1. What are the major growth drivers for the Marine Shaft Power Meter Market market?

Factors such as are projected to boost the Marine Shaft Power Meter Market market expansion.

+1 2315155523

Marine Shaft Power Meter Market

Marine Shaft Power Meter Market

Market Lens IQ is a global market intelligence and strategic consulting firm delivering advanced syndicated research reports, customized industry analysis, competitive intelligence, and data-driven advisory solutions to organizations across international markets. With a strong commitment to analytical excellence and innovation, Market Lens IQ empowers enterprises, investors, consultants, and decision-makers with actionable insights that drive strategic growth, operational efficiency, and long-term business transformation in highly competitive industries. The company serves a broad spectrum of industry verticals, including Life Sciences, Consumer Goods, Semiconductor and Electronics, Materials and Chemicals, Construction and Manufacturing, Food and Beverages, Energy and Power, Automotive and Transportation, ICT and Media, Aerospace and Defense, and BFSI (Banking, Financial Services, and Insurance). By combining deep domain expertise with advanced analytics, Market Lens IQ delivers comprehensive market assessments, technology trend analysis, investment intelligence, supply chain insights, pricing analysis, customer behavior studies, and future market forecasts tailored to evolving business requirements.

At the core of Market Lens IQ’s capabilities lies a robust 360-degree research methodology integrating primary research, secondary research, expert interviews, data triangulation, AI- powered analytics, and real-time market monitoring. Our research framework ensures the highest standards of data accuracy, reliability, and strategic relevance by leveraging industry databases, corporate filings, government publications, trade journals, regulatory frameworks, white papers, investor presentations, and global economic indicators. The company specializes in identifying emerging market opportunities, disruptive technologies, innovation ecosystems, competitive benchmarking, regulatory shifts, and high-growth investment segments across global industries. Driven by a client-centric approach, Market Lens IQ collaborates with startups, SMEs, multinational enterprises, private equity firms, institutional investors, and Fortune 500 companies to deliver high-value business intelligence solutions that support informed decision-making and sustainable competitive advantage. Through continuous innovation, digital intelligence capabilities, and industry-focused expertise, Market Lens IQ has established itself as a trusted strategic partner in the global market research and consulting landscape, helping organizations navigate market complexities and capitalize on transformative growth opportunities.

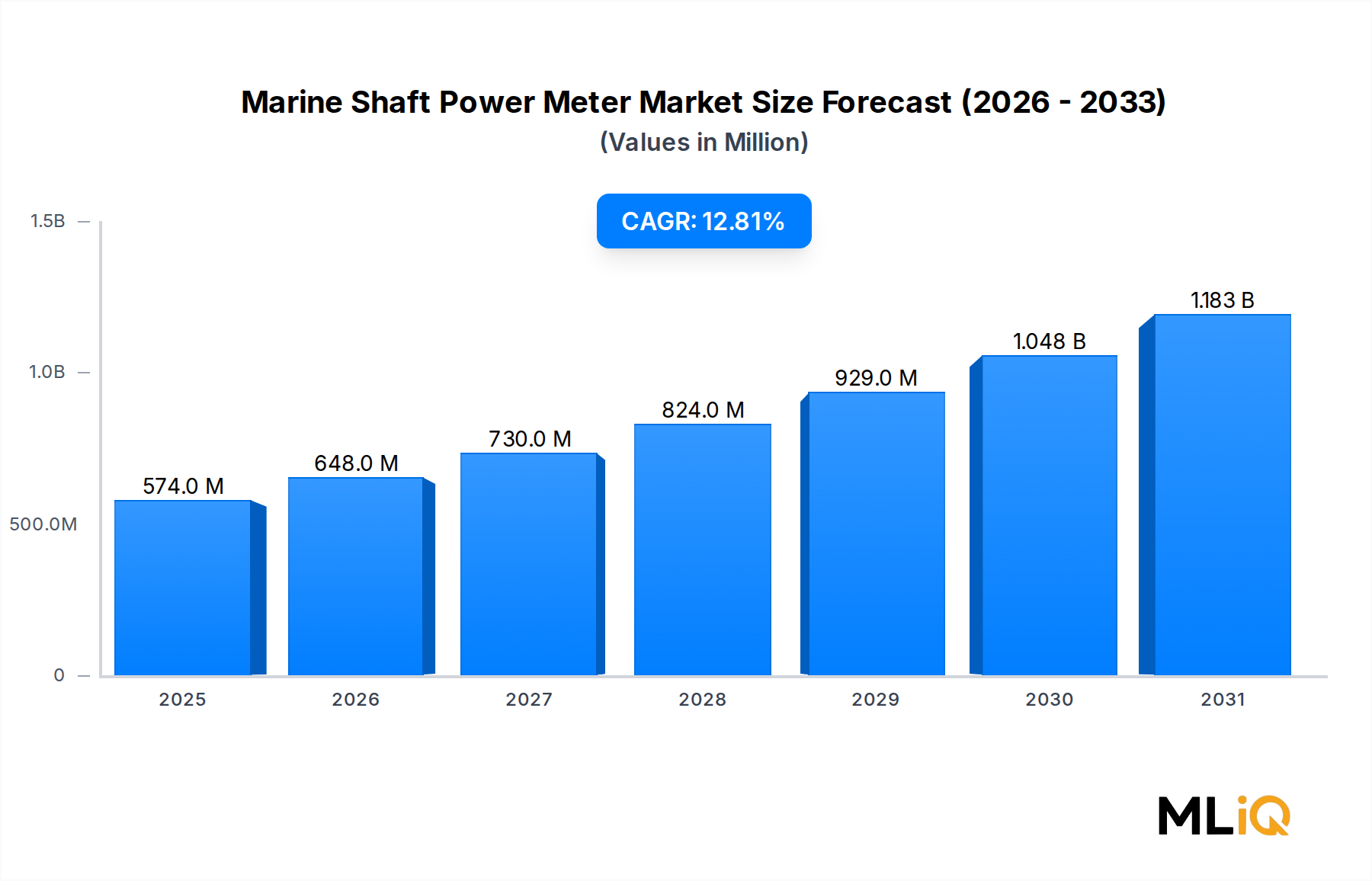

The global Marine Shaft Power Meter Market is valued at $574.1 million in 2025 and is projected to expand at a compound annual growth rate (CAGR) of 12.8% through 2033, reaching an estimated $1,512 million by the end of the forecast period. This robust trajectory is underpinned by a confluence of regulatory mandates, digital transformation in maritime operations, and escalating fuel efficiency imperatives across the global fleet.

Shaft power meters, which measure the mechanical power transmitted through a vessel's propeller shaft, have become indispensable instrumentation in the context of the International Maritime Organization's (IMO) Energy Efficiency Existing Ship Index (EEXI) and Carbon Intensity Indicator (CII) regulations. These frameworks, which became enforceable in January 2023, require shipowners to demonstrate measurable reductions in carbon intensity, directly elevating demand for certified shaft power metering solutions.

Key demand drivers include the accelerating retrofit cycle across the global fleet — estimated at over 50,000 vessels — as operators seek compliance-grade instrumentation to satisfy port state control inspections. The transition from analogue to digital display architectures is also reshaping procurement patterns, with digital solutions commanding premium pricing and higher margin profiles. Integration with vessel performance management platforms and fleet data analytics ecosystems has further elevated the strategic importance of shaft power meters beyond mere compliance tools.

Macro tailwinds reinforcing market growth include surging global trade volumes, expanding LNG carrier orderbooks, and heightened investment in green shipping corridors across Asia Pacific and Northern Europe. The rapid penetration of remote condition monitoring and predictive maintenance platforms is creating secondary demand cycles, as operators replace legacy instrumentation with networked, IoT-compatible shaft power measurement systems.

The competitive landscape is moderately consolidated, with established metrology and marine instrumentation specialists holding dominant positions. However, the entry of digitally native technology firms and the growing influence of classification society requirements are reshaping competitive dynamics. The aftermarket segment is experiencing particularly elevated activity as fleet operators accelerate mid-life retrofits to meet emissions benchmarks.

Looking ahead through 2033, the Marine Shaft Power Meter Market is expected to benefit from the proliferation of autonomous and semi-autonomous vessel programs, which demand high-fidelity, continuous shaft power data for propulsion optimization algorithms. The convergence of shaft power metering with broader vessel energy management ecosystems positions this market at the intersection of regulatory compliance, operational efficiency, and digital maritime transformation.

Among the vessel type segments defined within the Marine Shaft Power Meter Market — comprising passenger vessels, cargo carriers, tankers, container ships, and others — cargo carriers represent the single largest revenue-generating category, accounting for an estimated 38–42% of total market revenue in 2025. This dominance reflects the sheer numerical scale of bulk carriers, general cargo vessels, and multipurpose freighters in the global operational fleet, as well as the high retrofit intensity driven by IMO compliance mandates targeting this class.

Cargo carriers, which number in excess of 12,000 active vessels globally according to Clarksons Research, are disproportionately subject to CII rating pressures due to their variable operational profiles and fuel-intensive propulsion systems. The CII framework grades vessels on an A–E scale annually, and cargo carriers — given their longer voyages and higher annual fuel consumption relative to smaller coastal vessels — face greater urgency to instrument shaft power accurately. Class societies including DNV, Lloyd's Register, and Bureau Veritas have issued technical guidance specifically encouraging shaft power metering as a preferred method of engine power limitation (EPL) under EEXI compliance pathways, further reinforcing demand within this segment.

The retrofit dynamic within cargo carriers is particularly strong. Unlike newbuilds, where shaft power meters can be specified during design, the existing cargo fleet requires aftermarket installation. This aftermarket activity is characterized by short installation windows during scheduled dry-dockings, creating concentrated procurement cycles that major suppliers have structured their service networks to address. Companies such as Datum Electronics and Kyma AS have developed installation programs specifically optimized for the cargo carrier retrofit environment, including non-invasive strain gauge configurations that minimize shaft modification requirements.

Within cargo carriers, the dry bulk sub-segment — encompassing Capesize, Panamax, and Handymax vessels — exhibits the highest absolute volume of shaft power meter installations, driven by the large fleet size and the relatively thin operating margins that make fuel efficiency instrumentation economically attractive. Tankers, while often categorized separately, share significant technical overlap with cargo carriers in their shaft power metering requirements, particularly among product tankers and chemical carriers operating on irregular spot trading patterns.

The dominance of cargo carriers in the Marine Shaft Power Meter Market is not merely a function of fleet size but also reflects the economics of return on investment. For a Panamax bulk carrier consuming approximately 25–30 metric tons of fuel per day at sea, a 1–2% improvement in propulsion efficiency enabled by real-time shaft power monitoring translates to annual fuel savings of $150,000–$200,000 at prevailing VLSFO prices, making the instrumentation cost — typically $15,000–$40,000 per installation — highly justifiable.

Market share within the cargo carrier segment is consolidating around suppliers capable of providing classification society-approved systems with integrated data logging and remote reporting capabilities. The ability to interface shaft power data with third-party voyage optimization platforms — such as those offered by Wartsila, ABB Marine, and Nauticus — is increasingly a differentiating requirement in procurement decisions. As CII rating cycles intensify through 2026 and 2027, cargo carrier operators face escalating pressure to demonstrate continuous monitoring capability, sustaining elevated demand for certified shaft power measurement systems within this segment.

The Marine Shaft Power Meter Market is governed by a well-defined set of structural drivers and countervailing constraints, each traceable to specific regulatory, technological, or macroeconomic conditions.

Primary Driver — IMO Regulatory Framework: The EEXI and CII regulations, mandatory since January 2023, have created a non-discretionary demand baseline. Under EEXI, vessels must demonstrate compliance with energy efficiency ratios, and shaft power limitation — verified through certified power metering — is among the most cost-effective compliance pathways. The IMO's target of a 40% reduction in carbon intensity by 2030 relative to 2008 levels ensures sustained regulatory pressure throughout the forecast period.

Primary Driver — Fleet Renewal and Retrofit Activity: The global merchant fleet's average age exceeds 12 years, and approximately 3,500–4,000 vessels enter scheduled dry-dock annually. Each dry-docking represents a retrofit opportunity, and classification society requirements increasingly mandate shaft power metering installations during these events. This cyclical demand provides measurable revenue predictability for market participants.

Secondary Driver — Fuel Price Volatility: Marine fuel costs constitute 40–60% of vessel operating expenses. With VLSFO prices oscillating between $550–$750 per metric ton since 2022, operators have demonstrated heightened willingness to invest in efficiency instrumentation with demonstrable payback periods under 24 months.

Primary Constraint — High Installation and Calibration Costs: Initial installation costs for certified shaft power meter systems — ranging from $15,000 to $60,000 depending on shaft diameter and system complexity — represent a significant capital outlay for smaller operators managing fleets of coastal or regional vessels. Calibration requirements mandated by classification societies add recurring operational costs, creating friction in total cost of ownership calculations for price-sensitive segments.

Secondary Constraint — Technical Complexity in Retrofit Environments: Older vessels with non-standard shaft configurations present engineering challenges that increase installation time and cost, potentially deterring investment in vessels approaching end-of-life status.

The competitive landscape of the Marine Shaft Power Meter Market is characterized by a mix of specialized marine instrumentation firms, diversified industrial technology groups, and emerging digital-maritime entrants. The following profiles outline the strategic positioning of key participants:

Aalberts Industries (VAF Instruments): A subsidiary of Dutch industrial conglomerate Aalberts Industries, VAF Instruments is one of the most recognized brands in marine shaft power metering, offering a comprehensive portfolio of torsiometer-based power measurement systems approved by major classification societies. The company leverages its parent group's global distribution network to maintain strong aftermarket presence across European and Asian shipyards.

Hoppe Marine: A German manufacturer specializing in marine measurement technology, Hoppe Marine offers shaft power meters integrated within broader tank gauging and cargo management platforms. The company's strength lies in providing bundled instrumentation solutions that reduce integration complexity for fleet operators.

Kyma AS: A Norwegian technology company, Kyma AS provides shaft power measurement systems designed for seamless integration with vessel performance management software. Its focus on data connectivity and cloud-based analytics positions it favorably in the emerging digital-maritime segment of the market.

Datum Electronics: A UK-based specialist in torque and power measurement, Datum Electronics serves both marine and industrial markets with high-accuracy shaft power systems. The company has developed non-contact measurement technologies that facilitate installation on difficult shaft configurations without requiring vessel dry-docking.

Shoyo Engineering: A Japanese manufacturer serving the Asia Pacific fleet, Shoyo Engineering offers competitively priced shaft power meters aligned with classification society requirements in Japan and South Korea. The company benefits from strong relationships with domestic shipyards and ship management companies.

Trelleborg Marine Systems: Part of the Trelleborg Group, this division extends its marine systems expertise into power measurement instrumentation. Trelleborg's global service network supports lifecycle maintenance contracts across major port hubs.

Aquametro Oil & Marine: A Swiss-headquartered measurement technology company, Aquametro Oil & Marine provides shaft power meters alongside fuel flow measurement systems, enabling integrated energy efficiency monitoring packages appealing to operators seeking consolidated data acquisition.

Kongsberg Maritime: A division of the Norwegian Kongsberg Group, Kongsberg Maritime integrates shaft power measurement within its K-IMS (Kongsberg Integrated Machinery System) ecosystem, targeting high-specification newbuild projects and naval vessel programs where full propulsion monitoring integration is required.

January 2023: IMO EEXI and CII regulations entered into force, triggering an industry-wide surge in shaft power meter procurement as shipowners sought compliant energy efficiency verification methods, with order backlogs at leading suppliers reportedly extending to 6–9 months within the first quarter.

March 2023: Kongsberg Maritime announced an expanded partnership with a major European cruise operator to integrate shaft power metering data into its vessel performance optimization platform across a fleet of 14 vessels, representing one of the largest single fleet instrumentation contracts disclosed in the period.

September 2023: Datum Electronics launched its next-generation Series 420 shaft power meter featuring wireless data transmission capability, reducing installation complexity and enabling real-time integration with third-party fleet management systems.

February 2024: The European Union's FuelEU Maritime regulation was formally published, establishing greenhouse gas intensity targets for vessels calling at EU ports from 2025, further expanding the addressable market for certified shaft power measurement systems in European trade routes.

June 2024: Kyma AS secured certification from DNV for its KM-P shaft power system under revised DNV rules aligned with IMO CII calculation methodologies, enabling direct use of measured shaft power data in official CII reporting submissions.

November 2024: Aquametro Oil & Marine introduced an integrated shaft power and fuel consumption monitoring package targeting small-to-medium vessel operators, priced at a 20–25% discount to comparable standalone systems.

March 2025: The IMO Marine Environment Protection Committee (MEPC 82) confirmed enhanced CII correction factors for specific vessel types, requiring re-calibration of monitoring baselines and stimulating replacement demand for updated metering systems across affected vessel classes.

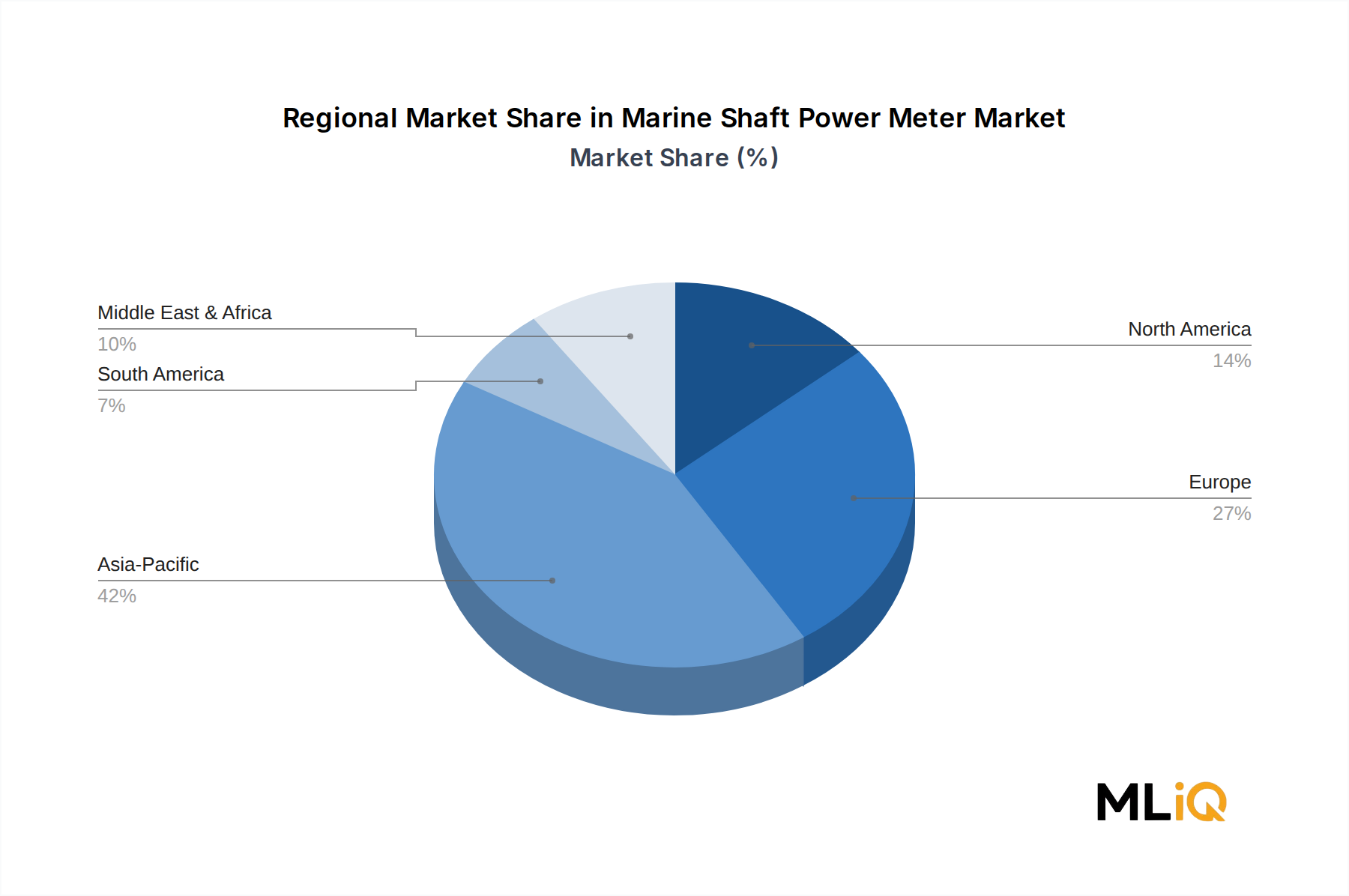

The Marine Shaft Power Meter Market exhibits distinct regional dynamics shaped by fleet concentration, regulatory enforcement intensity, and shipbuilding activity.

Asia Pacific: The dominant regional market, Asia Pacific accounts for approximately 42–45% of global revenue in 2025, driven by the concentration of the world's largest merchant fleets under Chinese, Japanese, South Korean, and Singaporean management. China alone operates over 6,000 ocean-going vessels and hosts the world's largest shipbuilding capacity. The regional CAGR is estimated at 14.2%, the highest globally, reflecting both newbuild specification activity and aggressive retrofit programs among Chinese state-owned shipping enterprises responding to IMO and domestic environmental regulations. Japan and South Korea contribute significant volumes through their technically sophisticated ship management sectors.

Europe: Europe represents approximately 28–30% of global market revenue, with the Nordic countries — Norway, Denmark, Sweden, and Finland — constituting the most technically advanced cluster. European operators face dual compliance pressure from IMO regulations and the EU ETS (Emissions Trading System), which incorporated shipping from January 2024. The regional CAGR is estimated at 11.5%. Germany, Greece (via vessel management entities), and the UK are key demand centers. Europe is considered the most mature regional market, characterized by high instrumentation penetration and strong aftermarket service activity.

North America: North America holds approximately 12–14% of global market revenue, driven primarily by the United States' Jones Act fleet and offshore support vessel sector. The regional CAGR is estimated at 10.8%. Regulatory drivers include USCG emissions monitoring requirements and growing adoption of IMO standards by vessels operating in international trade.

Middle East & Africa: This region accounts for approximately 8–10% of global revenue, with growth concentrated in GCC states operating large tanker fleets through national carriers such as ADNOC Logistics and National Shipping Company of Saudi Arabia. The regional CAGR is estimated at 13.1%, reflecting fleet expansion programs and increasing regulatory alignment with IMO frameworks.

South America: Contributing approximately 5–6% of global revenue, South America's market is led by Brazil's offshore and tanker fleet. Growth is moderate at an estimated CAGR of 9.5%, constrained by economic volatility but supported by Petrobras fleet modernization programs.

The supply chain supporting the Marine Shaft Power Meter Market is characterized by moderate upstream complexity, with critical dependencies on precision-engineered components sourced from specialized global suppliers. Understanding these dynamics is essential for assessing production cost stability and delivery reliability.

The principal raw material inputs include piezoelectric crystals and strain gauge alloys used in torque transducers, high-grade stainless steel for shaft mounting hardware, printed circuit board assemblies incorporating application-specific integrated circuits (ASICs), and tempered optical glass for display modules. Among these, strain gauge alloys — typically nickel-chromium or constantan compositions — are subject to non-ferrous metal price cycles. Nickel prices experienced significant volatility between 2021 and 2023, with LME spot prices ranging from $9,000 to $48,000 per metric ton, introducing meaningful input cost uncertainty for manufacturers.

Semiconductor components, particularly precision analog-to-digital converters and signal conditioning ICs essential for measurement accuracy, remain a structural supply chain vulnerability. The 2021–2023 global semiconductor shortage extended lead times for marine instrumentation components to 26–52 weeks, forcing several manufacturers to redesign products around alternative chip architectures or maintain elevated safety stock. While lead times normalized through 2024, geopolitical concentration of advanced semiconductor fabrication in Taiwan and South Korea represents an ongoing procurement risk.

Printed circuit board assemblies are predominantly sourced from contract manufacturers in China, Malaysia, and Vietnam. The imposition of US Section 301 tariffs on Chinese electronics components and the EU's own supply chain diversification initiatives have prompted several European manufacturers to qualify alternative PCB assembly suppliers in Eastern Europe and Southeast Asia, adding qualification cost but reducing single-country dependency.

Optical and display component sourcing is relatively stable, with multiple qualified suppliers in Japan, Germany, and China. However, precision calibration equipment — required both in manufacturing and field service contexts — is concentrated among a small number of specialist suppliers in Europe and Japan, creating potential bottlenecks during periods of high demand.

Historically, supply chain disruptions most severely affected the Marine Shaft Power Meter Market during 2021–2022, when pandemic-related logistics constraints

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 12.8% from 2020-2034 |

| Segmentation |

|

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Comprehensive validation mechanisms ensuring market intelligence accuracy, reliability, and adherence to international standards.

500+ data sources cross-validated

200+ industry specialists validation

NAICS, SIC, ISIC, TRBC standards

Continuous market tracking updates

Factors such as are projected to boost the Marine Shaft Power Meter Market market expansion.

Key companies in the market include Aalberts Industries (VAF Instruments), Hoppe Marine, Kyma AS, Datum Electronics, Shoyo Engineering, Trelleborg Marine Systems, Aquametro Oil & Marine, Kongsberg Maritie.

The market segments include Vessel Type, Display Type, Sales Channel.

The market size is estimated to be USD 574.1 million as of 2022.

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3690, USD 5820, and USD 9870 respectively.

The market size is provided in terms of value, measured in million and volume, measured in .

Yes, the market keyword associated with the report is "Marine Shaft Power Meter Market," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Marine Shaft Power Meter Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.