1. What are the major growth drivers for the Server Operating System Market market?

Factors such as are projected to boost the Server Operating System Market market expansion.

Server Operating System Market

Server Operating System Market

Market Lens IQ is a global market intelligence and strategic consulting firm delivering advanced syndicated research reports, customized industry analysis, competitive intelligence, and data-driven advisory solutions to organizations across international markets. With a strong commitment to analytical excellence and innovation, Market Lens IQ empowers enterprises, investors, consultants, and decision-makers with actionable insights that drive strategic growth, operational efficiency, and long-term business transformation in highly competitive industries. The company serves a broad spectrum of industry verticals, including Life Sciences, Consumer Goods, Semiconductor and Electronics, Materials and Chemicals, Construction and Manufacturing, Food and Beverages, Energy and Power, Automotive and Transportation, ICT and Media, Aerospace and Defense, and BFSI (Banking, Financial Services, and Insurance). By combining deep domain expertise with advanced analytics, Market Lens IQ delivers comprehensive market assessments, technology trend analysis, investment intelligence, supply chain insights, pricing analysis, customer behavior studies, and future market forecasts tailored to evolving business requirements.

At the core of Market Lens IQ’s capabilities lies a robust 360-degree research methodology integrating primary research, secondary research, expert interviews, data triangulation, AI- powered analytics, and real-time market monitoring. Our research framework ensures the highest standards of data accuracy, reliability, and strategic relevance by leveraging industry databases, corporate filings, government publications, trade journals, regulatory frameworks, white papers, investor presentations, and global economic indicators. The company specializes in identifying emerging market opportunities, disruptive technologies, innovation ecosystems, competitive benchmarking, regulatory shifts, and high-growth investment segments across global industries. Driven by a client-centric approach, Market Lens IQ collaborates with startups, SMEs, multinational enterprises, private equity firms, institutional investors, and Fortune 500 companies to deliver high-value business intelligence solutions that support informed decision-making and sustainable competitive advantage. Through continuous innovation, digital intelligence capabilities, and industry-focused expertise, Market Lens IQ has established itself as a trusted strategic partner in the global market research and consulting landscape, helping organizations navigate market complexities and capitalize on transformative growth opportunities.

+1 2315155523

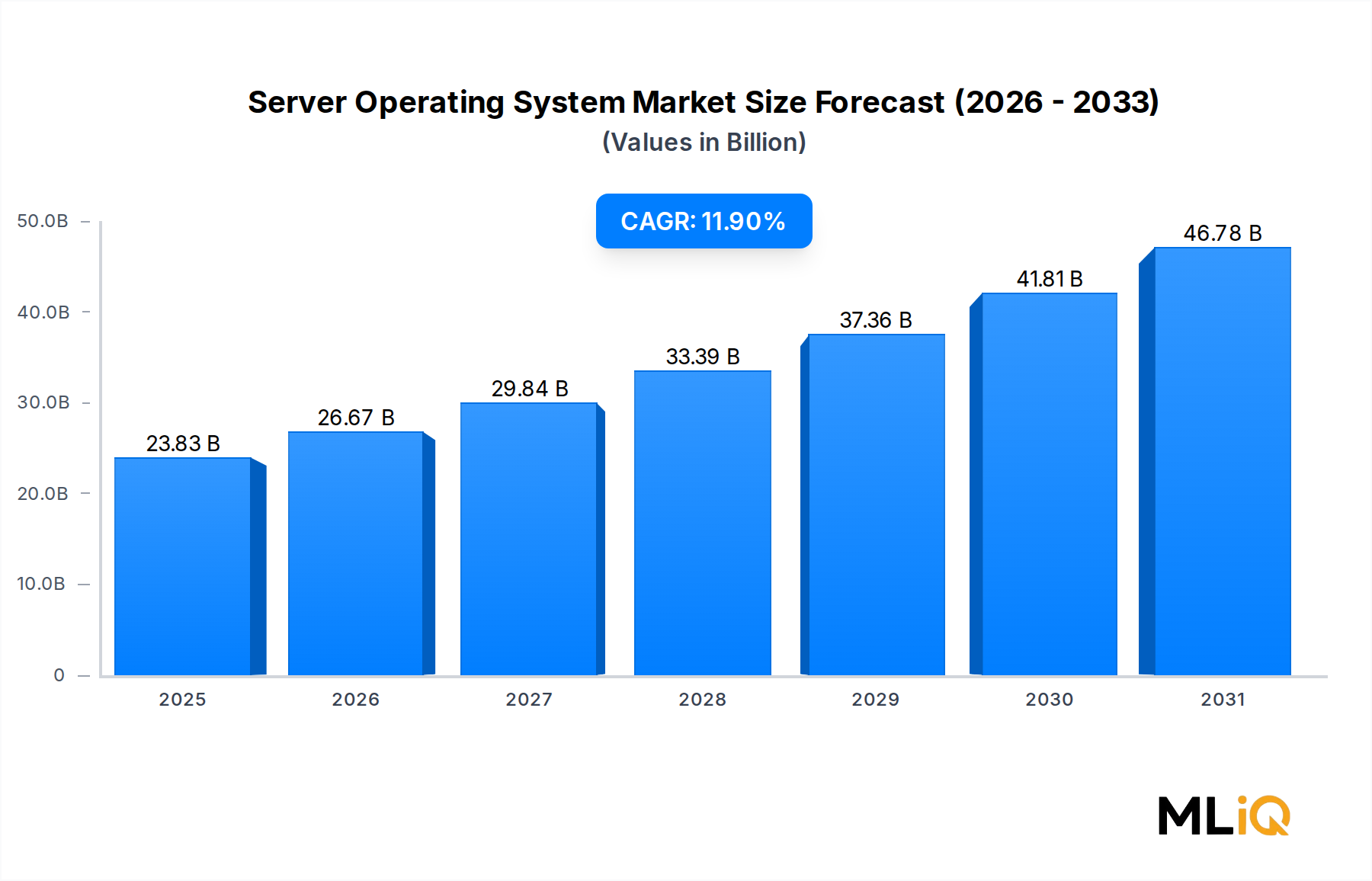

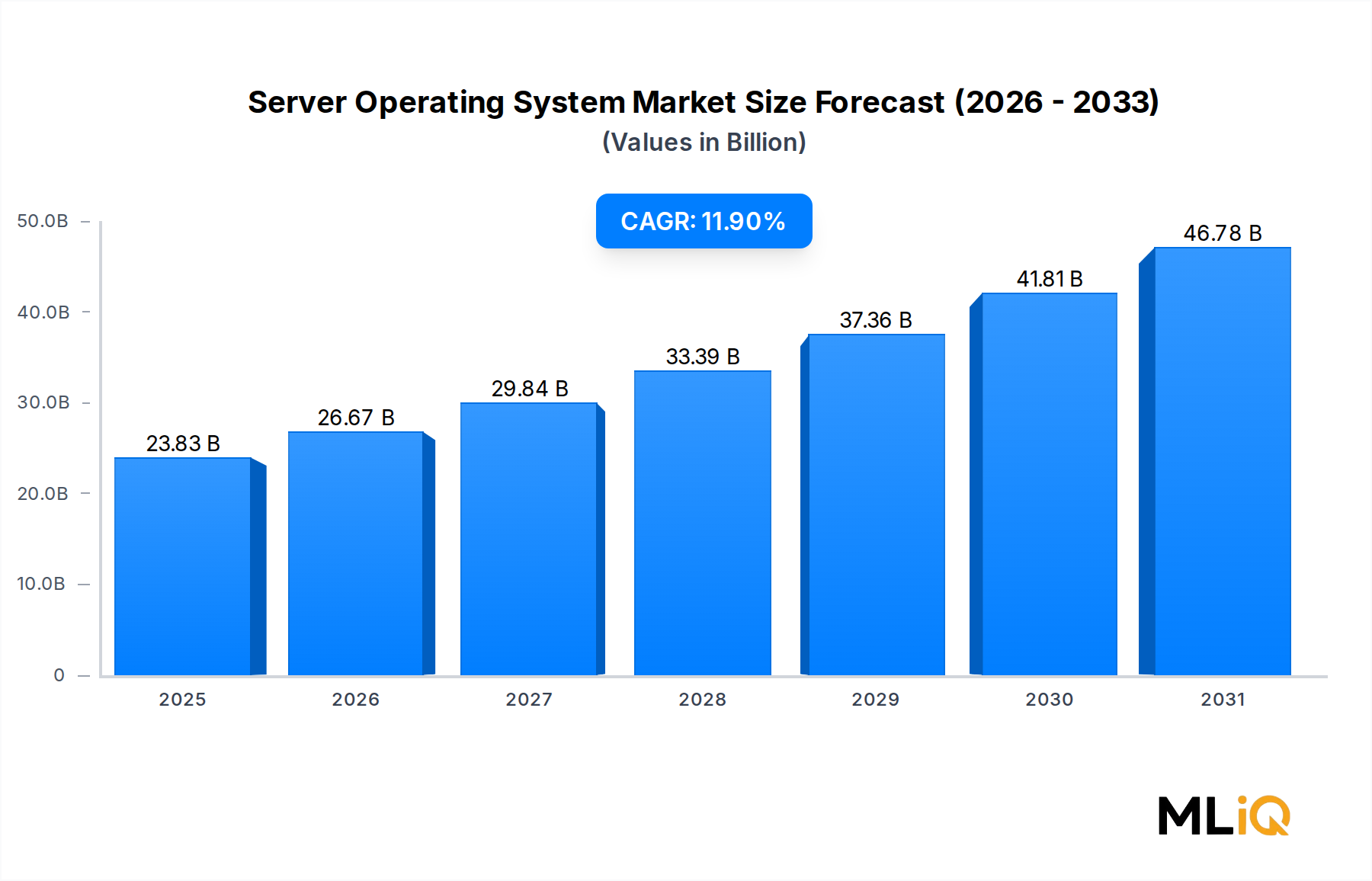

The global Server Operating System Market is valued at $23.83 billion and is projected to expand at a compound annual growth rate (CAGR) of 11.9% over the forecast period, reflecting robust and broad-based demand across industries ranging from banking and financial services to healthcare and e-commerce. This growth trajectory positions the market as one of the most resilient and strategically important segments within enterprise information technology.

The primary catalyst driving this expansion is the accelerating migration of enterprise workloads to hybrid and multi-cloud environments. Organizations across all major verticals are re-architecting their infrastructure to accommodate elastic compute requirements, containerized applications, and edge computing deployments — all of which demand capable, secure, and scalable server operating systems. The increasing proliferation of virtualized server environments has further intensified demand, as hypervisor-compatible operating systems become foundational to modern data center operations.

The BFSI sector remains a principal demand engine, leveraging hardened server operating environments for real-time transaction processing, fraud detection, and regulatory compliance. Similarly, the healthcare industry's rapid digitization — driven by electronic health records, telemedicine platforms, and AI-assisted diagnostics — has created substantial new deployment opportunities for enterprise-grade server operating systems.

From a technology standpoint, the dominance of Linux-based distributions continues to grow, particularly in cloud-native and containerized workload segments. Windows Server maintains a strong foothold in enterprise environments where Active Directory integration, .NET application hosting, and legacy workload compatibility are priorities. UNIX-based systems, while declining in relative share, persist in mission-critical financial and scientific computing contexts.

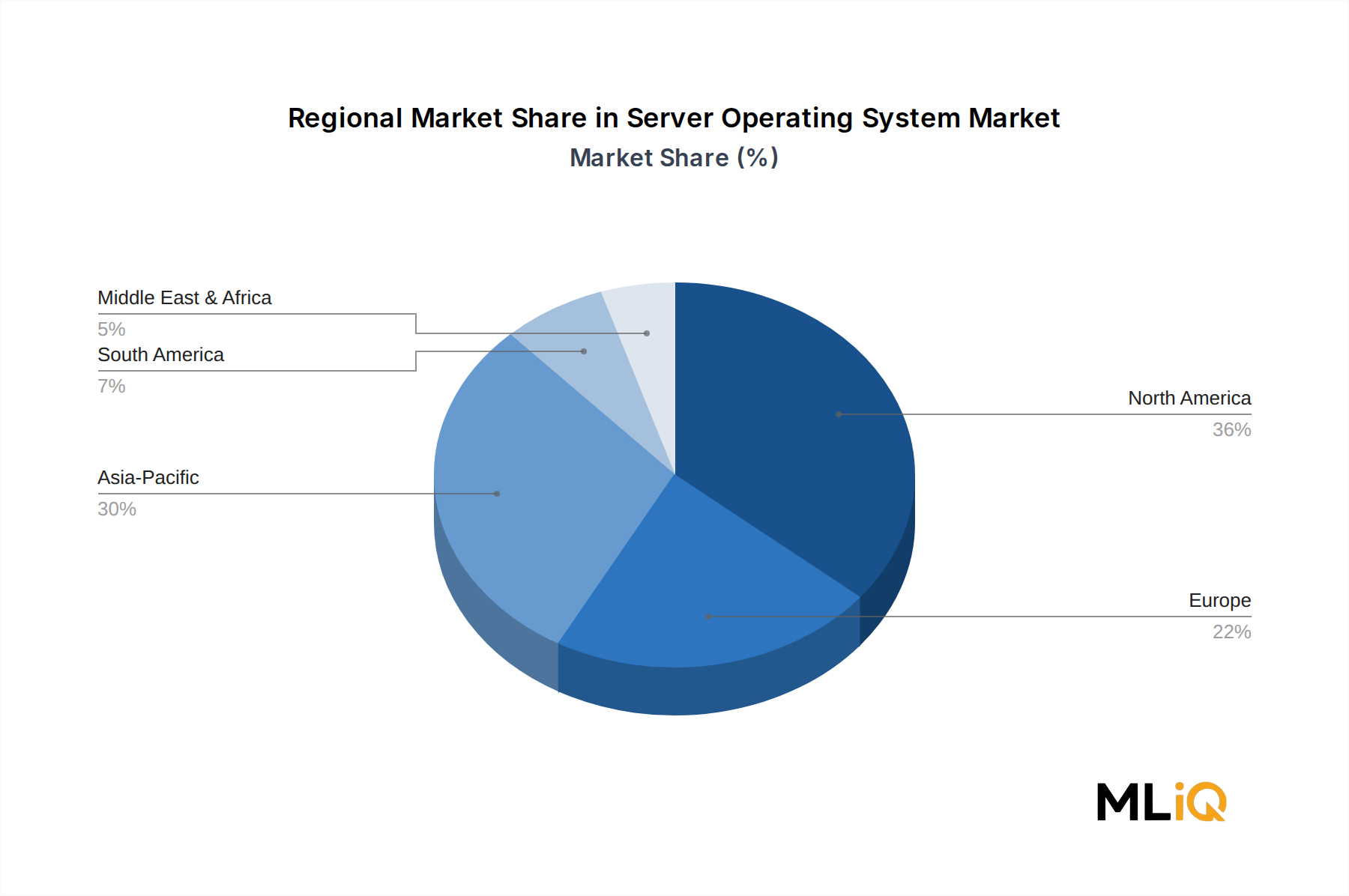

Geographically, North America commands the largest revenue share, buoyed by the presence of hyperscale cloud providers and large enterprise IT spenders. Asia Pacific is the fastest-growing region, driven by rapid digital transformation initiatives in China, India, and Southeast Asia. Europe exhibits steady growth supported by regulatory mandates around data sovereignty and localized cloud infrastructure.

Looking ahead, macro tailwinds including artificial intelligence infrastructure buildout, 5G network densification, and expanding sovereign cloud programs across government entities are expected to sustain elevated demand through the forecast horizon. The competitive landscape is intensifying as open-source ecosystems mature and cloud-native operating platforms redefine traditional licensing models, creating both disruption and opportunity for incumbent and emerging vendors alike.

Among all operating system types — Windows, Linux, UNIX, and others — the Linux segment commands the largest and most rapidly expanding revenue share within the Server Operating System Market. This dominance is structural, not cyclical, and is rooted in a convergence of technical superiority, cost economics, ecosystem maturity, and alignment with cloud-native architectural paradigms.

Linux-based server operating systems have achieved near-ubiquity in hyperscale cloud data centers. Amazon Web Services runs the majority of its EC2 instances on Linux, and Google Cloud Platform's infrastructure is predominantly Linux-based. Microsoft Azure, despite its historical affinity with Windows, now hosts more Linux virtual machines than Windows-based ones — a milestone that underscores the platform's cross-vendor acceptance. This cloud-layer dominance translates directly into server OS licensing, support contract, and subscription revenue.

Several structural factors sustain Linux's leadership. First, the open-source licensing model eliminates per-seat or per-server acquisition costs, dramatically lowering total cost of ownership for enterprises and service providers operating at scale. Second, Linux distributions such as Red Hat Enterprise Linux (RHEL), Ubuntu Server, and SUSE Linux Enterprise Server offer enterprise-grade support, security patching, and certification ecosystems that meet stringent compliance requirements in regulated industries. Third, containerization technologies such as Docker and Kubernetes are natively optimized for Linux environments, making Linux the de facto host OS for modern microservices architectures.

Red Hat, now an IBM subsidiary, remains the market leader in commercially supported Linux server operating systems. Its RHEL platform commands a premium positioning in enterprise accounts, particularly within the BFSI, government, and telecommunications verticals. Canonical Ltd., developer of Ubuntu Server, has aggressively expanded its footprint through cloud-optimized images, snap packaging, and managed Kubernetes offerings. SUSE competes strongly in industrial automation, SAP workloads, and high-performance computing environments, while also benefiting from its independent ownership following the Attachmate divestiture.

The Linux segment's share is not merely growing — it is consolidating. Smaller or proprietary Unix vendors have progressively lost ground as Linux demonstrated its ability to run at scale on commodity x86 hardware and ARM-based processors. The migration of workloads from legacy UNIX platforms (including Solaris and HP-UX) to Linux has been a multi-year structural shift that continues to add incremental revenue to the Linux segment.

In the context of organization size, large enterprises represent the dominant sub-segment within Linux deployments, as they possess the IT staff capacity to manage and customize open-source environments. However, small and medium-sized enterprises are increasingly adopting managed Linux distributions through cloud marketplaces, reducing the operational complexity historically associated with open-source server management.

Deployment mode dynamics further reinforce Linux dominance. Cloud deployments — where Linux is the default substrate for virtual machines, containers, and serverless compute — are growing faster than on-premise installations. This cloud-first orientation ensures that Linux's segment share will continue to expand as enterprise workloads shift from physical server deployments to virtualized and containerized cloud architectures.

Windows Server retains meaningful share in environments with deep Microsoft ecosystem dependencies, including Active Directory, SharePoint, SQL Server, and legacy .NET applications. Microsoft's investment in Windows Server 2022 and its Azure hybrid integration capabilities has helped stabilize Windows Server's competitive positioning, particularly among mid-market and regulated enterprise accounts that prioritize unified identity and compliance management.

Several quantifiable drivers and constraints define the competitive and growth dynamics of the Server Operating System Market, each carrying measurable implications for revenue trajectory and vendor strategy.

Cloud infrastructure spending is the most significant demand driver. Global spending on cloud infrastructure services exceeded $270 billion in 2023, with projections indicating continued double-digit growth annually. Every cloud instance provisioned requires a server operating system layer, making cloud expenditure growth a direct proxy for server OS demand. The expansion of hyperscale data centers by AWS, Microsoft Azure, and Google Cloud creates a sustained and high-volume pull for Linux-based and Windows-based server operating system deployments.

The proliferation of containerized workloads is a second structural driver. Container adoption rates have accelerated sharply, with industry surveys indicating that over 70% of enterprises running containers in production as of 2024. Container orchestration platforms such as Kubernetes are exclusively Linux-dependent, reinforcing the operating system layer's criticality and expanding total addressable market for distributions that offer Kubernetes-certified environments.

Digital transformation investment across the BFSI and healthcare verticals constitutes a third demand vector. Banks and financial institutions are migrating from mainframe and UNIX environments to Linux-based commodity server architectures, driven by cost reduction mandates and agility requirements. Healthcare providers are deploying server infrastructure to support electronic health record systems, real-time analytics, and AI-powered diagnostic tools, each of which demands a robust and certified server operating system.

On the constraint side, cybersecurity complexity represents a significant headwind. The expanding attack surface of server operating systems — particularly in multi-cloud and hybrid deployments — has elevated the cost and complexity of patch management, vulnerability remediation, and compliance attestation. Enterprises managing heterogeneous server OS environments face operational overhead that can delay upgrade cycles and increase total cost of ownership.

Vendor lock-in concerns and open-source fragmentation also moderate growth. Organizations evaluating enterprise Linux distributions must navigate a complex landscape of support contracts, certification requirements, and community versus commercial distribution trade-offs — a complexity that can slow procurement decisions.

The Server Operating System Market is characterized by a concentrated competitive landscape dominated by a handful of global technology giants, alongside specialized open-source vendors and cloud-native platform providers.

Microsoft Corporation: The developer of Windows Server, Microsoft maintains a commanding position in enterprise environments through deep integration with Azure hybrid cloud services, Active Directory, and the broader Microsoft 365 ecosystem. Its subscription-based licensing model has modernized revenue recognition and improved customer retention.

Red Hat, Inc.: A subsidiary of IBM Corporation, Red Hat is the market leader in commercially supported enterprise Linux with its RHEL platform. The company drives significant revenue through multi-year enterprise agreements and its OpenShift container platform, which extends Linux server OS capabilities into Kubernetes orchestration.

IBM Corporation: Beyond its Red Hat subsidiary, IBM contributes to the server OS market through AIX (its proprietary UNIX implementation) and through z/OS on mainframe platforms. IBM's server OS strategy is increasingly centered on hybrid cloud integration and AI-augmented operations.

Canonical Ltd: The publisher of Ubuntu Server, Canonical competes on the strength of its cloud-optimized distribution, extensive public cloud marketplace presence, and growing managed services portfolio including Managed Kubernetes and Managed OpenStack offerings.

SUSE, LLC: An independent open-source software company, SUSE offers SUSE Linux Enterprise Server (SLES) with particular strength in SAP HANA certified environments, high-performance computing clusters, and industrial edge deployments. Its acquisition of Rancher Labs strengthened its Kubernetes management capabilities.

Amazon Web Services: While primarily a cloud infrastructure provider, AWS has developed its own Linux distribution — Amazon Linux 2 and Amazon Linux 2023 — optimized for EC2 workloads, representing a vertically integrated approach to server OS provisioning within its hyperscale environment.

Hewlett Packard Enterprise: HPE bundles server OS capabilities through its GreenLake edge-to-cloud platform and maintains deep integration with Linux and Windows Server distributions on its ProLiant and Superdome server hardware lines.

Dell Technologies Inc.: Dell supports a broad portfolio of server OS certifications across its PowerEdge server line and contributes to enterprise Linux and Windows Server adoption through managed infrastructure and as-a-service consumption models.

Fujitsu Ltd.: Fujitsu provides server OS-integrated infrastructure solutions primarily for the Japanese and broader Asia Pacific markets, with certified Linux and Windows Server environments on its PRIMERGY server platforms.

Apple Inc.: While not a primary enterprise server OS vendor, Apple's macOS Server historically served niche deployment scenarios in creative and education environments, though its server-specific features have been substantially reduced in recent years.

March 2024: Red Hat announced the general availability of Red Hat Enterprise Linux 9.4, introducing enhanced security profiles including SELinux policy refinements and expanded support for confidential computing on AMD SEV-SNP and Intel TDX hardware, targeting regulated enterprise deployments in BFSI and government verticals.

November 2023: Microsoft released Windows Server 2025 preview builds featuring Azure Arc integration enhancements, hotpatch capabilities for reduced reboot requirements, and native support for NVMe storage accelerated by new storage controller drivers — positioning the platform for hybrid data center modernization.

September 2023: SUSE completed the general availability of SUSE Linux Enterprise Server 15 SP5, with extended support for ARM-based processors, expanded SAP HANA certified configurations, and integration with the Rancher Kubernetes management platform for unified edge and cloud deployments.

February 2024: Canonical announced Ubuntu Pro for AWS, Azure, and Google Cloud, offering extended security maintenance and compliance tooling for Ubuntu Server LTS releases — expanding its commercial support addressable market among cloud-native enterprises.

June 2023: Amazon Web Services released Amazon Linux 2023, a new major version of its cloud-optimized Linux distribution featuring deterministic package versioning, minimal footprint for container base images, and a five-year support lifecycle aligned with enterprise procurement cycles.

January 2024: IBM Corporation expanded its AIX on IBM Power10 roadmap, announcing extended support commitments through 2030 and new AI inference optimizations for on-premise mission-critical workloads in financial services and telecommunications.

The Server Operating System Market exhibits meaningful regional variation in growth rates, maturity levels, and demand drivers, reflecting divergent stages of digital infrastructure development and enterprise IT investment patterns across geographies.

North America is the most mature and largest revenue-generating region, accounting for an estimated 38% of global market revenue. The United States is the dominant contributor, underpinned by the world's highest concentration of hyperscale cloud data centers and Fortune 500 enterprise IT spending. Canadian and Mexican markets contribute incrementally, with growth driven by nearshoring of manufacturing technology and government digital infrastructure programs. The North American market is characterized by high Linux and Windows Server co-existence, sophisticated procurement processes, and strong demand for enterprise support contracts from vendors such as Red Hat and Microsoft.

Asia Pacific is the fastest-growing region, projected to register a regional CAGR of approximately 14–15% through the forecast period. China's domestic technology sector, including Alibaba Cloud, Tencent Cloud, and Huawei Cloud, is driving substantial server OS deployment volumes, with a notable shift toward domestically developed Linux distributions such as Kylin OS and Anolis OS in response to geopolitical technology decoupling pressures. India's IT services sector and expanding domestic cloud market are generating strong demand for Ubuntu Server and RHEL deployments. Southeast Asian markets, particularly Singapore, Indonesia, and Vietnam, are experiencing data center construction booms that directly translate into server OS procurement growth.

Europe represents the second-largest regional market, with growth moderated by stringent regulatory compliance requirements — particularly under GDPR and NIS2 — that influence OS selection toward certified, auditable distributions. Germany, France, and the United Kingdom are the primary contributors. The European market shows elevated interest in SUSE and open-source alternatives as part of digital sovereignty initiatives.

Middle East and Africa is an emerging growth region, with GCC countries — particularly Saudi Arabia and the UAE — investing heavily in national cloud infrastructure and smart city programs that generate server OS demand. South Africa anchors the African sub-market. Growth rates in this region are robust from a low base, driven by greenfield data center deployments.

South America exhibits moderate growth, with Brazil as the primary market, driven by financial services digitization and e-government platform development. Adoption of Linux distributions is high due to cost sensitivity among regional enterprises.

The regulatory environment governing the Server Operating System Market is evolving rapidly across multiple dimensions — data sovereignty, cybersecurity mandates, open-source procurement preferences, and export controls — each with direct implications for vendor strategy and enterprise OS selection.

In the European Union, the General Data Protection Regulation (GDPR) continues to exert structural influence on server OS deployment decisions by mandating that personal data processed on server infrastructure meets stringent localization and access control standards. The EU's NIS2 Directive, which expanded the scope of cybersecurity obligations for critical infrastructure operators effective October 2024, requires that server operating systems deployed in essential services sectors — including energy, transportation, healthcare, and banking — maintain documented patch management processes, incident reporting capabilities, and supply chain security assessments.

The EU Cyber Resilience Act, adopted in 2024, establishes mandatory security requirements for connected software products including operating systems, with conformity assessment obligations that will require server OS vendors to demonstrate vulnerability disclosure processes and lifecycle security support — raising compliance costs for smaller distributions.

In the United States, the Cybersecurity and Infrastructure Security Agency (CISA) has issued binding operational directives for federal agencies requiring the use of known-vulnerability-patched server operating systems, effectively mandating enterprise Linux distributions or Windows Server versions with current security patch status across federal IT infrastructure. Executive Order 14028, signed in 2021, initiated a broader federal push toward software supply chain security that continues to shape server OS procurement requirements in government contracting.

China's Cybersecurity Law and Data Security Law have accelerated domestic substitution of foreign server operating systems with domestically certified Linux distributions, reshaping the competitive landscape for international vendors seeking access to Chinese enterprise and government markets.

Government open-source policies in Germany, France, India, and Brazil explicitly encourage or mandate the evaluation of open-source server operating systems for public sector deployments, creating procurement advantages for Linux-based distributions and expanding market opportunity for vendors such as Canonical and SUSE in government verticals.

Although the Server Operating System Market is primarily a software market, its supply chain is intricately linked to hardware component availability, semiconductor manufacturing capacity, and the open-source software dependency ecosystem — each of which introduces distinct sourcing risks and price volatility vectors.

The most significant upstream dependency

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 11.9% from 2020-2034 |

| Segmentation |

|

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Comprehensive validation mechanisms ensuring market intelligence accuracy, reliability, and adherence to international standards.

500+ data sources cross-validated

200+ industry specialists validation

NAICS, SIC, ISIC, TRBC standards

Continuous market tracking updates

Factors such as are projected to boost the Server Operating System Market market expansion.

Key companies in the market include Fujitsu Ltd., Amazon Web Services, Canonical Ltd, Dell Technologies Inc., IBM Corporation, Microsoft Corporation, Hewlett Packard Enterprise, Red Hat, Inc., SUSE, LLC, Apple Inc..

The market segments include Component, Type, Deployment Mode, Organization Size, Virtualization, Industry Vertical.

The market size is estimated to be USD 23.83 billion as of 2022.

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3570, USD 5730, and USD 9600 respectively.

The market size is provided in terms of value, measured in billion and volume, measured in .

Yes, the market keyword associated with the report is "Server Operating System Market," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Server Operating System Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.