1. What are the major growth drivers for the OEM Retractable Roof System Market market?

Factors such as are projected to boost the OEM Retractable Roof System Market market expansion.

+1 2315155523

OEM Retractable Roof System Market

OEM Retractable Roof System Market

Market Lens IQ is a global market intelligence and strategic consulting firm delivering advanced syndicated research reports, customized industry analysis, competitive intelligence, and data-driven advisory solutions to organizations across international markets. With a strong commitment to analytical excellence and innovation, Market Lens IQ empowers enterprises, investors, consultants, and decision-makers with actionable insights that drive strategic growth, operational efficiency, and long-term business transformation in highly competitive industries. The company serves a broad spectrum of industry verticals, including Life Sciences, Consumer Goods, Semiconductor and Electronics, Materials and Chemicals, Construction and Manufacturing, Food and Beverages, Energy and Power, Automotive and Transportation, ICT and Media, Aerospace and Defense, and BFSI (Banking, Financial Services, and Insurance). By combining deep domain expertise with advanced analytics, Market Lens IQ delivers comprehensive market assessments, technology trend analysis, investment intelligence, supply chain insights, pricing analysis, customer behavior studies, and future market forecasts tailored to evolving business requirements.

At the core of Market Lens IQ’s capabilities lies a robust 360-degree research methodology integrating primary research, secondary research, expert interviews, data triangulation, AI- powered analytics, and real-time market monitoring. Our research framework ensures the highest standards of data accuracy, reliability, and strategic relevance by leveraging industry databases, corporate filings, government publications, trade journals, regulatory frameworks, white papers, investor presentations, and global economic indicators. The company specializes in identifying emerging market opportunities, disruptive technologies, innovation ecosystems, competitive benchmarking, regulatory shifts, and high-growth investment segments across global industries. Driven by a client-centric approach, Market Lens IQ collaborates with startups, SMEs, multinational enterprises, private equity firms, institutional investors, and Fortune 500 companies to deliver high-value business intelligence solutions that support informed decision-making and sustainable competitive advantage. Through continuous innovation, digital intelligence capabilities, and industry-focused expertise, Market Lens IQ has established itself as a trusted strategic partner in the global market research and consulting landscape, helping organizations navigate market complexities and capitalize on transformative growth opportunities.

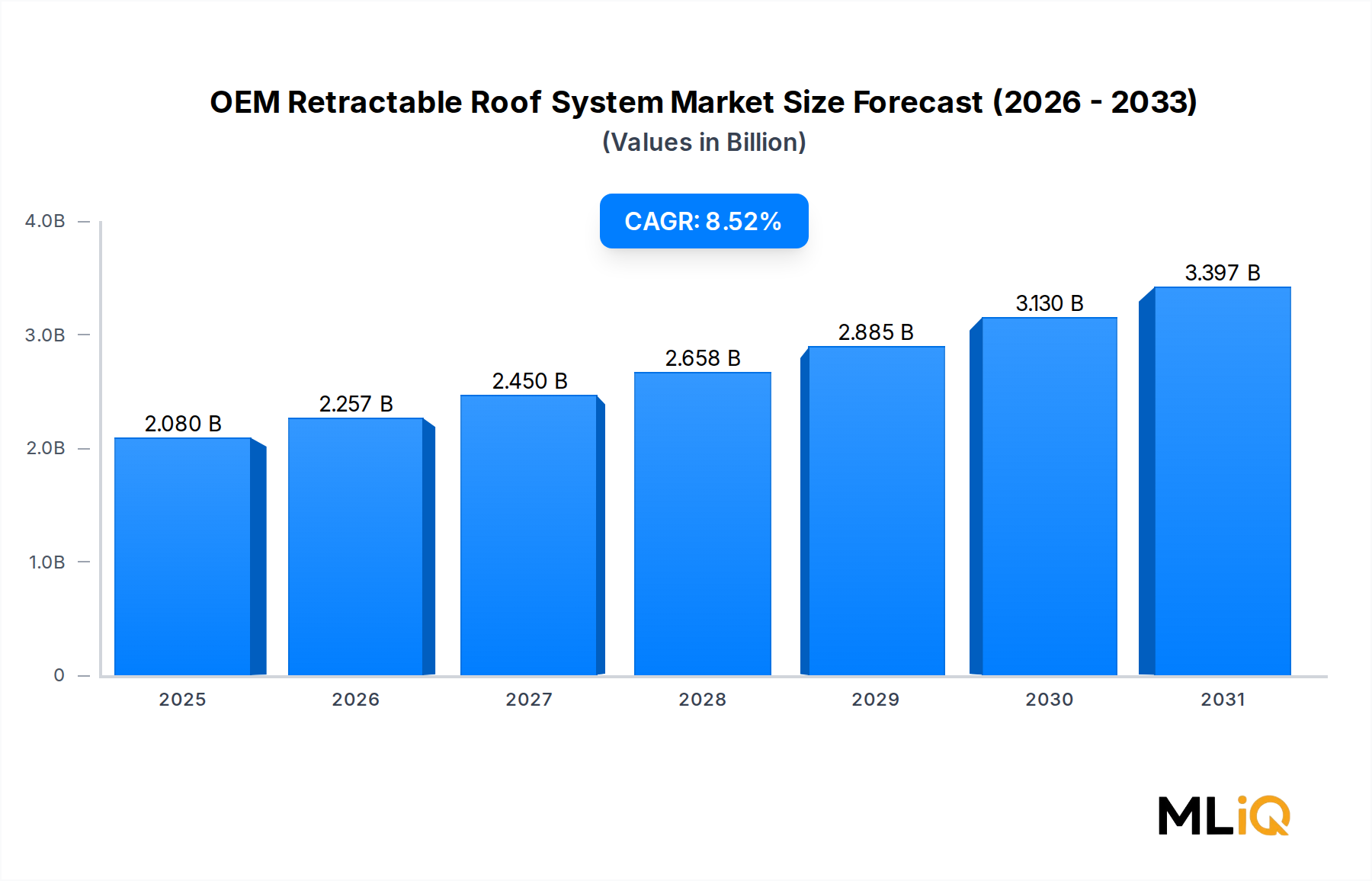

The global OEM Retractable Roof System Market was valued at $2.08 billion in 2024 and is projected to expand at a compound annual growth rate of 8.52% through the forecast period, reflecting robust structural demand across both premium and mainstream vehicle segments. This trajectory positions the market to potentially exceed $4.5 billion by 2032, driven by converging consumer lifestyle preferences, automaker differentiation strategies, and rapid electrification of premium vehicle platforms.

Retractable roof systems have evolved from niche luxury accessories to mainstream engineering solutions that automakers deploy to command margin premiums, reinforce brand identity, and meet increasingly sophisticated consumer expectations around open-air driving experiences. The integration of retractable systems into battery electric vehicles (BEVs) and plug-in hybrid electric vehicles (PHEVs) represents a particularly significant growth vector, as electrified platforms eliminate combustion-engine packaging constraints and allow more flexible roof architecture design.

Key demand drivers include rising global disposable income concentrated in urban populations across Asia Pacific and North America, the proliferation of crossover utility vehicles (CUVs) and sports utility vehicles (SUVs) that now incorporate panoramic and retractable variants, and aggressive OEM investment in open-top derivative models to extend nameplates. Regulatory tailwinds related to lightweighting — driven by both fuel economy mandates and electric range optimization — are accelerating material substitution toward aluminum and polycarbonate composites within roof assemblies.

The passenger car segment remains the dominant end-use application, accounting for the majority of revenue share; however, the light commercial vehicle segment is exhibiting faster incremental growth, particularly in lifestyle-oriented pickup truck and van derivatives entering premium trim configurations. Geographically, Europe currently holds the largest revenue share due to the density of premium automotive manufacturing, while Asia Pacific is the fastest-growing region, led by Chinese domestic OEM investment in premium open-top models.

From a competitive standpoint, the market is moderately consolidated, with Webasto Group, Magna International Inc., and Inalfa Roof Systems Group B.V collectively controlling a substantial share of global OEM supply agreements. Tier 1 suppliers are increasingly positioning themselves as full-system integrators — offering design, engineering, sealing, actuation, and glazing as a bundled solution — to deepen OEM relationships and raise switching costs. Strategic acquisitions, joint development agreements with electric vehicle startups, and co-engineering partnerships with glazing and actuation specialists are reshaping the competitive landscape heading into 2025 and beyond.

The market outlook remains firmly positive, supported by a structural shift toward personalization in automotive purchasing, the democratization of premium roof features into mid-market vehicles, and continued R&D investment in noise-vibration-harshness (NVH) performance, aerodynamic efficiency, and smart actuation technologies.

Within the OEM Retractable Roof System Market, the hard-top roof system sub-segment commands the largest revenue share and continues to consolidate its position as the preferred configuration among OEM procurement teams and end consumers. Hard-top retractable systems — characterized by rigid folding panels constructed from aluminum, steel, or polycarbonate — deliver superior noise insulation, structural rigidity, all-weather usability, and a premium aesthetic that soft-top alternatives structurally cannot replicate.

The dominance of hard-top systems is rooted in several mutually reinforcing factors. First, NVH performance has become a non-negotiable benchmark in the premium vehicle segment, and hard-top systems achieve NVH ratings far closer to conventional fixed-roof vehicles than fabric alternatives. As electric vehicles, which are inherently quieter powertrains, increasingly adopt retractable roof configurations, NVH performance differentials between hard-top and soft-top designs are amplified — further tilting procurement decisions toward rigid panel systems.

Second, the hard-top category benefits from strong alignment with the luxury and near-luxury passenger car segments, which generate disproportionately high gross margins per unit. OEMs including BMW (with its 4 Series Convertible), Mercedes-Benz (C-Class and E-Class Cabriolet derivatives), Porsche, and Audi deploy hard-top retractable systems as the technological centerpiece of open-top flagship models. These vehicles command transaction prices 30–60% above their coupe or sedan equivalents, creating strong economic incentives for OEMs to invest in next-generation hard-top engineering.

Third, material innovation is enabling hard-top systems to overcome their traditional weight disadvantage relative to soft-top configurations. The incorporation of polycarbonate glazing panels — which are approximately 40% lighter than equivalent glass — alongside aluminum structural frames has reduced hard-top assembly weight significantly, making these systems compatible with mass and range-sensitive BEV platforms. The ongoing transition from steel-intensive designs to aluminum-dominant architectures is a primary cost and weight driver reshaping supplier sourcing strategies across the segment.

Key players concentrating their product development resources in the hard-top sub-segment include Webasto Group, which has historically led the market in folding hard-top module supply; Magna International Inc., whose Cosma International and Magna Exteriors divisions provide aluminum structural components and system integration; and Inalfa Roof Systems Group B.V, which has expanded its hard-top capabilities through dedicated engineering centers in Europe and Asia. BOS Group and Valmet Automotive Inc. also participate in hard-top manufacturing, with Valmet leveraging its vehicle manufacturing expertise to offer complete convertible vehicle production services.

Geographically, hard-top system demand is most concentrated in Europe and North America, where the buyer demographics for premium convertibles are most developed. However, China is rapidly emerging as a significant growth market, with domestic OEMs such as BYD, NIO, and Li Auto incorporating hard-top retractable features into premium electric models to differentiate at launch. This regional diversification of hard-top demand is expected to sustain above-market growth for the sub-segment through the forecast horizon.

The hard-top sub-segment's share is not merely holding steady — it is actively expanding as OEMs extend retractable hard-top features into new vehicle categories, including compact crossovers and electric roadsters. This democratization trajectory, combined with continued engineering refinement in actuation speed, stack height, and NVH, positions hard-top systems as the structural growth engine of the broader OEM Retractable Roof System Market.

The OEM Retractable Roof System Market is shaped by a defined set of quantifiable drivers and structural constraints that collectively determine the pace and character of market expansion.

Primary drivers include the accelerating electrification of premium vehicle platforms. BEV and PHEV models represented approximately 18% of global new vehicle sales in 2024, a figure projected to exceed 35% by 2030 according to industry forecasts. Electrified platforms offer flatter underbody architectures and reduced powertrain intrusion into the passenger compartment, creating architectural freedom that OEM engineers are exploiting to introduce retractable roof variants across new model lines. This platform-level structural shift is translating directly into new RFQ (request for quotation) activity for Tier 1 roof system suppliers.

Consumer preference data consistently identifies open-air driving experience as a leading premium feature driver. In surveyed markets across North America and Western Europe, more than 45% of luxury vehicle buyers indicate willingness to pay a premium of $3,000–$8,000 for a factory-integrated retractable roof option. This robust willingness-to-pay metric sustains OEM investment in retractable roof engineering despite higher per-unit development costs relative to fixed-roof configurations.

Lightweighting mandates represent both a driver and a technical enabler. Fleet-average CO₂ targets in the European Union — set at 93.6 g/km for 2025 — are compelling OEMs to reduce vehicle mass across all subsystems. Roof assemblies, which can account for 15–25 kg of vehicle weight depending on design, are prime lightweighting targets. This regulatory pressure is directly accelerating substitution of steel components with aluminum alloys and polycarbonate glazing within retractable roof assemblies.

Key constraints include high system complexity and associated cost. A fully integrated hard-top retractable roof system carries an estimated average selling price of $1,500–$4,000 per vehicle at the OEM level, representing a significant bill-of-materials burden that limits adoption in volume-market vehicle segments. Supply chain complexity — involving precision aluminum stampings, hydraulic or electromechanical actuators, multi-layer sealing systems, and glazing — introduces quality and lead-time risks that constrain OEM rollout velocity. Additionally, increasing raw material price volatility for aluminum and engineering polymers creates margin pressure for Tier 1 suppliers navigating fixed-price OEM supply agreements.

The competitive landscape of the OEM Retractable Roof System Market features a mix of global Tier 1 automotive suppliers, specialty roof system integrators, and material-technology companies operating across design, manufacturing, and system integration dimensions.

AAS Automotive s.r.o.: A specialized manufacturer of convertible roof systems and components with deep engineering capabilities in soft-top and hard-top mechanisms, serving European OEM customers with bespoke roof solutions.

Webasto Group: The global market leader in automotive roof systems, Webasto maintains the broadest portfolio of retractable, panoramic, and sunroof products and holds long-standing OEM supply agreements with major German, American, and Asian automakers.

Covestro AG: A leading supplier of high-performance polycarbonate materials used in automotive glazing and lightweight roof panel applications, Covestro's Makrolon portfolio is widely specified in retractable roof glazing systems for its combination of optical clarity, impact resistance, and weight advantage over glass.

BOS Group: Specializes in shading systems, roller blinds, and auxiliary roof mechanisms, BOS Group serves as a Tier 1 and Tier 2 supplier to multiple European OEMs integrating interior roof management systems with retractable configurations.

Magna International Inc.: One of the world's largest automotive suppliers, Magna's roof systems division designs and manufactures complete hard-top and panoramic roof modules, with co-engineering capabilities spanning structural aluminum, actuation, sealing, and glazing integration.

Inalfa Roof Systems Group B.V: A dedicated roof system specialist with manufacturing facilities across Europe, North America, and Asia, Inalfa holds significant market share in panoramic and retractable sunroof systems and has invested in next-generation electromechanical actuation technologies.

Valmet Automotive Inc.: Operating at the intersection of contract vehicle manufacturing and systems supply, Valmet Automotive provides complete convertible vehicle production services including roof system integration, making it a unique full-vehicle competency player in the retractable roof value chain.

Inteva Products: Focuses on closure systems, motors, and roof mechanisms, with engineering centers serving North American and European OEM customers on retractable roof actuation and sealing subsystems.

ALUPROF Aluminum profile GmbH.: Supplies precision aluminum extrusion profiles used in structural roof frames and guide rail systems for retractable roof assemblies, bridging the material supply and component manufacturing layers.

AISIN SEIKI Co. Ltd.: A major Japanese automotive components supplier, AISIN SEIKI provides roof actuation motors, drive mechanisms, and electromechanical subsystems integrated into retractable roof assemblies for Japanese and global OEM customers.

March 2024: Webasto Group announced a co-development agreement with a major European electric vehicle manufacturer to deliver a lightweight, fully electric-actuated retractable hard-top roof system optimized for BEV platform architecture, targeting production launch in 2026.

June 2024: Covestro AG introduced its next-generation Makrolon RE polycarbonate — incorporating a minimum 25% recycled content — for automotive glazing applications, directly targeting OEM retractable roof panel specifications requiring both lightweighting and sustainability compliance.

September 2024: Magna International Inc. expanded its roof systems manufacturing footprint in China through a joint venture with a domestic Tier 1 supplier, targeting the rapidly growing Chinese premium EV segment for panoramic and retractable roof supply.

November 2024: Inalfa Roof Systems Group B.V secured a multi-year OEM supply agreement for panoramic retractable roof systems on a new crossover platform, with projected annual volumes exceeding 120,000 units beginning in 2026.

January 2025: The European Automobile Manufacturers' Association (ACEA) released updated lightweighting compliance guidance, specifically referencing roof system mass as a priority target for fleet CO₂ compliance, accelerating OEM specification of aluminum and polycarbonate roof architectures.

April 2025: AISIN SEIKI Co. Ltd. unveiled a new ultra-compact electromechanical roof actuation module delivering a 20% reduction in motor package volume, enabling retractable roof integration in compact vehicle segments previously constrained by space limitations.

The OEM Retractable Roof System Market exhibits meaningful regional differentiation across maturity levels, growth rates, and demand composition.

Europe represents the largest regional market by revenue share, estimated at approximately 38–42% of global market value in 2024. Germany, France, Italy, and the United Kingdom collectively anchor European demand, driven by the density of premium automotive manufacturing (BMW, Mercedes-Benz, Audi, Porsche, Ferrari, Aston Martin) and a consumer base with the highest per-capita spending on premium convertible and coupe-cabriolet vehicles globally. European regulatory intensity — particularly the EU CO₂ fleet targets and incoming Euro 7 emissions standards — is driving material lightweighting investment that benefits aluminum and polycarbonate roof system suppliers. Regional CAGR for Europe is estimated at 6.8–7.5%, reflecting a mature but innovation-active market.

Asia Pacific is the fastest-growing regional market, with a projected CAGR of 10.5–12% through the forecast period. China is the primary growth engine, with domestic OEM brands aggressively incorporating retractable and panoramic roof features into premium electric vehicles to compete with established luxury imports. India is an emerging secondary growth market, with rising aspirational vehicle purchasing and increasing OEM investment in premium segments. Japan and South Korea contribute through their globally competitive OEM supply chains. The Asia Pacific region is expected to close the revenue share gap with Europe significantly before 2030.

North America accounts for approximately 28–32% of global market revenue in 2024, anchored by strong consumer demand for open-air driving features in the United States and a robust premium and near-premium vehicle market. The regional CAGR is estimated at 7.5–8.2%, supported by EV adoption growth and expanding retractable roof options in the crossover and pickup truck lifestyle segments. Mexico contributes as a manufacturing hub for North American OEM supply chains rather than a primary demand market.

South America and the Middle East & Africa collectively represent a smaller combined share of approximately 6–8% of global market value. Brazil leads South American demand due to its scale, while GCC nations — particularly UAE and Saudi Arabia — are emerging premium vehicle markets where retractable roof systems command strong aspirational appeal. Growth rates in these regions are projected at 5.5–7%, constrained by lower vehicle parc density and price sensitivity outside the ultra-premium tier.

Environmental, social, and governance (ESG) pressures are fundamentally reshaping product development, material selection, and procurement strategies across the OEM Retractable Roof System Market. These pressures operate at multiple levels simultaneously — from regulatory mandates imposed on OEMs, through supply chain decarbonization requirements cascaded to Tier 1 suppliers, to ESG-driven investor screening of automotive sector companies.

On the regulatory front, the European Union's Corporate Sustainability Reporting Directive (CSRD) and the EU Taxonomy for Sustainable Activities are compelling both OEMs

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 8.52% from 2020-2034 |

| Segmentation |

|

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Comprehensive validation mechanisms ensuring market intelligence accuracy, reliability, and adherence to international standards.

500+ data sources cross-validated

200+ industry specialists validation

NAICS, SIC, ISIC, TRBC standards

Continuous market tracking updates

Factors such as are projected to boost the OEM Retractable Roof System Market market expansion.

Key companies in the market include AAS Automotive s.r.o., Webasto Group, Covestro AG, BOS Group, Magna International Inc., Inalfa Roof Systems Group B.V, Valmet Automotive Inc., Inteva Products, ALUPROF Aluminum profile GmbH., AISIN SEIKI Co. Ltd..

The market segments include Sales Channel, Vehicle type, Roof Type, Material.

The market size is estimated to be USD 2.08 billion as of 2022.

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3690, USD 5820, and USD 9870 respectively.

The market size is provided in terms of value, measured in billion and volume, measured in .

Yes, the market keyword associated with the report is "OEM Retractable Roof System Market," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the OEM Retractable Roof System Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.