1. What are the major growth drivers for the Ski Gear & Equipment Market market?

Factors such as are projected to boost the Ski Gear & Equipment Market market expansion.

Ski Gear & Equipment Market

Ski Gear & Equipment Market

Market Lens IQ is a global market intelligence and strategic consulting firm delivering advanced syndicated research reports, customized industry analysis, competitive intelligence, and data-driven advisory solutions to organizations across international markets. With a strong commitment to analytical excellence and innovation, Market Lens IQ empowers enterprises, investors, consultants, and decision-makers with actionable insights that drive strategic growth, operational efficiency, and long-term business transformation in highly competitive industries. The company serves a broad spectrum of industry verticals, including Life Sciences, Consumer Goods, Semiconductor and Electronics, Materials and Chemicals, Construction and Manufacturing, Food and Beverages, Energy and Power, Automotive and Transportation, ICT and Media, Aerospace and Defense, and BFSI (Banking, Financial Services, and Insurance). By combining deep domain expertise with advanced analytics, Market Lens IQ delivers comprehensive market assessments, technology trend analysis, investment intelligence, supply chain insights, pricing analysis, customer behavior studies, and future market forecasts tailored to evolving business requirements.

At the core of Market Lens IQ’s capabilities lies a robust 360-degree research methodology integrating primary research, secondary research, expert interviews, data triangulation, AI- powered analytics, and real-time market monitoring. Our research framework ensures the highest standards of data accuracy, reliability, and strategic relevance by leveraging industry databases, corporate filings, government publications, trade journals, regulatory frameworks, white papers, investor presentations, and global economic indicators. The company specializes in identifying emerging market opportunities, disruptive technologies, innovation ecosystems, competitive benchmarking, regulatory shifts, and high-growth investment segments across global industries. Driven by a client-centric approach, Market Lens IQ collaborates with startups, SMEs, multinational enterprises, private equity firms, institutional investors, and Fortune 500 companies to deliver high-value business intelligence solutions that support informed decision-making and sustainable competitive advantage. Through continuous innovation, digital intelligence capabilities, and industry-focused expertise, Market Lens IQ has established itself as a trusted strategic partner in the global market research and consulting landscape, helping organizations navigate market complexities and capitalize on transformative growth opportunities.

+1 2315155523

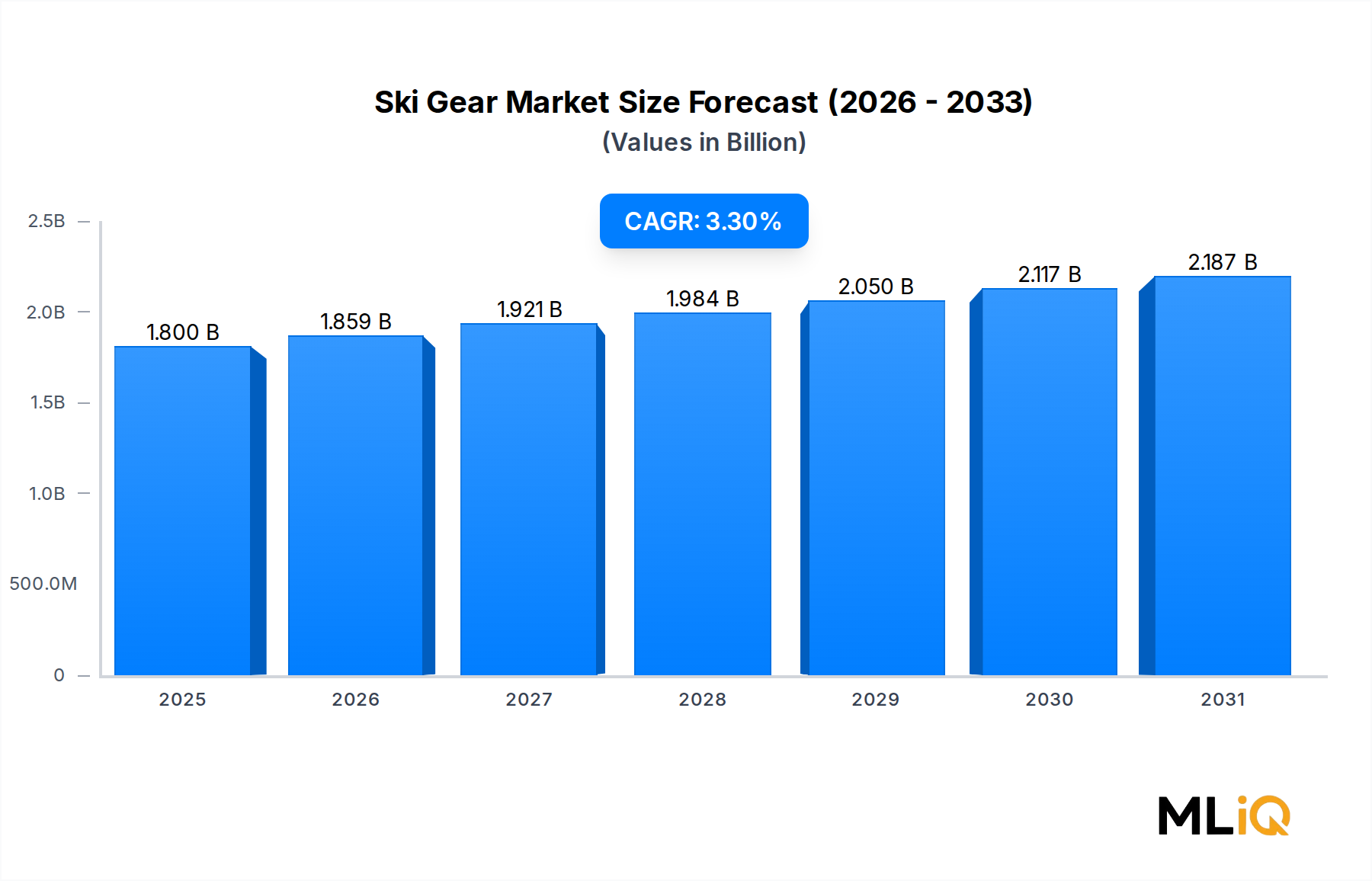

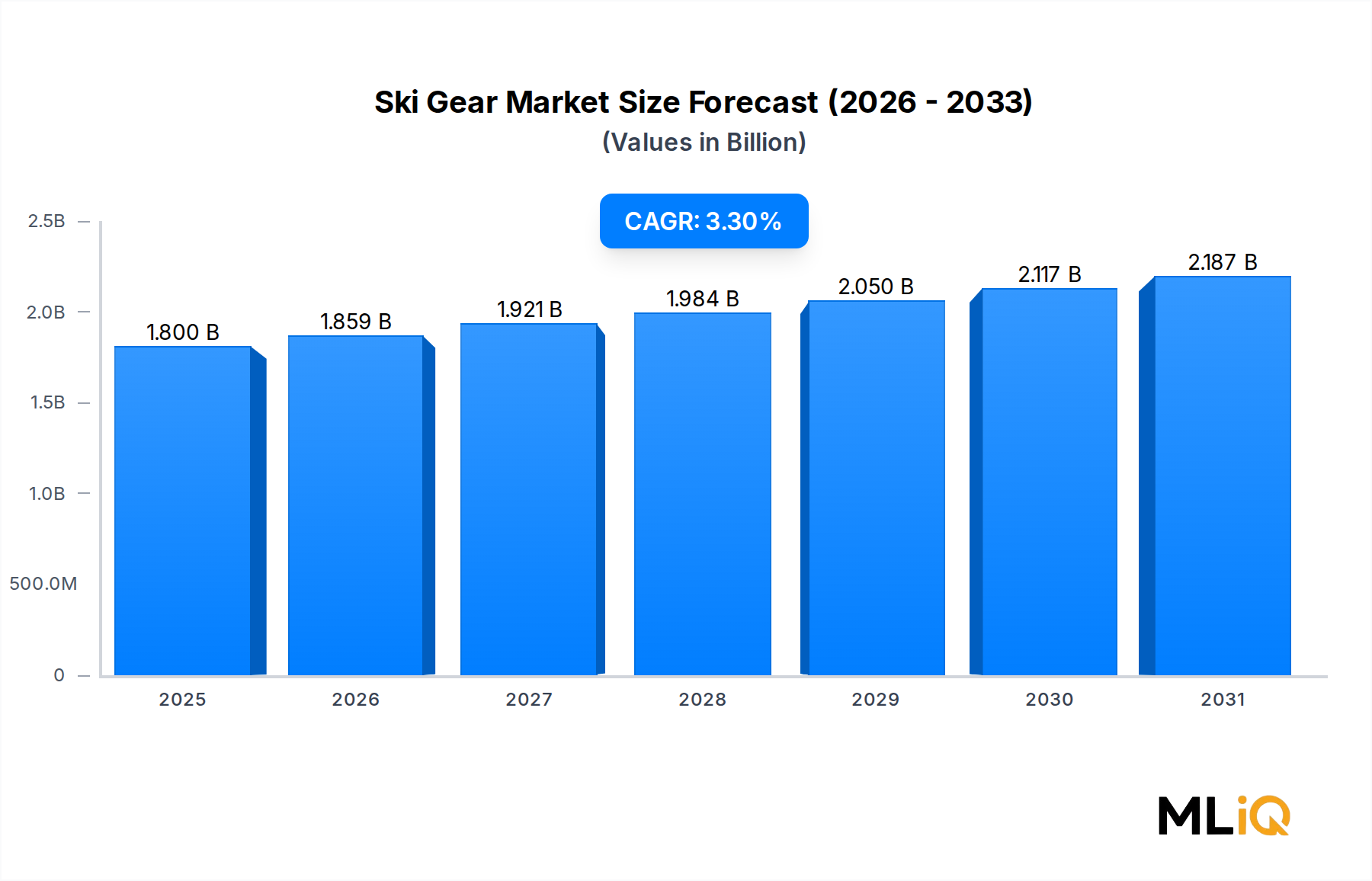

The global Ski Gear & Equipment Market is valued at $1.8 billion in 2025, expanding at a compound annual growth rate (CAGR) of 3.3% through the forecast period. This steady growth trajectory reflects a confluence of recovering post-pandemic travel patterns, rising disposable incomes in emerging economies, and intensifying participation in alpine and Nordic skiing disciplines across key geographies. The market encompasses a diverse product portfolio spanning skis and snowboards, ski boots, ski apparel, and protective gear, each catering to distinct recreational and competitive user segments.

Demand is being catalyzed by several macro-level tailwinds. First, the global winter tourism sector is rebounding strongly, with ski resort traffic in Europe and North America approaching pre-pandemic levels. This resurgence is directly translating into equipment rental upgrades and personal gear purchases. Second, a pronounced shift toward premium and performance-oriented equipment — driven by millennial and Gen Z outdoor enthusiasts — is elevating average selling prices across product categories, effectively boosting market revenue even when unit volumes grow modestly.

Technological innovation remains a central value driver. Manufacturers are investing heavily in advanced materials such as carbon fiber laminates, titanal alloys, and thermoplastic urethane shells to enhance performance-to-weight ratios in skis and boots. Meanwhile, smart wearables integrated into helmets and goggles are creating adjacent revenue streams and deepening consumer engagement with the sport. These innovations not only attract first-time buyers but also incentivize seasoned athletes to upgrade their existing gear on shorter replacement cycles.

The Asia Pacific region deserves special attention as a high-potential growth frontier. Rapid infrastructure development of ski resorts in China — accelerated by the 2022 Beijing Winter Olympics legacy investment — is generating demand for both entry-level and premium equipment. Japan and South Korea continue to demonstrate mature, sophisticated consumer bases favoring technical performance gear.

From a distribution perspective, online retail channels are gaining momentum, particularly for apparel and accessories, while offline specialty stores continue to dominate premium hard goods transactions where fit and expert consultation are paramount. This bifurcation is shaping go-to-market strategies for established brands and challenger entrants alike.

Looking forward, the market is poised for sustainable, moderate growth through the forecast horizon. Companies that align product development with sustainability mandates — particularly around recyclable materials and low-impact manufacturing processes — are likely to capture outsized share as environmentally conscious purchasing criteria gain weight among core consumer demographics. The competitive intensity is high but manageable, with several well-capitalized incumbents and a growing cohort of direct-to-consumer disruptors reshaping the landscape.

The Alpine application segment commands the largest revenue share within the Ski Gear & Equipment Market, driven by its mass participation base, infrastructure depth, and premium product attachment rates. Alpine skiing — characterized by downhill descents on groomed pistes and off-piste terrain — is the predominant form of skiing practiced globally, accounting for the majority of lift ticket sales, resort visits, and associated equipment purchases across North America, Europe, and increasingly Asia Pacific.

The dominance of the Alpine segment is structurally reinforced by the breadth of its product ecosystem. Alpine skiers require a comprehensive suite of gear: performance skis with specialized binding systems, rigid plastic boots offering precise power transmission, insulated and waterproof outerwear, helmets, goggles, gloves, and protective padding. This multi-item purchase basket significantly elevates the average consumer transaction value compared to Nordic skiing, where equipment requirements are generally lighter and less expensive.

Key players entrenched in the Alpine segment include Groupe Rossignol, one of the oldest and most technically sophisticated ski manufacturers globally, with a portfolio spanning race-grade World Cup equipment to all-mountain recreational skis. Amer Sports Oyj, parent company of the Salomon and Atomic brands, commands substantial market share across skis, bindings, and boots. Fischer Sports GmbH maintains a formidable position in both Alpine and Nordic categories, leveraging precision Austrian engineering as a core brand differentiator. Volkl Int. GmbH is another central European powerhouse focused on high-performance carving and freeride skis, particularly strong in the premium and expert-level consumer tiers.

The Alpine segment's revenue share is consolidating rather than expanding in mature markets such as Western Europe and the United States, where participation rates have plateaued. However, the segment is actively growing its absolute revenue base through two mechanisms: premiumization and geographic expansion. In terms of premiumization, consumers are increasingly trading up to higher-specification equipment — lightweight carbon-reinforced skis, heat-moldable boot liners, and technically advanced binding systems — which commands price premiums of 20% to 45% over entry-level alternatives. Brands are responding by tiering their product lines more granularly and investing in direct-to-consumer channels to capture richer margins.

Geographic expansion into China, India, and Southeast Asia represents the segment's most significant growth opportunity over the medium term. China alone has committed to developing over 800 ski resorts as part of its national winter sports promotion strategy, and while local equipment manufacturing is nascent, international Alpine brands are actively establishing distribution partnerships and flagship retail presences in tier-one and tier-two Chinese cities.

Within the Alpine segment, ski boots represent a particularly high-margin sub-category. Boot technology innovation — including BOA lacing systems, carbon fiber cuffs, and thermoformable shells — is driving replacement cycles of three to five years even among casual users, compared to the seven-to-ten-year replacement cycle historically observed. This compression of replacement frequency is a structural positive for segment revenue intensity and is a key focus area for brands including K2 Sports LLC and Alpina DOO, both of which have made notable investments in boot technology R&D over the past three fiscal years.

The competitive dynamic within the Alpine segment is characterized by a tiered structure: a handful of premium European heritage brands occupy the top of the market, mid-tier American and Asian brands compete on value and distribution breadth, and a growing base of direct-to-consumer startups target niche communities such as women-specific design, adaptive skiing, and sustainability-focused manufacturing.

Several well-defined drivers and constraints shape the demand and competitive dynamics within the Ski Gear & Equipment Market.

Driver — Winter Tourism Recovery: Global ski resort attendance has recovered meaningfully following the 2020–2021 pandemic-induced collapse. European alpine destinations including the Alps and Pyrenees reported aggregate visitor increases of 12% to 18% year-over-year during the 2023–2024 ski season, directly stimulating equipment rental upgrades and personal purchase decisions. This recovery is the single largest near-term demand catalyst.

Driver — Premiumization and Technology Adoption: Consumer willingness to spend on high-performance equipment is rising. Average unit selling prices for performance skis have increased by an estimated 8% to 12% over the past three years as carbon fiber and metallic laminate constructions become mainstream rather than niche. The Ski Boots Market is similarly experiencing upward price migration, with heat-moldable and custom-fit solutions commanding premiums that elevate category revenue despite modest volume growth.

Driver — Rising Participation in Asia Pacific: China's national winter sports initiative, energized by the 2022 Beijing Winter Olympics, has enrolled an estimated 300 million citizens in winter sports promotion programs. This policy-driven demand surge is creating a long-duration tailwind for equipment manufacturers with established Asia Pacific distribution infrastructure.

Constraint — Climate Change and Snow Reliability: Declining natural snowpack at lower elevations is reducing the operational season length for many mid-altitude resorts. Resorts in the Alps below 1,500 meters elevation face materially shorter reliable snow seasons, compressing the window of peak equipment demand and discouraging new participant entry. This is a structural headwind that intensifies over the medium and long term.

Constraint — High Entry Cost Barrier: The total cost of equipping a first-time alpine skier — including skis, boots, bindings, helmet, apparel, and accessories — can exceed $1,500 to $2,500 for mid-range equipment, representing a significant discretionary expenditure. This cost barrier suppresses new participant conversion rates, particularly in price-sensitive emerging markets and among lower-income demographic cohorts in mature markets.

Constraint — Supply Chain Fragility: Concentrated manufacturing of precision components — particularly high-grade steel edges, titanal alloy sheets, and specialized thermoplastic compounds — in a limited number of European and Asian facilities creates vulnerability to geopolitical disruptions, energy cost inflation, and logistics bottlenecks, as evidenced by component shortages experienced during 2021–2022.

The competitive landscape of the Ski Gear & Equipment Market is moderately consolidated at the premium tier and fragmented at the mid-to-value tier, with the following key participants:

Groupe Rossignol: A French heritage brand and one of the largest ski manufacturers globally, Rossignol maintains a vertically integrated portfolio spanning skis, boots, bindings, and apparel, with particular strength in the race and all-mountain Alpine segments.

K2 Sports LLC: An American brand known for its broad accessibility-focused product range, K2 competes across skis, snowboards, and boots with distribution strength in North American specialty retail and online channels.

Alpina DOO: A Slovenian precision manufacturer with a long heritage in ski boot construction, Alpina targets the mid-to-premium boot segment with technically sophisticated fit systems and is expanding its European and Asian distribution footprint.

Amer Sports Oyj: The Finnish conglomerate behind Salomon and Atomic brands, Amer Sports holds significant market share in both hard goods and apparel, leveraging cross-brand synergies and a global distribution network spanning over 100 countries.

Fischer Sports GmbH: An Austrian manufacturer with dual strength in Alpine and Nordic categories, Fischer is particularly dominant in cross-country racing equipment and maintains a strong competitive presence in boot innovation.

Volkl Int. GmbH: A German precision ski brand recognized for its Titanal-heavy construction and expert-level performance skis, Volkl commands strong brand loyalty among advanced and expert recreational skiers in Central Europe.

Helly Hansen: A Norwegian brand with deep roots in professional maritime and mountain environments, Helly Hansen competes in ski apparel with a focus on technical outerwear and base layer systems for demanding alpine conditions.

Clarus: The parent company of Black Diamond Equipment and PIEPS avalanche safety brands, Clarus has a focused position in technical mountain and backcountry gear, benefiting from the structural growth of off-piste and ski touring participation.

Black Diamond Equipment: Competing in technical ski hardware, avalanche safety equipment, and ski mountaineering tools, Black Diamond targets the fast-growing backcountry segment with high-margin specialized products.

Coalition Snow: A women-focused ski equipment brand emphasizing inclusive design and direct-to-consumer distribution, Coalition Snow represents the emerging challenger segment targeting underserved demographic niches within the broader market.

January 2024: Amer Sports Oyj completed its initial public offering on the New York Stock Exchange, raising significant capital to accelerate product development and global retail expansion across its Salomon and Atomic ski brands.

March 2024: Groupe Rossignol unveiled its next-generation Hero carving ski line incorporating a proprietary cork-and-flax biocomposite core, marking a significant step toward sustainable materials adoption in performance ski construction.

September 2023: Fischer Sports GmbH announced a strategic partnership with a leading Austrian research university to co-develop AI-assisted boot fitting algorithms, targeting the personalized performance footwear segment.

November 2023: Helly Hansen launched its Lifa Infinity Pro+ apparel collection, using a fully fluorocarbon-free waterproof-breathable membrane technology, directly responding to evolving EU chemical regulatory frameworks affecting the Ski Apparel Market.

February 2023: Black Diamond Equipment expanded its avalanche safety product line with the launch of the Recon BT beacon, featuring Bluetooth connectivity and smartphone integration, targeting the rapidly growing backcountry skiing community.

October 2022: K2 Sports LLC entered a multi-year licensing agreement with a prominent freestyle skiing federation to develop athlete-input pro-model skis, strengthening its competitive and aspirational brand positioning in the youth segment.

December 2022: China's National Winter Sports Administration published updated resort development guidelines, confirming investment commitments that are expected to drive sustained demand growth across the Asia Pacific region through 2030.

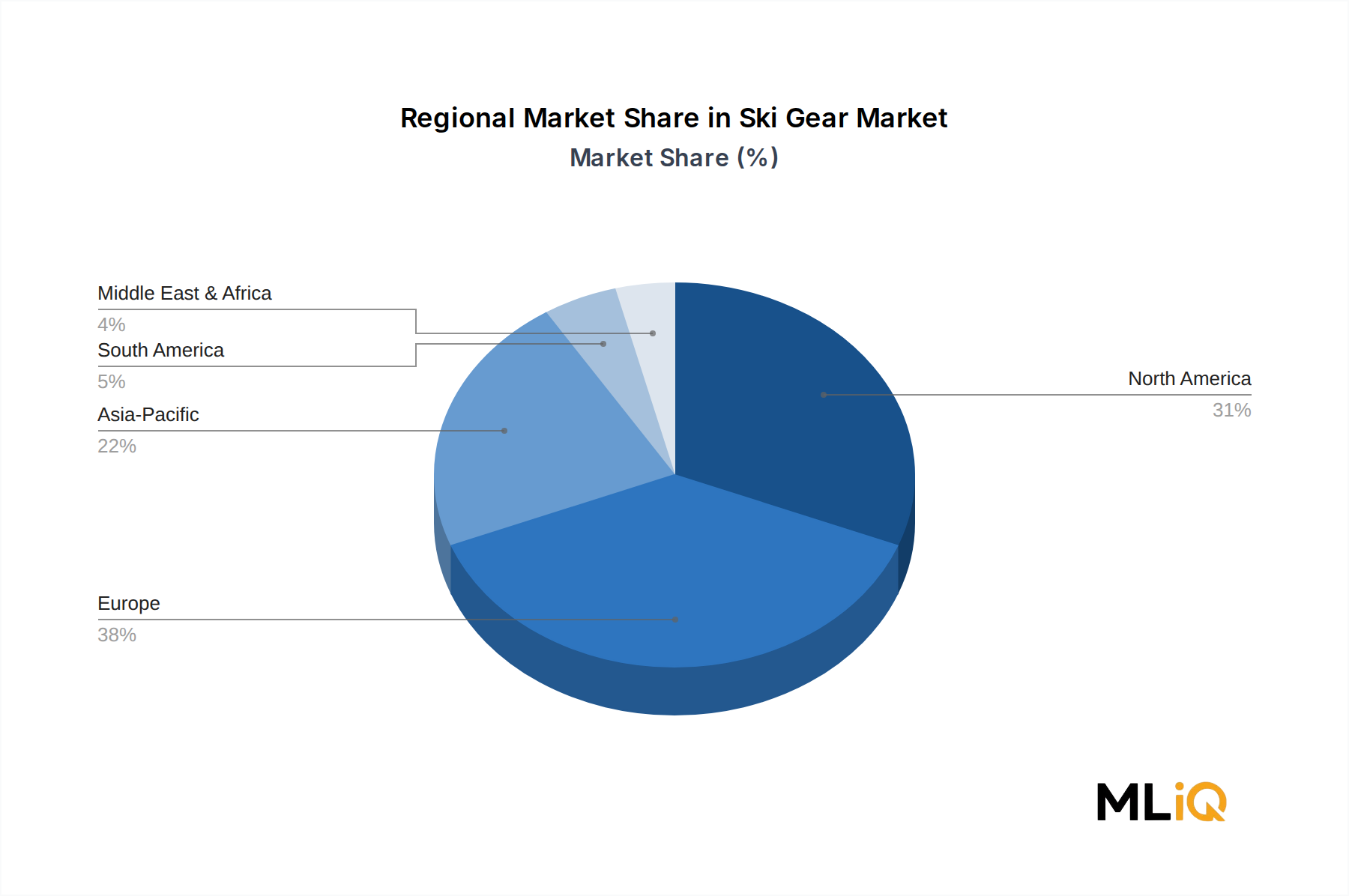

The Ski Gear & Equipment Market exhibits distinct regional demand profiles shaped by participation rates, infrastructure maturity, climate conditions, and economic factors.

Europe is the most mature and largest regional market, accounting for approximately 38% to 42% of global revenue in 2025. The Alpine arc — encompassing France, Austria, Switzerland, Italy, and Germany — constitutes the epicenter of both participation and premium equipment demand. Regional CAGR is estimated at 2.5% to 3.0%, reflecting saturation in core markets partially offset by growth in Eastern European destinations and Nordic skiing disciplines. The primary demand driver remains a deeply embedded skiing culture with high repeat participation rates and strong propensity for annual equipment upgrades.

North America, led by the United States and Canada, represents the second-largest regional market with a revenue share of approximately 30% to 34% and a CAGR aligned with the global average near 3.3%. The U.S. market is characterized by high per-capita equipment spending, strong resort infrastructure in Colorado, Utah, Vermont, and the Pacific Northwest, and a sophisticated specialty retail ecosystem. Mexico represents a minor but incrementally growing contributor within the region.

Asia Pacific is the fastest-growing regional market, with a projected CAGR of 5.5% to 7.0% through the forecast period. China is the dominant growth engine, with Japan and South Korea providing mature, technically sophisticated demand bases. The Beijing Winter Olympics legacy, ongoing resort construction, and government participation mandates are sustaining above-average growth rates. However, current revenue share remains lower than Europe and North America at approximately 18% to 22%, indicating substantial runway for expansion.

The Middle East & Africa and South America collectively represent smaller but strategically relevant markets. South America, centered on Argentina and Chile's Andes ski resorts, generates niche but premium demand catering largely to Latin American affluent consumers and international tourists. The Middle East, particularly Gulf Cooperation Council nations with indoor ski facilities, is an emerging micro-market for ski equipment retail, though volumes remain constrained by the artificial nature of the snow environment. Both regions are expected to grow at rates of 2.0% to 3.5%, primarily driven by outbound ski tourism rather than domestic resort development.

The Ski Gear & Equipment Market is materially dependent on a set of specialized upstream inputs whose price dynamics and supply reliability significantly influence manufacturer margins and product availability.

Titanal alloy — an aluminum-titanium composite widely used in premium ski construction for vibration damping and edge-hold enhancement — is sourced predominantly from a small number of European metallurgical producers. Titanal price trends have been upward over the past three years, driven by elevated energy costs at aluminum smelters and tightening titanium feedstock supply. This has directly contributed to bill-of-materials inflation for premium Alpine skis in the range of 6% to 9% since 2021.

Carbon fiber, a critical input for lightweight performance skis, poles, and boot reinforcements, is heavily concentrated in Japanese and American production facilities. Carbon fiber has experienced significant price volatility, with spot prices rising sharply during 2021–2022 due to aerospace sector demand recovery and supply bottlenecks, before partially moderating through 2023–2024. Manufacturers in the Carbon Fiber Composites Market are expanding production capacity, which is expected to provide gradual relief to downstream ski equipment producers over the medium term.

Thermoplastic polyurethane (TPU) and other specialized polymers used in ski boot shells and liner systems are subject to petrochemical feedstock price variability. Suppliers in the Thermoplastic Polyurethane Market have faced margin compression from both raw material cost inflation and energy

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 3.3% from 2020-2034 |

| Segmentation |

|

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Comprehensive validation mechanisms ensuring market intelligence accuracy, reliability, and adherence to international standards.

500+ data sources cross-validated

200+ industry specialists validation

NAICS, SIC, ISIC, TRBC standards

Continuous market tracking updates

Factors such as are projected to boost the Ski Gear & Equipment Market market expansion.

Key companies in the market include Groupe Rossignol, K2 Sports LLC, Alpina DOO, Amer Sports Oyj, Fischer Sports GmbH, Volkl Int. GmbH, Helly Hansen, Clarus, Black Diamond Equipment, Coalition Snow.

The market segments include Type, Application, Distribution Channel.

The market size is estimated to be USD 1.8 billion as of 2022.

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3690, USD 5820, and USD 9870 respectively.

The market size is provided in terms of value, measured in billion and volume, measured in .

Yes, the market keyword associated with the report is "Ski Gear & Equipment Market," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Ski Gear & Equipment Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.