1. What are the major growth drivers for the Marine Passenger Seat Market market?

Factors such as are projected to boost the Marine Passenger Seat Market market expansion.

Marine Passenger Seat Market

Marine Passenger Seat Market

Market Lens IQ is a global market intelligence and strategic consulting firm delivering advanced syndicated research reports, customized industry analysis, competitive intelligence, and data-driven advisory solutions to organizations across international markets. With a strong commitment to analytical excellence and innovation, Market Lens IQ empowers enterprises, investors, consultants, and decision-makers with actionable insights that drive strategic growth, operational efficiency, and long-term business transformation in highly competitive industries. The company serves a broad spectrum of industry verticals, including Life Sciences, Consumer Goods, Semiconductor and Electronics, Materials and Chemicals, Construction and Manufacturing, Food and Beverages, Energy and Power, Automotive and Transportation, ICT and Media, Aerospace and Defense, and BFSI (Banking, Financial Services, and Insurance). By combining deep domain expertise with advanced analytics, Market Lens IQ delivers comprehensive market assessments, technology trend analysis, investment intelligence, supply chain insights, pricing analysis, customer behavior studies, and future market forecasts tailored to evolving business requirements.

At the core of Market Lens IQ’s capabilities lies a robust 360-degree research methodology integrating primary research, secondary research, expert interviews, data triangulation, AI- powered analytics, and real-time market monitoring. Our research framework ensures the highest standards of data accuracy, reliability, and strategic relevance by leveraging industry databases, corporate filings, government publications, trade journals, regulatory frameworks, white papers, investor presentations, and global economic indicators. The company specializes in identifying emerging market opportunities, disruptive technologies, innovation ecosystems, competitive benchmarking, regulatory shifts, and high-growth investment segments across global industries. Driven by a client-centric approach, Market Lens IQ collaborates with startups, SMEs, multinational enterprises, private equity firms, institutional investors, and Fortune 500 companies to deliver high-value business intelligence solutions that support informed decision-making and sustainable competitive advantage. Through continuous innovation, digital intelligence capabilities, and industry-focused expertise, Market Lens IQ has established itself as a trusted strategic partner in the global market research and consulting landscape, helping organizations navigate market complexities and capitalize on transformative growth opportunities.

+1 2315155523

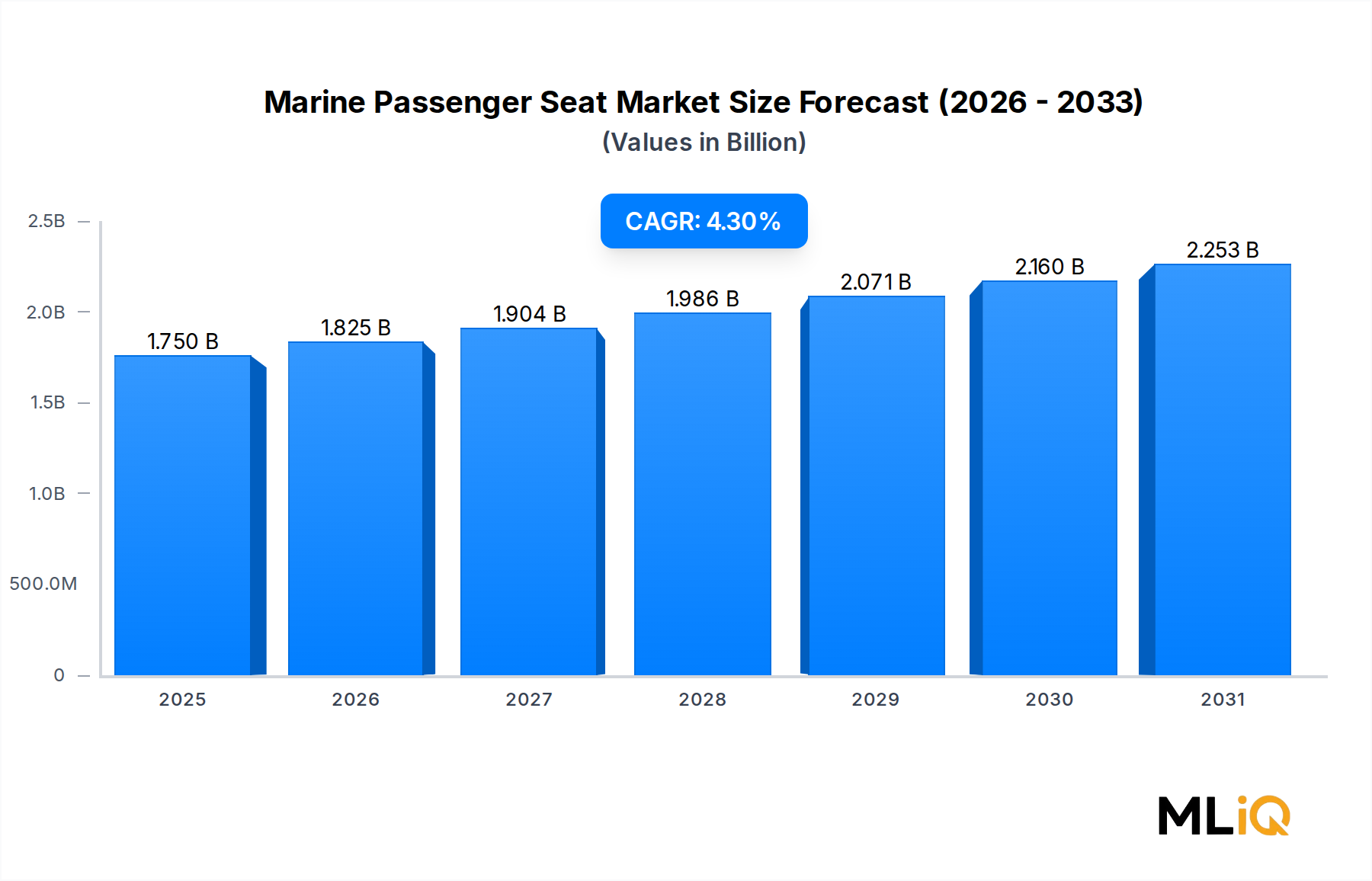

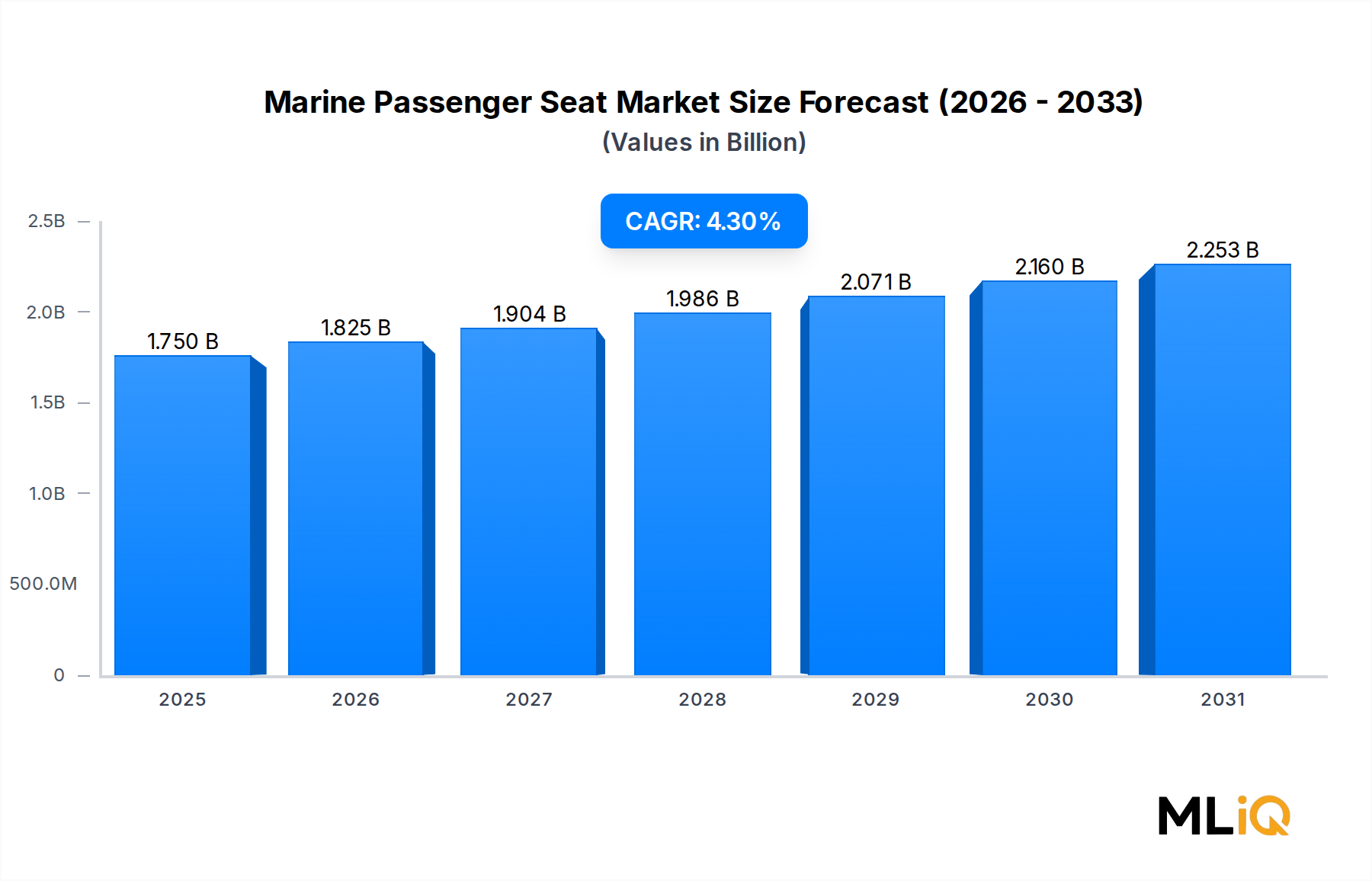

The global Marine Passenger Seat Market was valued at $1.75 billion in 2024 and is projected to expand at a compound annual growth rate (CAGR) of 4.3% through the forecast horizon, driven by accelerating fleet modernization, rising recreational boating participation, and stringent ergonomic and safety mandates imposed by international maritime regulators. This market sits at the confluence of the broader Shipbuilding and Repair Market and the specialized Marine Seating Systems Market, drawing demand impulses from both commercial operators and individual vessel owners.

Key demand drivers include a post-pandemic resurgence in leisure marine tourism, particularly in North America and the Asia-Pacific region, where discretionary spending on watercraft experiences has rebounded sharply. Commercial ferry operators across Europe and Southeast Asia are investing in passenger experience upgrades as a differentiator, translating directly into procurement cycles for high-specification seating assemblies. Simultaneously, naval modernization budgets in the United States, China, and India are funding advanced seating platforms that meet both vibration-mitigation and ballistic-resistance criteria.

Macro tailwinds reinforcing market expansion include rising global trade volumes increasing demand for passenger-cargo hybrid vessels, growing cruise tourism infrastructure in the Middle East and the Caribbean, and a wave of retrofitting activity driven by aging commercial fleets in Europe. Environmental regulations are also shaping product roadmaps: the International Maritime Organization's (IMO) decarbonization targets are accelerating the adoption of lightweight composite and recycled-material seating to reduce overall vessel weight and fuel consumption.

From a product perspective, seat cushion assemblies and pedestal sub-systems constitute the highest revenue-generating components, while aftermarket channels are exhibiting faster growth compared to OEM procurement as vessel owners extend asset life cycles rather than replacing entire fleets. The OEM segment, however, retains the largest absolute value share, underpinned by long-term supply agreements with major shipbuilders.

Looking forward, the market is expected to benefit from the intersection of smart vessel initiatives and occupant comfort innovation. Sensor-integrated seating capable of monitoring passenger biometrics, vibration exposure levels, and occupancy patterns is transitioning from concept to commercialization, particularly in military and high-speed passenger craft applications. Manufacturers capable of integrating IoT-enabled features without materially inflating unit cost will capture disproportionate share in premium segments. Overall, the market outlook through the end of the decade is constructive, with structural tailwinds outweighing near-term headwinds such as raw material cost volatility and geopolitical disruptions to global shipping supply chains.

Within the Marine Passenger Seat Market, the commercial ship type segment commands the largest revenue share, accounting for an estimated majority of total market value in 2024. This dominance is rooted in several structural factors: the sheer scale of commercial passenger vessel fleets, the frequency of seating replacement driven by intensive usage cycles, and the regulatory compliance requirements mandating certified ergonomic and safety-rated seating in vessels carrying fare-paying passengers.

Commercial applications span a broad spectrum of vessel types, including high-speed ferries, roll-on/roll-off (RoRo) passenger ships, river cruise vessels, excursion boats, and water taxis. Each vessel category imposes distinct seating specifications. High-speed catamaran ferries operating on routes such as those in Scandinavia, Hong Kong, and the Canary Islands demand shock-attenuating suspension seats capable of managing wave-induced vertical accelerations that can exceed 3g in open-water conditions. Conversely, inland river cruise vessels in Europe and Southeast Asia prioritize comfort, modularity, and aesthetic customization to align with premium hospitality positioning.

The commercial segment's revenue share is reinforced by the procurement behavior of fleet operators, who typically issue multi-year framework agreements covering initial outfitting and scheduled replacement cycles. This contrasts with the more fragmented and lower-average-order-value purchasing patterns observed in the military and private recreational segments. Major ferry operators in Europe — including those operating across the English Channel, the Baltic Sea, and the Adriatic — maintain fleet replacement cadences of 8 to 15 years, ensuring a predictable and recurring demand base for seating manufacturers.

Within the commercial sub-segment, the OEM channel currently absorbs approximately 60–65% of commercial seating volumes, with the balance flowing through aftermarket and refurbishment channels. Aftermarket demand is growing faster, however, as operators facing tight capital expenditure environments opt for seat refurbishment programs — replacing cushioning, upholstery, and mechanical components — rather than full seat replacement. This dynamic is creating a bifurcated competitive landscape where Tier-1 manufacturers compete on OEM program awards while a second tier of regional specialists captures aftermarket business through competitive pricing and rapid lead times.

Component-level analysis reveals that seat cushion assemblies and seat mounts represent the highest-value sub-components within the commercial segment. Cushion systems must comply with fire, smoke, and toxicity (FST) standards such as IMO Resolution A.652(16) for marine upholstery, driving demand for specialized foam formulations sourced from the Marine Foam and Cushioning Market. Pedestal and base systems, meanwhile, are increasingly engineered with corrosion-resistant aluminum and composite materials to extend service life in salt-water environments.

Key players dominating the commercial segment include Ullman Dynamics, which has established a global reputation for vibration-attenuating seats used in high-speed craft, and Thomas Scott Seating Ltd, which focuses on customized commercial ferry seating solutions across European markets. Todd Marine Products and Springfield Marine Company hold strong positions in the North American commercial and recreational overlap segment. The commercial segment's share appears stable to modestly growing, supported by the ongoing expansion of ferry infrastructure in Asia-Pacific markets and the retrofitting wave in mature European fleets. Companies that can demonstrate full lifecycle management — covering design, OEM supply, maintenance, and refurbishment — are best positioned to consolidate share within this segment over the next five years.

Several quantifiable drivers and constraints are actively shaping the trajectory of the Marine Passenger Seat Market, and understanding their relative weight is essential for strategic positioning.

On the demand side, the global recreational boating industry is a primary growth engine. According to industry data aligned with trends in the Recreational Boating Market, new powerboat registrations in the United States alone exceeded 280,000 units in recent years, sustaining strong aftermarket seating demand. The ASEAN region is experiencing boat fleet growth rates of 5–7% annually, creating incremental OEM seating demand as new vessels enter service.

Naval modernization programs represent a second high-value driver. Defense budgets globally have trended upward, with NATO member states collectively increasing maritime expenditure. Military-grade seating — incorporating blast attenuation, quick-release harness integration, and NVG (night-vision goggle) compatibility — commands 40–60% price premiums over standard commercial equivalents, materially elevating per-unit revenue for manufacturers serving this end-use.

Regulatory compliance mandates constitute a structural, non-discretionary driver. IMO SOLAS Chapter II-2 regulations governing fire safety of furnishings, combined with ASTM and ISO ergonomic standards, create mandatory replacement cycles that are independent of operator discretionary spending. Non-compliance risks vessel certification, ensuring a baseline demand floor.

Constraints are equally significant. Raw material cost volatility — particularly for marine-grade stainless steel, aluminum extrusions, and polyurethane foam — creates margin pressure throughout the value chain. Input cost inflation during 2021–2023 compressed gross margins for mid-tier manufacturers by an estimated 3–5 percentage points. Supply chain fragmentation for specialized components such as shock-absorbing pedestals further extends lead times, limiting responsiveness to OEM build schedules.

Geopolitical disruptions, including port congestion and Red Sea shipping route diversions observed through 2024, have inflated logistics costs for manufacturers relying on transoceanic component sourcing. These constraints are partially offsetting the positive demand impulses, and their resolution will be key to margin recovery across the industry.

The competitive landscape of the Marine Passenger Seat Market is moderately fragmented, with a mix of global specialists, regional champions, and vertically integrated marine hardware suppliers. The following profiles capture the strategic positioning of the key participants identified in market data:

The Marine Passenger Seat Market exhibits distinct regional dynamics, with growth rates and demand drivers varying substantially across geographies.

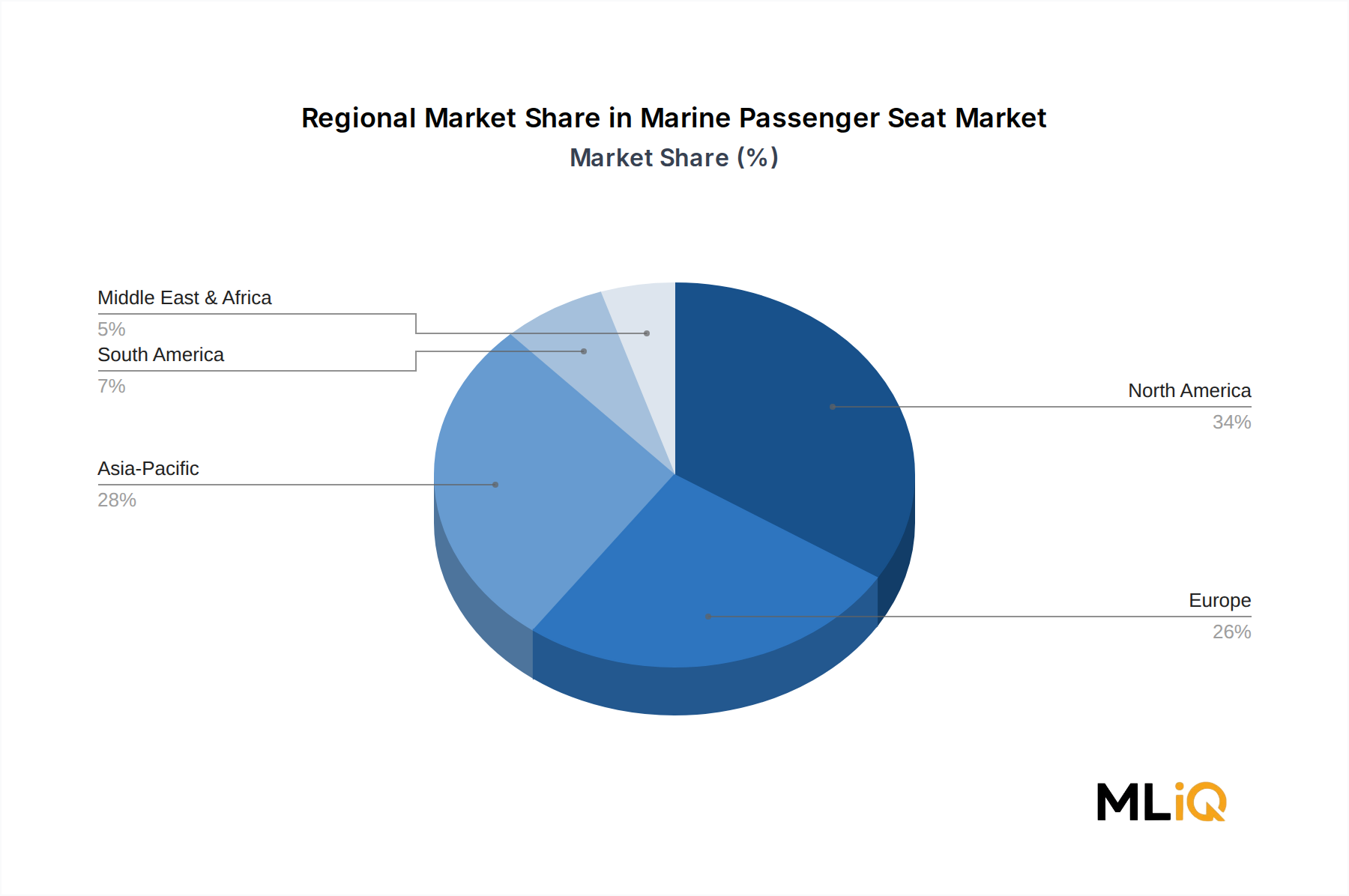

North America represents the largest single regional market, accounting for an estimated 35–38% of global revenue in 2024. The United States dominates due to the world's largest registered recreational boat fleet, a robust defense procurement budget for naval seating, and a well-developed aftermarket distribution infrastructure. Canada and Mexico contribute incrementally, particularly in commercial fishing and Great Lakes ferry applications. The North American market is growing at approximately 3.8–4.0% CAGR, reflecting its relative maturity and high existing penetration.

Europe is the second-largest region, with the United Kingdom, Germany, France, and the Nordic countries collectively generating substantial commercial ferry seating demand. European growth is supported by fleet modernization programs among Baltic and Mediterranean ferry operators, with CAGR estimated at 3.5–4.0%. Stringent EU safety and sustainability regulations are acting as both a compliance driver and an innovation catalyst, with FST-compliant and recycled-material seat systems commanding growing specification share.

Asia Pacific is the fastest-growing regional market, projected to expand at a CAGR of 5.5–6.0% through the forecast period. China's aggressive shipbuilding output, India's coastal ferry development programs, and ASEAN's booming maritime tourism infrastructure are collectively driving demand. Japan and South Korea contribute through advanced naval shipbuilding programs that specify sophisticated seating solutions. The region is expected to close the gap with North America in absolute value terms by the early 2030s.

The Middle East and Africa region is emerging as a growth market, supported by Gulf Cooperation Council investments in luxury marina infrastructure and passenger ferry development across the Red Sea and Arabian Gulf. The GCC sub-region is projected to grow at 4.5–5.0% CAGR, with premium seating demand driven by high-specification passenger vessels serving leisure and tourism routes.

South America remains the smallest regional contributor, with Brazil and Argentina representing the primary markets. Growth is constrained by macroeconomic volatility and limited domestic manufacturing capacity, though Brazil's Amazon river transport network generates consistent demand for durable, low-maintenance commercial seating.

Pricing dynamics in the Marine Passenger Seat Market are shaped by a complex interplay of raw material costs, competitive intensity at the mid-tier, and the premium commanded by technologically differentiated products in military and high-speed commercial applications.

At the product level, average selling prices (ASPs) range from approximately $80–$200 per unit for standard recreational seating to $1,500–$8,000 or more for military-grade shock-absorbing suspension seats. Commercial ferry seating occupies a mid-range band of $300–$1,200 per seat, depending on specification complexity, upholstery grade, and integration of armrests, fold-down mechanisms, and FST-compliant materials.

Margin structures vary significantly across the value chain. OEM seat manufacturers supplying directly to shipbuilders typically operate on gross margins of 18–25%, compressed by volume pricing expectations and the leverage shipbuilders exert in long-term supply negotiations. Aftermarket channels offer higher gross margins of 30–40%, reflecting fragmented competition and the urgency premium paid by vessel operators requiring rapid replacement parts. Distributors such as West Marine capture 15–20% margins by aggregating brands and providing last-mile accessibility.

Cost drivers are concentrated in three areas: raw materials (foam, vinyl, stainless steel, aluminum), labor (particularly for bespoke and upholstery-intensive products), and logistics. Polyurethane foam — a primary input sourced from the Marine Foam and Cushioning Market — experienced peak price increases of 25–30% during 2021–2022 due to MDI isocyanate supply disruptions, and while prices have partially normalized, volatility remains a persistent margin risk. Marine-grade vinyl and leather sourced from the Boat Upholstery Market have similarly fluctuated with petrochemical feedstock cycles.

Competitive intensity at the volume mid-tier is intensifying as Asian manufacturers — particularly from China and Taiwan — expand their export presence with cost-competitive recreational and light commercial seating. This dynamic is compressing ASPs in the $100–$400

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.3% from 2020-2034 |

| Segmentation |

|

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Comprehensive validation mechanisms ensuring market intelligence accuracy, reliability, and adherence to international standards.

500+ data sources cross-validated

200+ industry specialists validation

NAICS, SIC, ISIC, TRBC standards

Continuous market tracking updates

Factors such as are projected to boost the Marine Passenger Seat Market market expansion.

Key companies in the market include The Wise Company, Inc., Todd Marine Products, Tappezzeria Nautica Beggio, Quality Pacific Manufacturing, Inc., Swann Systems Ltd., Ullman Dynamics, Mercury Marine, Thomas Scott Seating Ltd, Springfield Marine Company, West Marine.

The market segments include Ship Type, Component, End User.

The market size is estimated to be USD 1.75 billion as of 2022.

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3690, USD 5820, and USD 9870 respectively.

The market size is provided in terms of value, measured in billion and volume, measured in .

Yes, the market keyword associated with the report is "Marine Passenger Seat Market," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Marine Passenger Seat Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.