1. What are the major growth drivers for the Automotive Fintech Market market?

Factors such as are projected to boost the Automotive Fintech Market market expansion.

Automotive Fintech Market

Automotive Fintech Market

Market Lens IQ is a global market intelligence and strategic consulting firm delivering advanced syndicated research reports, customized industry analysis, competitive intelligence, and data-driven advisory solutions to organizations across international markets. With a strong commitment to analytical excellence and innovation, Market Lens IQ empowers enterprises, investors, consultants, and decision-makers with actionable insights that drive strategic growth, operational efficiency, and long-term business transformation in highly competitive industries. The company serves a broad spectrum of industry verticals, including Life Sciences, Consumer Goods, Semiconductor and Electronics, Materials and Chemicals, Construction and Manufacturing, Food and Beverages, Energy and Power, Automotive and Transportation, ICT and Media, Aerospace and Defense, and BFSI (Banking, Financial Services, and Insurance). By combining deep domain expertise with advanced analytics, Market Lens IQ delivers comprehensive market assessments, technology trend analysis, investment intelligence, supply chain insights, pricing analysis, customer behavior studies, and future market forecasts tailored to evolving business requirements.

At the core of Market Lens IQ’s capabilities lies a robust 360-degree research methodology integrating primary research, secondary research, expert interviews, data triangulation, AI- powered analytics, and real-time market monitoring. Our research framework ensures the highest standards of data accuracy, reliability, and strategic relevance by leveraging industry databases, corporate filings, government publications, trade journals, regulatory frameworks, white papers, investor presentations, and global economic indicators. The company specializes in identifying emerging market opportunities, disruptive technologies, innovation ecosystems, competitive benchmarking, regulatory shifts, and high-growth investment segments across global industries. Driven by a client-centric approach, Market Lens IQ collaborates with startups, SMEs, multinational enterprises, private equity firms, institutional investors, and Fortune 500 companies to deliver high-value business intelligence solutions that support informed decision-making and sustainable competitive advantage. Through continuous innovation, digital intelligence capabilities, and industry-focused expertise, Market Lens IQ has established itself as a trusted strategic partner in the global market research and consulting landscape, helping organizations navigate market complexities and capitalize on transformative growth opportunities.

+1 2315155523

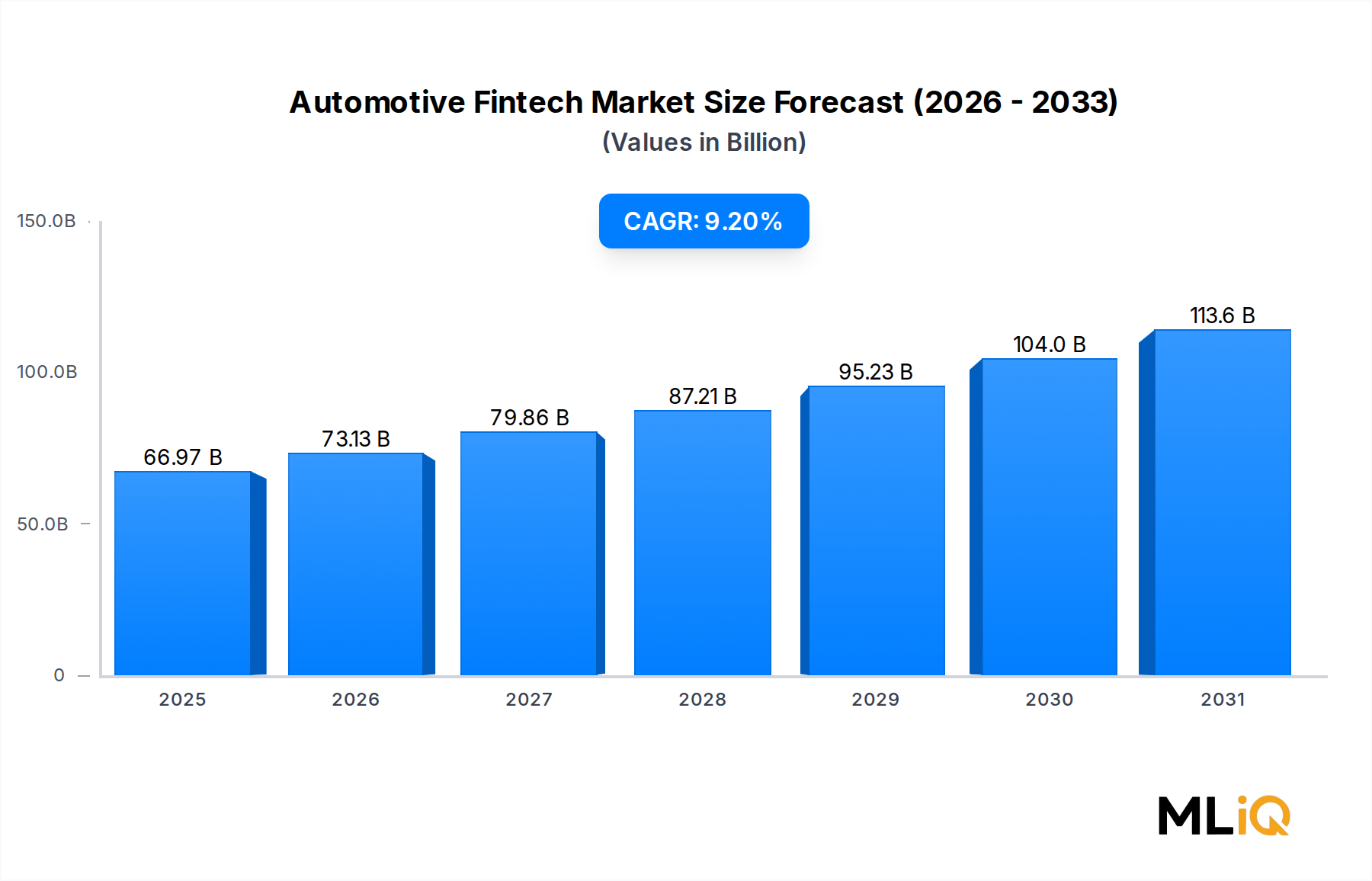

The global Automotive Fintech Market is valued at $66.97 billion in the base year and is projected to expand at a compound annual growth rate of 9.2% through the forecast period of 2025 to 2033. This robust trajectory reflects the deepening convergence of financial technology with automotive ecosystems — spanning vehicle acquisition, insurance, in-vehicle payments, and subscription-based mobility financing.

Several macro tailwinds underpin this growth. The accelerating shift toward electric vehicle adoption is reshaping traditional auto loan and leasing structures, demanding more flexible, data-driven financial products. The proliferation of connected vehicles is enabling real-time transactional capabilities directly within the vehicle cabin, unlocking entirely new revenue streams for financial service providers. Simultaneously, rising consumer preference for digital-first purchasing journeys — from loan origination to insurance policy issuance — is compressing the role of physical dealership finance desks and accelerating platform-based solutions.

Digitally native consumers, particularly millennials and Gen Z, now expect frictionless, mobile-accessible financing options comparable to other consumer fintech verticals. This behavioral shift is compelling both traditional auto lenders and insurgent fintech platforms to invest heavily in AI-driven credit scoring, instant loan decisioning, and embedded insurance modules. The Embedded Finance Market and the Connected Car Finance Market are both converging within the automotive ecosystem, creating overlapping demand layers that amplify total addressable market estimates.

From a segmentation perspective, digital loans and purchase financing commands the largest end-use revenue share, followed closely by online insurance. In-vehicle payments represent the highest-growth sub-segment, driven by telematics integration and the buildout of connected vehicle APIs. Subscription-based channel models are gaining traction, particularly in fleet and commercial vehicle segments, where predictable monthly outflows are preferred over large upfront capital commitments.

Geographically, North America remains the most mature region, benefiting from established credit infrastructure and high smartphone penetration. Asia Pacific, led by China and India, is the fastest-growing region, propelled by rising middle-class vehicle ownership, rapid fintech adoption, and government-backed digital payment initiatives. Europe is experiencing structural transformation driven by regulatory mandates around open banking and data sharing.

Looking forward, the Automotive Fintech Market is expected to increasingly intersect with blockchain-based title management, decentralized credit scoring, and AI-personalized insurance underwriting. Players that integrate across multiple financial product verticals — combining vehicle financing, insurance, payments, and aftersales credit — will achieve superior customer lifetime value and defensible platform positions through 2033.

Among all end-use segments within the Automotive Fintech Market, digital loans and purchase financing commands the dominant revenue share, reflecting both the scale of global vehicle sales and the rapid digitization of the auto credit value chain. This segment encompasses online loan origination, instant credit decisioning, digital dealership financing platforms, and direct-to-consumer auto lending portals.

The dominance of this segment is rooted in fundamental economics: vehicle purchases represent one of the largest discretionary expenditures in a consumer's financial life, and the vast majority of new and used vehicle transactions involve some form of financing. As physical dealership finance offices migrate their workflows online, and as third-party fintech platforms capture an increasing share of loan originations upstream of the dealership, digital loan volumes are compounding rapidly.

Artificial intelligence and machine learning are transforming credit underwriting within this segment. Traditional FICO-based models are being supplemented or replaced by alternative data scoring engines that incorporate employment history, utility payment records, rental payment behavior, and even telematics-derived driving patterns. Companies such as AutoFi Inc. and Creditas Solues Financeiras have built proprietary underwriting frameworks that dramatically reduce time-to-approval — in some cases from days to minutes — while expanding credit access to thin-file and underserved borrower segments.

The Digital Lending Market is a critical adjacent space that feeds talent, technology, and regulatory precedent into automotive-specific platforms. Innovations originating in personal lending fintechs — including open banking data aggregation, automated bank statement analysis, and income verification APIs — have been retooled for automotive use cases, accelerating product development cycles.

For electric vehicles specifically, the financing landscape is evolving distinctly. Battery degradation, residual value uncertainty, and government subsidy structures create unique underwriting challenges. The Electric Vehicle Financing Market is emerging as a specialized sub-vertical, with lenders developing EV-specific loan products that account for federal tax credits, charging infrastructure costs, and battery health assessments. This specialization is creating differentiation opportunities for fintech-native lenders over traditional bank auto finance divisions.

In the commercial vehicle segment, digital fleet financing platforms are gaining ground. Fleet operators increasingly demand integrated solutions that combine asset acquisition financing with telematics monitoring, maintenance cost projections, and real-time utilization data. RouteOne has positioned itself as a connective tissue between dealerships, lenders, and fleet operators in this space, processing millions of financing transactions annually.

The segment's share is not merely holding steady — it is consolidating further as dealer management system integrations deepen and as consumer expectations for fully digital, in-home vehicle buying experiences intensify post-pandemic. With the Mobility-as-a-Service Market expanding and blurring the lines between vehicle ownership and access-based models, digital loan platforms are also adapting to finance subscription and fractional ownership structures, further extending their addressable market. The combination of large ticket sizes, recurring refinancing cycles, and cross-sell opportunities in insurance and service contracts makes digital loans and purchase financing the highest-revenue and most strategically critical segment in the entire Automotive Fintech Market landscape.

The Automotive Fintech Market is shaped by a confluence of powerful structural drivers and notable constraints that collectively define its 9.2% CAGR trajectory through 2033.

Driver 1 — Electric Vehicle Proliferation: EV sales globally surpassed 10 million units in recent years and are projected to represent over 30% of new vehicle sales by 2030. This transition is creating discontinuity in traditional financing models, as EV residual values and total cost of ownership calculations differ materially from internal combustion engine vehicles. Fintech platforms that develop EV-native underwriting and leasing tools are capturing first-mover advantages. The Electric Vehicle Financing Market and the broader Automotive Payments Market are both expanding in direct correlation with EV adoption rates.

Driver 2 — Embedded Finance Integration: The embedding of financial services directly into automotive OEM platforms and dealer management systems is reducing customer acquisition costs for fintech providers. Automakers including major OEMs in Germany and the United States are building proprietary financial services arms, while simultaneously partnering with third-party fintechs to offer insurance, payments, and credit at the point of vehicle configuration. The Embedded Finance Market is enabling seamless financial product delivery within the vehicle purchase and ownership journey.

Driver 3 — Telematics-Driven Insurance Innovation: Usage-based insurance, enabled by onboard diagnostics and connected vehicle data streams, is reshaping auto insurance underwriting. Penetration of usage-based insurance products is growing at double-digit rates in North America and Europe, directly supporting growth in the Usage-Based Insurance Market and the Digital Auto Insurance Market.

Constraint 1 — Regulatory Fragmentation: Divergent lending, insurance, and data privacy regulations across jurisdictions significantly increase compliance costs for automotive fintech platforms operating cross-border. GDPR in Europe, state-level lending regulations in the United States, and evolving data localization requirements in Asia Pacific create complex operational environments.

Constraint 2 — Credit Risk in Emerging Markets: In high-growth markets such as India, Brazil, and Southeast Asia, thin credit file populations and volatile macroeconomic conditions elevate default risk. While alternative data scoring helps, it does not fully eliminate delinquency exposure, constraining aggressive lending expansion.

The competitive landscape of the Automotive Fintech Market is characterized by a heterogeneous mix of fintech startups, established financial institutions with digital arms, and automotive-native platforms. Key participants include:

Grab: Southeast Asia's leading super-app has extended its financial services infrastructure — including digital lending and insurance products — into the automotive vertical, leveraging its vast ride-hailing transaction dataset to underwrite vehicle financing for driver-partners across Indonesia, the Philippines, and other ASEAN markets.

Euroclear: A global leader in financial market infrastructure, Euroclear is exploring blockchain-based automotive asset tokenization and title registry solutions that could fundamentally alter how vehicle collateral is managed and transferred within automotive lending ecosystems.

AutoFi Inc.: A purpose-built automotive fintech platform, AutoFi connects consumers with lenders through dealership-integrated digital financing portals, enabling real-time loan origination and rate comparison at the point of vehicle purchase, serving hundreds of dealership groups and multiple national lenders.

Kuwy Technology Service Private Limited: India-focused automotive lending technology provider that digitizes the vehicle financing workflow for banks, NBFCs, and dealerships, enabling instant credit decisioning and digital document processing in one of the world's fastest-growing auto markets.

By Miles Ltd.: A UK-based pay-per-mile car insurance provider that leverages telematics and connected vehicle data to offer genuinely usage-based insurance products, directly competing within the Digital Auto Insurance Market segment and the broader Usage-Based Insurance Market.

Cuvva: A London-headquartered insurtech offering hourly and short-term vehicle insurance through a mobile-first platform, targeting younger drivers and shared vehicle scenarios that traditional annual policy structures fail to serve efficiently.

The Savings Group: A Brazilian financial technology company focused on automotive financing comparison and digital loan origination, operating in one of Latin America's largest vehicle markets and helping consumers navigate complex credit environments.

ROUTEONE: A joint venture among major automotive captive finance companies, RouteOne provides a dealership financing platform that processes a significant share of all U.S. auto loan applications, serving as critical infrastructure connecting dealerships with over 1,400 financing sources.

Creditas Solues Financeiras: A leading Brazilian digital lender specializing in asset-backed consumer credit, including auto equity loans, deploying AI-driven underwriting to serve underbanked populations with vehicle-secured financing products.

Blinker: A peer-to-peer automotive marketplace and fintech platform that combines vehicle listing, price valuation, and embedded financing into a single mobile application, enabling private-party vehicle transactions with integrated loan origination.

January 2025: AutoFi Inc. announced a strategic integration with a major U.S. dealer management system provider, enabling real-time financing pre-qualification directly within the vehicle configurator workflow, projected to accelerate loan application volumes across its dealership network.

March 2025: By Miles Ltd. secured Series C funding to expand its pay-per-mile insurance platform to continental European markets, marking the company's first significant geographic expansion beyond the United Kingdom and signaling growing investor confidence in the Usage-Based Insurance Market.

April 2025: Kuwy Technology Service Private Limited partnered with three additional public sector banks in India to deploy its automated vehicle loan origination platform, targeting rural and semi-urban dealership networks underserved by traditional digital banking infrastructure.

May 2025: A consortium of European automakers and fintech providers announced a pilot program for blockchain-based vehicle title management, using distributed ledger technology to reduce title fraud and accelerate collateral release in automotive lending — a development with significant implications for the Connected Car Finance Market.

June 2025: Creditas Solues Financeiras expanded its auto equity loan product to include electric vehicles in its collateral eligibility framework, becoming one of Brazil's first digital lenders to explicitly underwrite EV-backed credit products with battery health scoring integration.

August 2025: ROUTEONE launched an enhanced API suite enabling deeper integration between its financing platform and third-party insurtech providers, facilitating bundled financing and insurance quotation within a single dealership transaction workflow.

October 2025: Cuvva introduced a fleet-segment product targeting gig economy platforms, offering dynamic, per-trip insurance coverage for drivers using personal vehicles for commercial purposes — directly addressing a regulatory gap in existing commercial auto insurance frameworks.

The Automotive Fintech Market exhibits pronounced regional heterogeneity in terms of maturity, growth velocity, and dominant product categories.

North America represents the largest single regional market, accounting for an estimated 34–36% of global revenue. The United States anchors this position, supported by the world's most developed auto finance infrastructure, high per-capita vehicle ownership, and mature digital banking penetration. U.S.-based platforms such as AutoFi and RouteOne process tens of millions of financing transactions annually. Canadian and Mexican markets contribute incremental but growing volumes, with Mexico emerging as a key market for digital lending expansion tied to rising vehicle ownership rates. North America's CAGR is estimated at approximately 7.8% through 2033, reflecting high baseline saturation.

Europe is the second-largest region, with the United Kingdom, Germany, and France as primary contributors. The region benefits from strong open banking regulatory frameworks under PSD2, which are enabling automotive fintech platforms to access consumer financial data with explicit consent, dramatically improving credit underwriting precision. The Vehicle Subscription Services Market is particularly active in Germany and the Nordic countries, where flexible ownership models resonate strongly with urban consumers. European regional CAGR is estimated at 8.4%, slightly above North America, driven by EV adoption mandates and digital insurance innovation.

Asia Pacific is the fastest-growing region, projected at a CAGR of approximately 11.5% through 2033. China dominates, driven by the world's largest EV market, massive digital payment infrastructure (WeChat Pay, Alipay), and aggressive fintech investment. India represents the highest long-term growth potential, with vehicle financing penetration still below 55% of new vehicle sales and a rapidly expanding digital banking ecosystem. The Mobility-as-a-Service Market in ASEAN nations is driving demand for flexible micro-mobility financing products. Japan and South Korea contribute premium-segment digital insurance and connected vehicle finance innovation.

South America, led by Brazil and Argentina, is a high-potential but volatile region. Brazil's Creditas and The Savings Group are local champions navigating complex regulatory and macroeconomic environments. Regional CAGR is estimated at 9.0%.

Middle East and Africa, while currently the smallest region by absolute value, is growing rapidly through GCC digital banking initiatives and South Africa's maturing fintech ecosystem, with a projected CAGR of 10.2%.

Pricing dynamics within the Automotive Fintech Market are shaped by intense competition across the lending, insurance, and payments sub-segments, with margin structures varying significantly by product type and geographic market.

In digital auto lending, net interest margins (NIMs) have come under sustained pressure as fintech lenders compete aggressively on rate to win loan originations away from traditional bank and captive finance channels. The commoditization of loan comparison platforms — where consumers receive multiple competing offers within seconds — has effectively created rate auctions at the point of financing, compressing spreads particularly on prime borrower segments. Fintech lenders are responding by migrating toward non-prime and thin-file borrower segments, where alternative data scoring provides a proprietary underwriting advantage and interest rate spreads remain wider, albeit at higher credit risk.

The Digital Lending Market and the Connected Car Finance Market are both experiencing platform fee compression as dealer management system integrations become more standardized, reducing the incremental value proposition of API connectivity alone. Sustainable margin structures increasingly depend on cross-selling ancillary products — extended warranties, GAP insurance, and service contracts — which carry higher attach rates and better unit economics than raw loan origination fees.

In digital insurance, the usage-based and pay-per-mile models are disrupting traditional annual premium structures. While telematics-enabled pricing improves actuarial precision and reduces adverse selection losses, the operational costs of real-time data collection, processing, and model maintenance are non-trivial, creating margin dilution during scale-up phases. Mature platforms within the Digital Auto Insurance Market are achieving operating leverage as customer bases grow, but early-stage insurtech players face persistent combined ratios above 100% as they build claims history.

In-vehicle payments represent the highest-margin sub-segment due to low variable costs per transaction once infrastructure is established, analogous to payment network economics. The Automotive

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 9.2% from 2020-2034 |

| Segmentation |

|

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Comprehensive validation mechanisms ensuring market intelligence accuracy, reliability, and adherence to international standards.

500+ data sources cross-validated

200+ industry specialists validation

NAICS, SIC, ISIC, TRBC standards

Continuous market tracking updates

Factors such as are projected to boost the Automotive Fintech Market market expansion.

Key companies in the market include Grab, Euroclear, AutoFi Inc., Kuwy Technology Service Private Limited, By Miles Ltd., Cuvva, The Savings Group, Inc., ROUTEONE, Creditas Solues Financeiras, Blinker, Inc.

The market segments include End Use, Channel, Vehicle Type, Propulsion Type.

The market size is estimated to be USD 66.97 billion as of 2022.

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3570, USD 5730, and USD 9600 respectively.

The market size is provided in terms of value, measured in billion and volume, measured in .

Yes, the market keyword associated with the report is "Automotive Fintech Market," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Automotive Fintech Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.