, and overhead console assemblies, offering OEMs fully integrated lighting-structure modules that reduce assembly complexity and weight.

Koito Manufacturing Co. Ltd.: Japan's dominant automotive lighting manufacturer, Koito leverages deep relationships with Toyota, Honda, and other Japanese OEMs to supply interior ambient lighting systems alongside its core headlamp business, with growing penetration in Chinese joint venture platforms.

Dräxlmaier Group: A privately held German automotive supplier specializing in vehicle electrical systems and interior components, Dräxlmaier integrates ambient lighting within its wiring harness and interior trim assemblies, offering turnkey cabin illumination solutions for luxury OEMs including BMW and Rolls-Royce.

Valeo SA: A French multinational Tier 1 supplier, Valeo's ambient lighting systems are tightly integrated with its HMI and driver assistance technology portfolios, enabling dynamic lighting responses triggered by ADAS events and infotainment states.

Robert Bosch GmbH: As a global automotive technology leader, Bosch contributes ambient lighting system intelligence through its vehicle electronics and connected mobility divisions, with particular emphasis on software-defined lighting control modules for SDV architectures.

Philips: Operating through its automotive lighting division, Philips supplies high-performance LED packages and ambient light engines used by multiple Tier 1 assemblers, with a brand presence that extends into the premium aftermarket segment.

Stanley Electric Co. Ltd.: A Japanese specialty lighting manufacturer, Stanley Electric supplies interior LED ambient modules to domestic and international OEM customers, with competitive strength in compact, high-efficiency LED arrays designed for space-constrained cabin applications.

General Electric: Through its specialty lighting and advanced materials divisions, General Electric contributes component-level technologies—including phosphor formulations and LED substrates—that feed into automotive ambient lighting supply chains.

Osram Licht AG: A global photonics and semiconductor lighting leader, Osram supplies automotive-grade LED chips, laser sources, and smart lighting ICs that serve as foundational components for ambient lighting systems across the Tier 1 supplier ecosystem.

January 2023: HELLA KGaA Hueck & Co. announced the series launch of its next-generation multi-zone RGB ambient lighting system on a new European premium OEM platform, featuring 64-color dynamic mode capability synchronized with the vehicle's digital cockpit software.

March 2023: Valeo SA unveiled its "IntelliLighting" interior concept at the Geneva Motor Show, demonstrating ADAS-reactive ambient lighting that shifts color and intensity in real time based on forward collision warning sensor inputs.

June 2023: Osram Licht AG disclosed a supply agreement with two major Chinese NEV manufacturers to provide high-density LED ambient light engines for BEV interior programs entering production in 2024, reinforcing its Asia Pacific revenue diversification strategy.

September 2023: Grupo Antolin received a sourcing nomination from a North American OEM for an integrated ambient lighting headliner module spanning six independent lighting zones, with production scheduled to begin in 2025.

November 2023: Koito Manufacturing Co. Ltd. announced a capital investment of approximately ¥8 billion in its interior lighting division to expand LED module production capacity in Japan and Vietnam in anticipation of rising demand from electrification-driven content growth.

February 2024: Dräxlmaier Group revealed a collaboration with a European semiconductor firm to co-develop an automotive-grade microcontroller specifically optimized for real-time ambient lighting animation rendering in SDV architectures, targeting 2026 vehicle model year programs.

April 2024: Robert Bosch GmbH integrated ambient lighting control into its latest generation vehicle domain controller, enabling centralized, over-the-air-updatable ambient lighting management without discrete lighting ECUs—a move seen as a significant cost-reduction enabler for mass-market vehicle programs.

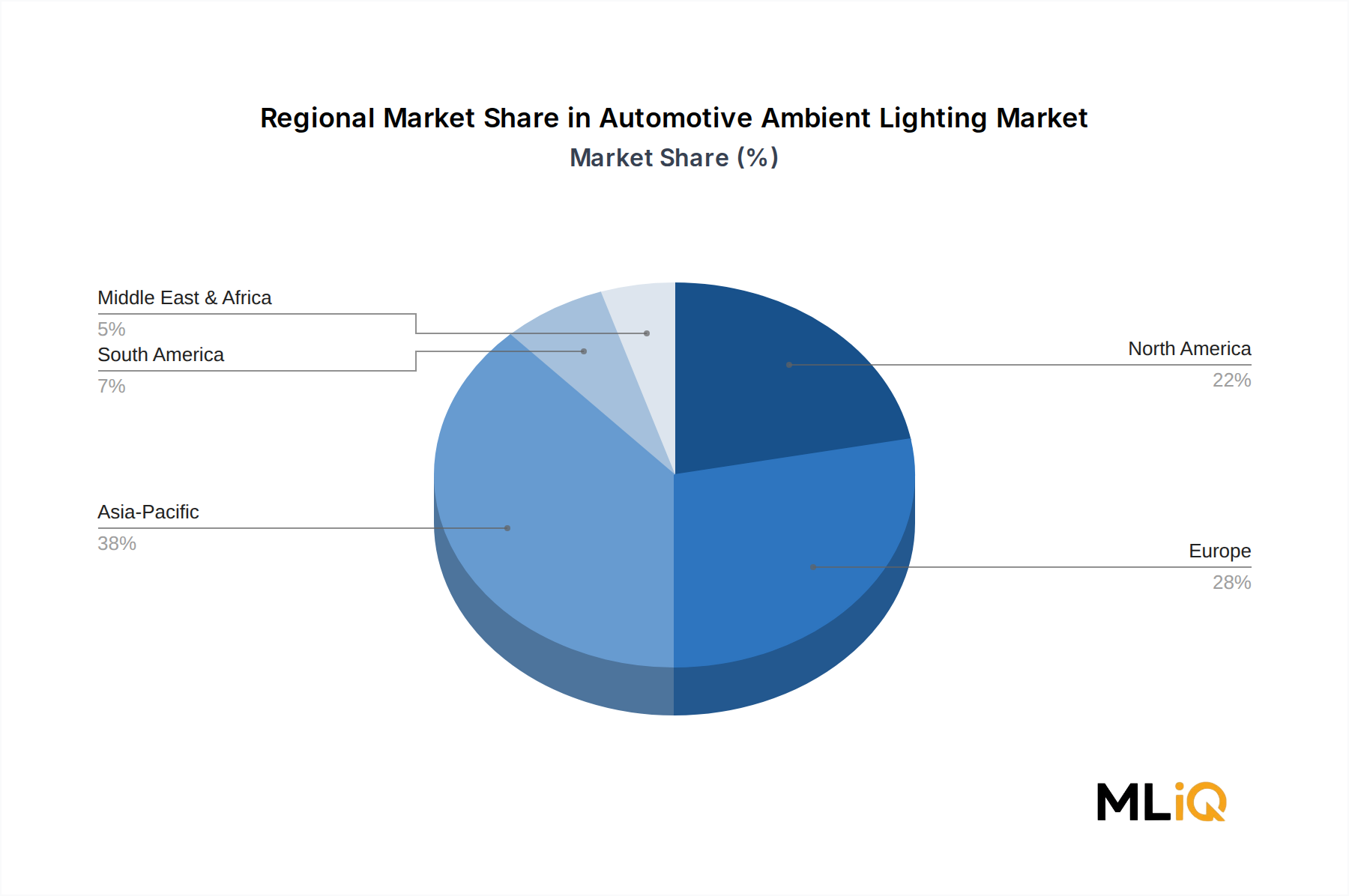

The Automotive Ambient Lighting Market exhibits pronounced regional differentiation across growth rates, revenue intensity, and demand drivers, with five major geographies meriting detailed analysis.

Asia Pacific is the largest regional market by volume and the fastest-growing geography, driven primarily by China's position as the world's largest single automotive market and its aggressive NEV transition policy. China alone accounted for more than 35% of global new vehicle sales with ambient lighting content in 2023, supported by domestic NEV mandates and the competitive intensity among Chinese EV brands—including BYD, NIO, and Li Auto—who deploy elaborate multi-zone ambient lighting as a core differentiation tool. The Asia Pacific region is estimated to sustain a CAGR in the range of 5.8–6.2% through the forecast period. India represents an emerging high-growth sub-market as domestic OEMs and international joint ventures accelerate cabin premiumization in the rapidly growing mid-size SUV segment.

Europe represents the highest revenue-per-vehicle intensity, reflecting the concentration of luxury and premium OEM programs in Germany, the United Kingdom, and Sweden. German automakers—BMW, Mercedes-Benz, Volkswagen Group—have been among the earliest and most aggressive deployers of multi-zone ambient lighting, averaging 8–10 zones per vehicle across their mid-range and above lineups. European regional growth is estimated at a CAGR of approximately 4.1%, moderated by relative market maturity and high existing penetration rates in the premium tier.

North America occupies a balanced growth position, with the United States driving the bulk of regional demand through its large SUV and pickup truck segments, which increasingly offer ambient lighting as a standard or near-standard feature in mid-trim configurations. Electrification mandates across multiple U.S. states and the Inflation Reduction Act's incentive structure for domestic EV production are expected to accelerate content expansion. North American CAGR is estimated at approximately 4.5%.

Middle East & Africa represents a smaller but structurally interesting sub-market, where Gulf Cooperation Council (GCC) nations exhibit disproportionately high per-capita luxury vehicle purchase rates, creating above-average ambient lighting content demand among a concentrated consumer base. Growth in this region is estimated at a CAGR of 3.8–4.2%.

South America remains the least penetrated major region, with Brazil and Argentina as the primary markets. Cost sensitivity and a vehicle mix weighted toward entry-level segments constrain near-term penetration rates, though gradual premiumization trends support a long-term CAGR of approximately 3.2%.

The Automotive Ambient Lighting Market's supply chain is a multi-tier ecosystem spanning semiconductor fabrication, rare earth mineral extraction, precision polymer compounding, and complex electronics assembly—each tier carrying distinct sourcing risk profiles and price volatility characteristics.

At the upstream level, LED chips and driver ICs represent the most strategically critical inputs. LED chip production is heavily concentrated in Taiwan, China, and South Korea, with companies such as Epistar, San'an Optoelectronics, and Cree (now Wolfspeed) accounting for a substantial share of global automotive-grade LED wafer output. This geographic concentration creates single-source dependency risks, as demonstrated during the 2020–2022 semiconductor shortage, which forced multiple Tier 1 ambient lighting suppliers to delay program launches and absorb expedite freight premiums that compressed gross margins by an estimated 150–300 basis points.

Rare earth phosphors—particularly cerium, terbium, and europium compounds—are essential for white LED production through photoluminescent down-conversion. China controls approximately 60–70% of global rare earth refining capacity

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.4% from 2020-2034 |

| Segmentation |

|

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Comprehensive validation mechanisms ensuring market intelligence accuracy, reliability, and adherence to international standards.

500+ data sources cross-validated

200+ industry specialists validation

NAICS, SIC, ISIC, TRBC standards

Continuous market tracking updates

Factors such as are projected to boost the Automotive Ambient Lighting Market market expansion.

Key companies in the market include HELLA KGaA Hueck & Co., Grupo Antolin, Koito Manufacturing Co. Ltd., Dräxlmaier Group, Valeo SA, Robert Bosch GmbH, Philips, Stanley Electric Co. Ltd., General Electric, Osram Licht AG.

The market segments include Product Type, Technology, Vehicle Type, Fuel Type, Application.

The market size is estimated to be USD 22.5 billion as of 2022.

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3690, USD 5820, and USD 9870 respectively.

The market size is provided in terms of value, measured in billion and volume, measured in .

Yes, the market keyword associated with the report is "Automotive Ambient Lighting Market," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Automotive Ambient Lighting Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.