1. What are the major growth drivers for the Automotive Terminal Market market?

Factors such as are projected to boost the Automotive Terminal Market market expansion.

+1 2315155523

Market Lens IQ is a global market intelligence and strategic consulting firm delivering advanced syndicated research reports, customized industry analysis, competitive intelligence, and data-driven advisory solutions to organizations across international markets. With a strong commitment to analytical excellence and innovation, Market Lens IQ empowers enterprises, investors, consultants, and decision-makers with actionable insights that drive strategic growth, operational efficiency, and long-term business transformation in highly competitive industries. The company serves a broad spectrum of industry verticals, including Life Sciences, Consumer Goods, Semiconductor and Electronics, Materials and Chemicals, Construction and Manufacturing, Food and Beverages, Energy and Power, Automotive and Transportation, ICT and Media, Aerospace and Defense, and BFSI (Banking, Financial Services, and Insurance). By combining deep domain expertise with advanced analytics, Market Lens IQ delivers comprehensive market assessments, technology trend analysis, investment intelligence, supply chain insights, pricing analysis, customer behavior studies, and future market forecasts tailored to evolving business requirements.

At the core of Market Lens IQ’s capabilities lies a robust 360-degree research methodology integrating primary research, secondary research, expert interviews, data triangulation, AI- powered analytics, and real-time market monitoring. Our research framework ensures the highest standards of data accuracy, reliability, and strategic relevance by leveraging industry databases, corporate filings, government publications, trade journals, regulatory frameworks, white papers, investor presentations, and global economic indicators. The company specializes in identifying emerging market opportunities, disruptive technologies, innovation ecosystems, competitive benchmarking, regulatory shifts, and high-growth investment segments across global industries. Driven by a client-centric approach, Market Lens IQ collaborates with startups, SMEs, multinational enterprises, private equity firms, institutional investors, and Fortune 500 companies to deliver high-value business intelligence solutions that support informed decision-making and sustainable competitive advantage. Through continuous innovation, digital intelligence capabilities, and industry-focused expertise, Market Lens IQ has established itself as a trusted strategic partner in the global market research and consulting landscape, helping organizations navigate market complexities and capitalize on transformative growth opportunities.

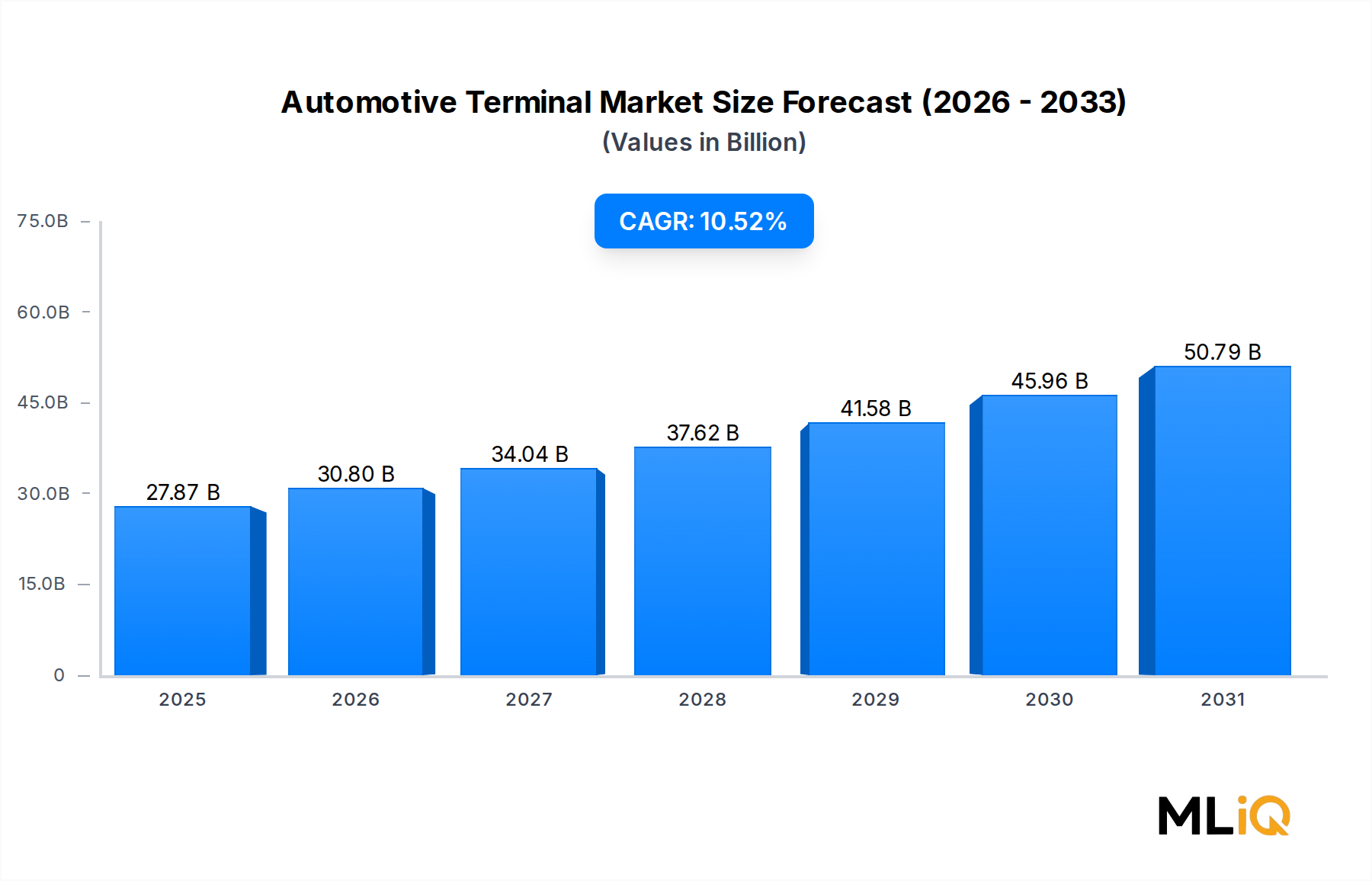

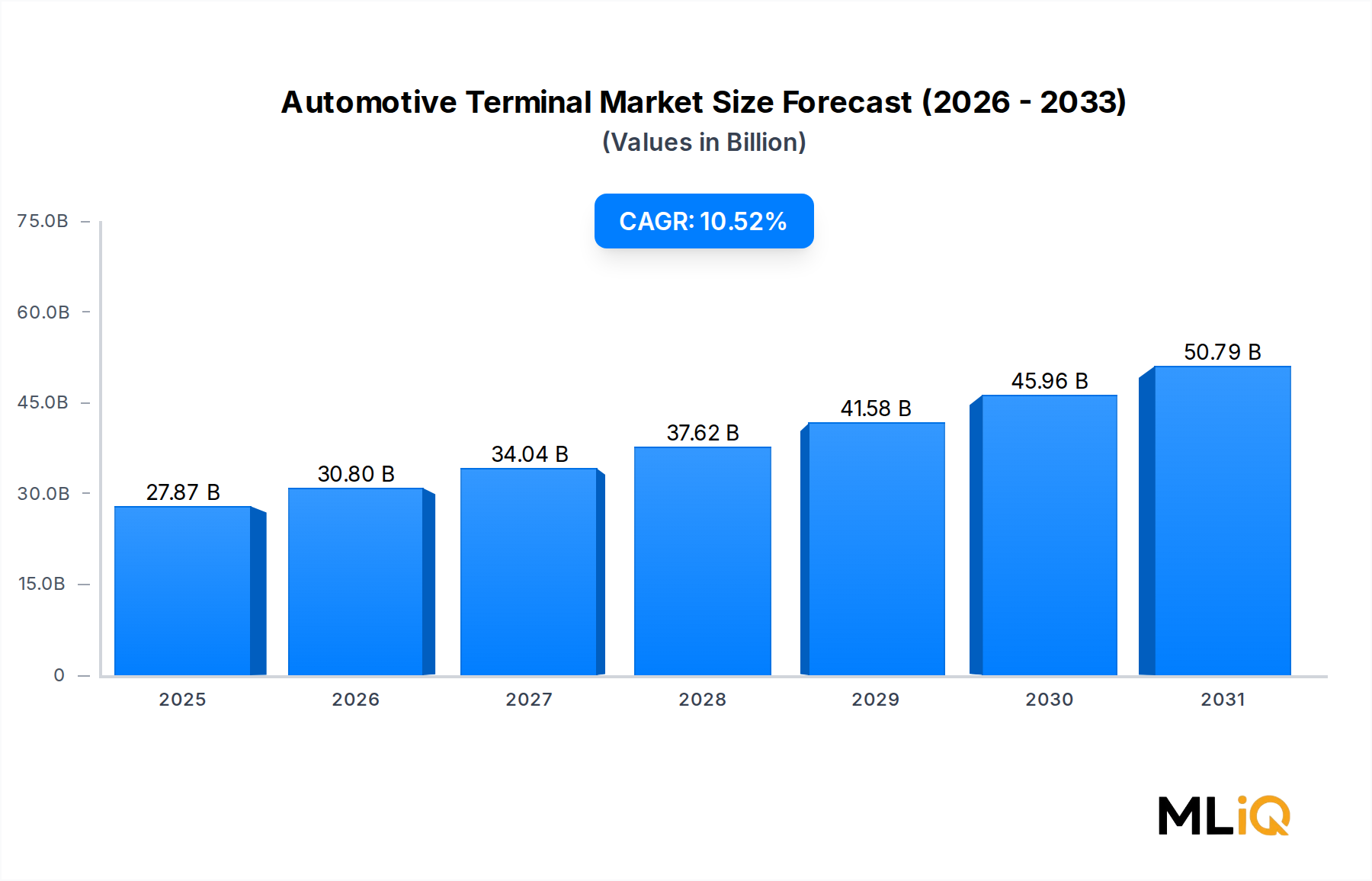

The global Automotive Terminal Market was valued at $27.87 billion in 2024 and is projected to expand at a compound annual growth rate (CAGR) of 10.52% through 2033, reflecting one of the most robust growth trajectories across the broader automotive components sector. This momentum is driven by an accelerating shift toward vehicle electrification, mounting complexity in in-vehicle electrical architectures, and increasingly stringent safety and emissions regulations across major economies.

Automotive terminals — encompassing crimp terminals, ring terminals, blade terminals, and butt connectors — serve as the fundamental interface between wiring harnesses and electrical subsystems. As modern vehicles integrate advanced driver-assistance systems (ADAS), infotainment platforms, and battery management units, the density of terminal connections per vehicle is rising sharply. A conventional internal combustion engine (ICE) vehicle typically contains between 1,500 and 2,500 electrical connections; a fully electric vehicle (EV) can require 3,000 or more, substantially expanding the total addressable market per unit produced.

Macroeconomic tailwinds reinforcing this expansion include government mandates for zero-emission vehicles in Europe, China, and North America, sustained growth in global vehicle production volumes — particularly in the Asia Pacific corridor — and the proliferation of 48-volt mild-hybrid architectures in commercial fleets. These factors are collectively amplifying per-vehicle terminal content, creating a durable demand floor even in years where overall vehicle production growth decelerates.

From a segmentation standpoint, current rating categories — particularly the below-40-ampere and 41-to-100-ampere bands — account for the majority of unit volumes, serving low-voltage signaling and sensor circuits. However, the above-100-ampere high-current segment is the fastest-growing sub-category, propelled by high-power battery interconnects and DC fast-charging architectures in electric vehicles.

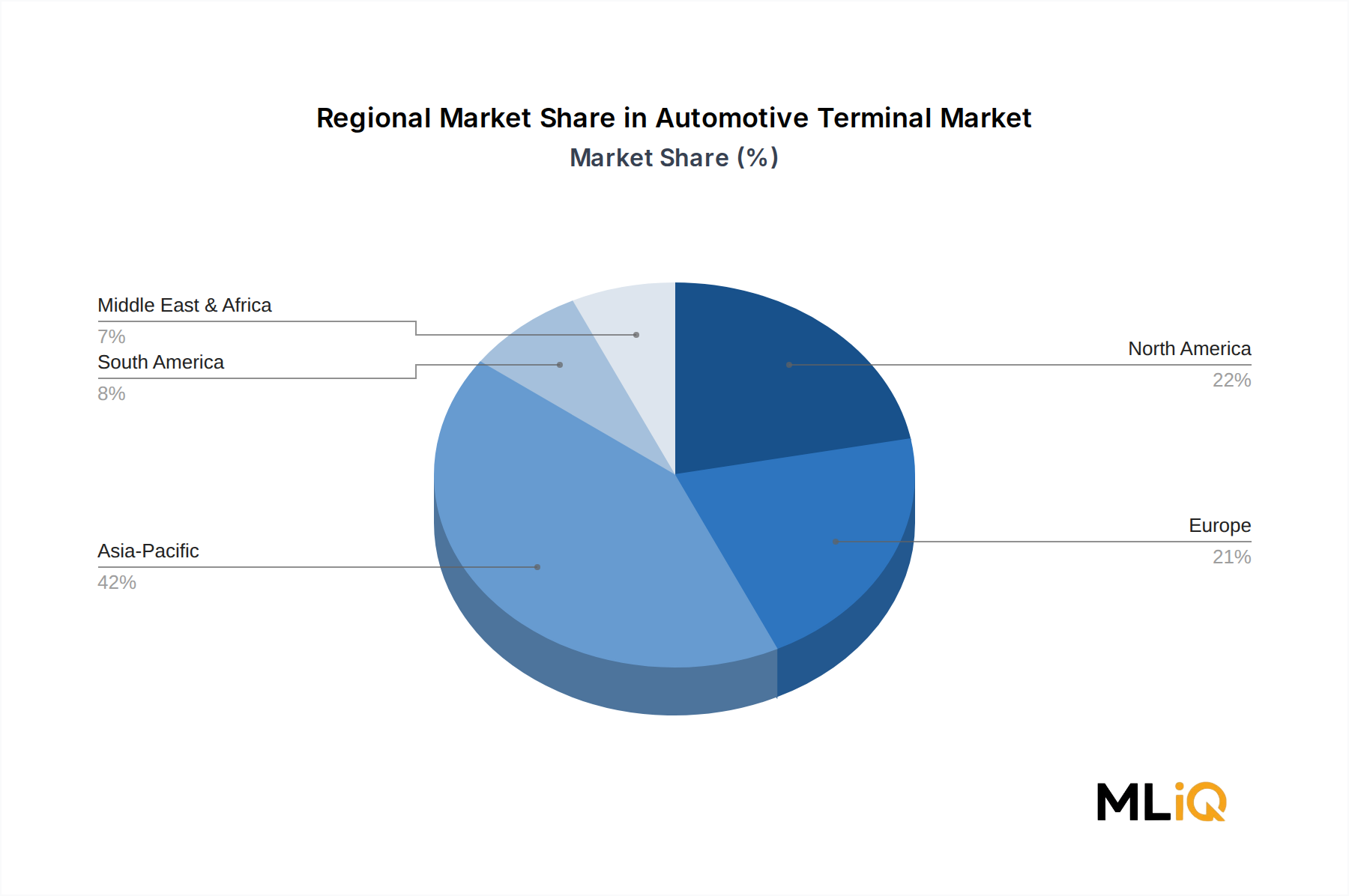

Geographically, Asia Pacific dominates both production and consumption, accounting for an estimated 47% of global market revenue in 2024, with China and India leading demand generation. North America and Europe represent the next significant revenue pools, with reshoring trends and nearshoring of EV supply chains accelerating capacity additions in both regions.

Looking ahead to 2033, the market is expected to surpass $70 billion, driven by the convergence of electrification mandates, software-defined vehicle platforms demanding denser electrical connectivity, and the gradual mass-market penetration of autonomous driving technologies. Companies that can deliver thermally robust, high-current-capable, and miniaturized terminal solutions will be best positioned to capture disproportionate value in this expanding ecosystem.

Within the vehicle-type segmentation of the Automotive Terminal Market, the passenger cars sub-segment commands the largest revenue share, estimated at approximately 58% of total global market value in 2024. This dominance is structural rather than cyclical, rooted in the sheer volume of passenger cars produced globally — exceeding 70 million units annually in pre-disruption years — combined with the exponentially rising electrical content per vehicle driven by electrification, connectivity, and autonomy trends.

Passenger vehicles today bear the most complex electrical architectures among all vehicle categories. A contemporary mid-segment sedan integrates upwards of 100 electronic control units (ECUs), each requiring multiple terminal-based interconnects for power delivery, signal transmission, and grounding. Premium and electric passenger vehicles can carry 150–200 ECUs, further compounding terminal density. The net effect is that terminal bill-of-materials (BOM) content per passenger vehicle has grown at an estimated 6–8% annually in value terms over the past five years, independent of broader vehicle volume growth.

The transition from 12-volt to 48-volt and full high-voltage (400V/800V) architectures in battery electric vehicles (BEVs) is particularly consequential for this segment. High-voltage terminals require advanced materials — silver-plated copper contacts, specialized polymer housings rated for elevated thermal and chemical environments — that carry significantly higher per-unit ASPs (average selling prices) than conventional low-voltage alternatives. This ASP inflation is a key structural driver supporting market value expansion even during periods of flat vehicle unit sales.

Key players competing aggressively for leadership in the passenger car sub-segment include Hitachi Ltd., TOSHIBA CORPORATION, and Siemens, all of which have invested in R&D facilities dedicated to next-generation connector and terminal systems optimized for EV platforms. Hitachi's automotive systems division, for instance, has articulated a clear strategic priority around high-voltage terminal and connector assemblies aligned with its broader EV components roadmap.

Alstom and Wabtec Corporation, while more traditionally associated with rail transit electrical systems, have leveraged their high-current terminal expertise to address crossover opportunities in commercial EV charging infrastructure and heavy-duty electric bus segments — both of which share terminal specification overlaps with passenger EV platforms.

The segment's share is consolidating around a smaller number of Tier 1 suppliers capable of delivering fully integrated terminal-harness sub-assemblies rather than standalone terminal components. Original equipment manufacturers (OEMs) are increasingly awarding integrated electrical architecture contracts to reduce assembly complexity, which means that standalone terminal suppliers must either partner with harness integrators or vertically expand their capabilities.

Looking forward, the passenger car sub-segment's dominance is expected to persist through 2033, reinforced by the global EV ramp. However, its share of total market revenue may modestly compress from 58% to approximately 53–55% as heavy commercial vehicles and light commercial vehicles gain share through electrification of logistics fleets and last-mile delivery platforms — both of which are attracting significant OEM investment and government subsidy support across Europe and China.

Product innovation within this sub-segment is centering on ultra-compact, high-pin-density terminal systems capable of withstanding vibration, thermal cycling, and corrosive environments — critical for under-hood and underbody installation in EVs. Manufacturers investing in automated terminal crimping and quality verification technologies are gaining competitive advantage through yield improvement and defect rate reduction at scale.

The Automotive Terminal Market is shaped by a set of well-quantified demand drivers and structural constraints that collectively define its growth trajectory through 2033.

Driver 1 — EV Proliferation and High-Voltage Architecture Adoption: Global battery electric vehicle sales reached approximately 14 million units in 2023, representing a 35% year-over-year increase. Each BEV requires terminals capable of handling 400V to 800V systems, driving per-vehicle terminal ASP substantially above ICE vehicle equivalents. The International Energy Agency projects EV penetration to reach 40% of new vehicle sales globally by 2030, representing a structural, multi-year demand catalyst.

Driver 2 — ADAS and Connected Vehicle Electronics Density: Modern vehicles deploying Level 2+ ADAS capabilities incorporate radar, LiDAR, ultrasonic, and camera sensor arrays, each requiring dedicated wiring and terminal connections. The average ADAS sensor count per premium vehicle grew from 6 in 2018 to over 20 in 2024, directly expanding terminal volume per unit. This is closely tied to growth in the Automotive Sensor Market, which serves as both a direct demand driver and a co-expanding ecosystem.

Driver 3 — Commercial Vehicle Fleet Electrification: Light commercial vehicle electrification, driven by last-mile logistics operators and municipal fleet mandates in Europe and China, is amplifying terminal demand in a segment that previously had low electrical content intensity.

Constraint 1 — Raw Material Price Volatility: Copper — the dominant conductive material in automotive terminals — experienced price fluctuations ranging from $7,500 to $10,500 per metric ton between 2021 and 2024. This volatility directly pressures terminal manufacturer margins, particularly for long-term supply contracts with fixed pricing. The dynamics of the Copper Wire and Cable Market remain a persistent headwind for cost stability.

Constraint 2 — Skilled Labor Scarcity in Terminal Assembly: Despite automation advances, precision terminal crimping and quality inspection still require skilled technicians, and labor shortages in key manufacturing geographies — notably Eastern Europe and Southeast Asia — are inflating operational costs.

Constraint 3 — Miniaturization and Material Complexity: As terminal form factors shrink to accommodate space-constrained EV platforms, manufacturing tolerances tighten, increasing scrap rates and tooling investment requirements.

The Automotive Terminal Market features a mix of diversified industrial conglomerates and specialized electrical systems providers. The competitive intensity is high, with players differentiating on material science innovation, manufacturing scale, and systems integration capability.

Hitachi Ltd.: A diversified Japanese industrial conglomerate with a robust automotive systems division; Hitachi has strategically prioritized high-voltage terminal and connector assemblies aligned with its EV powertrain components portfolio, investing significantly in Japanese and European R&D centers.

Bharat Heavy Electricals Limited: An Indian state-owned enterprise with deep expertise in high-current electrical equipment; Bharat Heavy Electricals has been expanding its presence in electric mobility infrastructure, including traction terminal systems for domestic EV and rail projects.

Strukton: A Dutch engineering company specializing in rail and road infrastructure electrification; Strukton leverages its rail terminal expertise to address adjacent opportunities in EV charging infrastructure terminal systems across the Benelux and Nordics regions.

TOSHIBA CORPORATION: A Japanese technology giant with significant investment in power electronics and electrical components; TOSHIBA's automotive division focuses on high-reliability terminal systems for hybrid and electric drivetrains, with production facilities across Japan and China.

Siemens: A global leader in industrial electrification and automation; Siemens applies its power systems expertise to automotive-grade terminal and connector solutions, particularly for commercial EV charging and vehicle-to-grid (V2G) applications.

Alstom: Primarily a rail transport technology company, Alstom has developed transferable competencies in high-current terminal systems that are being applied to heavy-duty EV bus and truck platforms, particularly in European markets.

CRRC: The world's largest rolling stock manufacturer by revenue; CRRC's electrical systems division is an emerging force in automotive-adjacent terminal markets, leveraging its massive Chinese manufacturing base and government-backed EV bus fleet deployments.

Bombardier: A Canadian aerospace and rail technology firm; Bombardier's rail systems division contributes terminal and connector engineering expertise relevant to electric transit and commercial vehicle applications.

Wabtec Corporation: A US-based freight and transit rail technology leader; Wabtec's expertise in high-power electrical systems and terminal assemblies is being extended into commercial EV and locomotive electrification platforms.

AEG Power Solutions B.V.: A European specialist in industrial power conversion and energy storage systems; AEG Power Solutions focuses on high-reliability terminal and interface solutions for EV charging infrastructure and industrial automation markets.

March 2024: Siemens announced a strategic partnership with a leading Tier 1 automotive harness supplier to co-develop 800-volt-rated terminal systems for next-generation BEV platforms targeting the European OEM market, with production scheduled to commence in 2026.

January 2024: TOSHIBA CORPORATION unveiled a new series of silver-alloy-plated high-current terminals designed for 400A continuous rating applications in commercial EV drivetrains, claiming a 15% improvement in thermal performance over predecessor products.

November 2023: Wabtec Corporation completed the integration of a rail electrical systems acquisition, consolidating terminal manufacturing capabilities across North American and European facilities to serve dual rail-and-automotive EV market channels.

September 2023: Hitachi Ltd. disclosed a $200 million capital expenditure commitment to expand its automotive electrical components production capacity in India, targeting the rapidly growing domestic EV market and export-oriented supply chain opportunities.

June 2023: CRRC signed a memorandum of understanding with two Chinese provincial governments to supply terminal and connector systems for 50,000 electric buses planned for deployment through 2027, establishing a multi-year demand anchor for its automotive electrical components division.

February 2023: Alstom and a European charging infrastructure consortium announced a joint development agreement to standardize high-current terminal interfaces for megawatt-class charging systems targeting heavy-duty electric trucks.

August 2022: AEG Power Solutions B.V. launched a new product line of IP67-rated waterproof terminal blocks engineered for EV battery management system integration, targeting harsh-environment automotive applications in both passenger and commercial vehicle platforms.

The Automotive Terminal Market exhibits pronounced regional concentration, with Asia Pacific serving as both the largest revenue generator and the fastest-growing geography.

Asia Pacific: This region accounted for an estimated 47% of global Automotive Terminal Market revenue in 2024, underpinned by China's position as the world's largest EV market, India's accelerating vehicle production ramp, and established automotive manufacturing hubs in Japan, South Korea, and ASEAN nations. The regional CAGR is estimated at 12.1% through 2033, outpacing the global average. China alone contributed over 60% of Asia Pacific terminal demand, driven by government EV mandates and the massive scale of domestic OEMs and battery manufacturers. India is the fastest-growing single country within the region, with terminal demand growing in tandem with domestic vehicle production capacity expansions and the government's FAME II and PM e-Bus schemes.

North America: North America represented approximately 22% of global market revenue in 2024, with the United States as the dominant contributor. The Inflation Reduction Act's domestic content provisions are catalyzing reshoring of EV supply chains, creating near-term demand for locally manufactured terminal components. The regional CAGR is projected at 9.8%, supported by EV adoption in passenger and light commercial vehicle segments and the expansion of DC fast-charging infrastructure networks. Mexico's role as a low-cost terminal manufacturing hub is expanding, attracting investment from both Asian and European suppliers.

Europe: Europe held approximately 21% of global revenue in 2024, with Germany, France, and the United Kingdom as primary demand centers. The European Union's 2035 ICE ban and CO2 fleet emission standards are structural drivers sustaining terminal market growth. The regional CAGR is estimated at 9.3%, slightly below the global average, reflecting a more mature automotive ecosystem with established supply chains. The Nordics and Benelux sub-regions are emerging as significant demand nodes for EV charging terminal systems.

Middle East & Africa and South America: These regions collectively account for approximately 10% of global market revenue but represent meaningful growth optionality. South America's CAGR is estimated at 8.1%, led by Brazil's domestic vehicle production and nascent EV policy frameworks. The Middle East & Africa region, while smaller in absolute terms, is growing at approximately 7.5%, driven by GCC infrastructure investments and South Africa's automotive manufacturing sector.

The Automotive Terminal Market has attracted substantial capital inflows over the past two to three years, reflecting investor confidence in the structural EV-driven demand thesis. M&A activity has been particularly pronounced, with larger industrial conglomerates acquiring or merging with specialized connector and terminal manufacturers to consolidate supply chain control and expand product portfolio breadth.

Hitachi Ltd.'s $200 million India capacity expansion, disclosed in 2023, is representative of a broader trend of greenfield and brownfield investment in emerging market manufacturing hubs designed to serve both domestic EV demand and global export supply chains. Similarly, Wabtec Corporation's acquisition integration in 2023 reflects strategic consolidation logic, combining rail and automotive electrical competencies to serve converging market segments.

Venture capital activity is concentrated in the technology layer adjacent to terminal hardware — specifically in smart connector systems with embedded condition monitoring sensors, automated crimping quality verification platforms, and AI-driven defect detection solutions for terminal assembly lines. Several European and Israeli deep-tech startups have raised Series A and B rounds in the $15–50 million range targeting these process innovation opportunities.

Strategic partnerships between terminal manufacturers and EV OEMs are multiplying, often structured as multi-year exclusive or preferred supplier agreements that provide revenue visibility in exchange for co-investment in application

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 10.52% from 2020-2034 |

| Segmentation |

|

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Comprehensive validation mechanisms ensuring market intelligence accuracy, reliability, and adherence to international standards.

500+ data sources cross-validated

200+ industry specialists validation

NAICS, SIC, ISIC, TRBC standards

Continuous market tracking updates

Factors such as are projected to boost the Automotive Terminal Market market expansion.

Key companies in the market include Hitachi Ltd., Bharat Heavy Electricals Limited, Strukton, TOSHIBA CORPORATION, Siemens, Alstom, CRRC, Bombardier, Wabtec Corporation, AEG Power Solutions B.V..

The market segments include Current rating, Vehicle type.

The market size is estimated to be USD 27.87 billion as of 2022.

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3690, USD 5820, and USD 9870 respectively.

The market size is provided in terms of value, measured in billion and volume, measured in .

Yes, the market keyword associated with the report is "Automotive Terminal Market," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Automotive Terminal Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.