1. What are the major growth drivers for the Logistics Business Outsourcing Market market?

Factors such as are projected to boost the Logistics Business Outsourcing Market market expansion.

+1 2315155523

Market Lens IQ is a global market intelligence and strategic consulting firm delivering advanced syndicated research reports, customized industry analysis, competitive intelligence, and data-driven advisory solutions to organizations across international markets. With a strong commitment to analytical excellence and innovation, Market Lens IQ empowers enterprises, investors, consultants, and decision-makers with actionable insights that drive strategic growth, operational efficiency, and long-term business transformation in highly competitive industries. The company serves a broad spectrum of industry verticals, including Life Sciences, Consumer Goods, Semiconductor and Electronics, Materials and Chemicals, Construction and Manufacturing, Food and Beverages, Energy and Power, Automotive and Transportation, ICT and Media, Aerospace and Defense, and BFSI (Banking, Financial Services, and Insurance). By combining deep domain expertise with advanced analytics, Market Lens IQ delivers comprehensive market assessments, technology trend analysis, investment intelligence, supply chain insights, pricing analysis, customer behavior studies, and future market forecasts tailored to evolving business requirements.

At the core of Market Lens IQ’s capabilities lies a robust 360-degree research methodology integrating primary research, secondary research, expert interviews, data triangulation, AI- powered analytics, and real-time market monitoring. Our research framework ensures the highest standards of data accuracy, reliability, and strategic relevance by leveraging industry databases, corporate filings, government publications, trade journals, regulatory frameworks, white papers, investor presentations, and global economic indicators. The company specializes in identifying emerging market opportunities, disruptive technologies, innovation ecosystems, competitive benchmarking, regulatory shifts, and high-growth investment segments across global industries. Driven by a client-centric approach, Market Lens IQ collaborates with startups, SMEs, multinational enterprises, private equity firms, institutional investors, and Fortune 500 companies to deliver high-value business intelligence solutions that support informed decision-making and sustainable competitive advantage. Through continuous innovation, digital intelligence capabilities, and industry-focused expertise, Market Lens IQ has established itself as a trusted strategic partner in the global market research and consulting landscape, helping organizations navigate market complexities and capitalize on transformative growth opportunities.

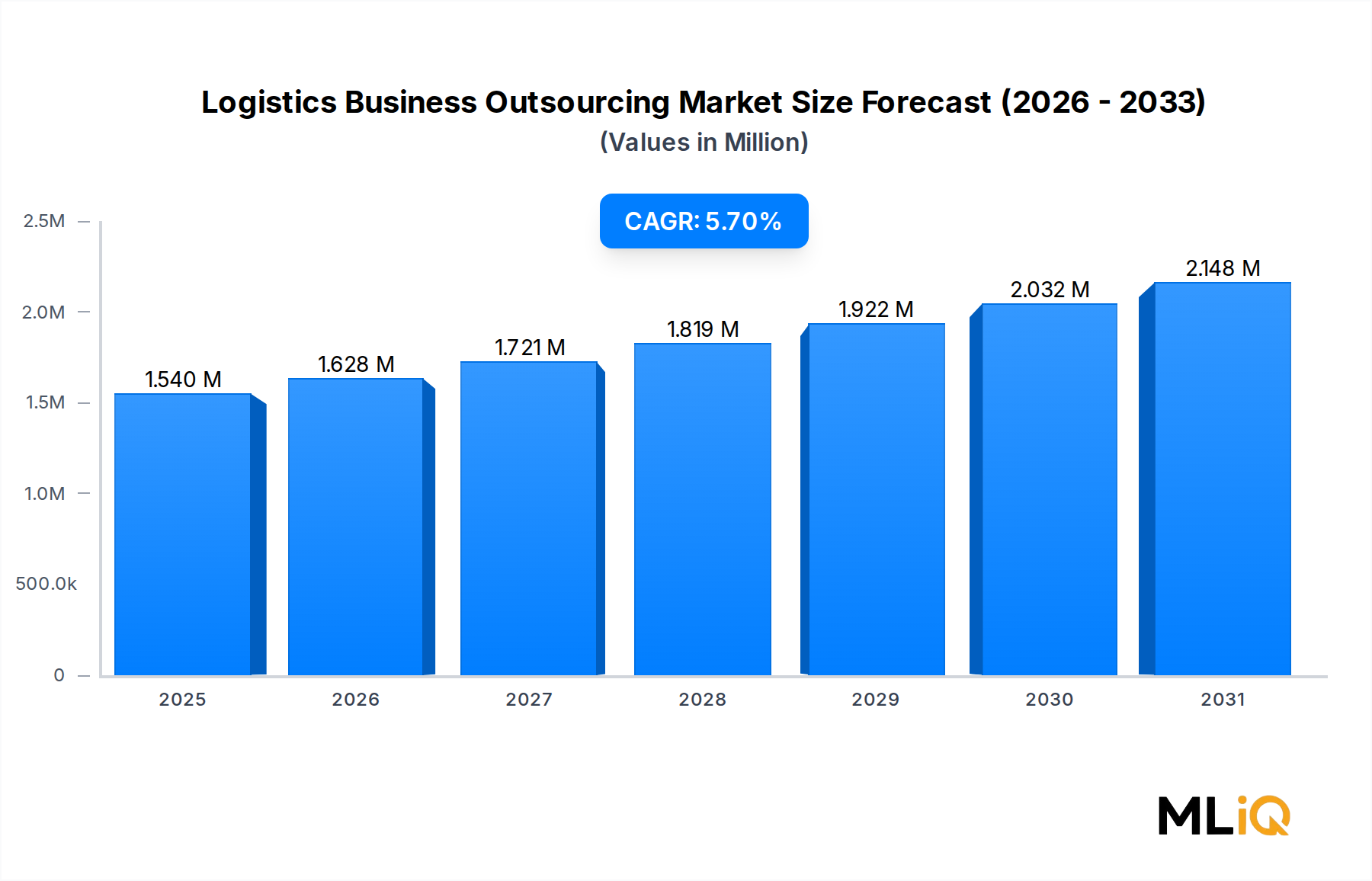

The global Logistics Business Outsourcing Market is currently valued at $1.54 trillion and is projected to expand at a compound annual growth rate (CAGR) of 5.7% over the forecast period, reflecting robust structural demand across end-use verticals and geographies. This market encompasses the delegation of logistics functions — including freight forwarding, warehousing, inventory management, distribution, customs clearance, and value-added services — to specialized third-party providers, enabling enterprises to focus on core competencies while achieving cost efficiency and operational agility.

Key demand drivers underpinning this growth trajectory include the accelerating globalization of supply chains, rising e-commerce penetration, and the increasing complexity of regulatory and compliance frameworks across international trade corridors. Enterprises across pharmaceuticals, automotive, food and beverages, and chemicals are actively migrating from in-house logistics operations to outsourced models, driven by the dual imperatives of cost reduction and service-level improvement.

Macro tailwinds reinforcing market expansion include sustained growth in cross-border trade volumes, digital transformation of supply chain operations through artificial intelligence, Internet of Things (IoT), and blockchain-enabled visibility platforms, and the post-pandemic reconfiguration of global supply chains toward resilience and redundancy. The surge in nearshoring and friendshoring strategies has particularly elevated demand for outsourced logistics services in emerging regional hubs across Southeast Asia, Eastern Europe, and Latin America.

From a modal perspective, roadways continue to account for the largest share of outsourced logistics revenues globally, while air freight outsourcing is registering above-average growth rates driven by time-sensitive pharmaceutical and high-value electronics shipments. Ocean carrier outsourcing remains a cornerstone of global trade, particularly for bulk commodities and containerized goods.

Looking ahead, the market is expected to witness continued consolidation among tier-one logistics service providers through mergers, acquisitions, and strategic alliances, as scale becomes a critical competitive differentiator. Investment in technology infrastructure — particularly in warehouse automation, predictive analytics, and real-time tracking platforms — is expected to reshape the value proposition of outsourced logistics partners. Sustainability imperatives, including decarbonization mandates and ESG-aligned procurement, are also emerging as material factors influencing provider selection criteria among large enterprise shippers. The outlook for the Logistics Business Outsourcing Market remains constructive, with structural demand expected to outpace GDP growth in most major economies through the end of the decade.

Within the mode of transport segmentation, roadways represent the dominant sub-segment of the Logistics Business Outsourcing Market, commanding the largest share of total outsourced logistics revenues globally. This dominance is rooted in the segment's unmatched geographic reach, flexibility, and cost-effectiveness for short-to-medium haul freight movements, which constitute the backbone of domestic and regional supply chains.

Road freight outsourcing is particularly entrenched in mature markets such as North America, Western Europe, and China, where dense highway infrastructure supports full truckload (FTL) and less-than-truckload (LTL) services at scale. In the United States alone, truckload freight represents the single largest mode of domestic freight by value, and the outsourcing of road logistics to third-party carriers and brokers has become standard practice across virtually all manufacturing and retail verticals.

The pharmaceutical end-user segment has emerged as a high-growth contributor to road logistics outsourcing, driven by the need for temperature-controlled transportation and regulatory compliance in last-mile distribution. Similarly, the food and beverages sector relies heavily on outsourced road logistics for perishable goods movement, requiring specialized cold-chain capabilities that most shippers prefer to delegate to experienced providers rather than develop in-house.

The automotive segment is another critical demand pillar for road-based outsourced logistics. Just-in-time and just-in-sequence manufacturing philosophies, which are central to automotive production, demand highly reliable and precisely timed road freight services. Companies such as XPO Logistics, Inc. and Deutsche Bahn AG have built dedicated automotive logistics verticals that offer integrated road transport solutions tailored to the production schedules of major original equipment manufacturers (OEMs).

From a competitive standpoint, the roadways outsourcing sub-segment is characterized by a mix of large integrated logistics conglomerates and regional specialists. DSV A/S and DHL International GmbH maintain extensive road freight networks across Europe and North America, leveraging scale to offer competitive pricing and broad service coverage. Kuehne + Nagel International AG has similarly invested in expanding its road logistics capabilities, particularly in contract logistics and integrated supply chain management.

Digital disruption is reshaping the competitive dynamics within road logistics outsourcing. The proliferation of digital freight matching platforms and Transportation Management Systems has enabled shippers to access capacity more efficiently, driving margin compression among traditional asset-heavy carriers. This has accelerated the shift toward asset-light, technology-driven logistics providers that emphasize visibility, analytics, and dynamic routing optimization.

Despite headwinds from driver shortages in North America and Europe, rising fuel costs, and increasing regulatory requirements around emissions and driver hours, the roadways outsourcing segment is expected to sustain its leadership position. The ongoing expansion of e-commerce fulfillment networks, which rely disproportionately on road-based last-mile and middle-mile delivery, will continue to generate incremental demand for outsourced road logistics services throughout the forecast period. The segment's share is consolidating around a smaller number of larger, technology-enabled providers capable of offering end-to-end visibility and integrated multimodal solutions.

The Logistics Business Outsourcing Market is shaped by a constellation of quantifiable drivers and structural constraints that collectively determine the pace and direction of market expansion.

On the demand side, the exponential growth of global e-commerce — projected to surpass $7 trillion in gross merchandise value by 2025 — is the single most powerful demand driver for outsourced logistics services. E-commerce growth directly increases the volume of parcels, returns, and fulfillment operations that require specialized logistics capabilities, most of which are beyond the operational scope of traditional retailers and brand manufacturers.

The pharmaceutical sector's expansion is another material driver. Global pharmaceutical logistics spending is estimated to exceed $100 billion annually, with cold-chain and serialization compliance requirements creating substantial barriers to in-house logistics management. This dynamic is driving pharmaceutical companies to outsource specialized logistics functions to providers with validated cold-chain infrastructure.

Digital transformation investment across supply chains is also accelerating outsourcing adoption. Enterprises that invest in Third-Party Logistics Market capabilities benefit from providers' proprietary technology platforms, avoiding the capital expenditure required to build equivalent in-house systems. The integration of IoT sensors, AI-driven demand forecasting, and blockchain-based provenance tracking within outsourced logistics platforms creates switching costs that deepen client relationships.

On the constraint side, geopolitical fragmentation and trade policy volatility represent the most significant structural headwinds. Tariff escalations, sanctions regimes, and border control tightening have introduced unpredictability into cross-border logistics planning, increasing the operational complexity for outsourced providers and, in some cases, compelling shippers to repatriate logistics functions. Additionally, cybersecurity vulnerabilities within interconnected logistics networks have elevated operational risk, with high-profile ransomware attacks on major logistics providers resulting in significant service disruptions and reputational damage. Labor cost inflation in key logistics markets further constrains margin expansion for service providers.

The competitive landscape of the Logistics Business Outsourcing Market is dominated by a set of globally integrated logistics conglomerates, each pursuing differentiated strategies across modal, geographic, and vertical dimensions.

DSV A/S: A Danish integrated transport and logistics group that has aggressively expanded through acquisitions, including the landmark purchase of Agility's Global Integrated Logistics business. DSV operates one of the largest air and ocean freight networks globally, with a growing contract logistics footprint.

A.P. Moller - Maersk: The world's largest container shipping company has executed a strategic pivot toward integrated logistics, acquiring multiple warehousing, customs brokerage, and last-mile delivery companies. Maersk aims to offer end-to-end supply chain solutions, positioning itself as a logistics integrator rather than a pure-play carrier.

DHL International GmbH: A subsidiary of Deutsche Post DHL Group, DHL maintains one of the most comprehensive global logistics networks, spanning express delivery, freight forwarding, supply chain management, and e-commerce logistics. Its investments in green logistics and automation are market-leading.

XPO Logistics, Inc.: A North American logistics leader specializing in LTL freight, last-mile delivery, and technology-driven brokerage. XPO has divested non-core assets to focus on its core LTL and brokerage operations, enhancing margin profiles.

UNITED PARCEL SERVICE OF AMERICA, INC.: A global leader in small package delivery and healthcare logistics, UPS has expanded its outsourced supply chain services, including temperature-controlled pharmaceutical distribution and returns management.

Kuehne + Nagel International AG: A Swiss-based logistics giant with leadership positions in sea freight and air freight forwarding. Kuehne + Nagel's digital platform, KN FreightNet, provides real-time pricing and booking capabilities that differentiate its service offering.

inexia (sncf group): The logistics arm of the French national railway group, inexia focuses on rail-based multimodal logistics solutions across Europe, leveraging the SNCF rail network for sustainable freight transport.

Deutsche Bahn AG: Through its DB Cargo and DB Schenker divisions, Deutsche Bahn operates one of Europe's largest rail and logistics networks, offering integrated multimodal services across road, rail, and ocean freight.

Nippon Express Co., Ltd.: Japan's largest logistics provider, Nippon Express has a strong presence across Asia Pacific and is expanding its global footprint through acquisitions and greenfield investments in contract logistics.

FedEx Corporation: A global express delivery and freight company that offers outsourced supply chain solutions including warehousing, order fulfillment, and returns management, with particular strength in healthcare and technology verticals.

January 2024: A.P. Moller - Maersk completed the full integration of its acquired logistics businesses, officially launching its end-to-end integrated logistics product suite targeted at mid-market and enterprise shippers across North America and Europe.

March 2024: DHL International GmbH announced a $500 million investment in expanding its Asia Pacific logistics infrastructure, including new automated warehouse facilities in Singapore, Vietnam, and India, targeting e-commerce and pharmaceutical verticals.

May 2024: DSV A/S finalized a strategic technology partnership with a leading AI platform provider to deploy machine learning-driven demand forecasting and dynamic routing optimization across its European road freight network.

July 2024: Kuehne + Nagel International AG launched an enhanced version of its KN FreightNet digital platform, incorporating real-time carbon emissions tracking and sustainability reporting tools to meet growing ESG disclosure requirements from enterprise clients.

September 2024: XPO Logistics, Inc. announced the expansion of its LTL network in the United States, adding 28 new service centers to improve density and transit times, directly responding to market share opportunities created by competitor restructuring.

November 2024: FedEx Corporation unveiled a restructured outsourced supply chain services division, consolidating its warehousing, fulfillment, and returns management operations under a unified brand to streamline go-to-market positioning.

February 2025: Nippon Express Co., Ltd. completed the acquisition of a European contract logistics provider, accelerating its international expansion strategy and adding 1.2 million square meters of warehousing capacity across Western Europe.

The Logistics Business Outsourcing Market exhibits distinct regional dynamics, with demand concentrations driven by industrial output, trade volumes, e-commerce penetration, and infrastructure maturity.

Asia Pacific represents the fastest-growing regional market, driven by the manufacturing powerhouses of China, India, and the ASEAN bloc. The region benefits from expanding middle-class consumption, rapid e-commerce adoption, and large-scale infrastructure investment under initiatives such as China's Belt and Road. Asia Pacific is expected to register a regional CAGR above 7% through the forecast period, with India emerging as a particularly high-growth market due to government-led logistics modernization programs and the formalization of the freight sector under the Goods and Services Tax regime. China remains the dominant country contributor to regional revenues, accounting for approximately 35% of Asia Pacific outsourced logistics spending.

North America is the most mature regional market, accounting for the largest absolute revenue share globally. The United States is the primary demand engine, supported by a sophisticated third-party logistics ecosystem, high e-commerce penetration, and well-developed road and air freight infrastructure. North America's regional CAGR is estimated at approximately 4.5%, reflecting market maturity but sustained underlying demand from pharmaceutical, retail, and automotive verticals. Canada and Mexico are growing contributors, with nearshoring trends boosting cross-border logistics volumes between the United States and Mexico.

Europe represents the second-largest regional market by revenue, with Germany, the United Kingdom, and France serving as the primary logistics hubs. Stringent environmental regulations, including the European Green Deal and CO2 emission standards for commercial vehicles, are reshaping modal preferences toward rail and intermodal solutions. Europe's regional CAGR is estimated at 4.8%, with Eastern Europe recording faster growth as manufacturing investment relocates from Asia.

The Middle East and Africa region is an emerging growth corridor, underpinned by investment in logistics free zones, port infrastructure expansion, and growing intra-regional trade. The GCC countries, particularly the UAE and Saudi Arabia, are investing heavily in logistics infrastructure as part of economic diversification strategies. South America, led by Brazil and Argentina, presents moderate growth potential, constrained by infrastructure deficits and macroeconomic volatility but supported by agricultural commodity export logistics.

Global trade flows are the foundational demand driver for the Logistics Business Outsourcing Market, with cross-border freight volumes directly correlating to outsourced logistics revenues. The Asia-to-North America and Asia-to-Europe trade corridors collectively represent the highest-volume and highest-value lanes in the global outsourced logistics ecosystem. China remains the world's largest exporter by volume, generating disproportionate demand for ocean carrier outsourcing, air freight services, and customs brokerage across Pacific and trans-Eurasian routes.

The trans-Pacific trade corridor has experienced significant disruption since 2018 due to successive rounds of tariff escalations between the United States and China. Section 301 tariffs on Chinese imports, which cover a wide range of manufactured goods, have increased landed costs and prompted shippers to diversify sourcing toward Vietnam, India, Bangladesh, and Mexico. This geographic diversification of manufacturing has, paradoxically, expanded the addressable market for outsourced logistics by increasing the complexity of multi-origin supply chains that require specialized coordination.

The implementation of the European Union's Carbon Border Adjustment Mechanism (CBAM), phasing in from 2026, is expected to introduce a new layer of compliance complexity for cross-border logistics providers serving European importers. Logistics outsourcing partners with embedded customs brokerage and compliance capabilities are positioned to capture incremental revenue from CBAM-related advisory and documentation services.

In the Middle East and Africa region, the development of logistics free zones — particularly in Dubai, Abu Dhabi, and Jebel Ali — has created competitive trade facilitation environments that attract outsourced logistics operations servicing Africa-bound and South Asia-bound trade flows. The African Continental Free Trade Area (AfCFTA), which came into force in 2021, has the potential to generate substantial new intra-African trade volumes, creating long-term demand for logistics outsourcing across the continent.

Non-tariff barriers, including customs delays, documentation requirements, and sanitary and phytosanitary standards, remain significant constraints on cross-border outsourced logistics efficiency, particularly in South Asia and Sub-Saharan Africa. Providers with deep local regulatory expertise are able to command premium pricing in these markets, reflecting the value of compliance knowledge as a differentiator in the Logistics Business Outsourcing Market.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.7% from 2020-2034 |

| Segmentation |

|

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Comprehensive validation mechanisms ensuring market intelligence accuracy, reliability, and adherence to international standards.

500+ data sources cross-validated

200+ industry specialists validation

NAICS, SIC, ISIC, TRBC standards

Continuous market tracking updates

Factors such as are projected to boost the Logistics Business Outsourcing Market market expansion.

Key companies in the market include DSV A/S, A.P. Moller - Maersk, DHL International GmbH, XPO Logistics, Inc., UNITED PARCEL SERVICE OF AMERICA, INC., Kuehne + Nagel International AG, inexia (sncf group), Deutsche Bahn AG, Nippon Express Co., Ltd., FedEx Corporation.

The market segments include Mode of Transport, End-user.

The market size is estimated to be USD 1.54 trillion as of 2022.

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3570, USD 5730, and USD 9600 respectively.

The market size is provided in terms of value, measured in trillion and volume, measured in .

Yes, the market keyword associated with the report is "Logistics Business Outsourcing Market," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Logistics Business Outsourcing Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.