1. What are the major growth drivers for the Automotive Oil Seals Market market?

Factors such as are projected to boost the Automotive Oil Seals Market market expansion.

+1 2315155523

Automotive Oil Seals Market

Automotive Oil Seals Market

Market Lens IQ is a global market intelligence and strategic consulting firm delivering advanced syndicated research reports, customized industry analysis, competitive intelligence, and data-driven advisory solutions to organizations across international markets. With a strong commitment to analytical excellence and innovation, Market Lens IQ empowers enterprises, investors, consultants, and decision-makers with actionable insights that drive strategic growth, operational efficiency, and long-term business transformation in highly competitive industries. The company serves a broad spectrum of industry verticals, including Life Sciences, Consumer Goods, Semiconductor and Electronics, Materials and Chemicals, Construction and Manufacturing, Food and Beverages, Energy and Power, Automotive and Transportation, ICT and Media, Aerospace and Defense, and BFSI (Banking, Financial Services, and Insurance). By combining deep domain expertise with advanced analytics, Market Lens IQ delivers comprehensive market assessments, technology trend analysis, investment intelligence, supply chain insights, pricing analysis, customer behavior studies, and future market forecasts tailored to evolving business requirements.

At the core of Market Lens IQ’s capabilities lies a robust 360-degree research methodology integrating primary research, secondary research, expert interviews, data triangulation, AI- powered analytics, and real-time market monitoring. Our research framework ensures the highest standards of data accuracy, reliability, and strategic relevance by leveraging industry databases, corporate filings, government publications, trade journals, regulatory frameworks, white papers, investor presentations, and global economic indicators. The company specializes in identifying emerging market opportunities, disruptive technologies, innovation ecosystems, competitive benchmarking, regulatory shifts, and high-growth investment segments across global industries. Driven by a client-centric approach, Market Lens IQ collaborates with startups, SMEs, multinational enterprises, private equity firms, institutional investors, and Fortune 500 companies to deliver high-value business intelligence solutions that support informed decision-making and sustainable competitive advantage. Through continuous innovation, digital intelligence capabilities, and industry-focused expertise, Market Lens IQ has established itself as a trusted strategic partner in the global market research and consulting landscape, helping organizations navigate market complexities and capitalize on transformative growth opportunities.

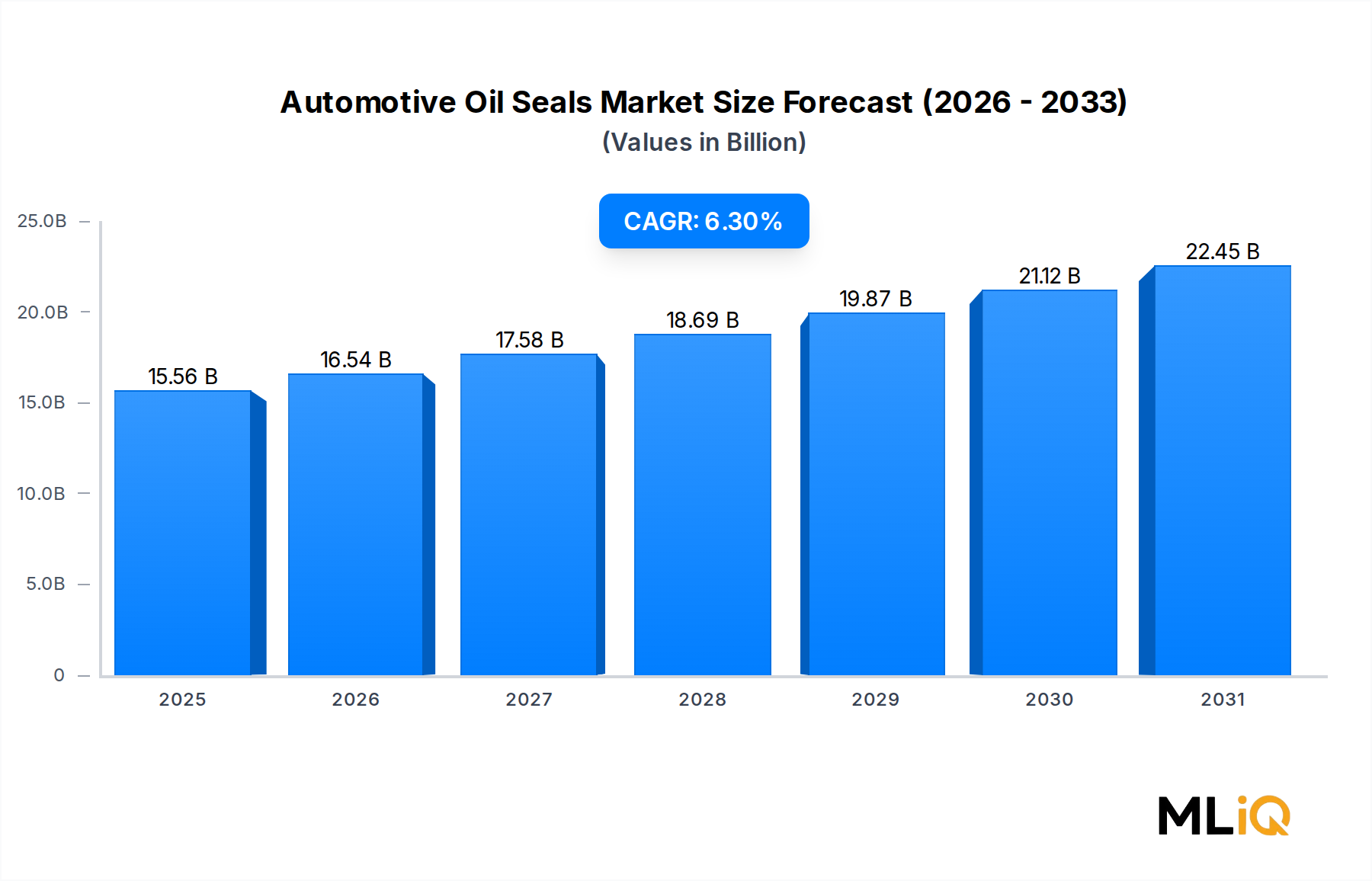

The global Automotive Oil Seals Market is valued at $15.56 billion in 2025 and is projected to expand at a compound annual growth rate (CAGR) of 6.3% through 2033, reflecting robust and sustained demand across both OEM and aftermarket channels worldwide. This growth trajectory is underpinned by accelerating vehicle production volumes, the increasing complexity of modern powertrain architectures, and the expanding global vehicle parc that consistently drives replacement demand.

Automotive oil seals serve a mission-critical function: they prevent lubricant leakage and contamination ingress across rotating and reciprocating shafts in engines, transmissions, axles, and wheel hubs. As vehicle platforms grow more sophisticated — integrating higher-pressure lubrication systems, tighter engineering tolerances, and extended service intervals — the performance specifications for oil seals have risen commensurately, pushing material science and manufacturing precision to new frontiers.

Key demand drivers include the surging sales of passenger vehicles in Asia Pacific markets, particularly China and India, where middle-class expansion and urbanization are fueling automotive uptake at an unprecedented pace. Commercial vehicle fleet expansion across South and Southeast Asia, sub-Saharan Africa, and Latin America further reinforces volumetric demand. Simultaneously, the global push toward electric vehicles (EVs) introduces a new design paradigm for sealing technologies, as EV powertrains — while eliminating traditional combustion-related seal points — introduce new requirements around battery enclosures, e-axle shafts, and thermal management fluid circuits.

From a macro perspective, the post-pandemic normalization of automotive supply chains has restored production cadences across major manufacturing hubs in Europe, North America, and Asia, alleviating the semiconductor and raw-material bottlenecks that suppressed output between 2020 and 2022. This normalization, combined with near-record global vehicle sales forecasts for 2025 and beyond, positions the Automotive Oil Seals Market for a prolonged growth phase.

Aftermarket dynamics are equally compelling. With the average vehicle age in mature markets such as the United States exceeding 12 years, the frequency of seal replacement driven by wear-and-tear cycles is structurally elevated. This creates a durable, recurring revenue base that insulates suppliers from cyclical OEM production downturns. The integration of digital diagnostics and telematics into fleet management further accelerates seal replacement by enabling predictive maintenance protocols that identify seal degradation before catastrophic failure occurs.

Looking ahead to 2033, the market is expected to approach approximately $26 billion, driven by product premiumization, geographic expansion, electrification-related new application development, and increasing regulatory mandates around emissions and fluid containment. Participants who invest in advanced polymer compounding, precision molding, and application-specific engineering will be best positioned to capture disproportionate value creation within this market.

Within the Automotive Oil Seals Market, the rubber oil seals segment commands the largest revenue share by a substantial margin, a position it has maintained for decades and is expected to consolidate further through 2033. Rubber oil seals — primarily manufactured from nitrile butadiene rubber (NBR), fluoroelastomer (FKM/Viton), polyacrylate (ACM), and silicone compounds — dominate due to their unmatched combination of flexibility, sealing effectiveness, chemical resistance, and cost efficiency across a broad operating temperature range.

Rubber's inherent viscoelasticity allows it to conform dynamically to shaft surfaces under variable load and speed conditions, maintaining a consistent sealing lip contact that minimizes lubricant leakage even as shaft surfaces experience minor runout, deflection, or surface wear. This performance characteristic is irreplaceable in high-duty automotive applications such as crankshaft seals, camshaft seals, transmission output shaft seals, and differential pinion seals.

The dominance of the rubber oil seals segment is further reinforced by the breadth of elastomer chemistry available to formulators. NBR compounds remain the workhorse for standard engine applications, offering excellent resistance to petroleum-based lubricants at moderate temperatures. FKM elastomers command the premium tier, where high-temperature engine environments — increasingly common in downsized, turbocharged powertrains — demand sustained sealing integrity at continuous operating temperatures exceeding 200°C. The growing adoption of synthetic lubricants, which carry more aggressive additive packages, has accelerated the substitution of NBR with FKM and ACM grades, a trend that is simultaneously elevating average selling prices within the rubber sub-segment.

From a volume perspective, passenger vehicle applications account for the single largest consumption pool within the rubber oil seals segment, given the sheer number of seal points per vehicle (ranging from 15 to 30+ per powertrain assembly, depending on complexity) and the massive global passenger vehicle parc. Commercial vehicle applications, while representing fewer units, contribute disproportionately to revenue due to the larger seal dimensions, higher-performance specifications, and elevated replacement frequency associated with heavy-duty operating profiles.

Key participants with significant exposure to the rubber oil seals segment include NOK Corporation, which holds a globally recognized position in precision rubber sealing components and has deep OEM supply relationships across Japan, Europe, and North America. SKF leverages its materials expertise and global manufacturing footprint to deliver engineered rubber seals under its LR and HMS product families. NAK Sealing Technologies Corporation has built a strong position in Asia Pacific and North American markets through continuous investment in rubber compounding R&D. The Timken Company integrates rubber oil seal production within its broader power transmission portfolio, enabling bundled solutions for bearing-and-seal assemblies that reduce OEM procurement complexity.

The rubber oil seals segment's share is not merely holding — it is actively expanding in premium applications as electrification creates new sealing requirements for e-motor shaft assemblies and thermal management circuits, most of which are being addressed with FKM and silicone rubber formulations. This dual growth dynamic — replacement-driven volume in conventional powertrains plus specification-driven value uplift from electrification — ensures the rubber oil seals sub-segment remains the structural anchor of the broader Automotive Oil Seals Market for the foreseeable future.

Manufacturing investments in advanced injection molding, bonded metal-rubber assemblies, and PTFE lip coating technologies are further differentiating premium rubber seal offerings, enabling suppliers to command 15–25% price premiums over standard grades while locking in OEM design approvals that create multi-year supply security.

The Automotive Oil Seals Market is propelled by a convergence of structural and cyclical forces, each quantifiable within the available market intelligence framework.

The most significant demand driver is global vehicle production recovery and expansion. Following production disruptions between 2020 and 2022 attributable to semiconductor shortages and supply chain dislocations, global light vehicle production has rebounded sharply, with annual output tracking toward 95 million units by 2025. Each vehicle requires multiple oil seals across powertrain, driveline, and chassis systems, creating a near-linear linkage between production volumes and seal demand.

A second structural driver is the increasing powertrain complexity associated with turbocharged gasoline direct injection (TGDI) and diesel engines. These architectures operate at higher combustion pressures and oil circuit pressures than naturally aspirated predecessors, subjecting oil seals to more demanding thermal and mechanical loads. This raises both the per-vehicle seal content and the specification grade required, elevating average revenue per vehicle. Turbocharged engines now account for over 50% of global passenger vehicle production, a share that continues to rise.

The global vehicle aftermarket also provides a durable demand buffer. With average vehicle age exceeding 12 years in the United States and over 11 years in Western Europe, the installed base requiring seal maintenance is vast. This aftermarket channel, which typically carries higher margins than OEM supply, insulates market revenue against new vehicle production cycles.

On the constraint side, raw material price volatility represents the most significant headwind. Fluoroelastomers and specialty nitrile compounds are petroleum-derived or chemically synthesized materials whose input costs fluctuate with crude oil prices, specialty monomer supply, and energy prices. FKM costs in particular have been subject to significant inflation, as global FKM production capacity is concentrated among a limited number of global chemical producers, creating supply concentration risk. This margin pressure is particularly acute for smaller, regional seal manufacturers with limited hedging capability.

Electrification also introduces a structural constraint on conventional seal volume over a multi-decade horizon, as battery electric vehicles eliminate internal combustion engine seal points. However, this is partially offset by new EV-specific sealing applications in e-axles, battery thermal management, and cooling circuits.

The Automotive Oil Seals Market features a moderately concentrated competitive landscape, with global Tier 1 suppliers competing alongside strong regional specialists. The following profiles outline the strategic positioning of key participants:

Leak Pack: A specialist sealing solutions provider with focused product development in automotive rubber seals, Leak Pack serves both OEM and aftermarket segments with competitively priced standard and custom seal configurations.

The Timken Company: A globally recognized power transmission leader, The Timken Company integrates oil seal manufacturing within its comprehensive bearing and mechanical power transmission portfolio, leveraging bundled supply programs with major OEM customers across North America, Europe, and Asia Pacific.

JTEKT Corporation: JTEKT, a Japanese multinational and Toyota Group affiliate, combines deep OEM relationships with advanced materials research capabilities to produce high-performance oil seals for passenger and commercial vehicle applications globally.

UK Seals & Polymers Ltd: A UK-based specialist manufacturer, UK Seals & Polymers Ltd focuses on precision-engineered rubber and polymer sealing components for the automotive aftermarket and industrial sectors, with a strong European distribution network.

NS Bearings: NS Bearings offers an integrated portfolio of bearings and associated sealing solutions, leveraging cross-selling opportunities within its distribution channels to penetrate both OEM and replacement markets effectively.

NOK Corporation: One of the world's largest oil seal manufacturers, NOK Corporation holds dominant OEM supply positions across Japanese and international automakers, supported by decades of fluoroelastomer compounding expertise and vertically integrated manufacturing.

SKF: A Swedish engineering group with global leadership in bearings and seals, SKF invests heavily in R&D for advanced elastomer compounds and PTFE-based sealing technologies, maintaining comprehensive coverage across all major automotive seal application categories.

NAK Sealing Technologies Corporation: Specializing exclusively in oil seals and hydraulic seals, NAK Sealing Technologies Corporation has built a globally recognized product portfolio with particularly strong penetration in Asia Pacific and North American OEM supply chains.

SSP Manufacturing Inc: SSP Manufacturing Inc focuses on precision rubber and metal-rubber bonded sealing components, serving automotive OEM and Tier 1 supplier programs with a strong emphasis on custom-engineered solutions.

Blue Diamond Technologies Limited: Blue Diamond Technologies Limited provides advanced sealing and polymer components with growing capabilities in high-performance elastomer formulations suited to electrified powertrain applications.

January 2024: SKF announced the expansion of its sealing solutions manufacturing facility in Pune, India, targeting a 30% increase in production capacity to address surging demand from domestic OEMs and export programs.

March 2024: NOK Corporation unveiled a new generation of FKM-based crankshaft oil seals engineered for continuous operating temperatures up to 230°C, specifically targeting the growing population of 48V mild-hybrid and full-hybrid powertrains in the Japanese and European markets.

June 2024: The Timken Company completed the integration of a specialty sealing components manufacturer into its engineered bearings business unit, consolidating its oil seal product line and expanding aftermarket distribution reach across Latin American markets.

September 2024: JTEKT Corporation entered a joint development agreement with a leading European automaker to co-engineer next-generation e-axle shaft seals for battery electric vehicle platforms scheduled for production launch in 2026.

November 2024: NAK Sealing Technologies Corporation announced a capital investment program targeting advanced PTFE lip seal production lines at its North American facility, responding to increasing OEM demand for low-friction sealing solutions in fuel-efficiency-optimized powertrain applications.

February 2025: Industry trade body ASTM International released updated test standards for automotive dynamic oil seals, incorporating new endurance protocols designed to validate seal performance under electrified powertrain thermal cycling conditions.

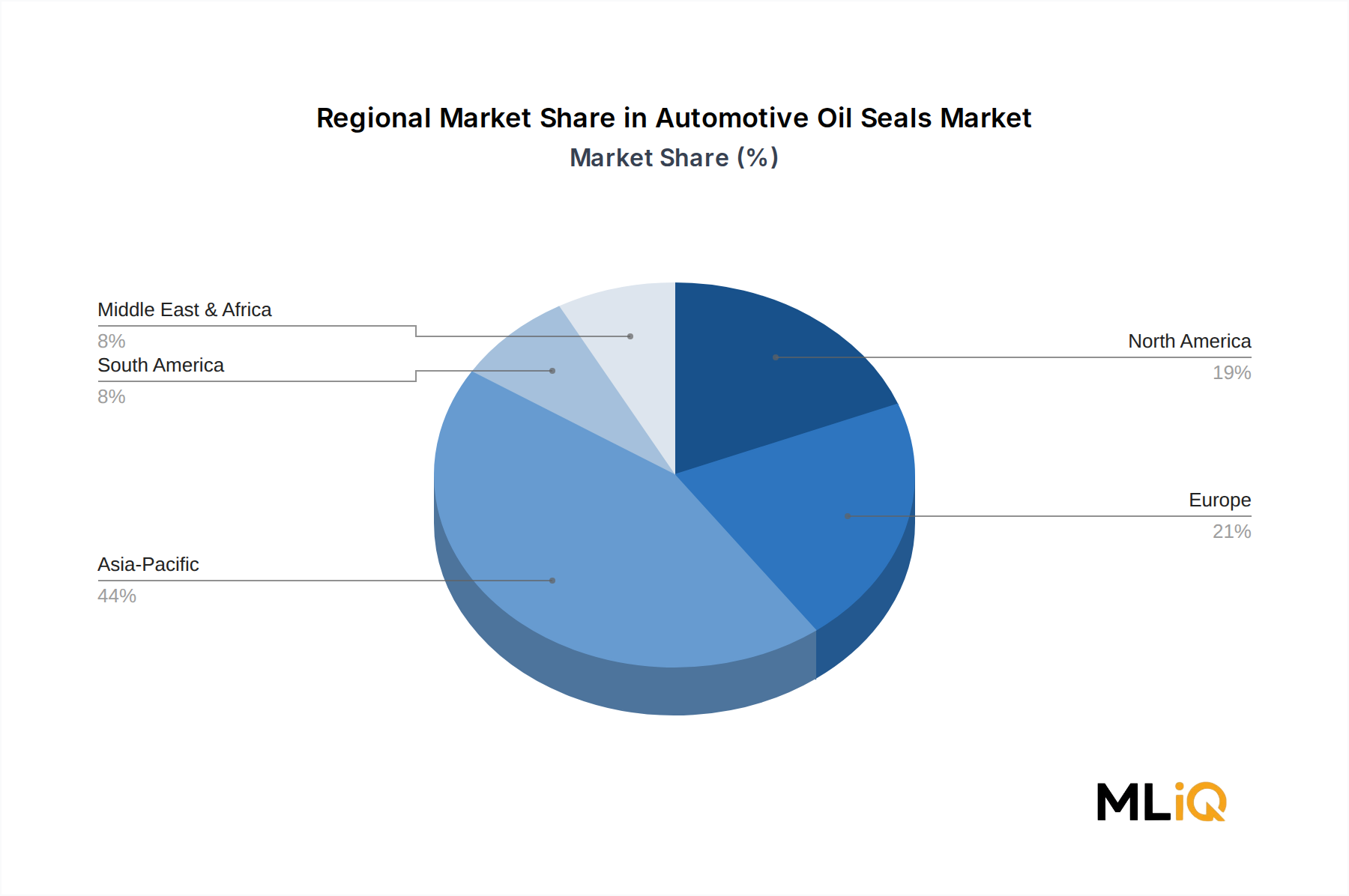

The Automotive Oil Seals Market exhibits distinct regional growth profiles, reflecting differential automotive production volumes, fleet age dynamics, and electrification adoption rates.

Asia Pacific constitutes the largest regional market, accounting for an estimated 42–45% of global revenue in 2025. China alone contributes the plurality of this share, driven by world-leading vehicle production volumes — exceeding 30 million units annually — and a rapidly maturing automotive aftermarket as the vehicle parc ages. India is the fastest-growing sub-region, posting a regional CAGR approaching 8.5%, underpinned by passenger vehicle and two-wheeler production expansion and a government push toward vehicle manufacturing self-sufficiency under the Production Linked Incentive (PLI) scheme. Japan and South Korea contribute high-value premium seal demand aligned with their globally competitive OEM ecosystems.

North America represents the second-largest market, valued at approximately $3.8–4.2 billion in 2025, with a projected CAGR of 5.1%. The United States dominates regional demand, supported by one of the world's oldest vehicle parcs, robust light truck and SUV production, and a highly developed automotive aftermarket distribution infrastructure. Mexico is an increasingly important production hub, with expanding Tier 1 and Tier 2 supplier ecosystems serving North American OEM assembly plants.

Europe is characterized by high technical specification requirements and strong regulatory compliance pressures, contributing approximately 22–24% of global market revenue. Germany remains the regional epicenter, home to premium OEM brands with high per-vehicle seal content and demanding engineering standards. Europe's CAGR of approximately 4.8% reflects the region's automotive maturity, though electrification-driven reformulation demand is creating premium product upgrade cycles.

The Middle East & Africa and South America regions, while smaller in absolute terms, are emerging growth markets. Brazil leads South American demand with a CAGR of approximately 6.0%, tied to commercial vehicle fleet expansion and improving aftermarket penetration. The GCC countries within the Middle East are driving replacement market growth given high vehicle usage intensity and extreme thermal operating conditions that accelerate seal degradation.

The Automotive Oil Seals Market is undergoing a meaningful technology transformation, driven by three converging innovation vectors that are reshaping both product architecture and competitive dynamics.

The first is advanced fluoropolymer and fluoroelastomer seal engineering. The proliferation of turbocharged, downsized engines and hybrid thermal management systems has pushed the operating envelope for oil seals beyond the capability of standard NBR formulations. FKM compounds, reinforced with nano-mineral fillers and PTFE particulates for reduced friction coefficients, are displacing NBR in a growing proportion of OEM seal specifications. R&D investment in this area is significant — leading producers such as NOK Corporation and SKF allocate substantial portions of their engineering budgets to compound development, with laboratory-to-production cycles now compressing to 18–24 months for formulation refinements.

The second innovation trajectory is PTFE and composite lip seal technology. PTFE (polytetrafluoroethylene) labyrinth and lip seal designs offer near-zero breakout friction, near-elimination of stick-slip under cold-start conditions, and outstanding chemical resistance to modern synthetic lubricant additive packages. Adoption is accelerating in fuel-economy-optimized OEM programs where parasitic friction reduction from drivetrain seals is quantifiably mapped to CO2 emission compliance calculations. The Sealing Solutions Market is witnessing a structural shift as PTFE-based products command premium ASPs.

The third and most disruptive innovation is the development of sealing solutions tailored specifically for battery electric and fuel-cell vehicles. E

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6.3% from 2020-2034 |

| Segmentation |

|

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Comprehensive validation mechanisms ensuring market intelligence accuracy, reliability, and adherence to international standards.

500+ data sources cross-validated

200+ industry specialists validation

NAICS, SIC, ISIC, TRBC standards

Continuous market tracking updates

Factors such as are projected to boost the Automotive Oil Seals Market market expansion.

Key companies in the market include Leak Pack, The Timken Company, JTEKT Corporation, UK Seals & Polymers Ltd, NS Bearings, NOK Corporation, SKF, NAK Sealing Technologies Corporation., SSP Manufacturing Inc, Blue Diamond Technologies Limited.

The market segments include Type, Sales Channel, Application, HCV.

The market size is estimated to be USD 15.56 billion as of 2022.

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3690, USD 5820, and USD 9870 respectively.

The market size is provided in terms of value, measured in billion and volume, measured in .

Yes, the market keyword associated with the report is "Automotive Oil Seals Market," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Automotive Oil Seals Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.