1. What are the major growth drivers for the North American Drivetrain Market market?

Factors such as are projected to boost the North American Drivetrain Market market expansion.

+1 2315155523

Market Lens IQ is a global market intelligence and strategic consulting firm delivering advanced syndicated research reports, customized industry analysis, competitive intelligence, and data-driven advisory solutions to organizations across international markets. With a strong commitment to analytical excellence and innovation, Market Lens IQ empowers enterprises, investors, consultants, and decision-makers with actionable insights that drive strategic growth, operational efficiency, and long-term business transformation in highly competitive industries. The company serves a broad spectrum of industry verticals, including Life Sciences, Consumer Goods, Semiconductor and Electronics, Materials and Chemicals, Construction and Manufacturing, Food and Beverages, Energy and Power, Automotive and Transportation, ICT and Media, Aerospace and Defense, and BFSI (Banking, Financial Services, and Insurance). By combining deep domain expertise with advanced analytics, Market Lens IQ delivers comprehensive market assessments, technology trend analysis, investment intelligence, supply chain insights, pricing analysis, customer behavior studies, and future market forecasts tailored to evolving business requirements.

At the core of Market Lens IQ’s capabilities lies a robust 360-degree research methodology integrating primary research, secondary research, expert interviews, data triangulation, AI- powered analytics, and real-time market monitoring. Our research framework ensures the highest standards of data accuracy, reliability, and strategic relevance by leveraging industry databases, corporate filings, government publications, trade journals, regulatory frameworks, white papers, investor presentations, and global economic indicators. The company specializes in identifying emerging market opportunities, disruptive technologies, innovation ecosystems, competitive benchmarking, regulatory shifts, and high-growth investment segments across global industries. Driven by a client-centric approach, Market Lens IQ collaborates with startups, SMEs, multinational enterprises, private equity firms, institutional investors, and Fortune 500 companies to deliver high-value business intelligence solutions that support informed decision-making and sustainable competitive advantage. Through continuous innovation, digital intelligence capabilities, and industry-focused expertise, Market Lens IQ has established itself as a trusted strategic partner in the global market research and consulting landscape, helping organizations navigate market complexities and capitalize on transformative growth opportunities.

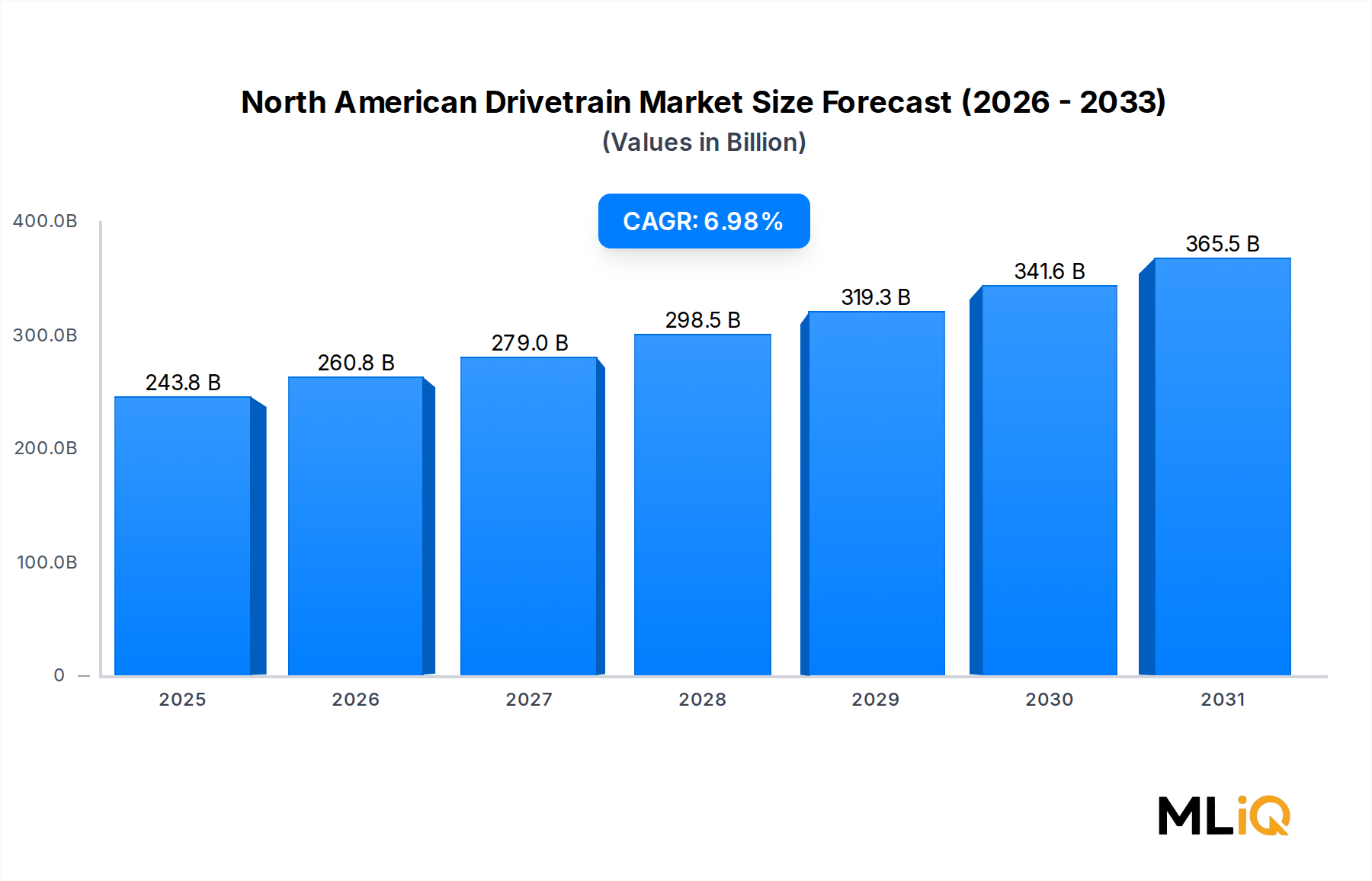

The North American Drivetrain Market is valued at $243.81 billion in the base year 2025, reflecting its position as one of the most capital-intensive and strategically consequential segments within the continental automotive manufacturing ecosystem. The market is projected to expand at a compound annual growth rate (CAGR) of 6.98% through the forecast period of 2025 to 2033, driven by a confluence of electrification mandates, lightweighting imperatives, and sustained demand across passenger and commercial vehicle segments.

At its core, the North American Drivetrain Market encompasses the full spectrum of torque-transfer and power-delivery components — axles, driveshafts, differentials, transmission systems, transfer cases, and coupling mechanisms — that translate engine or motor output into tractive effort at the wheel. The technological transformation underway across OEM production floors is reshaping procurement patterns, supplier hierarchies, and product lifecycle timelines at an unprecedented pace.

Several macro tailwinds underpin this trajectory. First, the accelerating transition toward battery electric vehicles (BEVs) and plug-in hybrid electric vehicles (PHEVs) is prompting a wholesale redesign of drivetrain architectures. Traditional multi-speed transmissions give way to single-speed reducers and integrated e-axle assemblies. Second, tightening fuel economy standards under revised CAFE regulations continue to incentivize the adoption of advanced AWD and torque-vectoring systems that optimize energy use across all four corners of the vehicle. Third, the post-pandemic reshoring of automotive supply chains into Mexico and the Sunbelt states of the U.S. is generating substantial greenfield capital expenditure in drivetrain component manufacturing.

Regional demand within North America is heavily anchored in the United States, which accounts for the dominant share of OEM production volume. Canada contributes through its established assembly plants and tier-1 supplier ecosystem, while Mexico is rapidly emerging as a low-cost, high-throughput manufacturing hub for drivetrain subassemblies exported to final assembly facilities across the continent.

Looking forward through 2033, the market's trajectory will be shaped by the competitive dynamics between incumbent drivetrain specialists adapting to electrification and new-entrant e-drive system integrators. Strategic M&A, joint ventures around e-axle platforms, and software-defined torque management represent the defining battlegrounds. The CAGR of 6.98% signals robust, sustained expansion that outpaces historical averages for automotive powertrain segments, reflecting structural demand rather than cyclical recovery alone.

Among the drive-type segments — front-wheel drive (FWD), rear-wheel drive (RWD), and all-wheel drive (AWD) — the AWD configuration has emerged as the revenue-dominant category within the North American Drivetrain Market, and its share continues to consolidate rather than plateau. This dominance is rooted in both consumer preference dynamics and OEM platform strategy.

North American consumers, particularly in the northern United States and Canada, have consistently prioritized all-weather traction capability over fuel economy incrementalism. The sport utility vehicle and crossover segments, which together represent the plurality of new vehicle sales in the United States, are disproportionately configured with AWD systems. Industry data consistently shows that AWD take rates on mid-size crossovers in markets like the Great Lakes region, the Pacific Northwest, and the Canadian prairies routinely exceed 60% to 70% of total trim configurations sold. This geographic and consumer preference overlap creates a structural floor for AWD drivetrain demand that is largely insulated from short-term economic fluctuations.

From an OEM architecture standpoint, AWD systems have become platform differentiators. Major automakers including General Motors, Ford, and Stellantis have invested heavily in on-demand and full-time AWD technologies that can be software-calibrated to optimize between efficiency and performance. This software integration layer adds margin to the AWD drivetrain stack while increasing switching costs for downstream buyers.

The competitive landscape within the AWD segment is dominated by a set of well-capitalized tier-1 and tier-2 suppliers. Magna Internationals Inc. is particularly prominent, offering a wide range of AWD coupling systems and eAWD modules that are fitted across multiple OEM platforms. GKN PLC brings deep expertise in driveshaft and propshaft integration, which is critical for AWD torque vectoring. Dana Holding Corp. has leveraged its Spicer brand to supply AWD-compatible differential and axle assemblies to both light truck and passenger car platforms. Borg Warner's intelligent all-wheel drive systems, including its Torque-On-Demand coupling, are embedded in numerous North American-assembled vehicles.

The evolution of AWD architectures in the context of vehicle electrification is particularly notable. Electric AWD configurations — where independent motors drive the front and rear axles without a mechanical connection — are becoming increasingly prevalent on BEV platforms. This e-AWD topology eliminates the traditional prop shaft and transfer case, fundamentally restructuring the bill of materials. However, it creates new demand for precision motor controllers, torque arbitration software, and high-voltage coupling harnesses — components that incumbent drivetrain suppliers are racing to internalize or acquire.

FWD remains relevant primarily in entry-level sedan and compact crossover segments, where cost optimization remains paramount. RWD, while retained in performance vehicles and traditional body-on-frame trucks, occupies a more niche position in terms of unit volume. The structural shift in consumer preference from FWD sedans to AWD crossovers over the past decade has been the single most consequential demand-side force in reshaping the North American Drivetrain Market's segmentation profile.

Considering all these vectors, AWD's revenue dominance is not only entrenched but is likely to deepen as electrification enables new AWD configurations at lower incremental cost relative to the overall vehicle price point.

The North American Drivetrain Market is propelled by a set of quantifiable structural drivers and tempered by identifiable constraints that any strategic participant must navigate with precision.

Electrification mandates represent the foremost demand driver. The U.S. Environmental Protection Agency's revised vehicle emissions standards, finalized in 2024, target an industry fleet average equivalent to approximately 85 miles per gallon CO2-equivalent by 2032, effectively requiring mass electrification. This regulatory pressure directly translates into OEM capital allocation toward e-axle and integrated drivetrain development programs, with estimated cumulative OEM drivetrain R&D expenditure across the continent projected to exceed $40 billion through 2030.

Light truck and SUV production volume is a second driver. The U.S. light truck segment — encompassing pickups, SUVs, and crossovers — accounted for approximately 78% of total new vehicle sales in 2024, a record share. Since drivetrain content per vehicle is materially higher for trucks and SUVs than for passenger cars, this sales mix enrichment is highly favorable for average revenue per unit across the drivetrain supply chain.

NAFSTA-era and USMCA-framed manufacturing integration has created a highly interconnected North American drivetrain supply chain, enabling just-in-time delivery economics that allow suppliers to operate at lean inventory ratios. Mexico's expanding automotive manufacturing base — with over 15 OEM assembly plants operational or under construction as of 2025 — creates sustained component sourcing demand.

On the constraint side, raw material cost volatility is the most acute headwind. Steel and aluminum, which constitute the majority of drivetrain structural mass, experienced price spikes of 30% to 50% during 2021–2022 and remain susceptible to geopolitical supply disruptions. Rare earth elements critical for electric motor magnets embedded in e-axle systems are subject to Chinese export controls, introducing supply chain concentration risk.

Skilled labor shortages at precision machining facilities across Michigan, Ohio, and Ontario further constrain production scalability and elevate per-unit labor costs. Workforce transition demands as ICE drivetrain workers retool for EV component manufacturing add a structural friction cost to the electrification pivot.

The competitive landscape of the North American Drivetrain Market is characterized by a blend of diversified global tier-1 suppliers, specialized drivetrain integrators, and regionally focused component manufacturers. Below is a strategic profile of the primary participants:

ATC Drivetrain: A specialist remanufacturer and rebuilder of transfer cases and transmissions, ATC Drivetrain serves the aftermarket and fleet replacement segments with a cost-competitive proposition focused on product reliability and rapid order fulfillment.

Borg Warner: A global powertrain technology leader, Borg Warner has aggressively repositioned its portfolio toward electrification through the acquisition of Delphi Technologies and Akasol, offering integrated e-drive modules, high-voltage inverters, and thermal management systems alongside its legacy torque management products.

Showa Corp.: A Honda Group affiliate, Showa Corp. specializes in steering and suspension systems with drivetrain-adjacent driveshaft components, leveraging its close OEM relationships to supply into compact and mid-size vehicle platforms across North America.

Magna Internationals Inc.: One of the most diversified automotive suppliers globally, Magna Internationals Inc. offers a comprehensive drivetrain portfolio encompassing AWD systems, e-axles, driveline modules, and transmission components, with major production footprint across Ontario, Michigan, and Mexico.

Aisin Seiki Co.: A Toyota Group company, Aisin Seiki Co. is a dominant supplier of automatic transmissions and AWD transfer cases, with its products embedded across a wide range of North American-assembled Toyota, Lexus, and third-party OEM platforms.

American Axle & Manufacturing Inc.: Headquartered in Detroit, American Axle & Manufacturing Inc. is a vertically integrated producer of driveline and metal forming products, with strong exposure to GM's truck and SUV platforms and an expanding e-Beam and e-Drive product line targeting electrification.

Allison Transmission: Focused primarily on fully automatic transmissions for commercial vehicles and specialty applications, Allison Transmission holds a near-dominant position in the North American heavy-duty truck and bus transmission segment and is expanding into electric hybrid propulsion for fleet applications.

GKN PLC: A global engineering group with deep expertise in driveshafts, eDrive systems, and powder metallurgy components, GKN PLC supplies driveline components across virtually every major OEM platform active in North America.

Dana Holding Corp.: Dana Holding Corp. provides axle, driveshaft, sealing, and thermal management products across light, medium, and heavy vehicle segments, with a growing Spicer Electrified product line aimed at commercial EV drivetrains.

JATCO: A Nissan-affiliated transmission specialist, JATCO is one of the world's largest CVT manufacturers and supplies continuously variable and stepped automatic transmissions to multiple OEM brands active in the North American market.

January 2025: Borg Warner announced a multi-year supply agreement with a major Detroit-based OEM for its fourth-generation eDS (eDrive System) module, targeting production volumes starting in 2026 for a new electric truck platform.

March 2025: American Axle & Manufacturing Inc. broke ground on a $120 million electric driveline manufacturing facility in Auburn Hills, Michigan, intended to supply e-Beam axle assemblies for next-generation electric light trucks.

April 2025: Dana Holding Corp. secured a contract to supply Spicer Electrified e-axles to a Class 6–7 commercial EV manufacturer operating in the U.S. regional delivery segment, with initial volume deliveries scheduled for late 2025.

May 2025: Magna Internationals Inc. unveiled its next-generation eAWD module at the SAE World Congress in Detroit, featuring an integrated oil-cooled motor design achieving a 12% improvement in torque density versus the prior generation.

June 2025: Allison Transmission received certification for its H 50 EP electric hybrid propulsion system from California's Air Resources Board (CARB), enabling fleet operators to qualify for clean vehicle incentive programs under the Inflation Reduction Act.

August 2025: GKN PLC completed the expansion of its Driveline Americas manufacturing campus in Newton, North Carolina, adding 200,000 square feet of production capacity dedicated to electric vehicle driveshaft assemblies.

October 2025: JATCO announced a technical collaboration with a North American engineering firm to adapt its next-generation CVT platform for mild-hybrid applications, targeting production readiness by 2027.

The North American Drivetrain Market exhibits pronounced regional differentiation across its three primary geographies — the United States, Canada, and Mexico — with additional context drawn from cross-border trade dynamics and supply chain geography.

The United States is the dominant revenue contributor to the North American Drivetrain Market, accounting for an estimated 68% to 72% of total regional market value. The country's vast light truck production base, concentrated in Michigan, Indiana, Ohio, Kentucky, and Tennessee, generates unparalleled drivetrain component demand. The U.S. market is also the epicenter of EV drivetrain investment, with the Inflation Reduction Act's domestic content provisions incentivizing North American localization of battery and drivetrain manufacturing. The U.S. sub-market is projected to grow at a CAGR of approximately 6.5% through 2033, reflecting its maturity relative to the continental average but sustained by electrification capex.

Canada represents a structurally important but relatively mature sub-market, contributing roughly 12% to 15% of total regional drivetrain revenue. Ontario's automotive corridor — anchored by Windsor, Cambridge, Woodstock, and Alliston — hosts a dense concentration of assembly plants and tier-1 supplier facilities. The Canadian drivetrain sub-market is growing at an estimated CAGR of 5.8% to 6.2%, constrained by a smaller consumer base but supported by export-oriented production for the U.S. market and growing EV assembly investment by Honda, Toyota, and Stellantis.

Mexico is the fastest-growing geography within the North American Drivetrain Market, driven by aggressive OEM assembly investment and its preferential USMCA trade status. Mexico's drivetrain sub-market is projected to expand at a CAGR of 8.5% to 9.2% through 2033, significantly outpacing the continental average. The Bajio region — encompassing Guanajuato, Aguascalientes, and San Luis Potosi — has emerged as a tier-1 drivetrain manufacturing cluster, with BMW, General Motors, Stellantis, and Volkswagen all operating major assembly facilities within the region. Lower labor costs, proximity to U.S. final assembly plants, and improving logistics infrastructure make Mexico the primary growth engine for drivetrain component production across the continent.

Trade flows between the three nations are deeply integrated, with the majority of North American drivetrain subassembly crossing at least one international border before final vehicle assembly. This integration creates systemic interdependence that amplifies both the growth opportunities and the policy risk exposure across all three sub-markets.

Pricing dynamics within the North American Drivetrain Market are defined by a persistent tension between OEM cost-reduction mandates and the rising engineering content embedded in next-generation drivetrain systems. The average selling price (ASP) of a complete passenger car drivetrain assembly — encompassing transmission, axles, driveshafts, and differentials — has historically ranged between $1,800 and $3,500 depending on drive configuration and vehicle segment. AWD and 4WD system assemblies command premium pricing, with full-time AWD packages in the $2,800 to $4,500 range at the tier-1 supplier level.

However, the structural shift toward electric drivetrain architectures is introducing significant ASP disruption. E-axle modules for BE

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6.98% from 2020-2034 |

| Segmentation |

|

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Comprehensive validation mechanisms ensuring market intelligence accuracy, reliability, and adherence to international standards.

500+ data sources cross-validated

200+ industry specialists validation

NAICS, SIC, ISIC, TRBC standards

Continuous market tracking updates

Factors such as are projected to boost the North American Drivetrain Market market expansion.

Key companies in the market include ATC Drivetrain, Borg Warner, Showa Corp., Magna Internationals Inc., Aisin Seiki Co., American Axle & Manufacturing Inc., Allison Transmission, GKN PLC, Dana Holding Corp., JATCO.

The market segments include Drive Type, Vehicle Type.

The market size is estimated to be USD 243.81 billion as of 2022.

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3200, USD 4245, and USD 6270 respectively.

The market size is provided in terms of value, measured in billion and volume, measured in .

Yes, the market keyword associated with the report is "North American Drivetrain Market," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the North American Drivetrain Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.