1. What are the major growth drivers for the Airport Biometric Service Market market?

Factors such as are projected to boost the Airport Biometric Service Market market expansion.

Market Lens IQ is a global market intelligence and strategic consulting firm delivering advanced syndicated research reports, customized industry analysis, competitive intelligence, and data-driven advisory solutions to organizations across international markets. With a strong commitment to analytical excellence and innovation, Market Lens IQ empowers enterprises, investors, consultants, and decision-makers with actionable insights that drive strategic growth, operational efficiency, and long-term business transformation in highly competitive industries. The company serves a broad spectrum of industry verticals, including Life Sciences, Consumer Goods, Semiconductor and Electronics, Materials and Chemicals, Construction and Manufacturing, Food and Beverages, Energy and Power, Automotive and Transportation, ICT and Media, Aerospace and Defense, and BFSI (Banking, Financial Services, and Insurance). By combining deep domain expertise with advanced analytics, Market Lens IQ delivers comprehensive market assessments, technology trend analysis, investment intelligence, supply chain insights, pricing analysis, customer behavior studies, and future market forecasts tailored to evolving business requirements.

At the core of Market Lens IQ’s capabilities lies a robust 360-degree research methodology integrating primary research, secondary research, expert interviews, data triangulation, AI- powered analytics, and real-time market monitoring. Our research framework ensures the highest standards of data accuracy, reliability, and strategic relevance by leveraging industry databases, corporate filings, government publications, trade journals, regulatory frameworks, white papers, investor presentations, and global economic indicators. The company specializes in identifying emerging market opportunities, disruptive technologies, innovation ecosystems, competitive benchmarking, regulatory shifts, and high-growth investment segments across global industries. Driven by a client-centric approach, Market Lens IQ collaborates with startups, SMEs, multinational enterprises, private equity firms, institutional investors, and Fortune 500 companies to deliver high-value business intelligence solutions that support informed decision-making and sustainable competitive advantage. Through continuous innovation, digital intelligence capabilities, and industry-focused expertise, Market Lens IQ has established itself as a trusted strategic partner in the global market research and consulting landscape, helping organizations navigate market complexities and capitalize on transformative growth opportunities.

Airport Biometric Service Market

Airport Biometric Service Market+1 2315155523

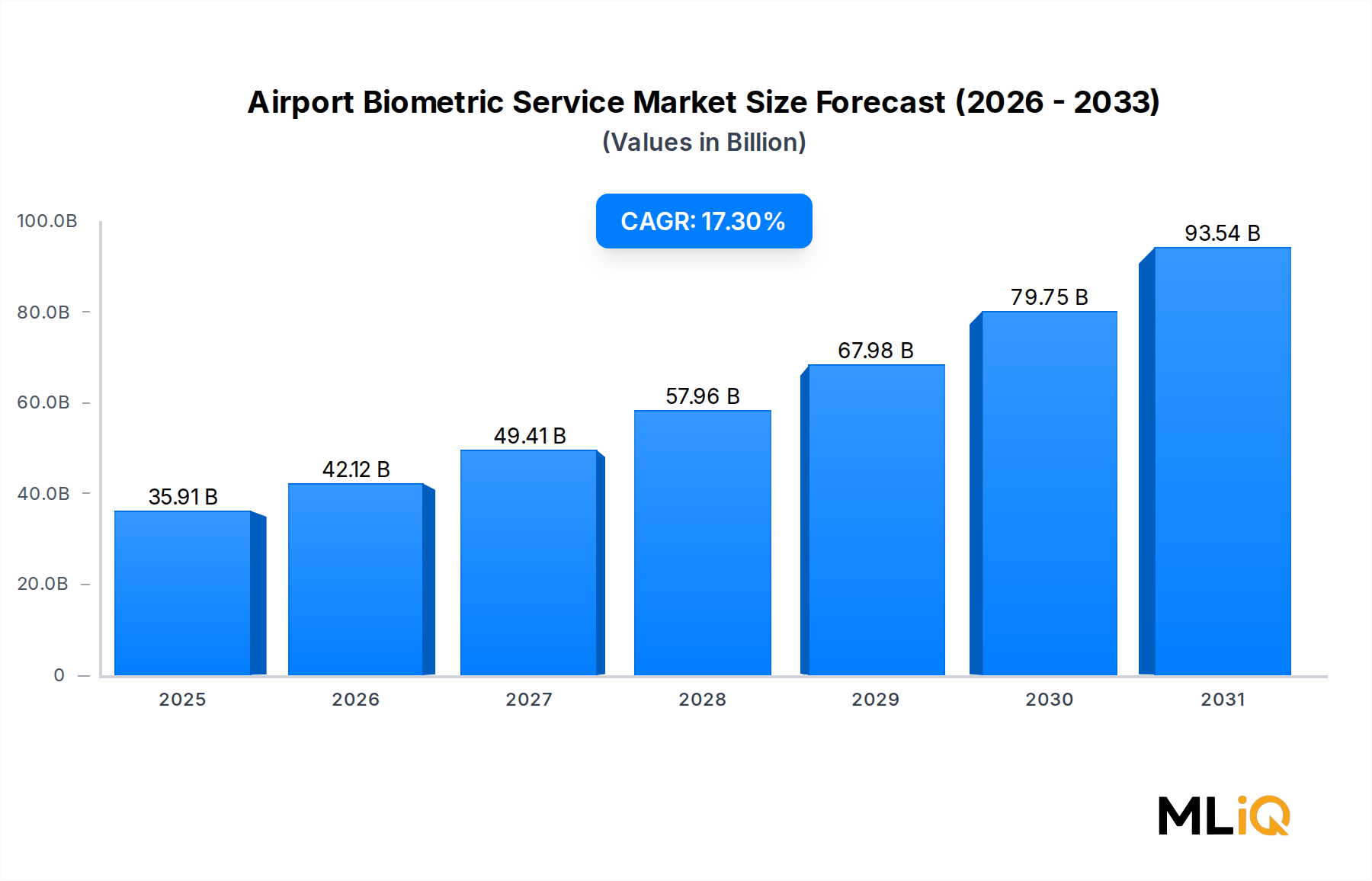

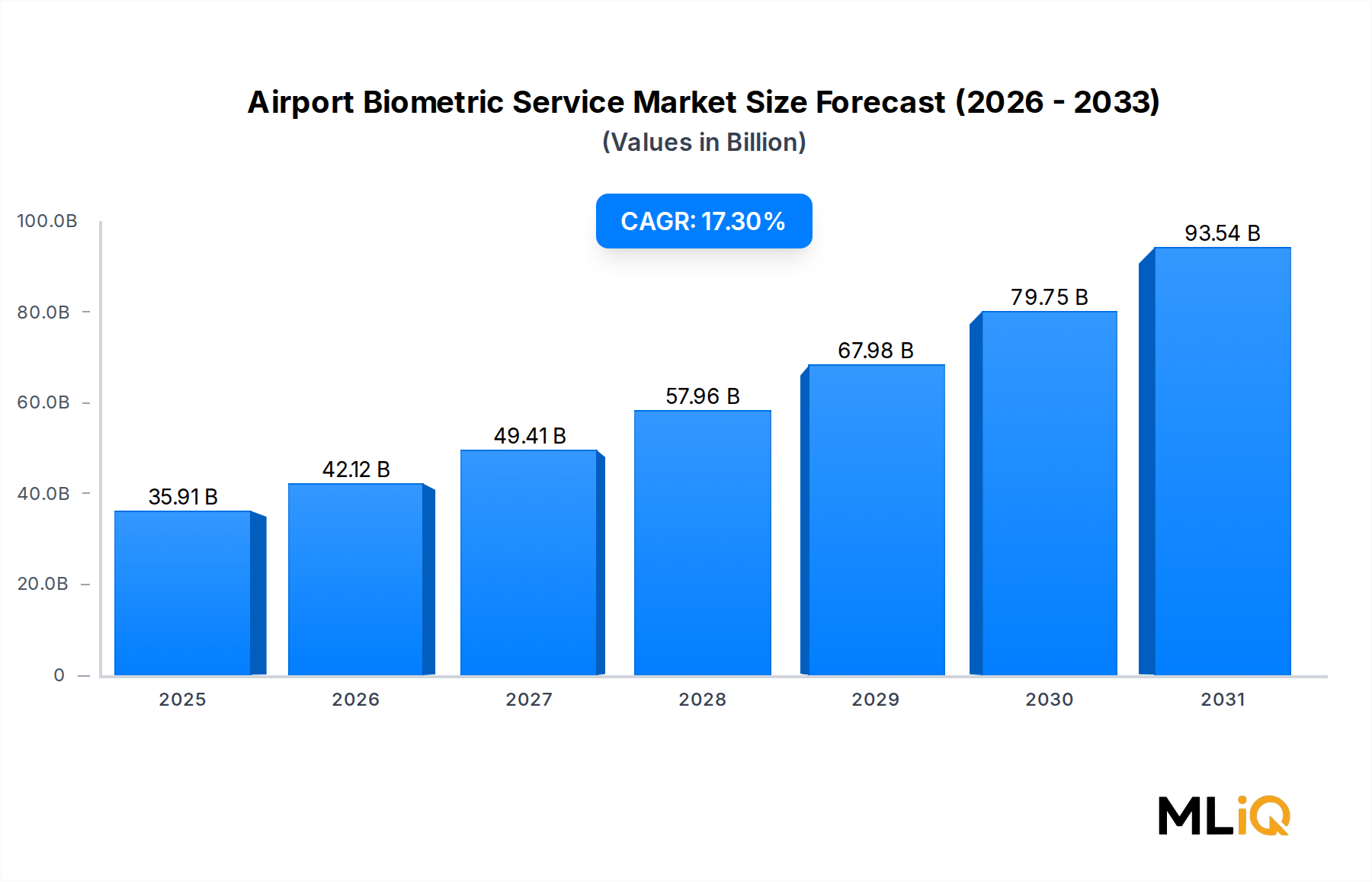

The global Airport Biometric Service Market is experiencing an era of accelerated transformation, driven by the convergence of security imperatives, passenger experience mandates, and digital infrastructure modernization across the aviation sector. The market was valued at $35.91 billion and is projected to expand at a compound annual growth rate (CAGR) of 17.3% through the forecast period, reflecting one of the strongest growth trajectories within the broader ICT and Media category.

The primary demand engine stems from the escalating global passenger volumes, which according to the International Air Transport Association (IATA), are expected to surpass pre-pandemic records within the near term, placing unprecedented pressure on airports to streamline throughput without compromising security protocols. Biometric identity solutions — spanning facial recognition, fingerprint scanning, iris authentication, and palm vein mapping — are being rapidly deployed at check-in kiosks, boarding gates, immigration desks, and secure access zones to reduce dwell times and eliminate manual document verification bottlenecks.

Macro tailwinds reinforcing this market include regulatory frameworks mandating biometric data collection at international borders across the United States, European Union, and Gulf Cooperation Council (GCC) nations, alongside significant public infrastructure investment programs allocating dedicated capital to airport modernization. The U.S. Transportation Security Administration (TSA) and the European Union Aviation Safety Agency (EASA) have both issued directives encouraging the adoption of automated biometric screening, amplifying demand across government-contracted procurement channels.

Technologically, the market is benefitting from continued improvements in deep-learning-based recognition accuracy, edge computing deployments that reduce latency in real-time authentication, and cloud-native platform architectures that allow scalable deployment across multi-terminal and multi-airport environments. The shift from single-modal to multi-modal biometric systems — combining two or more biometric identifiers for higher accuracy and fraud resistance — is a pivotal trend reshaping product development roadmaps across leading vendors.

From a segmentation perspective, facial recognition commands the largest revenue share due to its contactless nature and compatibility with existing surveillance infrastructure, while cloud-based deployment models are gaining traction over on-premises systems, particularly among mid-sized airports seeking lower capital expenditure.

Looking forward, the Airport Biometric Service Market is positioned for sustained double-digit growth, with Asia Pacific emerging as the fastest-growing regional market and North America retaining the highest absolute revenue contribution. Strategic mergers, government partnerships, and interoperability standardization efforts will be the defining competitive dynamics over the next five years.

Among all scanner types within the Airport Biometric Service Market, facial recognition stands as the unequivocal revenue leader, capturing the largest share of total market value. This dominance is not incidental — it reflects a confluence of technological maturity, regulatory alignment, infrastructure compatibility, and passenger acceptance that collectively distinguish facial recognition from competing biometric modalities.

Facial recognition systems operate by capturing a two-dimensional or three-dimensional image of a passenger's face and comparing it against a stored template derived from a passport chip, enrollment database, or government identity registry. Unlike fingerprint or iris recognition, which require deliberate physical interaction with a scanner, facial recognition can function passively and at-a-distance, enabling seamless processing in high-throughput environments such as boarding gates and immigration halls without interrupting passenger flow. This contactless capability became especially valuable following health-safety sensitivities highlighted during the COVID-19 pandemic, accelerating adoption timelines at airports globally.

From a regulatory standpoint, several governments have explicitly mandated or incentivized facial recognition deployment. The United States Customs and Border Protection (CBP) Biometric Exit program, for example, requires biometric face comparison for all international departures at major U.S. airports. Similar mandates exist across the European Union's Entry/Exit System (EES), which relies heavily on facial capture as a primary verification tool. In the GCC, airports in the United Arab Emirates — including Dubai International and Abu Dhabi International — have implemented end-to-end facial recognition passenger journeys as flagship infrastructure investments.

The Facial Recognition Market more broadly is benefiting from rapid advances in convolutional neural network architectures, liveness detection algorithms that defeat spoofing attempts using photographs or masks, and 3D structured light sensors that improve accuracy in variable lighting and crowd-density conditions. These technological improvements are directly feeding back into airport deployments, elevating matching accuracy rates to above 99.5% in controlled airport environments according to published benchmark studies.

Key players driving facial recognition revenue within the airport context include NEC Corporation, which has deployed its NeoFace platform across multiple international airports in the Asia Pacific and Americas regions; Thales Group, which integrates facial recognition into its end-to-end passenger processing suites; and Safran, whose Morpho division offers facial biometric systems deeply embedded in government border control programs.

The share of facial recognition within the Airport Biometric Service Market is not merely holding steady — it is actively consolidating as airports that previously piloted standalone fingerprint or iris systems increasingly migrate toward facial recognition as their primary modality, often retaining other biometric types as secondary or fallback verification layers. This consolidation is reinforced by falling hardware costs for high-resolution camera arrays and the growing availability of AI-inference chips that enable real-time processing without reliance on centralized cloud compute.

Beyond primary identification, facial recognition is increasingly being extended into retail personalization, lounge access management, and priority lane routing within airports, expanding its monetization surface well beyond traditional security applications. This functional broadening further entrenches facial recognition as the dominant segment and signals that its share will continue to grow through the forecast period.

The Airport Biometric Service Market is propelled by a well-defined set of structural drivers, each quantifiable and directly linked to observable market behavior.

The most powerful demand driver is passenger volume growth. IATA forecasts that global air travel will reach 4.7 billion passengers annually by 2026, a figure that creates acute throughput pressure on airport infrastructure and makes automated biometric processing economically essential rather than optional. Each percentage point increase in passenger volume directly increases the cost of manual identity verification, creating a compelling ROI case for biometric automation.

Government mandates constitute the second major driver. The U.S. CBP Biometric Exit program alone covers 27 of the largest U.S. international airports, and the EU's EES mandate — now delayed but legislatively firm — will require biometric capture for over 700 million non-EU traveler crossings annually once operational. These mandates create captive procurement pipelines for solution vendors.

Airport modernization capital expenditure is a third quantifiable driver. Global airport infrastructure investment is expected to exceed $190 billion between 2023 and 2030, with biometric technology constituting a growing share of IT budget allocations within major terminal development projects.

On the constraint side, data privacy regulations present the most substantive barrier. The EU's General Data Protection Regulation (GDPR) classifies biometric data as a special category requiring explicit consent, creating legal complexity for always-on biometric capture systems. Non-compliance fines of up to 4% of annual global turnover create meaningful compliance risk for technology vendors and airport operators alike.

Interoperability fragmentation is a secondary constraint. Different biometric systems from different vendors frequently lack the data format standardization necessary for seamless cross-border identity sharing, limiting the potential of international interoperability programs and requiring costly integration middleware.

Cybersecurity risk, while not unique to this market, is particularly acute given the sensitivity of biometric data. A single database breach involving facial or fingerprint templates cannot be remediated by issuing new credentials — the affected individuals' biometric identities are permanently compromised, creating elevated reputational and legal exposure for operators.

The competitive landscape of the Airport Biometric Service Market features a mix of large defense and technology conglomerates, specialized biometric solution providers, and aviation IT platform vendors. The following profiles characterize the strategic positioning of key market participants:

3M Cogent Inc.: A pioneer in automated fingerprint identification systems (AFIS) and multimodal biometric platforms, 3M Cogent has built a strong presence in government and border control biometric deployments, supplying large-scale fingerprint recognition infrastructure to immigration agencies globally.

ADB Safegate: Specializing in airfield and airport operations technology, ADB Safegate integrates biometric identity solutions into its broader gate management and boarding systems, offering airports a unified operational technology stack that bridges airside and terminal environments.

Inform Software: Focused on airport resource management and operations optimization, Inform Software incorporates biometric data flows into its decision-support systems, enabling real-time passenger tracking and gate assignment optimization based on biometrically verified throughput data.

Inner Range: A provider of integrated access control and security management systems, Inner Range delivers biometric access solutions for secure airport zones including control towers, baggage handling facilities, and maintenance areas, where employee identity verification is operationally critical.

Safran: Through its Morpho (now IDEMIA) heritage and its current Identity and Security division, Safran is a tier-one supplier of biometric enrollment and verification systems to government border control programs across Europe, the Americas, and Asia Pacific.

Amadeus IT Group SA: A dominant force in global airline IT infrastructure, Amadeus IT Group SA is integrating biometric passenger identity tokens into its passenger service systems (PSS) and departure control systems (DCS), enabling airlines to use biometric identifiers as boarding passes across its installed base of airline customers.

Vanderbilt Industries: Providing enterprise security systems with biometric access control capabilities, Vanderbilt Industries serves airports seeking scalable identity management for both landside and airside personnel access, with particular strength in European airport deployments.

NEC Corporation: One of the global leaders in facial recognition technology, NEC Corporation deploys its NeoFace biometric platform across airports in Japan, the United States, Australia, and Singapore, recognized for its consistently high accuracy ratings in independent benchmark evaluations.

IndraSistemas S.A.: A Spanish technology conglomerate with deep roots in air traffic management and airport IT, IndraSistemas S.A. offers biometric-enabled passenger processing systems and has secured significant contracts across Spanish and Latin American airport authorities.

Thales Group: A global defense and digital security leader, Thales Group provides end-to-end biometric identity solutions including enrollment kiosks, document readers, and automated border control e-gates, with deployments across major European and Asia Pacific international airports.

January 2024: NEC Corporation announced the expansion of its NeoFace facial recognition platform to five additional international airports in Southeast Asia under a multi-year managed services contract, reinforcing its regional leadership position.

March 2024: Thales Group secured a contract with a major European airport consortium to deploy its PARAFE automated border control e-gate system across 12 terminal facilities, incorporating both facial and fingerprint recognition for dual-modal verification.

May 2024: The U.S. Transportation Security Administration (TSA) released updated biometric technology standards requiring facial recognition accuracy thresholds of 98% or above for all newly procured airport identity verification systems, raising the compliance bar for vendors.

July 2024: Amadeus IT Group SA launched its biometric token integration module within its Altéa Departure Control suite, enabling airlines on the Altéa platform to offer contactless biometric boarding across enrolled passenger populations.

September 2024: IndraSistemas S.A. completed deployment of its biometric passenger processing solution at a major Latin American hub airport, processing over 40,000 daily passengers through facial recognition-enabled check-in and boarding gates.

November 2024: The European Union confirmed revised implementation timelines for its Entry/Exit System (EES), mandating biometric capture at all Schengen external borders by mid-2025, catalyzing accelerated procurement activity among EU member state airport authorities.

February 2025: Safran announced a strategic R&D partnership with a leading semiconductor firm to develop next-generation edge-AI biometric processing chips designed specifically for high-throughput airport gate environments.

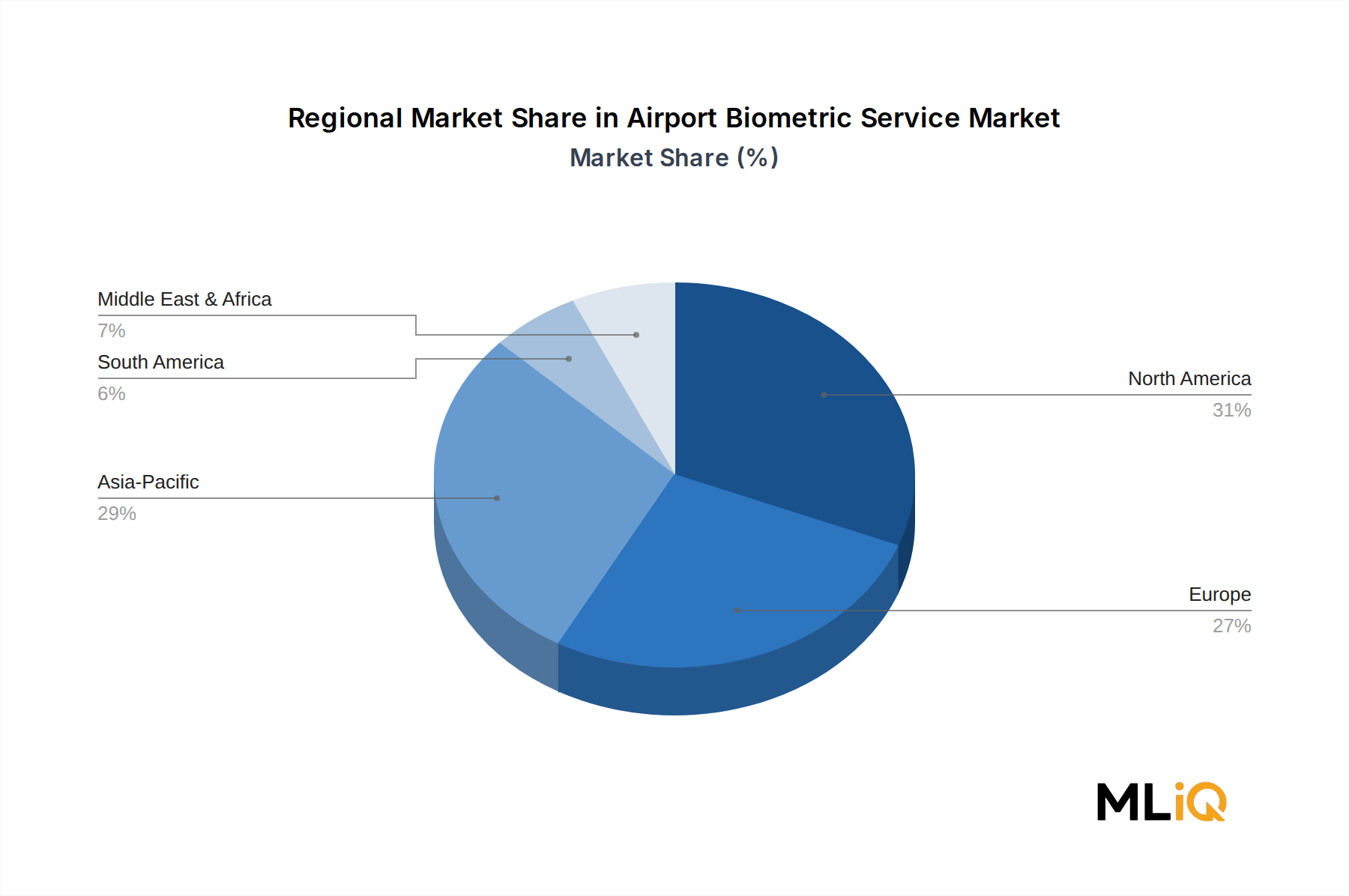

The Airport Biometric Service Market exhibits significant regional heterogeneity in terms of growth rates, adoption maturity, regulatory context, and investment volumes.

North America holds the largest absolute revenue share of the global market, accounting for an estimated 34% of total market value. The United States is the primary revenue contributor, driven by the CBP Biometric Exit program, TSA biometric screening pilots, and substantial private investment by major hub airports including Hartsfield-Jackson Atlanta, Los Angeles International, and John F. Kennedy International. Canada is advancing its biometric border modernization under the Beyond the Border initiative. The regional CAGR for North America is estimated at 14.8%, slightly below the global average, reflecting the relative maturity of existing deployments.

Asia Pacific is the fastest-growing region, projected to expand at a CAGR of 20.1% through the forecast period. China's rapid airport infrastructure buildout — with over 200 new airport projects in various stages of development — combined with Japan's biometric modernization ahead of major international events and India's DIGI Yatra facial recognition rollout across domestic airports, collectively make Asia Pacific the highest-growth opportunity. South Korea and ASEAN nations are also investing heavily in biometric border control.

Europe represents the second-largest market by revenue, with a CAGR of approximately 16.2%. The impending EES mandate is the single largest procurement catalyst, compelling all Schengen-area airports to install biometric enrollment and verification infrastructure. Germany, France, and the United Kingdom are leading deployers, while Nordics and Benelux nations are advancing voluntary biometric self-service initiatives beyond regulatory minimum requirements.

The Middle East and Africa region, led by GCC nations, is emerging as a premium adopter of biometric technology. Dubai International Airport's Smart Gates and Abu Dhabi's integrated biometric passenger journey — which eliminates passports across the entire terminal process — represent global showcase implementations. The regional CAGR is estimated at 18.5%, driven by high per-passenger infrastructure investment and government digital transformation agendas.

South America, while a smaller absolute contributor, is showing accelerating interest, particularly in Brazil and Argentina, where airport concession privatizations are driving technology modernization investment. The regional CAGR stands at approximately 15.3%.

Three disruptive technology vectors are reshaping the innovation landscape of the Airport Biometric Service Market and will determine competitive advantage over the next five to seven years.

The first is multimodal biometric fusion. While single-modal systems — particularly the Facial Recognition Market and Fingerprint Recognition Market — have achieved significant deployment scale, next-generation systems are increasingly fusing two or more biometric modalities in real time. Multimodal fusion algorithms combine facial geometry, gait patterns, iris texture, and palm vein maps into a single confidence score, dramatically reducing false acceptance and rejection rates. R&D investment in this area is accelerating, with major vendors allocating between 8% and 12% of annual revenue to fusion algorithm development. Adoption timelines suggest commercial-grade multimodal solutions will be standard in new airport installations by 2027.

The second disruptive technology is edge AI inference for on-device biometric processing. Traditional architectures route biometric templates to centralized data centers for matching, introducing latency and network dependency. Edge AI chips — purpose-designed neural processing units embedded directly in camera housings, kiosk terminals, or gate readers — perform matching locally in under 200 milliseconds, eliminating cloud round-trip delays and reducing data exposure surface. This architectural shift threatens incumbent cloud-platform business models while creating new hardware component market opportunities within the broader Biometric Authentication Market. Semiconductor investments in airport-grade edge AI processors are projected to grow at above 25% annually through 2028.

The third vector is behavioral and continuous biometrics. Rather than single-point verification at a gate or kiosk, behavioral biometric systems continuously monitor gait, posture, and movement signatures throughout the terminal, providing ongoing identity assurance without repeated explicit verification steps. These systems operate within the context of the broader Identity Verification Market and overlap with surveillance analytics platforms. While adoption is currently limited to high-security terminals and pilot programs, behavioral biometric solutions are expected to achieve meaningful commercial penetration in international airport environments by 2028 to 2030.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 17.3% from 2020-2034 |

| Segmentation |

|

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Comprehensive validation mechanisms ensuring market intelligence accuracy, reliability, and adherence to international standards.

500+ data sources cross-validated

200+ industry specialists validation

NAICS, SIC, ISIC, TRBC standards

Continuous market tracking updates

Factors such as are projected to boost the Airport Biometric Service Market market expansion.

Key companies in the market include 3M Cogent Inc.?, ADB Safegate, Inform Software, Inner Range, Safran?, Amadeus IT Group SA, Vanderbilt Industries, NEC Corporation?, IndraSistemas S.A., Thales Group.

The market segments include Scanner Type, Deployment Mode.

The market size is estimated to be USD 35.91 billion as of 2022.

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3200, USD 4335, and USD 7261 respectively.

The market size is provided in terms of value, measured in billion and volume, measured in .

Yes, the market keyword associated with the report is "Airport Biometric Service Market," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Airport Biometric Service Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.