1. What are the major growth drivers for the Digital Workplace Market market?

Factors such as are projected to boost the Digital Workplace Market market expansion.

Market Lens IQ is a global market intelligence and strategic consulting firm delivering advanced syndicated research reports, customized industry analysis, competitive intelligence, and data-driven advisory solutions to organizations across international markets. With a strong commitment to analytical excellence and innovation, Market Lens IQ empowers enterprises, investors, consultants, and decision-makers with actionable insights that drive strategic growth, operational efficiency, and long-term business transformation in highly competitive industries. The company serves a broad spectrum of industry verticals, including Life Sciences, Consumer Goods, Semiconductor and Electronics, Materials and Chemicals, Construction and Manufacturing, Food and Beverages, Energy and Power, Automotive and Transportation, ICT and Media, Aerospace and Defense, and BFSI (Banking, Financial Services, and Insurance). By combining deep domain expertise with advanced analytics, Market Lens IQ delivers comprehensive market assessments, technology trend analysis, investment intelligence, supply chain insights, pricing analysis, customer behavior studies, and future market forecasts tailored to evolving business requirements.

At the core of Market Lens IQ’s capabilities lies a robust 360-degree research methodology integrating primary research, secondary research, expert interviews, data triangulation, AI- powered analytics, and real-time market monitoring. Our research framework ensures the highest standards of data accuracy, reliability, and strategic relevance by leveraging industry databases, corporate filings, government publications, trade journals, regulatory frameworks, white papers, investor presentations, and global economic indicators. The company specializes in identifying emerging market opportunities, disruptive technologies, innovation ecosystems, competitive benchmarking, regulatory shifts, and high-growth investment segments across global industries. Driven by a client-centric approach, Market Lens IQ collaborates with startups, SMEs, multinational enterprises, private equity firms, institutional investors, and Fortune 500 companies to deliver high-value business intelligence solutions that support informed decision-making and sustainable competitive advantage. Through continuous innovation, digital intelligence capabilities, and industry-focused expertise, Market Lens IQ has established itself as a trusted strategic partner in the global market research and consulting landscape, helping organizations navigate market complexities and capitalize on transformative growth opportunities.

Digital Workplace Market

Digital Workplace Market+1 2315155523

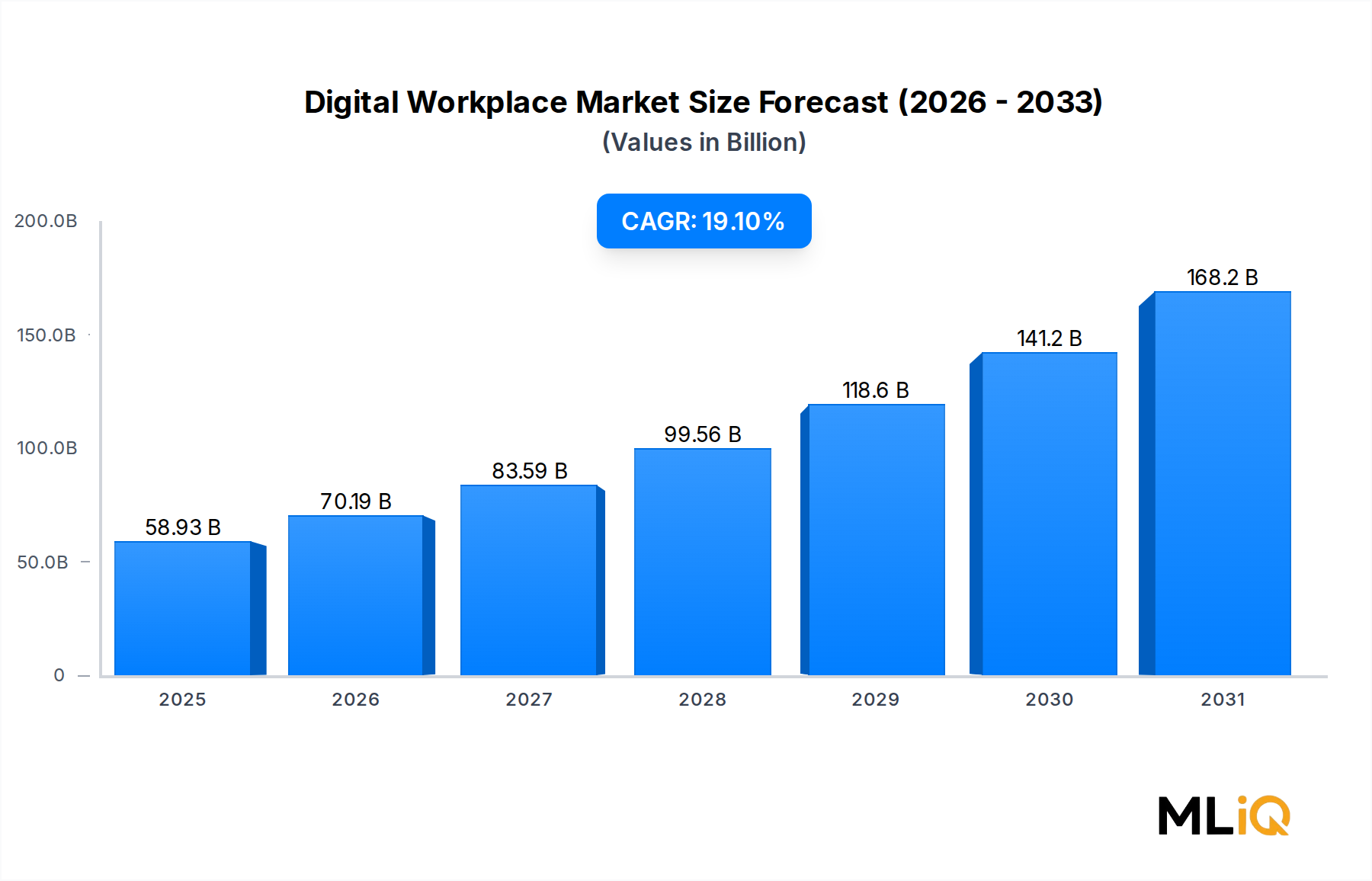

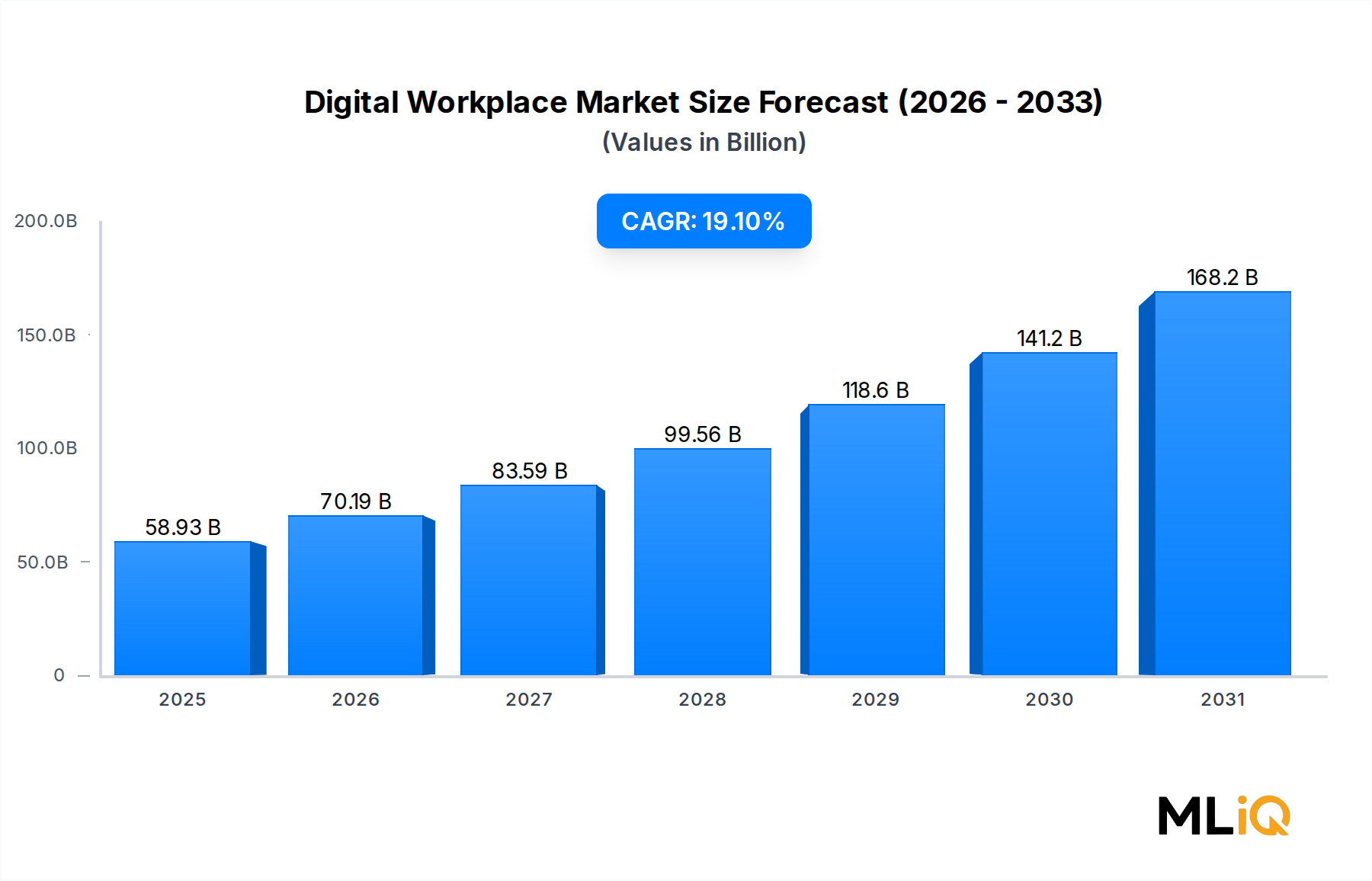

The global Digital Workplace Market is positioned at a pivotal inflection point, with a base valuation of $58.93 billion in 2025 and projected to expand at a compound annual growth rate (CAGR) of 19.1% through 2033. This trajectory implies a market value exceeding $230 billion by the end of the forecast period, driven by the confluence of organizational transformation, workforce mobility imperatives, and accelerating cloud adoption across all major industry verticals.

At its core, the digital workplace paradigm redefines how enterprises orchestrate people, processes, and technology. The shift away from traditional on-premise infrastructure toward integrated, cloud-native ecosystems has generated unprecedented demand for collaborative tools, intelligent automation, and unified endpoint management. The COVID-19 pandemic served as a structural catalyst, compressing a decade of digital transformation into fewer than three years, and the momentum has not subsided. Organizations that initially adopted remote-work solutions as contingency measures have now institutionalized hybrid work models, creating durable, long-term demand.

Macro tailwinds reinforcing this growth include rising enterprise IT spending, government-led digitization initiatives across emerging economies, and growing regulatory mandates around data governance and employee experience. The proliferation of 5G networks is further enabling seamless mobile workplace experiences, reducing latency barriers that previously constrained field-worker productivity. Meanwhile, the integration of generative artificial intelligence into everyday enterprise workflows is reshaping task automation, knowledge management, and decision support—functionalities now considered table-stakes rather than differentiators.

From a segmentation perspective, cloud-based deployment is capturing a disproportionate share of new revenue, while large enterprises continue to represent the dominant organizational cohort by spend. However, SMEs are closing the gap rapidly as platform vendors increasingly offer scalable, consumption-based pricing models. Vertically, BFSI, healthcare, and telecommunications remain the highest-spending sectors, though manufacturing and government are emerging as high-velocity growth verticals.

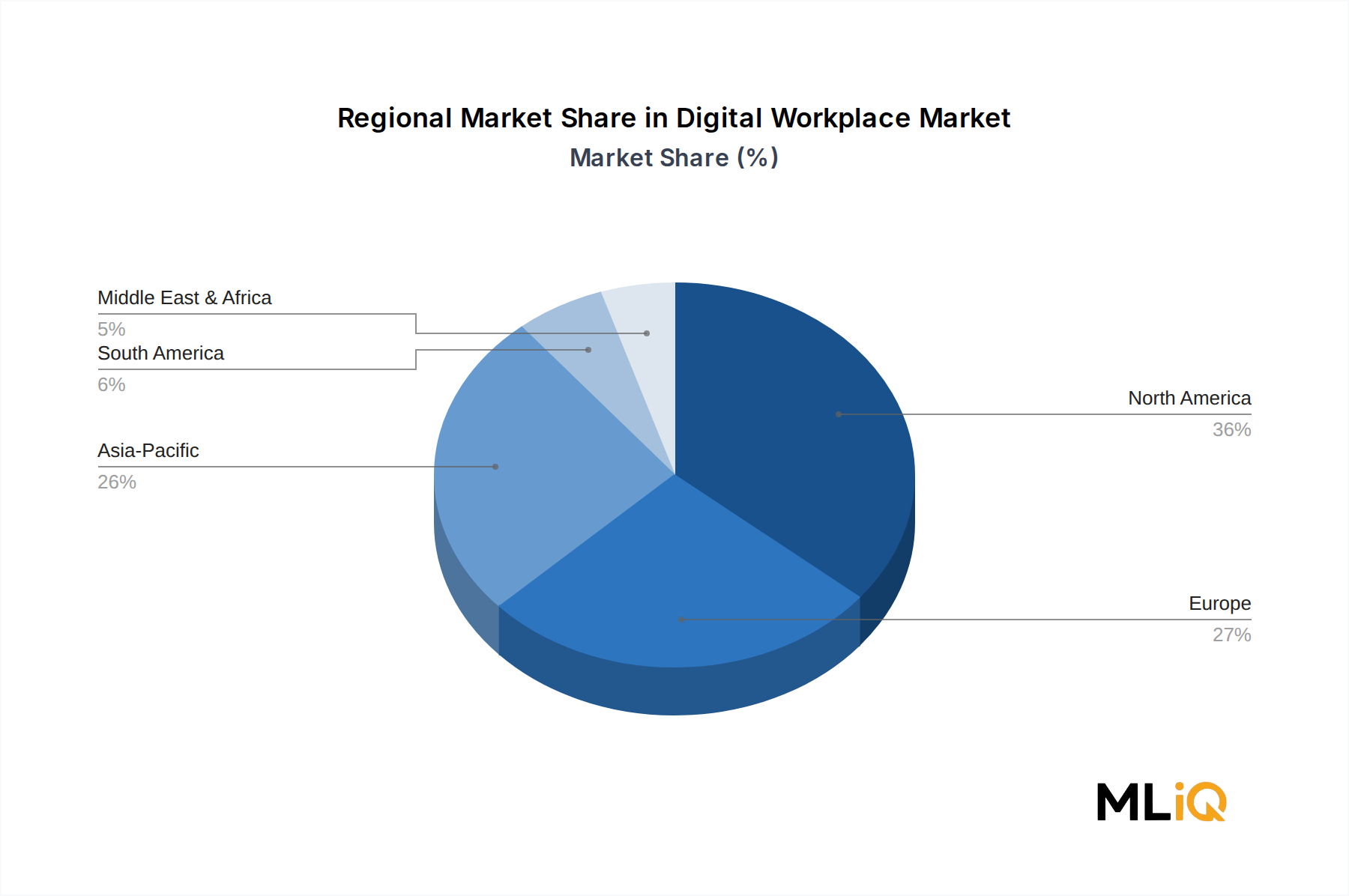

Geographically, North America retains its leadership position, but Asia Pacific is the fastest-growing region, underpinned by aggressive digitization programs in China, India, and Southeast Asia. Europe presents a stable, compliance-driven growth environment, while the Middle East and Africa are gaining traction through sovereign digital infrastructure investments.

Forward-looking, the market's competitive intensity is escalating. Established technology hyperscalers are extending their platform footprints through acquisitions and ecosystem partnerships, while specialized vendors are carving out defensible niches in employee experience, AI-augmented workflows, and zero-trust security architectures. The next three years will be defined by platform consolidation, verticalized solution stacks, and the maturation of AI-native workplace tools.

Among all segmentation dimensions analyzed within the Digital Workplace Market, the deployment-type segment—specifically cloud-based solutions—represents the single largest and fastest-consolidating revenue pool. As of 2025, cloud deployment accounts for the majority of new contract value, a structural shift that reflects fundamental changes in enterprise IT procurement philosophy, vendor go-to-market strategies, and the operational realities of distributed workforce management.

The primacy of cloud deployment is rooted in several interconnected dynamics. First, the total cost of ownership (TCO) calculus has decisively shifted in favor of cloud. On-premise infrastructure requires substantial upfront capital expenditure, ongoing hardware refresh cycles, dedicated IT staffing for maintenance, and complex disaster recovery planning. Cloud-native digital workplace platforms, by contrast, convert these fixed costs into predictable operating expenditures, align cost with actual utilization, and offload infrastructure management to the vendor. For CFOs navigating uncertain macroeconomic conditions, this financial flexibility is strategically compelling.

Second, the scalability and geographic agility offered by cloud architectures are uniquely suited to the hybrid workforce era. Enterprises operating across multiple time zones and geographies require workplace platforms that can provision new users, roll out feature updates, and enforce security policies uniformly—capabilities that on-premise systems struggle to deliver at scale and speed. Hyperscale cloud providers such as Microsoft Corporation have embedded their digital workplace suites directly into their cloud infrastructure, creating tight integration between productivity applications, identity management, and device compliance.

Third, the software-as-a-service (SaaS) delivery model has democratized access to enterprise-grade workplace tools, enabling SMEs to deploy capabilities previously reserved for large enterprises. This has materially expanded the total addressable market and compressed vendor sales cycles, as cloud solutions can be trialed, configured, and operationalized in days rather than months.

Within the cloud deployment segment, platform vendors are intensifying competition across three layers: the infrastructure layer (dominated by hyperscalers), the platform layer (where unified communication and collaboration suites compete), and the application layer (where specialized vendors offer point solutions in HR, analytics, and workflow automation). Microsoft Corporation maintains an outsized position across all three layers through its Microsoft 365 and Azure ecosystem, making it the de facto incumbent in enterprise digital workplace deployments globally.

HPE, CAPGEMINI, and NTT DATA are positioning themselves as cloud migration and managed services partners, enabling enterprises to transition legacy on-premise workloads to cloud-native digital workplace architectures. FUJITSU and UNISYS offer hybrid cloud models that bridge on-premise and cloud environments, catering to regulated industries where data residency requirements constrain pure-cloud adoption.

The cloud segment's share is not merely growing—it is consolidating. Vendors that cannot offer credible cloud-native roadmaps are losing renewal cycles to cloud-first competitors. This consolidation dynamic is expected to intensify through 2028, as multi-year enterprise agreements signed during the 2020–2022 pandemic acceleration period come up for renewal, creating a significant market displacement opportunity. Analysts tracking enterprise software procurement trends consistently identify digital workplace cloud platforms as among the highest-priority renewal and expansion categories within IT budgets.

On-premise deployment retains relevance in highly regulated verticals such as defense, central banking, and critical national infrastructure, but even within these segments, sovereign cloud and private cloud variants are eroding traditional on-premise strongholds. The trajectory is unmistakable: cloud deployment will account for an increasingly dominant proportion of Digital Workplace Market revenue through 2033.

Understanding the forces shaping the Digital Workplace Market requires a data-centric examination of both growth accelerants and structural limitations. Each factor carries quantifiable implications for market velocity and competitive dynamics.

Hybrid work institutionalization is the primary demand driver. According to enterprise workforce surveys, more than 70% of knowledge workers globally now operate under hybrid arrangements as of 2025, creating sustained demand for tools that unify communication, document collaboration, and project management across physical and virtual environments. This is not a cyclical trend but a structural reset of workplace operating models.

AI-augmented productivity tools represent a secondary but rapidly intensifying driver. Enterprises integrating generative AI copilots into their digital workplace stacks report productivity gains of 20–35% in knowledge-intensive workflows, according to enterprise pilot program data. The commercial release of AI assistants embedded in leading workplace platforms has accelerated adoption timelines, compressing what was projected as a 2027–2028 mainstream adoption window to 2025–2026.

Cybersecurity requirements are functioning simultaneously as a driver and a constraint. As a driver, zero-trust architecture mandates and endpoint security requirements are increasing per-seat digital workplace platform spending by an estimated 15–22%. As a constraint, security audit cycles, procurement compliance reviews, and data residency regulations are extending enterprise sales cycles, particularly in Europe under GDPR enforcement and in Asia Pacific under emerging national data protection frameworks.

Talent competition is an underappreciated demand driver. Enterprises deploying best-in-class digital workplace experiences report measurable improvements in employee retention metrics, reducing annual attrition costs that can represent 50–200% of annual salary per departing employee. This positions digital workplace investment as a talent strategy, not merely an IT procurement decision.

Cost rationalization pressures represent the most significant market constraint. Following aggressive SaaS expansion during 2020–2022, many enterprises entered 2024–2025 with bloated software portfolios and redundant platform subscriptions. SaaS portfolio optimization initiatives have caused some enterprises to consolidate vendors and reduce seat counts, creating short-term headwinds for point-solution providers while benefiting integrated platform vendors.

The competitive landscape of the Digital Workplace Market is characterized by a layered ecosystem of global technology titans, specialized managed service providers, and regional integrators. The following profiles capture the strategic positioning of leading participants:

NTT DATA: A global IT services leader with deep expertise in digital workplace transformation, NTT DATA delivers end-to-end managed workplace services spanning unified communications, device lifecycle management, and AI-powered service desk capabilities across enterprise and public-sector clients in over 50 countries.

STEFANINI: A Brazil-headquartered technology services firm with a strong presence in Latin America and growing operations in North America and Europe, STEFANINI differentiates through its proprietary Sophie AI platform, which automates IT service management and workplace support functions for multinational corporations.

Microsoft Corporation: The dominant platform vendor in the global digital workplace ecosystem, Microsoft Corporation leverages its Microsoft 365, Teams, and Azure Active Directory portfolio to deliver integrated productivity, communication, security, and compliance capabilities to over 300 million monthly active users worldwide.

CAPGEMINI: A French multinational technology and consulting firm, CAPGEMINI provides digital workplace advisory, design, and implementation services with particular strength in European enterprise accounts, combining human-centered design methodologies with cloud-native architecture expertise.

COMPUCOM: A North American managed workplace services provider, COMPUCOM specializes in device-as-a-service, IT field support, and hybrid workplace infrastructure management for large distributed enterprises in retail, healthcare, and financial services.

HPE: Hewlett Packard Enterprise positions its digital workplace offerings around intelligent edge infrastructure, secure remote access, and hybrid cloud connectivity, targeting enterprises with complex multi-site and distributed workforce requirements through its GreenLake platform.

FUJITSU: A Japanese technology conglomerate with extensive public-sector and enterprise relationships across Asia Pacific and Europe, FUJITSU delivers digital workplace services encompassing managed end-user computing, AI-driven IT operations, and sustainable workspace design.

UNISYS: Specializing in secure digital workplace solutions for regulated industries, UNISYS brings particular depth in government, defense, and financial services, offering zero-trust security frameworks integrated with its managed workplace service portfolio.

TCS: Tata Consultancy Services deploys its Cognitive Workplace platform to support large-scale enterprise transformations globally, combining AI-based automation with human capital analytics to optimize employee experience and IT service efficiency.

ILEGRA: A Brazilian technology services firm focused on innovation consulting and digital workplace enablement for mid-market enterprises, ILEGRA leverages design thinking and agile methodologies to accelerate workplace modernization programs.

SONDA: A leading Latin American IT services provider, SONDA delivers digital workplace managed services across Chile, Brazil, and Colombia, with growing capabilities in cloud migration, unified communications, and endpoint security.

SANTO DIGITAL: A specialist digital transformation firm operating primarily in South American markets, SANTO DIGITAL offers workplace digitization consulting and implementation services tailored to organizations undergoing foundational IT modernization.

January 2025: Microsoft Corporation announced the general availability of Microsoft 365 Copilot for frontline workers, extending AI-assisted productivity tools beyond knowledge workers to manufacturing floor, retail, and healthcare field personnel for the first time at scale.

February 2025: NTT DATA launched its next-generation Managed Digital Workplace platform, incorporating generative AI-powered service desk automation and predictive device health monitoring, targeting enterprise clients with more than 10,000 endpoints.

March 2025: CAPGEMINI entered a strategic alliance with a leading hyperscale cloud provider to jointly deliver AI-augmented digital workplace transformation services to European enterprises, with an initial focus on BFSI and manufacturing verticals under EU AI Act compliance frameworks.

April 2025: TCS expanded its Cognitive Workplace offering with a new employee experience analytics module, enabling HR and IT leaders to correlate digital tool usage patterns with workforce productivity and retention outcomes.

May 2025: HPE announced an expansion of its GreenLake edge-to-cloud workplace connectivity solutions, introducing new zero-trust network access capabilities designed to support enterprises managing hybrid workforces across more than 20 countries simultaneously.

June 2025: UNISYS secured a multi-year government contract to modernize digital workplace infrastructure for a major national public administration, deploying secure end-user computing and AI-enhanced IT service management across more than 50,000 government employees.

August 2025: STEFANINI unveiled the third generation of its Sophie AI platform, featuring enhanced natural language processing capabilities for IT support automation, reducing mean-time-to-resolution for common workplace incidents by 40% in pilot deployments.

The Digital Workplace Market exhibits pronounced regional variation in maturity, growth velocity, and dominant demand drivers, reflecting differences in enterprise digitization readiness, regulatory environments, and workforce composition.

North America is the most mature and highest-revenue region, accounting for an estimated 38–42% of global Digital Workplace Market revenue in 2025. The United States drives the overwhelming majority of regional spend, underpinned by high enterprise IT budgets, deep cloud infrastructure penetration, and a workforce culture that embraced hybrid work models earlier and more comprehensively than any other region. Canada contributes meaningfully through its financial services and government sectors. Regional CAGR is estimated at approximately 15–16%, reflecting a market that is scaling from an already-elevated base rather than undergoing foundational adoption.

Asia Pacific is the fastest-growing region, with a projected CAGR of 23–25% through 2033. China, India, Japan, and South Korea collectively represent the region's revenue core, while ASEAN economies are emerging as high-velocity growth markets. India's IT services sector is both a major consumer and a global delivery engine for digital workplace solutions. Government-led Digital India, Smart Nation Singapore, and Thailand 4.0 initiatives are amplifying public-sector demand. The sheer scale of workforce digitization in manufacturing and business process outsourcing sectors across Asia Pacific creates a demand profile unlike any other region.

Europe represents a stable, compliance-driven growth environment, with a regional CAGR of approximately 16–18%. Germany, the United Kingdom, and France are the primary revenue contributors. GDPR compliance requirements have elevated data governance and privacy-preserving workplace tool adoption, creating a market dynamic where security and compliance features are as commercially important as productivity functionality. The EU AI Act is expected to further shape procurement criteria for AI-augmented workplace tools in the 2026–2028 period.

Middle East and Africa is an emerging growth region, with a CAGR of approximately 20–22%, driven by Gulf Cooperation Council (GCC) sovereign digital transformation programs, including Saudi Arabia's Vision 2030 and UAE's National Innovation Strategy. South Africa represents the continent's most mature digital workplace market. North Africa is at an earlier adoption stage but is accelerating through telecom infrastructure upgrades.

South America is a developing market with a CAGR of approximately 17–19%, anchored by Brazil and Argentina. STEFANINI, SONDA, and SANTO DIGITAL are particularly active in this region, offering locally contextualized digital workplace services to enterprises navigating currency volatility and uneven infrastructure quality.

Three emerging technology vectors are materially reshaping the innovation landscape of the Digital Workplace Market, each carrying distinct implications for adoption timelines, incumbent business models, and competitive positioning.

Generative AI and AI copilots represent the most immediately disruptive technology force. Embedded AI assistants capable of drafting communications, summarizing meetings, generating code, and routing IT service requests are transitioning from pilot projects to standard platform features at unprecedented speed. Enterprise R&D investment in this category is substantial: leading platform vendors collectively allocated an estimated $15–20 billion toward AI workplace integration initiatives in 2024 alone. The adoption timeline has compressed sharply—what vendors projected as a 2027 mainstream capability is now a 2025–2026 commercial reality. The business model implication is significant: AI copilots are commanding premium per-seat pricing tiers, expanding average revenue per user (ARPU) for incumbent platform vendors while simultaneously raising the barrier to entry for smaller competitors who lack the data scale to train comparable models.

Zero-trust security architecture is the second disruptive

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 19.1% from 2020-2034 |

| Segmentation |

|

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Comprehensive validation mechanisms ensuring market intelligence accuracy, reliability, and adherence to international standards.

500+ data sources cross-validated

200+ industry specialists validation

NAICS, SIC, ISIC, TRBC standards

Continuous market tracking updates

Factors such as are projected to boost the Digital Workplace Market market expansion.

Key companies in the market include NTT DATA, STEFANINI, Microsoft Corporation, CAPGEMINI, COMPUCOM, HPE, FUJITSU, UNISYS, TCS, ILEGRA, SONDA, SANTO DIGITAL.

The market segments include Component, Deployment type, Organization Size, Industry Verticals.

The market size is estimated to be USD 58.93 billion as of 2022.

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3690, USD 5820, and USD 9870 respectively.

The market size is provided in terms of value, measured in billion and volume, measured in .

Yes, the market keyword associated with the report is "Digital Workplace Market," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Digital Workplace Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.