1. What are the major growth drivers for the Web Services Cloud Market market?

Factors such as are projected to boost the Web Services Cloud Market market expansion.

+1 2315155523

Market Lens IQ is a global market intelligence and strategic consulting firm delivering advanced syndicated research reports, customized industry analysis, competitive intelligence, and data-driven advisory solutions to organizations across international markets. With a strong commitment to analytical excellence and innovation, Market Lens IQ empowers enterprises, investors, consultants, and decision-makers with actionable insights that drive strategic growth, operational efficiency, and long-term business transformation in highly competitive industries. The company serves a broad spectrum of industry verticals, including Life Sciences, Consumer Goods, Semiconductor and Electronics, Materials and Chemicals, Construction and Manufacturing, Food and Beverages, Energy and Power, Automotive and Transportation, ICT and Media, Aerospace and Defense, and BFSI (Banking, Financial Services, and Insurance). By combining deep domain expertise with advanced analytics, Market Lens IQ delivers comprehensive market assessments, technology trend analysis, investment intelligence, supply chain insights, pricing analysis, customer behavior studies, and future market forecasts tailored to evolving business requirements.

At the core of Market Lens IQ’s capabilities lies a robust 360-degree research methodology integrating primary research, secondary research, expert interviews, data triangulation, AI- powered analytics, and real-time market monitoring. Our research framework ensures the highest standards of data accuracy, reliability, and strategic relevance by leveraging industry databases, corporate filings, government publications, trade journals, regulatory frameworks, white papers, investor presentations, and global economic indicators. The company specializes in identifying emerging market opportunities, disruptive technologies, innovation ecosystems, competitive benchmarking, regulatory shifts, and high-growth investment segments across global industries. Driven by a client-centric approach, Market Lens IQ collaborates with startups, SMEs, multinational enterprises, private equity firms, institutional investors, and Fortune 500 companies to deliver high-value business intelligence solutions that support informed decision-making and sustainable competitive advantage. Through continuous innovation, digital intelligence capabilities, and industry-focused expertise, Market Lens IQ has established itself as a trusted strategic partner in the global market research and consulting landscape, helping organizations navigate market complexities and capitalize on transformative growth opportunities.

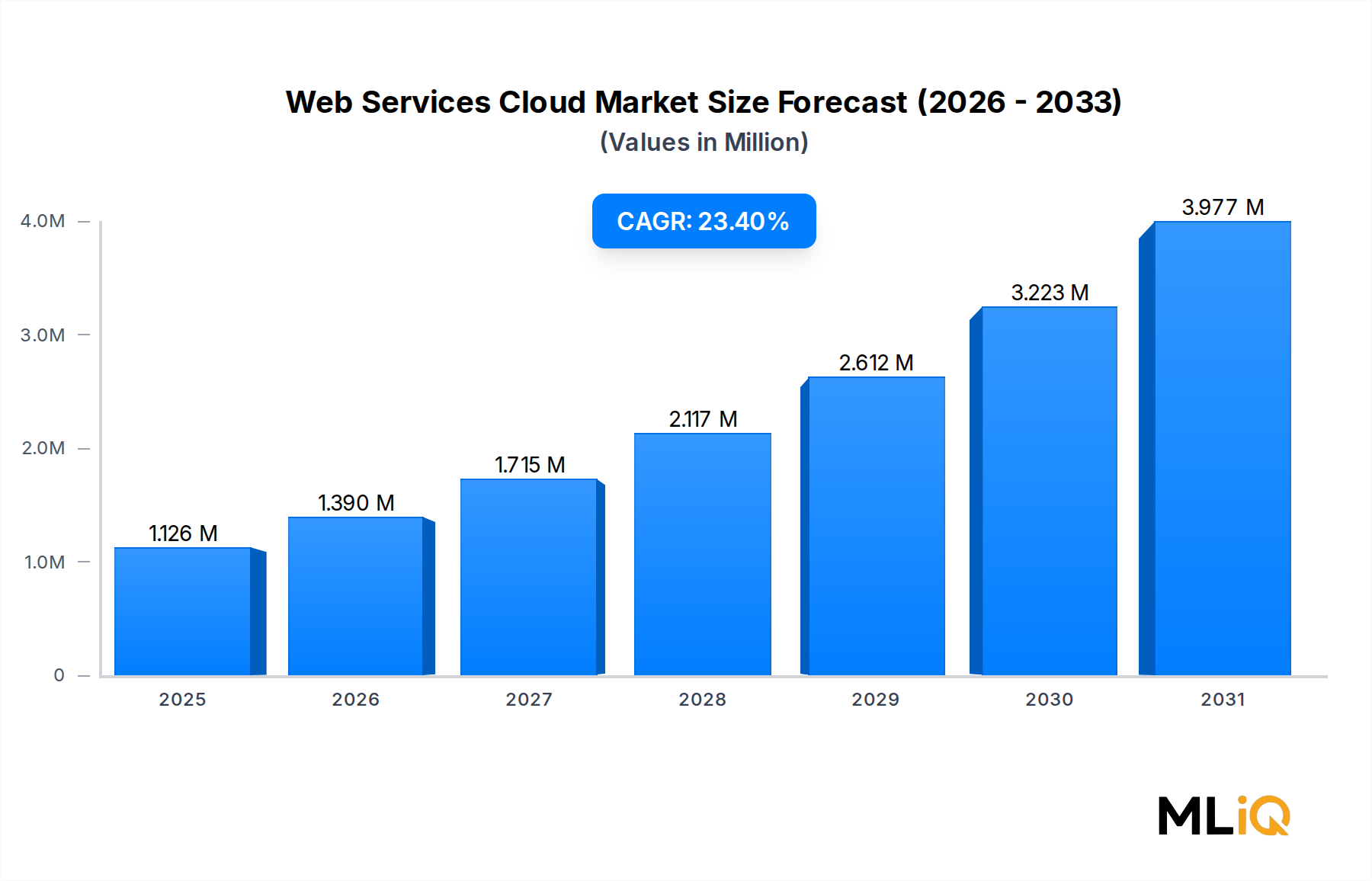

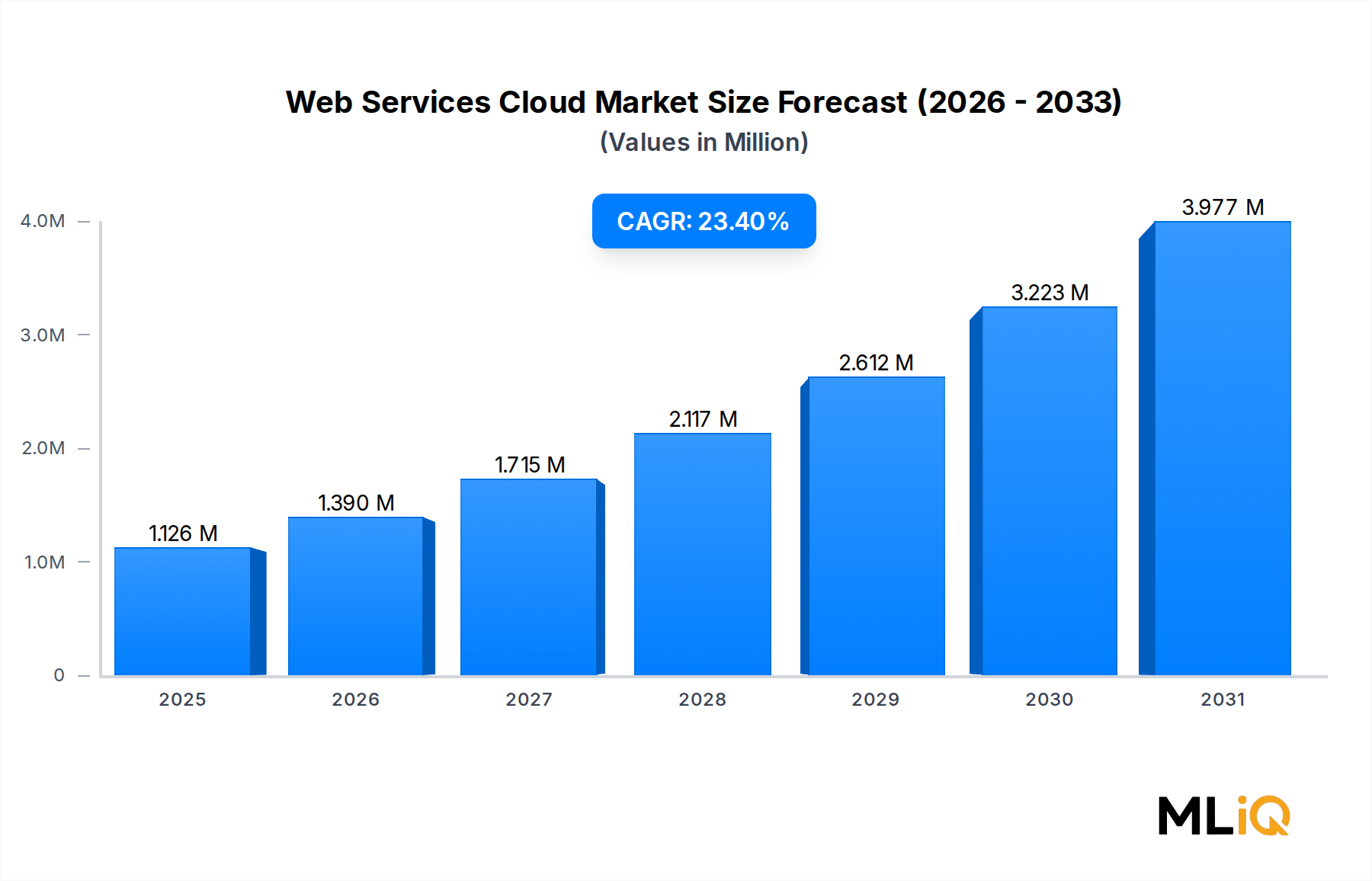

The global Web Services Cloud Market is valued at $1,126.36 billion in 2025, establishing it as one of the most capital-intensive and strategically significant segments within the broader ICT and Media landscape. Driven by an exceptional compound annual growth rate of 23.4%, the market is projected to more than quadruple over the forecast horizon, underpinned by accelerating enterprise digitalization, the proliferation of AI-native workloads, and the irreversible migration of mission-critical applications to cloud-native architectures.

Several macro tailwinds are converging to sustain this growth trajectory. First, hyperscaler capital expenditure commitments continue to reach record levels, with leading providers announcing multi-year infrastructure investment programs exceeding hundreds of billions of dollars collectively. Second, generative AI and large language model deployments are driving disproportionate demand for scalable compute and storage resources—precisely the domain where cloud platforms excel. Third, regulatory frameworks in the European Union, North America, and Asia Pacific are increasingly mandating data residency and sovereignty compliance, pushing organizations toward managed cloud environments that offer certified, auditable infrastructure.

On the demand side, small and medium enterprises (SMEs) are emerging as a decisive growth cohort, enabled by consumption-based pricing models that eliminate upfront capital expenditure. Concurrently, large enterprises are shifting from lift-and-shift migrations to cloud-native refactoring, deepening their dependency on platform-layer services and multi-cloud orchestration tools. The democratization of cloud access through edge nodes and local availability zones is expanding addressable markets into regions previously constrained by latency and connectivity limitations.

From a segment perspective, Infrastructure as a Service continues to dominate total revenue share, while Software as a Service maintains the highest volume of active workloads. Public cloud deployments hold the largest share by deployment type, though private cloud is experiencing accelerated adoption in regulated verticals such as financial services, healthcare, and defense.

The competitive landscape is intensifying as second-tier providers differentiate on price transparency, geographic reach, and vertical-specific compliance certifications. The entry of sovereign cloud initiatives in Europe and the Middle East is further reshaping competitive dynamics. Forward-looking indicators—including developer ecosystem metrics, API call volumes, and multi-cloud adoption rates—all point to sustained double-digit expansion through the end of the decade. Organizations that align infrastructure strategy with cloud-native principles today are positioned to capture compounding efficiency gains as the market matures.

Within the segmentation framework of the Web Services Cloud Market, the public cloud deployment mode stands as the unambiguous revenue leader, commanding the majority of total market value and continuing to expand its share as enterprise adoption matures. Public cloud architecture—defined by shared, multi-tenant infrastructure operated and maintained by third-party hyperscalers—offers a combination of elastic scalability, global availability, and economies of scale that private and hybrid alternatives currently cannot fully replicate at equivalent cost efficiency.

The dominance of public cloud is structurally anchored in the economics of hyperscaler operations. Providers such as Amazon Web Services, Google Cloud Platform, and Microsoft Azure (broadly representative of the tier-1 cohort) operate at infrastructure utilization efficiencies that individual enterprise data centers cannot approach. These efficiencies translate directly into pricing power: public cloud providers can offer compute resources at marginal cost structures that make on-premises alternatives progressively less attractive, particularly for variable or burst workloads.

From a service-layer perspective, the public cloud segment encompasses all three primary mode-of-service categories: Infrastructure as a Service, Platform as a Service, and Software as a Service. Among these, Software as a Service represents the highest volume of distinct deployments, as every SaaS application ultimately resides on public cloud infrastructure. Platform as a Service layers—spanning managed Kubernetes, serverless compute, and data pipeline orchestration—are the fastest-growing sub-layers within the public cloud segment, driven by developer productivity mandates and the shift toward microservices-based application architectures.

Key players anchoring the public cloud segment include Amazon Web Services, which consistently reports the highest absolute cloud revenue among global providers; Google Cloud Platform, which has aggressively expanded its AI and analytics service portfolio to differentiate on data workloads; Oracle Cloud, which targets enterprise database migration with aggressive pricing for existing Oracle license holders; and IBM Cloud, which emphasizes hybrid integration and regulated industry compliance. Rackspace operates as a managed services layer atop multiple public clouds, capturing customers who require operational expertise alongside raw infrastructure access.

The share of public cloud within the overall Web Services Cloud Market is not merely holding steady—it is actively growing as a proportion of total deployment. Several structural forces are reinforcing this trend. The proliferation of containerized workloads and Kubernetes-native development eliminates many of the portability barriers that previously tied workloads to private infrastructure. The maturation of zero-trust security architectures is also eroding the security-based objections that historically drove workloads toward private environments. Additionally, the expansion of public cloud providers into local and sovereign cloud zones—dedicated physical infrastructure operated under specific national regulatory frameworks—is absorbing workloads that previously required private deployment for compliance reasons.

Enterprise adoption patterns reveal a pronounced shift toward multi-cloud public strategies, where organizations distribute workloads across two or more hyperscalers to avoid vendor lock-in, optimize cost, and ensure resilience. This behavior is simultaneously expanding total public cloud consumption and complicating provider retention strategies. Providers are responding with enhanced interoperability tooling, committed use discount programs, and vertical-specific cloud environments (e.g., financial services clouds, healthcare clouds) designed to create stickiness through compliance pre-certification rather than technical barriers.

The public cloud segment is also the primary beneficiary of the AI infrastructure boom. Training and inference workloads for large language models and multimodal AI systems require GPU cluster scale that only hyperscaler public clouds currently offer at production grade. This dynamic is expected to sustain public cloud's revenue leadership through the forecast period, even as hybrid and private cloud deployments grow in absolute terms.

The Web Services Cloud Market's 23.4% CAGR through the forecast period is propelled by a constellation of quantifiable drivers, while a discrete set of constraints moderate the pace of expansion in specific geographies and verticals.

Driver 1 — AI and Machine Learning Workload Explosion: Enterprise AI adoption has produced a step-change in cloud compute demand. Industry data indicates that AI-related cloud infrastructure spending grew at more than twice the rate of general cloud infrastructure in recent years, with GPU-accelerated compute emerging as the most capacity-constrained resource across all major hyperscalers. This imbalance is driving premium pricing for AI-optimized instances, expanding average revenue per workload significantly.

Driver 2 — SME Cloud Migration Acceleration: The sub-1,000-employee enterprise segment now represents a disproportionate share of net-new cloud workload additions globally. Consumption-based billing, pre-configured SaaS solutions, and partner-managed cloud services have lowered the activation barrier for SMEs that previously lacked the internal expertise for cloud migration. This demographic shift broadens the total addressable market substantially.

Driver 3 — Regulatory-Driven Compliance Workloads: Frameworks including GDPR in Europe, HIPAA in the United States, and evolving data localization mandates in India, Brazil, and Southeast Asia are compelling organizations to adopt certified cloud environments. Compliance-certified public and private cloud deployments command a pricing premium of 15–25% over standard equivalents, enriching provider margins in regulated verticals.

Driver 4 — Multi-Cloud and Hybrid Architecture Adoption: Enterprise surveys consistently indicate that more than 85% of large organizations now operate in a multi-cloud or hybrid cloud configuration. This increases total cloud spend per organization and drives demand for cloud management platforms, security orchestration tools, and interconnect services.

Constraint 1 — Talent Scarcity: The shortage of certified cloud architects, DevSecOps professionals, and data engineers constrains the pace at which organizations can execute cloud transformation programs. This acts as a demand-side bottleneck, delaying project timelines and increasing implementation costs.

Constraint 2 — Data Sovereignty and Cross-Border Transfer Restrictions: Inconsistent regulatory frameworks across jurisdictions create compliance complexity for multinational deployments, adding latency and cost to cross-border data flows and limiting the addressable market for single-region providers.

Constraint 3 — Hyperscaler Concentration Risk: Customer concerns about dependency on a small number of dominant providers influence procurement decisions, particularly in public sector and critical infrastructure markets, moderating adoption rates in these segments.

The competitive landscape of the Web Services Cloud Market is characterized by a tiered structure: a small cohort of hyperscalers commanding dominant revenue share, a mid-tier of specialist and regional providers competing on price and vertical focus, and a growing layer of managed service providers that abstract complexity across multiple underlying clouds.

AMAZON WEB SERVICES: The global revenue leader in cloud infrastructure services, Amazon Web Services maintains the broadest service portfolio—exceeding 200 distinct services—and benefits from deep enterprise penetration built over more than a decade of market leadership. Its strategic focus on AI accelerator instances and Bedrock generative AI services positions it at the center of the current infrastructure upgrade cycle.

GOOGLE CLOUD PLATFORM: Google Cloud Platform differentiates on data analytics, AI/ML frameworks, and open-source Kubernetes leadership through GKE. Its BigQuery and Vertex AI platforms have driven significant enterprise wins in data-intensive sectors, and the company has posted multiple consecutive quarters of accelerating revenue growth, narrowing the gap with the top two hyperscalers.

IBM CLOUD: IBM Cloud targets hybrid cloud and regulated enterprise segments with a portfolio anchored in IBM Watson, Red Hat OpenShift, and compliance-certified financial services cloud environments. Its acquisition of Red Hat repositioned the company as a hybrid cloud middleware leader, enabling workload portability across on-premises and multi-cloud environments.

ORACLE CLOUD: Oracle Cloud competes aggressively on database migration incentives, offering substantial discounts to existing Oracle license holders who migrate workloads to Oracle Cloud Infrastructure. Its distributed cloud and sovereign cloud offerings are gaining traction in government and financial services verticals with strict data residency requirements.

RACKSPACE: Rackspace operates as a multi-cloud managed services provider, offering Fanatical Support across AWS, Azure, and Google Cloud deployments. This positioning allows it to capture customers seeking operational expertise and SLA accountability without committing to a single hyperscaler.

DIGITALOCEAN: DigitalOcean targets developers and SMEs with simplified infrastructure products, transparent pricing, and a strong developer community. Its acquisition of Cloudways extended its reach into managed application hosting, broadening the addressable customer base beyond pure infrastructure consumers.

CLOUDSIGMA: CloudSigma positions as a European and US-based provider emphasizing full infrastructure customization, pay-per-use billing, and data sovereignty for enterprise and research clients. Its open standards approach appeals to customers seeking to avoid hyperscaler lock-in.

ATLANTIC.NET: Atlantic.net focuses on HIPAA-compliant cloud hosting and managed services for healthcare and life sciences organizations, leveraging compliance certifications as a primary competitive differentiator in a high-margin vertical.

VMWARE: VMware, operating within the Broadcom portfolio, anchors the private and hybrid cloud infrastructure segment through vSphere, NSX, and VMware Cloud Foundation. Its installed base of virtualized enterprise data centers represents a structural distribution advantage for hybrid cloud extension products.

1&1: 1&1 (operating as IONOS) serves the European SME and web hosting market with cloud IaaS and dedicated server products, competing primarily on price and regional data center coverage across Germany, the UK, and broader Europe.

January 2025: Amazon Web Services announced the general availability of its next-generation GPU-accelerated EC2 instances based on NVIDIA H200 architecture, targeting large-scale generative AI training workloads and reinforcing its leadership in AI infrastructure capacity.

February 2025: Google Cloud Platform launched expanded sovereign cloud regions in Saudi Arabia and Malaysia, responding to government data localization mandates and positioning for public sector contract wins in high-growth Middle East and ASEAN markets.

March 2025: Oracle Cloud Infrastructure completed a strategic partnership with a major European telecommunications group to deploy distributed cloud nodes across the operator's national network, targeting latency-sensitive edge workloads and enterprise private connectivity use cases.

March 2025: IBM Cloud received FedRAMP High authorization for an expanded set of managed services, enabling broader deployment across US federal civilian and defense agency environments and strengthening its position in the regulated government cloud segment.

April 2025: DigitalOcean introduced a GPU Droplets product line aimed at AI inference workloads for developer and startup customers, marking its first deliberate entry into the AI infrastructure segment that has driven outsized hyperscaler revenue growth.

April 2025: VMware (Broadcom) released VMware Cloud Foundation 9.0 with enhanced multi-cloud lifecycle management capabilities, integrating AI-driven workload placement optimization and expanded support for ARM-based server architectures.

May 2025: CloudSigma announced a new data center presence in Johannesburg, South Africa, extending its footprint into sub-Saharan Africa and addressing growing enterprise demand for compliant, sovereign cloud infrastructure in the region.

May 2025: Rackspace Technology unveiled a managed AI operations (AIOps) service offering built on multi-cloud infrastructure, targeting enterprise customers seeking to operationalize generative AI applications without building dedicated internal platform engineering teams.

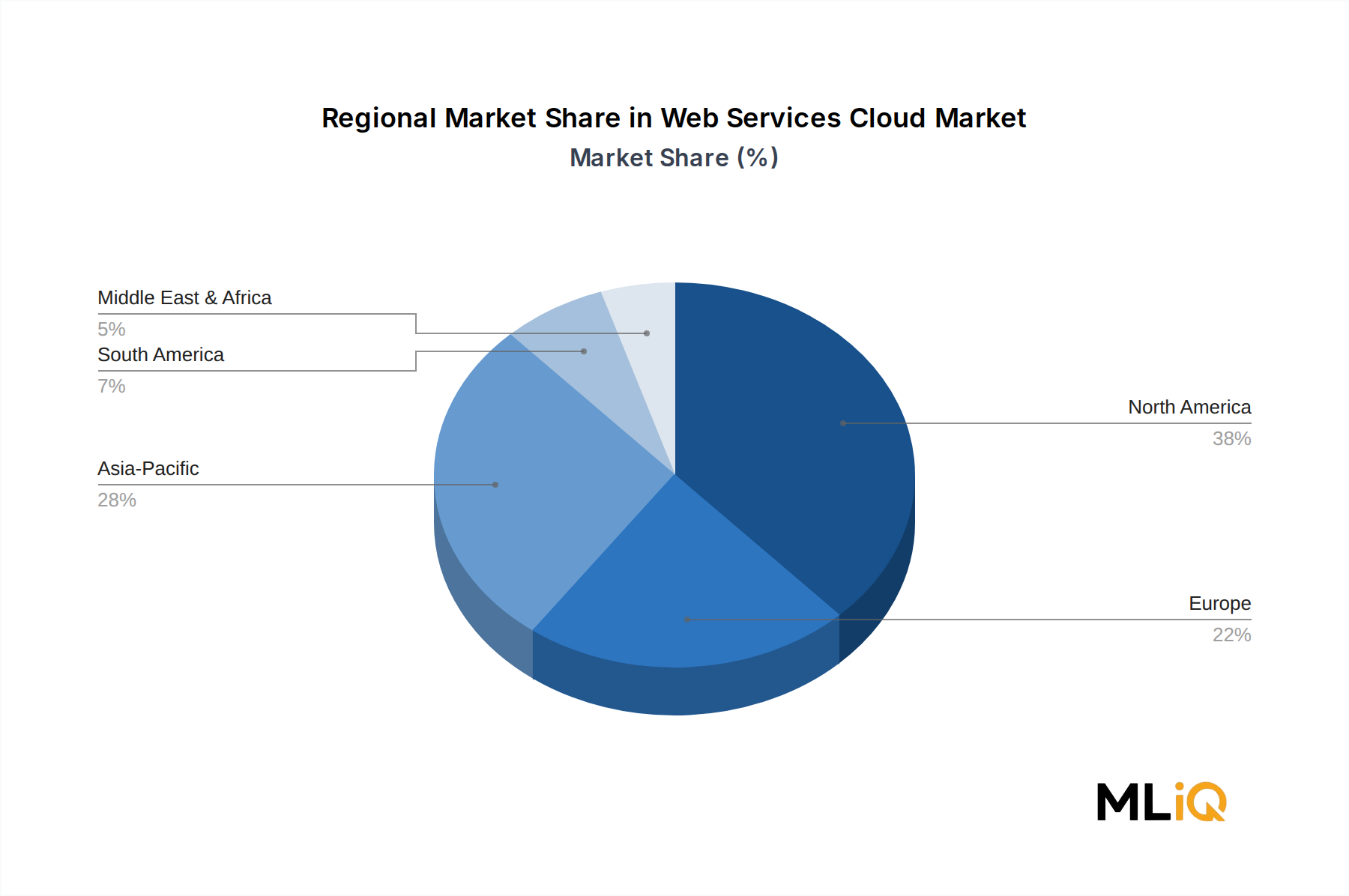

The Web Services Cloud Market exhibits pronounced regional heterogeneity in both revenue concentration and growth velocity, reflecting divergent stages of digital infrastructure maturity, regulatory environments, and enterprise adoption curves.

North America — Dominant Revenue Region: North America accounts for the largest absolute revenue share of the global Web Services Cloud Market, driven by the concentration of hyperscaler headquarters, the highest enterprise IT spending per capita globally, and a mature developer ecosystem. The United States alone represents the single largest national market, anchored by federal cloud mandates, Fortune 500 digital transformation programs, and the AI infrastructure investment cycle. Canada and Mexico contribute incremental growth, with Canada benefiting from data residency relationships with US hyperscalers. The regional CAGR is estimated at approximately 19–21%, slightly below the global average due to baseline maturity effects, but absolute incremental dollar value remains the highest globally.

Europe — Regulatory Complexity with Steady Growth: Europe represents the second-largest regional market, characterized by GDPR-driven compliance demand, strong sovereign cloud investment, and a well-capitalized enterprise base in Germany, the United Kingdom, and France. Data localization requirements are accelerating investment in local cloud availability zones. The regional CAGR is estimated at 18–20%, with Germany and the Nordics leading adoption in manufacturing (Industry 4.0) and public sector digitalization respectively.

Asia Pacific — Fastest-Growing Region: Asia Pacific is the highest-growth regional market within the Web Services Cloud Market, with an estimated CAGR of 27–30% driven by China's domestic cloud expansion, India's digital public infrastructure buildout, and rapid adoption across ASEAN economies. India is a particularly high-velocity market, fueled by government cloud mandates under the Meghraj policy framework and a large base of cloud-native technology firms. Japan and South Korea contribute significant enterprise cloud spend, while ASEAN markets including Indonesia, Vietnam, and the Philippines represent emerging high-growth opportunities as internet penetration and smartphone adoption deepen.

Middle East and Africa — High-Potential Emerging Region: The Middle East and Africa region is experiencing accelerating cloud adoption driven by Vision 2030 digitalization programs in Saudi Arabia and the UAE, hyperscaler data center investment, and sovereign cloud frameworks. The GCC sub-region is the primary revenue driver, while South Africa anchors sub-Saharan African demand. Regional CAGR is estimated at 24–26%.

South America — Nascent but Expanding: Brazil dominates South American cloud spend, supported by a large enterprise base and growing fintech sector. Regional CAGR is estimated at 20–23%, with infrastructure investment and regulatory harmonization serving as the primary growth enablers.

The Web Services Cloud Market operates through a distinctive trade architecture that differs fundamentally from physical goods markets: the primary "export" is cross-border data service delivery, software licensing, and cloud platform access rather than tangible shipments. Nevertheless, trade policy, tariff regimes, and non-tariff barriers exert measurable influence on market structure, vendor positioning, and cross-border revenue flows.

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Comprehensive validation mechanisms ensuring market intelligence accuracy, reliability, and adherence to international standards.

500+ data sources cross-validated

200+ industry specialists validation

NAICS, SIC, ISIC, TRBC standards

Continuous market tracking updates

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 23.4% from 2020-2034 |

| Segmentation |

|

Factors such as are projected to boost the Web Services Cloud Market market expansion.

Key companies in the market include RACKSPACE, AMAZON WEB SERVICES, IBM CLOUD, DIGITALOCEAN, CLOUDSIGMA, ATLANTIC.NET, GOOGLE CLOUD PLATFORM, VMWARE, 1&1, ORACLE CLOUD.

The market segments include Mode, MODE OF SERVICE.

The market size is estimated to be USD 1126.36 billion as of 2022.

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3690, USD 5820, and USD 9870 respectively.

The market size is provided in terms of value, measured in billion and volume, measured in .

Yes, the market keyword associated with the report is "Web Services Cloud Market," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Web Services Cloud Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.