1. What are the major growth drivers for the Automotive eSIM Market market?

Factors such as are projected to boost the Automotive eSIM Market market expansion.

+1 2315155523

Automotive eSIM Market

Automotive eSIM Market

Market Lens IQ is a global market intelligence and strategic consulting firm delivering advanced syndicated research reports, customized industry analysis, competitive intelligence, and data-driven advisory solutions to organizations across international markets. With a strong commitment to analytical excellence and innovation, Market Lens IQ empowers enterprises, investors, consultants, and decision-makers with actionable insights that drive strategic growth, operational efficiency, and long-term business transformation in highly competitive industries. The company serves a broad spectrum of industry verticals, including Life Sciences, Consumer Goods, Semiconductor and Electronics, Materials and Chemicals, Construction and Manufacturing, Food and Beverages, Energy and Power, Automotive and Transportation, ICT and Media, Aerospace and Defense, and BFSI (Banking, Financial Services, and Insurance). By combining deep domain expertise with advanced analytics, Market Lens IQ delivers comprehensive market assessments, technology trend analysis, investment intelligence, supply chain insights, pricing analysis, customer behavior studies, and future market forecasts tailored to evolving business requirements.

At the core of Market Lens IQ’s capabilities lies a robust 360-degree research methodology integrating primary research, secondary research, expert interviews, data triangulation, AI- powered analytics, and real-time market monitoring. Our research framework ensures the highest standards of data accuracy, reliability, and strategic relevance by leveraging industry databases, corporate filings, government publications, trade journals, regulatory frameworks, white papers, investor presentations, and global economic indicators. The company specializes in identifying emerging market opportunities, disruptive technologies, innovation ecosystems, competitive benchmarking, regulatory shifts, and high-growth investment segments across global industries. Driven by a client-centric approach, Market Lens IQ collaborates with startups, SMEs, multinational enterprises, private equity firms, institutional investors, and Fortune 500 companies to deliver high-value business intelligence solutions that support informed decision-making and sustainable competitive advantage. Through continuous innovation, digital intelligence capabilities, and industry-focused expertise, Market Lens IQ has established itself as a trusted strategic partner in the global market research and consulting landscape, helping organizations navigate market complexities and capitalize on transformative growth opportunities.

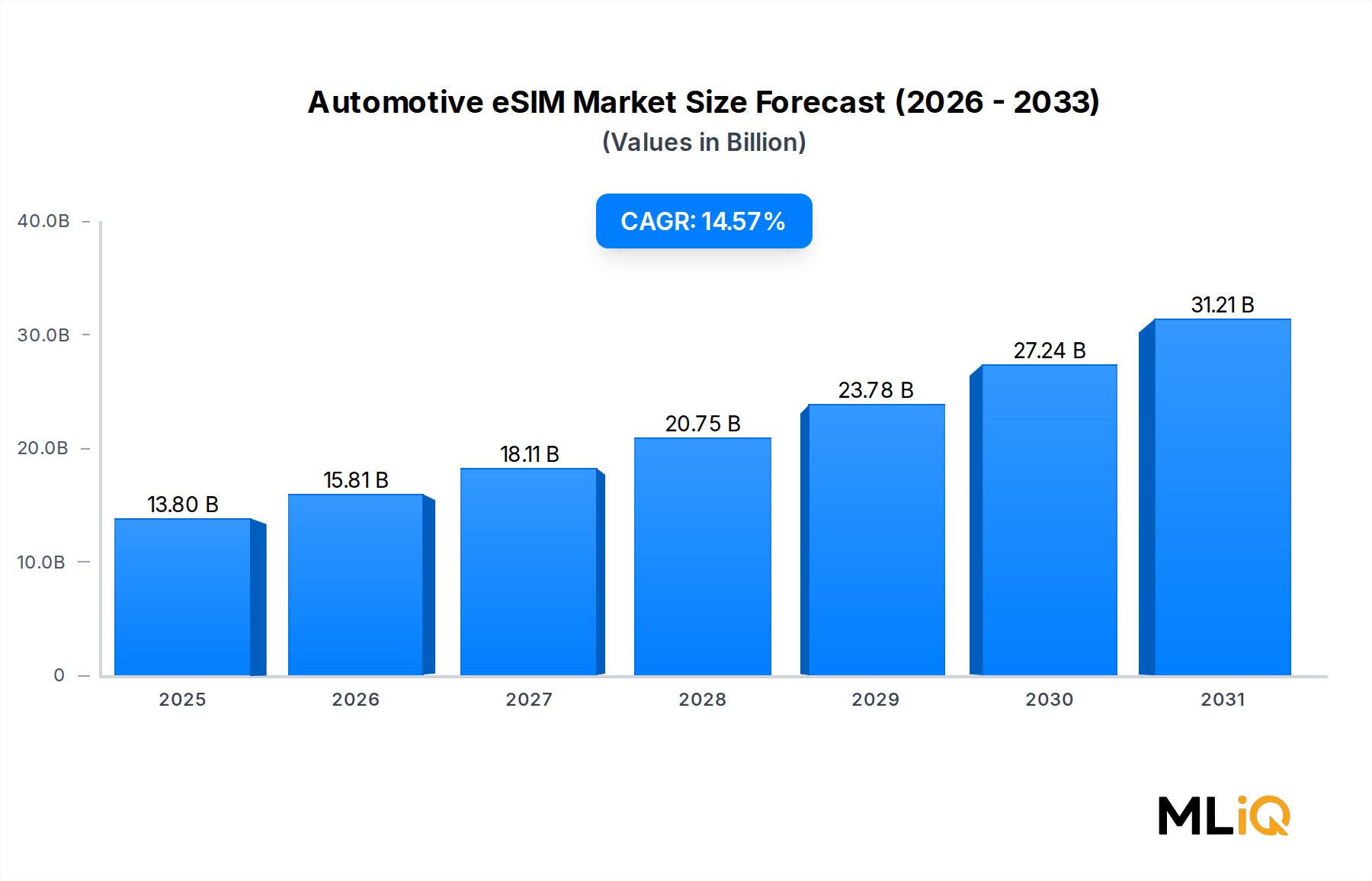

The global Automotive eSIM Market is valued at $13.8 billion in 2025 and is projected to expand at a compound annual growth rate of 14.57% through 2033, establishing it as one of the most dynamically evolving segments within the broader connected mobility ecosystem. This robust growth trajectory is underpinned by a confluence of technological, regulatory, and consumer-behavior shifts that collectively amplify demand for embedded SIM solutions across passenger and commercial vehicle segments worldwide.

At its core, the automotive eSIM enables seamless, over-the-air carrier switching, allowing vehicles to maintain persistent network connectivity regardless of geographic boundaries. This capability is increasingly non-negotiable for original equipment manufacturers (OEMs) pursuing global platform strategies, where a single vehicle architecture must support heterogeneous telecommunications environments across dozens of regulatory jurisdictions. As OEMs accelerate software-defined vehicle (SDV) roadmaps, the eSIM serves as a foundational connectivity layer enabling remote diagnostics, over-the-air software updates, real-time traffic integration, and advanced driver-assistance system (ADAS) telemetry.

Regulatory tailwinds are amplifying adoption further. The European Union's eCall mandate, which requires all new passenger vehicles to incorporate emergency call functionality, has effectively institutionalized cellular connectivity hardware as standard equipment, creating a structural demand floor for embedded SIM modules across the European market. Similar legislative frameworks are emerging across Asia Pacific, particularly in China and South Korea, where national intelligent transportation system (ITS) initiatives are embedding connectivity requirements into vehicle homologation standards.

On the demand side, consumer expectations for in-vehicle infotainment, navigation-as-a-service, and subscription-based feature unlocking are reshaping the value proposition of automotive connectivity. Automotive OEMs are increasingly monetizing connected services post-sale, generating recurring revenue streams that depend entirely on persistent eSIM-enabled network access. This shift from one-time hardware revenue to annuity-based service models is a critical macro tailwind sustaining investment in eSIM infrastructure throughout the forecast period.

The proliferation of electric vehicles (EVs) is also a meaningful demand amplifier. EVs are natively software-intensive platforms requiring continuous telemetry transmission — battery state-of-health monitoring, predictive charging network routing, and remote thermal management — all of which depend on reliable embedded cellular connectivity. As EV penetration accelerates globally, the intersection of electrification and connectivity mandates will structurally reinforce eSIM adoption rates.

Looking ahead to 2033, the market is expected to reach a valuation exceeding $40 billion, with hardware revenue share gradually compressing as connectivity services and managed subscription platforms capture a growing proportion of total market value. The competitive landscape will intensify as telecommunications operators, semiconductor vendors, and cloud platform providers converge on the automotive connectivity stack, each seeking to own higher-margin layers of the eSIM value chain.

Within the application segmentation of the Automotive eSIM Market, the connected car sub-segment commands the largest revenue share and continues to consolidate its dominance through 2033. This primacy reflects the breadth of use cases that connected car applications encompass — ranging from real-time navigation and infotainment streaming to V2X (vehicle-to-everything) communication protocols and emergency services integration — all of which require persistent, high-reliability cellular connectivity delivered through embedded SIM infrastructure.

The connected car application generates superior average revenue per unit (ARPU) compared to remote connectivity or internet connectivity sub-segments because it encompasses both the hardware module and the associated managed services layer. OEMs deploying connected car platforms typically bundle eSIM activation with multi-year connectivity subscriptions, creating recurring revenue profiles that attract higher valuation multiples and incentivize deeper OEM-telecom partnerships. This bundling dynamic structurally elevates the connected car sub-segment's revenue contribution relative to its unit volume share.

Technology integration complexity further reinforces connected car's dominant position. Connected car deployments require eSIM modules certified to automotive-grade standards (AEC-Q100), capable of operating across extended temperature ranges (-40°C to +125°C), and compliant with GSMA SGP.02 and SGP.32 IoT eSIM specifications. These technical barriers to entry concentrate market share among a limited number of qualified module vendors, creating oligopolistic supply dynamics that sustain premium pricing within the connected car segment.

Key players driving connected car eSIM revenue include Giesecke & Devrient GmbH, which has developed purpose-built automotive eSIM management platforms integrating subscription management data preparation (SM-DP+) capabilities with OEM telematics control unit (TCU) architectures. Sierra Wireless Inc. contributes ruggedized automotive-grade eSIM modules optimized for always-on connectivity in passenger vehicles. NXP Semiconductors N.V. and STMicroelectronics supply the underlying secure element silicon that forms the hardware root of trust for eSIM credential storage in connected car applications.

From a vehicle type perspective, passenger vehicles represent the largest volume contributor to the connected car sub-segment, driven by high global production volumes and accelerating standard-equipment connectivity rates among premium and mid-range OEM brands. However, light commercial vehicles are exhibiting faster growth within connected car applications, as logistics fleet operators integrate connected car-grade telemetry with supply chain visibility platforms, requiring the same security and reliability standards as passenger vehicle deployments.

Geographically, connected car eSIM deployments are most concentrated in North America and Europe, where OEM connectivity mandates and consumer willingness-to-pay for subscription services are highest. Asia Pacific, particularly China, is emerging as the fastest-growing connected car eSIM market, supported by domestic OEM investment in intelligent cockpit platforms and government-backed V2X infrastructure rollouts in tier-1 cities.

The connected car sub-segment's share is not merely holding — it is actively expanding as new use cases, particularly over-the-air (OTA) software update delivery and cybersecurity patch management, generate incremental data transmission requirements that cannot be satisfied by legacy removable SIM architectures. This structural dependency on eSIM for SDV lifecycle management ensures that connected car applications will remain the market's largest and most strategically significant revenue contributor throughout the forecast horizon.

Several high-impact drivers are accelerating adoption across the Automotive eSIM Market, each supported by measurable market evidence and regulatory context.

The most significant driver is the global expansion of 5G network infrastructure. As of 2024, 5G network coverage had been deployed commercially across more than 80 countries, with automotive-grade 5G NR (New Radio) modem chipsets beginning to penetrate volume vehicle platforms. The transition from 4G LTE to 5G connectivity doubles the data throughput requirements of in-vehicle applications, necessitating next-generation eSIM modules capable of managing multi-slice network profiles — a technical requirement only addressable through embedded SIM architectures supporting GSMA's SGP.32 standard.

Regulatory mandates constitute a structural, non-cyclical driver. The EU eCall regulation, which became mandatory for all new type-approved vehicles from April 2018, created baseline eSIM hardware demand across the European vehicle parc. China's GB/T 32960 telematics standard for new energy vehicles (NEVs) similarly mandates real-time data reporting to government platforms, functionally requiring persistent cellular connectivity for all NEV registrations. These mandates collectively affect hundreds of millions of vehicle production units annually.

OTA software update adoption is a third quantifiable driver. A survey of global OEM SDV programs indicates that over 65% of new vehicle platforms launched after 2023 incorporate OTA update capabilities, each requiring persistent eSIM connectivity to function. As regulatory bodies in the EU and US move toward mandatory cybersecurity update requirements for connected vehicles (UNECE WP.29 R155/R156), OTA dependency — and therefore eSIM demand — becomes structurally locked in across vehicle lifecycles.

On the constraint side, the primary inhibitor is the fragmented global eSIM standards landscape. The coexistence of GSMA M2M (SGP.02) and consumer eSIM (SGP.22/SGP.32) specifications creates interoperability uncertainty for OEMs deploying global vehicle platforms, increasing integration complexity and certification costs. Additionally, geopolitical supply chain disruptions affecting semiconductor manufacturing — particularly the 2021–2023 automotive chip shortage, which reduced global vehicle production by an estimated 7.7 million units — exposed the vulnerability of single-source eSIM chipset supply chains, creating risk premiums that constrain margin expansion for module vendors.

The competitive landscape of the Automotive eSIM Market is characterized by vertical integration across semiconductor, module, and platform layers, with telecommunications operators increasingly partnering with hardware vendors to capture managed services revenue.

Giesecke & Devrient GmbH: A global leader in eSIM operating system and subscription management platform development, Giesecke & Devrient provides automotive-certified SM-DP+ infrastructure and eSIM personalization services to major European and Asian OEMs, positioning itself as the trusted intermediary between vehicle platforms and mobile network operators.

Sierra Wireless Inc.: Specializing in ruggedized IoT modules for industrial and automotive applications, Sierra Wireless offers automotive-grade eSIM-embedded modules compliant with AEC-Q100 standards and has established OEM supply agreements across North American and European vehicle programs.

Singapore Telecommunications Limited: As a regional telecommunications anchor in Asia Pacific, Singapore Telecommunications Limited has developed automotive eSIM connectivity management services targeting cross-border fleet operators and connected vehicle platforms across Southeast Asian markets.

Deutsche Telekom AG: Operating one of Europe's largest mobile network footprints, Deutsche Telekom AG has invested in automotive eSIM subscription management platforms and partners with global OEMs to provide embedded connectivity bundles, leveraging its T-Systems enterprise services division for fleet telematics integration.

NXP Semiconductors N.V.: A dominant supplier of automotive-grade secure element silicon, NXP Semiconductors N.V. provides the hardware security module (HSM) foundations underpinning eSIM credential storage and cryptographic operations in vehicle TCUs, with deep integration into major automotive MCU platforms.

Telefónica S.A.: Through its global IoT connectivity division, Telefónica S.A. delivers automotive eSIM lifecycle management and multi-IMSI connectivity services, with particular strength in Latin American and Southern European OEM programs.

NTT DOCOMO INC.: Japan's leading mobile operator, NTT DOCOMO INC. has built automotive eSIM management infrastructure targeting the Japanese domestic OEM market and is expanding into Asia Pacific cross-border connected vehicle services.

Gemalto NV: Now integrated within Thales Group's digital security division, Gemalto NV maintains a significant intellectual property portfolio in eSIM personalization and remote SIM provisioning, with extensive automotive OEM certification history across GSMA SGP.02 compliant deployments.

STMicroelectronics: A key supplier of secure microcontroller units (MCUs) for automotive eSIM applications, STMicroelectronics provides ISO 7816-compliant secure element silicon optimized for ultra-low-power vehicle telematics use cases.

Infineon Technologies AG: Infineon Technologies AG supplies automotive security controllers and SIM interface chipsets used in eSIM module assemblies, with a strategic focus on functional safety certification (ISO 26262 ASIL-B/D) compliance for safety-critical connected vehicle applications.

January 2024: GSMA officially released the SGP.32 IoT eSIM architecture specification, providing a unified technical framework for automotive-grade remote SIM provisioning that eliminates the operational complexity of managing separate M2M and consumer eSIM profiles within a single vehicle platform.

March 2024: A major European OEM consortium announced a multi-year eSIM connectivity agreement spanning 5 million vehicles annually, establishing a standardized embedded SIM provisioning infrastructure across its global vehicle production network and marking one of the largest single automotive eSIM platform commitments on record.

June 2024: Infineon Technologies AG launched its SLx 9670 TPM automotive security controller with integrated eSIM profile management capabilities, targeting next-generation vehicle TCU architectures requiring combined trusted platform module (TPM) and eSIM functionality on a single silicon die.

September 2024: China's Ministry of Industry and Information Technology (MIIT) expanded its connected vehicle data security regulations, mandating encrypted telematics transmission for all passenger vehicles sold after January 2025, effectively requiring eSIM-grade secure element hardware as baseline equipment in China's 30+ million unit annual vehicle market.

November 2024: NXP Semiconductors N.V. announced volume production availability of its SAF5400 automotive-grade 5G modem with integrated eSIM functionality, representing the industry's first automotive-certified 5G NR modem-eSIM combination chipset qualified for production vehicle programs.

February 2025: Giesecke & Devrient GmbH completed certification of its AirOn eSIM platform under GSMA SGP.32 for automotive IoT applications, enabling OEMs to manage eSIM profiles for millions of vehicles across 190+ network operators globally through a single API-driven management interface.

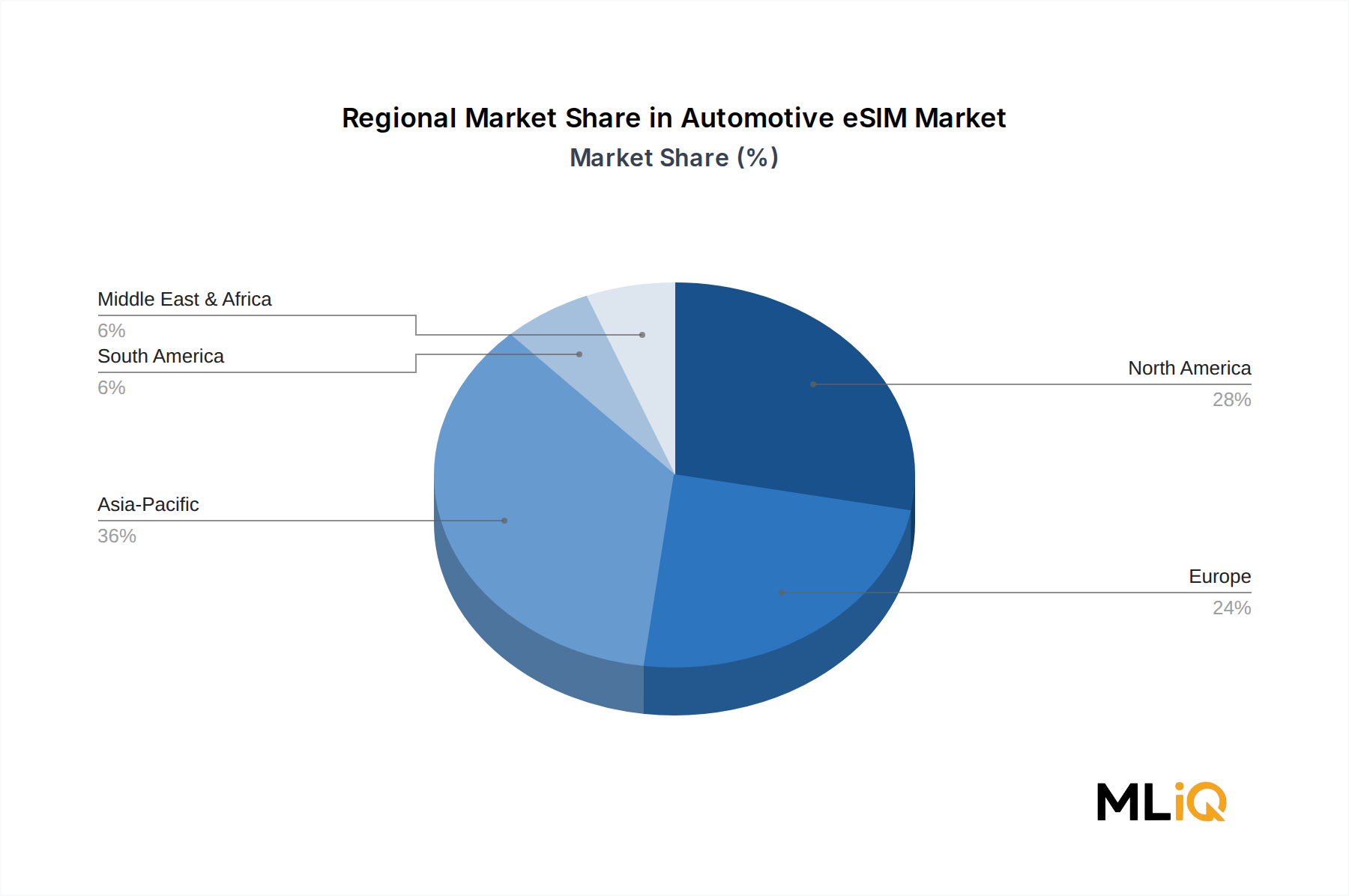

The Automotive eSIM Market exhibits pronounced regional differentiation in growth rates, adoption maturity, and demand drivers, reflecting the heterogeneous regulatory, infrastructure, and OEM production landscapes across key geographic zones.

North America represents one of the most mature regional markets, accounting for approximately 28% of global revenue in 2025. The region benefits from high OEM connectivity penetration rates, with major domestic automakers having standardized eSIM across their passenger vehicle lineups. The US market is driven by consumer demand for connected services, fleet telematics adoption among logistics operators, and ongoing 5G network densification by major carriers. North America is projected to grow at a CAGR of approximately 12.8% through 2033, reflecting a mature-market growth profile with incremental upside from SDV platform transitions.

Europe is the second-largest regional market, holding approximately 26% of global eSIM revenue in 2025. The region's growth at a CAGR of approximately 13.5% is structurally anchored by the eCall mandate and the EU's GDPR-compliant connected services ecosystem that demands eSIM-based data sovereignty management. Germany, France, and the United Kingdom are the primary revenue contributors, aligned with their dominance in premium vehicle OEM production.

Asia Pacific is the fastest-growing regional market, projected to expand at a CAGR exceeding 17.2% through 2033, driven by China's massive NEV market, Japan's domestically-oriented connected vehicle ecosystem, and South Korea's 5G infrastructure leadership. China alone contributes over 40% of Asia Pacific's eSIM automotive revenue, supported by government mandates, domestic OEM investment, and the world's largest annual vehicle production volume exceeding 30 million units. India is an emerging high-growth sub-market, with government-backed connected vehicle initiatives beginning to catalyze eSIM adoption from a low base.

Middle East & Africa represents the smallest regional market share at approximately 4% of global revenue in 2025, but exhibits above-average growth potential driven by GCC-region smart city infrastructure investments and fleet telematics mandates in the logistics sector. South Africa is the primary sub-Saharan contributor, with connected vehicle programs linked to stolen vehicle recovery networks.

South America accounts for approximately 5% of global revenue, with Brazil as the dominant market. Growth is moderate at approximately 11.2% CAGR, constrained by economic volatility but supported by Brazil's mandatory vehicle tracking (CONTRAN) regulatory framework for commercial vehicles, which is driving fleet-segment eSIM adoption.

The Automotive eSIM Market's supply chain is a multi-tier ecosystem spanning raw semiconductor materials, secure element silicon fabrication, module assembly, and software platform provisioning, each tier carrying distinct sourcing risks and price volatility profiles.

At the upstream raw material level, silicon wafer supply is the foundational input. Automotive-grade eSIM secure elements require high-purity silicon wafers (300mm diameter) fabricated at advanced nodes (

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 14.57% from 2020-2034 |

| Segmentation |

|

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Comprehensive validation mechanisms ensuring market intelligence accuracy, reliability, and adherence to international standards.

500+ data sources cross-validated

200+ industry specialists validation

NAICS, SIC, ISIC, TRBC standards

Continuous market tracking updates

Factors such as are projected to boost the Automotive eSIM Market market expansion.

Key companies in the market include Giesecke & Devrient GmbH, Sierra Wireless Inc., Singapore Telecommunications Limited, Deutsche Telekom AG, NXP Semiconductors N.V., Telefónica S.A., NTT DOCOMO INC., Gemalto NV, STMicroelectronics, Infineon Technologies AG.

The market segments include Solution, Application, Vehicle Type, Solution, Application, Vehicle Type.

The market size is estimated to be USD 13.8 billion as of 2022.

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3690, USD 5820, and USD 9870 respectively.

The market size is provided in terms of value, measured in billion and volume, measured in .

Yes, the market keyword associated with the report is "Automotive eSIM Market," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Automotive eSIM Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.