1. What are the major growth drivers for the Agricultural Tires Market market?

Factors such as are projected to boost the Agricultural Tires Market market expansion.

Market Lens IQ is a global market intelligence and strategic consulting firm delivering advanced syndicated research reports, customized industry analysis, competitive intelligence, and data-driven advisory solutions to organizations across international markets. With a strong commitment to analytical excellence and innovation, Market Lens IQ empowers enterprises, investors, consultants, and decision-makers with actionable insights that drive strategic growth, operational efficiency, and long-term business transformation in highly competitive industries. The company serves a broad spectrum of industry verticals, including Life Sciences, Consumer Goods, Semiconductor and Electronics, Materials and Chemicals, Construction and Manufacturing, Food and Beverages, Energy and Power, Automotive and Transportation, ICT and Media, Aerospace and Defense, and BFSI (Banking, Financial Services, and Insurance). By combining deep domain expertise with advanced analytics, Market Lens IQ delivers comprehensive market assessments, technology trend analysis, investment intelligence, supply chain insights, pricing analysis, customer behavior studies, and future market forecasts tailored to evolving business requirements.

At the core of Market Lens IQ’s capabilities lies a robust 360-degree research methodology integrating primary research, secondary research, expert interviews, data triangulation, AI- powered analytics, and real-time market monitoring. Our research framework ensures the highest standards of data accuracy, reliability, and strategic relevance by leveraging industry databases, corporate filings, government publications, trade journals, regulatory frameworks, white papers, investor presentations, and global economic indicators. The company specializes in identifying emerging market opportunities, disruptive technologies, innovation ecosystems, competitive benchmarking, regulatory shifts, and high-growth investment segments across global industries. Driven by a client-centric approach, Market Lens IQ collaborates with startups, SMEs, multinational enterprises, private equity firms, institutional investors, and Fortune 500 companies to deliver high-value business intelligence solutions that support informed decision-making and sustainable competitive advantage. Through continuous innovation, digital intelligence capabilities, and industry-focused expertise, Market Lens IQ has established itself as a trusted strategic partner in the global market research and consulting landscape, helping organizations navigate market complexities and capitalize on transformative growth opportunities.

+1 2315155523

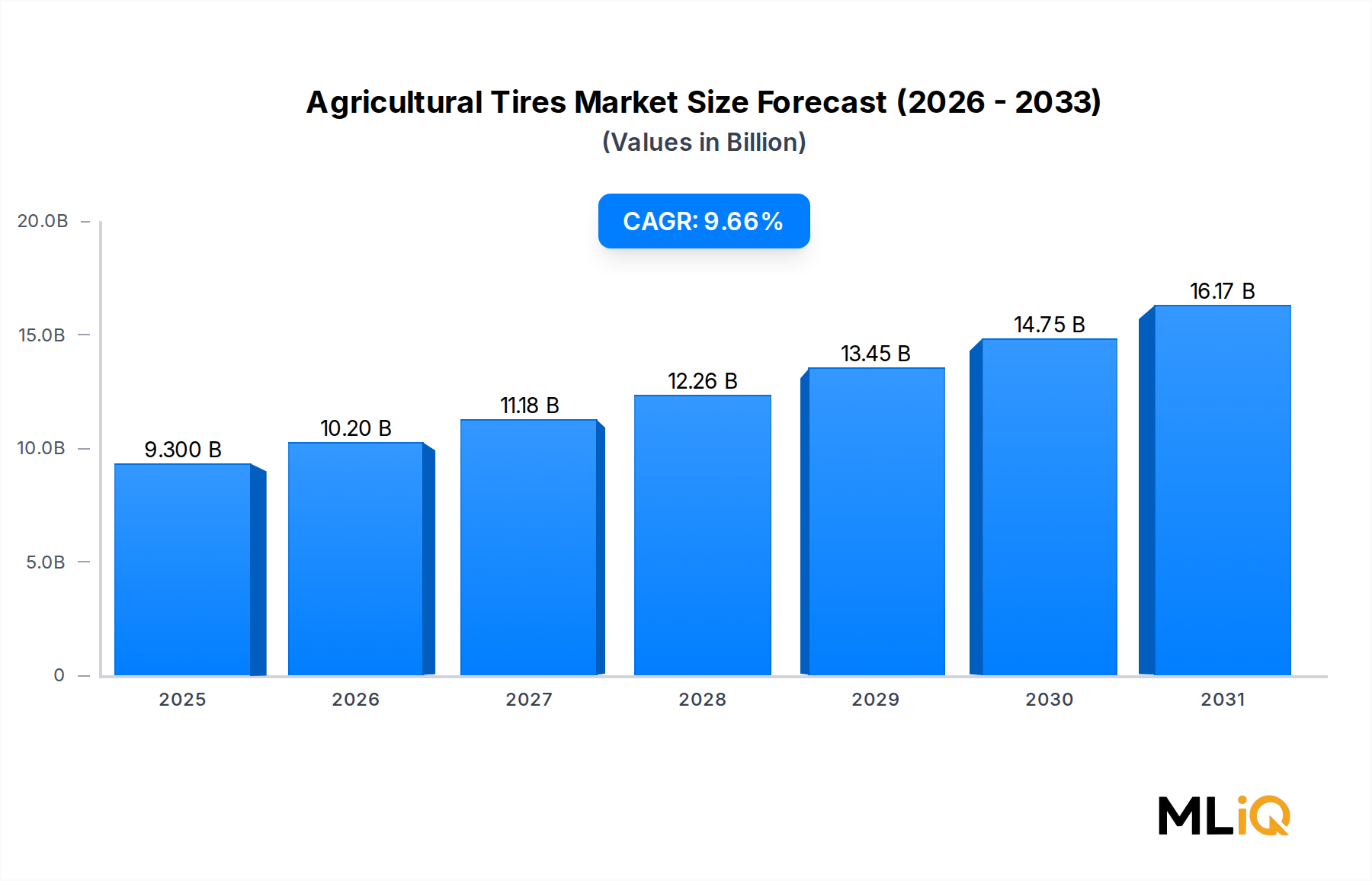

The global Agricultural Tires Market was valued at $9.3 billion in 2024 and is projected to expand at a compound annual growth rate (CAGR) of 9.66% through 2033, reflecting robust demand dynamics driven by mechanization trends, rising food security imperatives, and accelerating adoption of precision farming technologies. This growth trajectory positions the market to surpass $21 billion by the end of the forecast period, underscoring the critical role of specialized tire solutions in modern agricultural operations.

Several macro-level forces are converging to sustain this momentum. Global arable land per capita continues to decline, compelling farmers to extract greater productivity from existing acreage, which in turn elevates demand for high-performance equipment — and by extension, the tires that support it. The United Nations Food and Agriculture Organization projects that global food production must increase by approximately 70% by 2050 to meet population demands, placing substantial pressure on agricultural mechanization value chains.

From a demand-driver perspective, the replacement and aftermarket segment is gaining disproportionate traction as the installed base of agricultural machinery worldwide continues to mature. Tractors, combine harvesters, sprayers, and loaders collectively represent a massive fleet requiring periodic tire replacement, creating a structurally recurring revenue stream for tire manufacturers. OEM channels, meanwhile, benefit from rising new equipment sales in emerging economies across Asia Pacific, South America, and Africa.

Technological advancements in tire construction — notably the transition from bias-ply to radial designs — are reshaping the competitive landscape. Radial tires offer superior fuel efficiency, lower soil compaction, and extended service life, attributes that resonate strongly with farmers under cost-containment pressures and increasingly subject to environmental compliance requirements.

Geopolitically, supply chain realignments following pandemic-era disruptions and raw material price volatility have prompted leading manufacturers to diversify sourcing and invest in regional production hubs. This strategic pivot is gradually restructuring the global supply architecture, with implications for pricing competitiveness and delivery lead times.

The competitive ecosystem remains concentrated among a handful of globally integrated players — including Michelin, Bridgestone, Goodyear, and Continental — though regional challengers in China and India are steadily eroding incumbent market shares in price-sensitive segments. Innovation intensity is rising, with investment flowing into smart tire technologies, embedded sensors, and sustainable rubber compounding, signaling that the next competitive frontier will be defined as much by digital capability as by manufacturing scale.

Overall, the Agricultural Tires Market enters the 2025–2033 forecast window with strong fundamental support, moderate competitive rivalry, and meaningful upside from emerging-market mechanization and technology-driven product premiumization.

Among all tire type segments, radial tires represent the single largest revenue contributor within the Agricultural Tires Market, commanding an estimated share exceeding 58% of global revenues in 2024. This dominance is not incidental; it reflects a decades-long structural shift driven by agronomic, economic, and regulatory forces that continue to reinforce the segment's leadership position.

Radial tire architecture — characterized by cord plies arranged perpendicular to the direction of travel and a stabilizing belt package beneath the tread — delivers a suite of performance advantages that are uniquely aligned with the operational requirements of modern agricultural machinery. Chief among these is reduced soil compaction. As soil health has emerged as a central concern for both productivity and regulatory compliance in major farming economies, the larger, more flexible footprint of radial tires versus bias alternatives has become a decisive purchasing criterion. Studies conducted across European agricultural research institutions have demonstrated that radial tires can reduce soil compaction by up to 20–30% compared with equivalent bias-ply designs, a finding that has permeated extension services and OEM specification sheets globally.

Fuel economy is a second structural advantage. Radial tires exhibit lower rolling resistance, translating to measurable diesel consumption savings across a typical farming season. Given that fuel represents one of the largest variable cost items in commercial farming — often 30–40% of total operating expenses — even marginal efficiency gains carry significant economic weight. This efficiency narrative has been particularly compelling in North America and Western Europe, where large-scale commodity producers operate extensive equipment fleets and are acutely sensitive to per-acre input costs.

From a competitive standpoint, the radial tire segment is dominated by global integrated manufacturers. Michelin, through its AGRIBIB and AXIOBIB product lines, has consistently positioned radial technology as the premium standard, investing heavily in compound development to optimize traction, wear resistance, and load-carrying capacity under varied soil and speed conditions. Bridgestone's VT-TRACTOR series and Goodyear's DT800 Super series similarly reflect sustained R&D investment in high-value radial applications.

Continental and Yokohama Tire have also expanded their radial agricultural portfolios in recent years, targeting the mid-market tier where product differentiation is increasingly based on total cost of ownership rather than unit price. Meanwhile, Chinese manufacturers — including China National Tire & Rubber and Cheng-Shin Rubber — are aggressively scaling their radial production capabilities, competing on price while improving quality standards to gain acceptance in Southeast Asian and African markets.

The radial segment's share is not merely holding; it is growing. Radial penetration in developing agricultural economies — including India, Brazil, and key ASEAN markets — remains below the saturation levels seen in North America and Europe, indicating meaningful runway for volume expansion. Indian tractor OEMs, for instance, have been progressively shifting factory-fitted tire specifications toward radial designs as farmer awareness of long-term cost benefits improves and financing accessibility for premium equipment expands.

Product innovation within the radial segment is also advancing along several axes: very high flexion (VF) and intermediate flexion (IF) tire technologies allow operation at lower inflation pressures without sacrificing load capacity, further reducing compaction impacts. These next-generation variants are expected to command a growing share of the radial segment premium tier over the forecast period, supporting average selling price appreciation and revenue mix improvement for leading manufacturers.

In summary, the radial tire segment's dominance within the Agricultural Tires Market is structurally entrenched, technologically advancing, and geographically still expanding, positioning it as the primary engine of market revenue growth through 2033.

The Agricultural Tires Market is propelled by a well-defined set of demand drivers while simultaneously navigating a series of structural constraints that modulate growth velocity.

On the demand side, agricultural mechanization rates in emerging economies represent the most significant volume growth catalyst. India's tractor industry sold approximately 0.9 million units in 2023–2024, making it the world's largest tractor market by volume. Each new tractor sale generates immediate OEM tire demand and initiates a replacement cycle that recurs every 3–5 years depending on usage intensity. Brazil's Cerrado region and Argentina's Pampas continue to expand cultivated acreage, driving demand for large-format tires suited to the wide-span machinery used in row-crop production.

Precision agriculture adoption is a secondary but increasingly important driver. The Precision Agriculture Market is expanding rapidly, and as GPS-guided equipment, autonomous tractors, and variable-rate application systems become mainstream, demand for tires that minimize field damage during intensive, GPS-directed field operations intensifies. This creates a quality upgrade cycle that benefits premium radial and VF/IF tire manufacturers.

The replacement and aftermarket channel provides demand stability. The global agricultural machinery fleet represents hundreds of millions of tire positions requiring periodic replacement, insulating market revenues from cyclical OEM production fluctuations to a meaningful degree.

On the constraint side, raw material price volatility represents the most acute margin risk. Natural rubber — a primary input — experienced price swings of 25–40% in certain periods between 2020 and 2024, compressing manufacturer margins and complicating long-term contract pricing. Synthetic rubber derived from petroleum-based feedstocks introduces correlated exposure to crude oil price cycles.

Geographic concentration of rubber supply — with Thailand, Indonesia, and Vietnam collectively accounting for over 70% of global natural rubber production — creates systemic sourcing risk. Climate-related disruptions, disease outbreaks affecting rubber tree plantations (such as South American Leaf Blight), and labor market dynamics in producer countries can rapidly tighten supply and escalate input costs.

Farm income cyclicality also acts as a demand moderator. When commodity prices for corn, soybeans, wheat, or cotton decline sharply, farmers defer discretionary capital expenditures including tire replacement, creating periodic demand troughs that affect aftermarket revenues.

The competitive landscape of the Agricultural Tires Market is characterized by a tiered structure of global integrated manufacturers, regional specialists, and emerging-market challengers. The following profiles capture the strategic posture of the primary participants:

Michelin: The French tire giant maintains a commanding premium position in agricultural radial tires, leveraging its AXIOBIB 2 and TRAILXBIB product lines. Michelin's investment in very high flexion technology and its global distribution network of over 170 countries reinforce its leadership in the high-value segment.

Bridgestone: Operating through its agricultural tire division and the Firestone Agricultural brand, Bridgestone combines breadth of product range with deep OEM relationships with major farm equipment manufacturers. The company's VT-TRACTOR series has been widely adopted across North American and European large-farm operations.

Goodyear: Goodyear's agricultural tire portfolio targets both the premium and mid-market tiers, with particular strength in the North American aftermarket channel. Its DT800 Super and IT620 lines are widely specified by large-scale grain and row-crop producers.

Continental: Continental has steadily expanded its agricultural tire business globally, investing in radial technology and digital tire management solutions. Its TractorMaster and CombineMaster product lines address tractor and harvester applications respectively.

Yokohama Tire: Yokohama competes across multiple agricultural segments, with growing presence in Asia Pacific markets. The company has been investing in sustainable rubber compounding and low-emission manufacturing processes as part of its ESG commitments.

MRF: India's largest tire manufacturer by revenue, MRF holds a dominant position in the domestic agricultural tire market, benefiting from deep distribution penetration in rural India and strong brand equity among smallholder and mid-scale farmers.

Cheng-Shin Rubber: Operating under the MAXXIS brand, Cheng-Shin Rubber has aggressively expanded its agricultural tire portfolio targeting price-sensitive markets across Asia, Africa, and Latin America. Its manufacturing cost advantages support competitive pricing at scale.

China National Tire & Rubber: As one of China's state-backed tire conglomerates, this entity operates across multiple agricultural tire categories, leveraging low-cost domestic manufacturing and government-supported export financing to compete in emerging markets.

Belshina: The Belarusian manufacturer holds a specialized niche in large-format tires for heavy agricultural and forestry equipment, with distribution concentrated in Eastern Europe and the CIS region.

Eurotire.: A regional player with focused presence in European aftermarket channels, offering both radial and bias products across tractor and implement applications.

January 2024: Michelin announced the global commercial launch of its AXIOBIB 2 very high flexion tire range for large-frame tractors, offering enhanced load capacity at reduced inflation pressure and targeting large-scale farming operations in North America and Western Europe.

March 2024: Bridgestone revealed a strategic partnership with a leading European precision agriculture software provider to develop integrated tire pressure monitoring and soil impact management systems, combining hardware and data analytics into a unified farm management offering.

May 2024: Continental introduced its updated TractorMaster Hybrid compound formulation, claiming a 12% improvement in tread wear life compared with its predecessor, targeting the high-utilization aftermarket replacement segment.

August 2024: India's MRF completed capacity expansion at its Tiruvottiyur manufacturing facility, adding dedicated agricultural radial tire production lines with an annual output capacity increase of approximately 500,000 units, targeting domestic OEM and export markets.

October 2024: Goodyear signed an agreement to supply tires for a major autonomous tractor platform under development by a North American agricultural technology company, marking an early commitment to the emerging autonomous farm machinery segment.

December 2024: The European Tyre and Rubber Manufacturers' Association (ETRMA) published updated guidance on agricultural tire sustainability labeling, establishing new benchmarks for rolling resistance, durability reporting, and end-of-life material recovery applicable to tires sold within EU member states from 2026 onward.

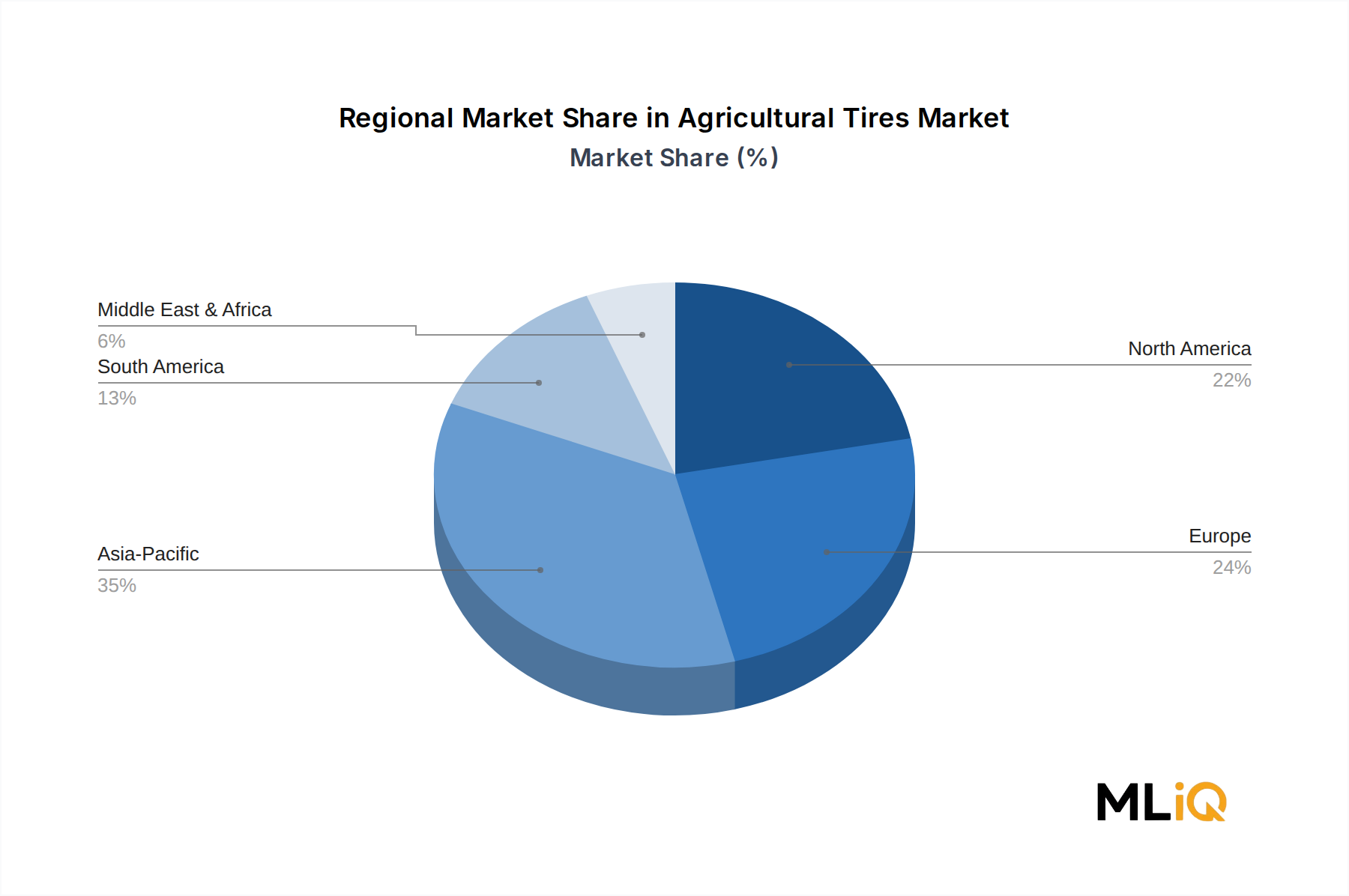

The Agricultural Tires Market exhibits significant regional heterogeneity in terms of growth rates, demand structure, and competitive intensity, reflecting differences in agricultural mechanization maturity, farm structure, and macroeconomic conditions.

Asia Pacific represents the fastest-growing regional market, projected to expand at a CAGR of approximately 11.5% through 2033. The region's growth is anchored by India and China, which together account for the world's two largest agricultural machinery fleets. India's government-subsidized farm mechanization programs, combined with rising rural incomes and favorable credit access for equipment purchases, are driving sustained volume demand. Southeast Asian markets — particularly Indonesia, Vietnam, and Thailand — are contributing incremental growth as plantation agriculture and paddy farming operations increase equipment intensity.

North America is the most mature regional market, accounting for an estimated 28% of global revenue in 2024. The region is characterized by a large, well-maintained equipment fleet, high average tire sizes (driven by the prevalence of wide-span row-crop machinery), and strong aftermarket replacement demand. Growth is moderate at approximately 7.2% CAGR, driven by product premiumization toward VF/IF radial technologies and the expansion of precision-guided equipment platforms.

Europe represents the second-largest revenue region, driven by Western European large-farm operations in France, Germany, and the United Kingdom, as well as expanding mechanization in Central and Eastern European economies. EU sustainability regulations are accelerating the transition from bias to radial tires and creating demand for environmentally certified products. The region is projected to grow at approximately 7.8% CAGR through 2033.

South America — led by Brazil and Argentina — is a high-growth market supported by continuous agricultural frontier expansion in the Cerrado and Patagonian regions. Brazil alone represents one of the world's largest markets for large-frame tractor and combine harvester tires. Regional CAGR is estimated at 10.2%, though currency volatility and political risk introduce forecast uncertainty.

Middle East and Africa remains the smallest but most nascent regional segment, with a projected CAGR of 9.1%. Subsistence farming transitions toward mechanized commercial agriculture in Sub-Saharan Africa, supported by international development finance and government modernization programs, are laying the groundwork for sustained volume growth through the forecast period.

The supply chain underpinning the Agricultural Tires Market is complex, geographically concentrated at the raw material level, and subject to multiple interacting risk vectors that have demonstrated their capacity to materially disrupt production economics.

Natural rubber constitutes the single most critical upstream input, typically comprising 40–50% of the rubber compound in agricultural tire formulations. As noted previously, the Natural Rubber Market is geographically concentrated in Southeast Asia, exposing agricultural tire manufacturers to regional supply shocks from weather events, phytosanitary threats, and geopolitical developments. Prices for Standard Malaysian Rubber (SMR 20) and Thai RSS3 grades have historically exhibited high interannual volatility, with movements of 20–45% observed across multiple commodity cycles in the past decade. The price trend through 2023–2024 has been broadly upward due to constrained supply growth relative to expanding automotive and industrial demand.

Synthetic rubber — primarily styrene-butadiene rubber (SBR) and butadiene rubber (BR) — provides a partial substitute and blending option for manufacturers seeking to manage natural rubber cost exposure. However, SBR and BR pricing is correlated with crude oil and naphtha markets, meaning synthetic alternatives do not fully decouple manufacturers from energy price cycles. The Carbon Black Market is equally relevant, as carbon black — a critical reinforcing filler

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 9.66% from 2020-2034 |

| Segmentation |

|

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Comprehensive validation mechanisms ensuring market intelligence accuracy, reliability, and adherence to international standards.

500+ data sources cross-validated

200+ industry specialists validation

NAICS, SIC, ISIC, TRBC standards

Continuous market tracking updates

Factors such as are projected to boost the Agricultural Tires Market market expansion.

Key companies in the market include Michelin, Eurotire., Cheng-Shin Rubber, China National Tire & Rubber, Goodyear, Bridgestone, Belshina, MRF, Continental, Yokohama Tire.

The market segments include Sales Channel Type, Application Type, Tire Type.

The market size is estimated to be USD 9.3 billion as of 2022.

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3690, USD 5820, and USD 9870 respectively.

The market size is provided in terms of value, measured in billion and volume, measured in .

Yes, the market keyword associated with the report is "Agricultural Tires Market," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Agricultural Tires Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.