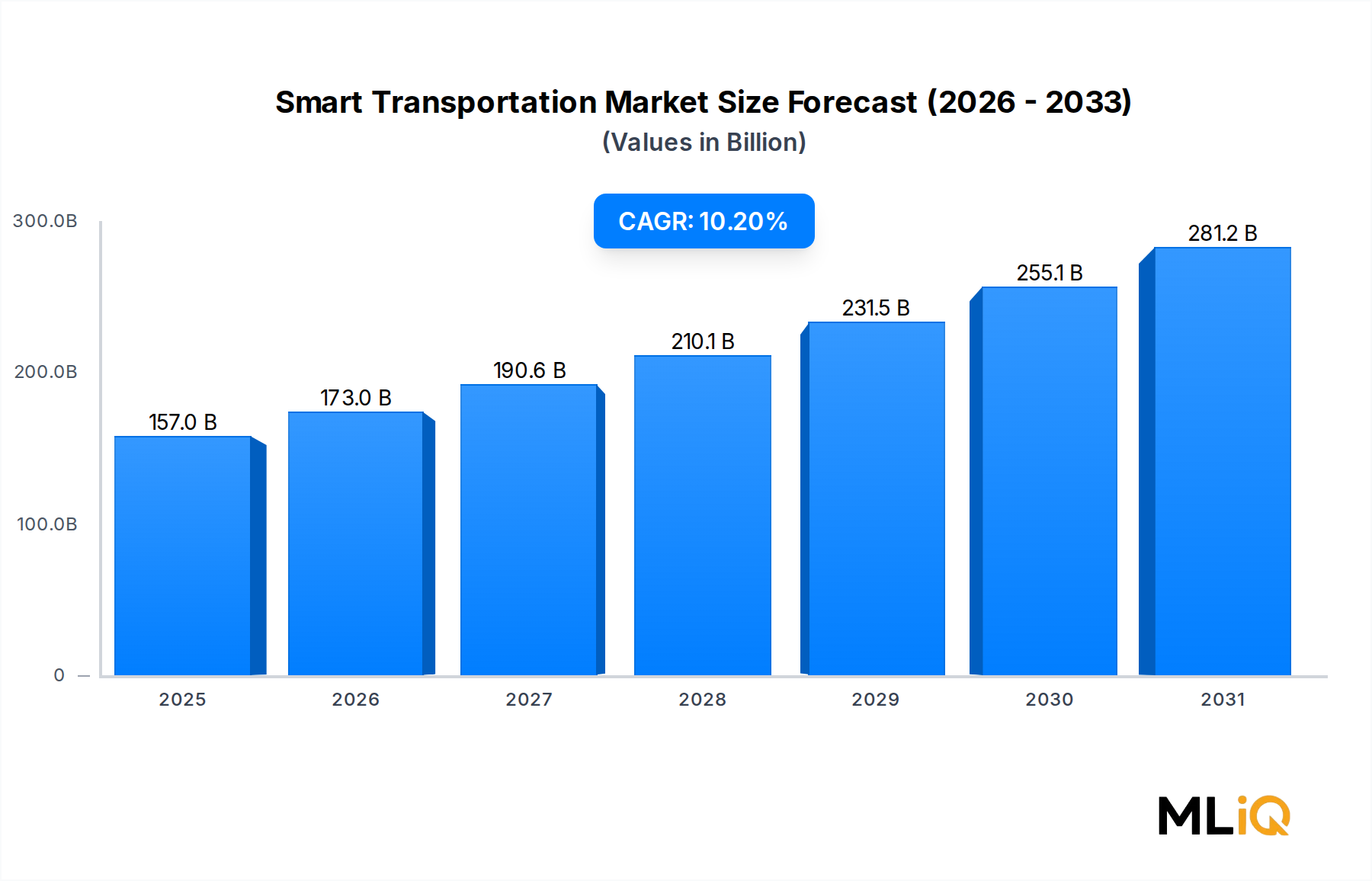

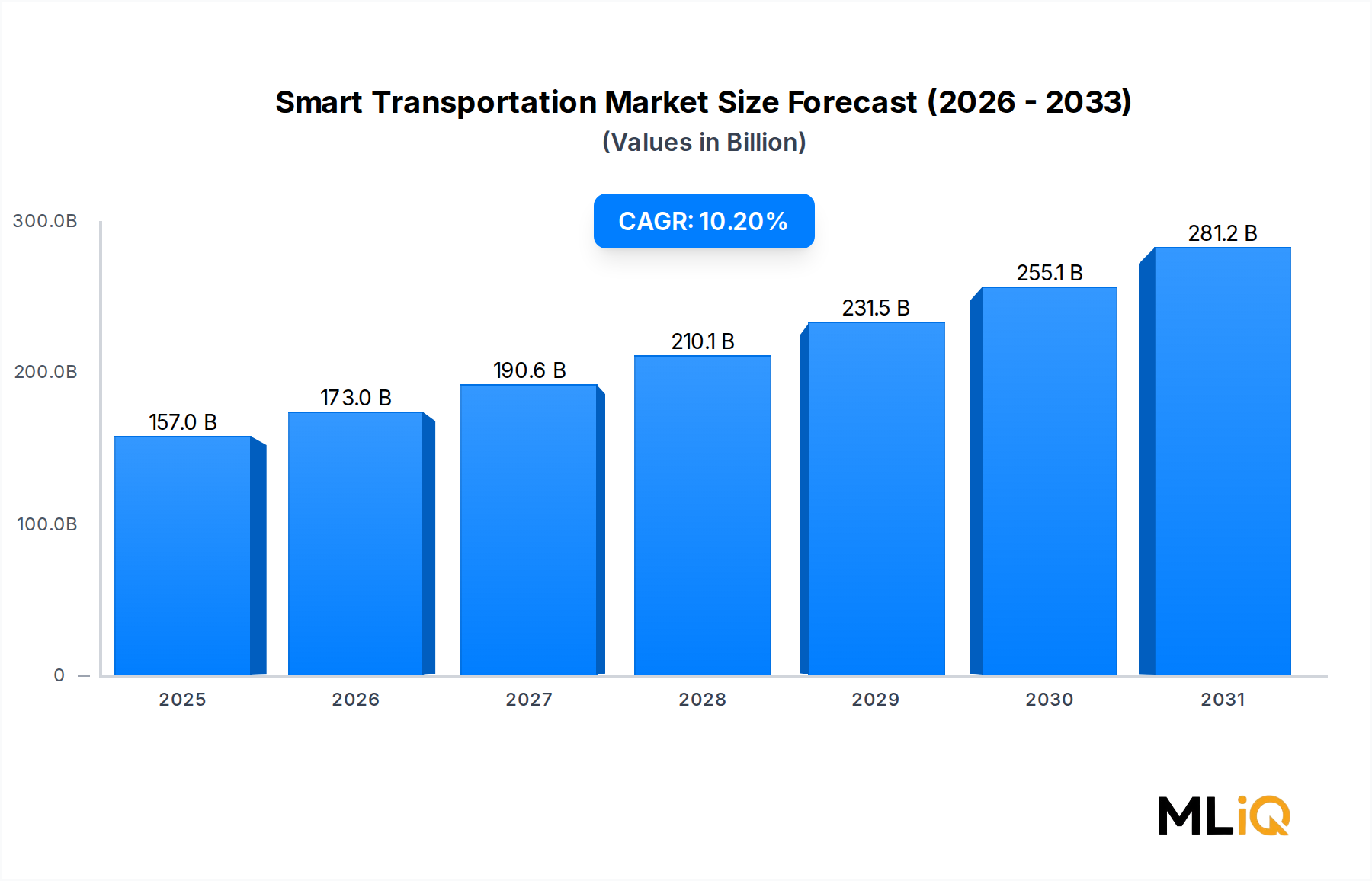

The Smart Transportation Market is undergoing a period of transformative acceleration, driven by the convergence of digital infrastructure, government urbanization mandates, and the proliferation of connected devices across mobility ecosystems. As of the current assessment period, the global market is valued at $156.99 billion and is projected to expand at a compound annual growth rate (CAGR) of 10.2% through the forecast horizon. This trajectory positions smart transportation as one of the most capital-intensive and strategically critical verticals within the broader Automotive and Transportation category.

Several macro-level forces are amplifying this growth. First, accelerating urbanization — with the United Nations projecting that 68% of the world's population will reside in urban areas by 2050 — is placing unprecedented strain on legacy transportation infrastructure. Municipalities and national governments are responding by deploying intelligent systems that optimize traffic flows, reduce congestion-related emissions, and enhance commuter experience. Second, the global push toward decarbonization is reshaping procurement priorities, compelling transport authorities to integrate emissions-monitoring, dynamic routing, and intermodal coordination technologies at scale.

Demand is also being catalyzed by the rapid maturation of 5G networks, which provide the ultra-low-latency communication backbone essential for real-time vehicle-to-infrastructure (V2I) and vehicle-to-vehicle (V2V) data exchange. Cloud-based platforms are enabling centralized supervision and predictive analytics across previously siloed transportation segments including roadways, railways, airways, and maritime operations.

On the supply side, the competitive landscape is consolidating around technology integrators capable of delivering end-to-end solutions — encompassing ticketing management, parking guidance, integrated supervision, and traffic management — as standalone point solutions give way to platform architectures. Key players such as Cisco Systems Inc., Siemens AG, IBM Corporation, and Thales Group are investing heavily in software-defined infrastructure that supports real-time decision-making at city scale.

Geographically, North America currently holds the largest revenue share, underpinned by federal infrastructure investment programs and mature digital ecosystems. However, Asia Pacific is emerging as the fastest-growing region, fueled by China's smart city initiatives and India's National Intelligent Transportation Systems Programme. Europe remains a strong performer, driven by stringent emissions regulations and the EU's Sustainable and Smart Mobility Strategy.

Looking ahead, the Smart Transportation Market is poised for structural expansion as public-private partnerships scale deployment, autonomous vehicle frameworks mature, and data monetization models emerge as a secondary revenue layer for platform operators. The market's outlook through the next decade is robustly positive, with innovation cycles shortening and total addressable market boundaries continuously widening.