1. What are the major growth drivers for the Middleware Market market?

Factors such as are projected to boost the Middleware Market market expansion.

+1 2315155523

Middleware Market

Middleware Market

Market Lens IQ is a global market intelligence and strategic consulting firm delivering advanced syndicated research reports, customized industry analysis, competitive intelligence, and data-driven advisory solutions to organizations across international markets. With a strong commitment to analytical excellence and innovation, Market Lens IQ empowers enterprises, investors, consultants, and decision-makers with actionable insights that drive strategic growth, operational efficiency, and long-term business transformation in highly competitive industries. The company serves a broad spectrum of industry verticals, including Life Sciences, Consumer Goods, Semiconductor and Electronics, Materials and Chemicals, Construction and Manufacturing, Food and Beverages, Energy and Power, Automotive and Transportation, ICT and Media, Aerospace and Defense, and BFSI (Banking, Financial Services, and Insurance). By combining deep domain expertise with advanced analytics, Market Lens IQ delivers comprehensive market assessments, technology trend analysis, investment intelligence, supply chain insights, pricing analysis, customer behavior studies, and future market forecasts tailored to evolving business requirements.

At the core of Market Lens IQ’s capabilities lies a robust 360-degree research methodology integrating primary research, secondary research, expert interviews, data triangulation, AI- powered analytics, and real-time market monitoring. Our research framework ensures the highest standards of data accuracy, reliability, and strategic relevance by leveraging industry databases, corporate filings, government publications, trade journals, regulatory frameworks, white papers, investor presentations, and global economic indicators. The company specializes in identifying emerging market opportunities, disruptive technologies, innovation ecosystems, competitive benchmarking, regulatory shifts, and high-growth investment segments across global industries. Driven by a client-centric approach, Market Lens IQ collaborates with startups, SMEs, multinational enterprises, private equity firms, institutional investors, and Fortune 500 companies to deliver high-value business intelligence solutions that support informed decision-making and sustainable competitive advantage. Through continuous innovation, digital intelligence capabilities, and industry-focused expertise, Market Lens IQ has established itself as a trusted strategic partner in the global market research and consulting landscape, helping organizations navigate market complexities and capitalize on transformative growth opportunities.

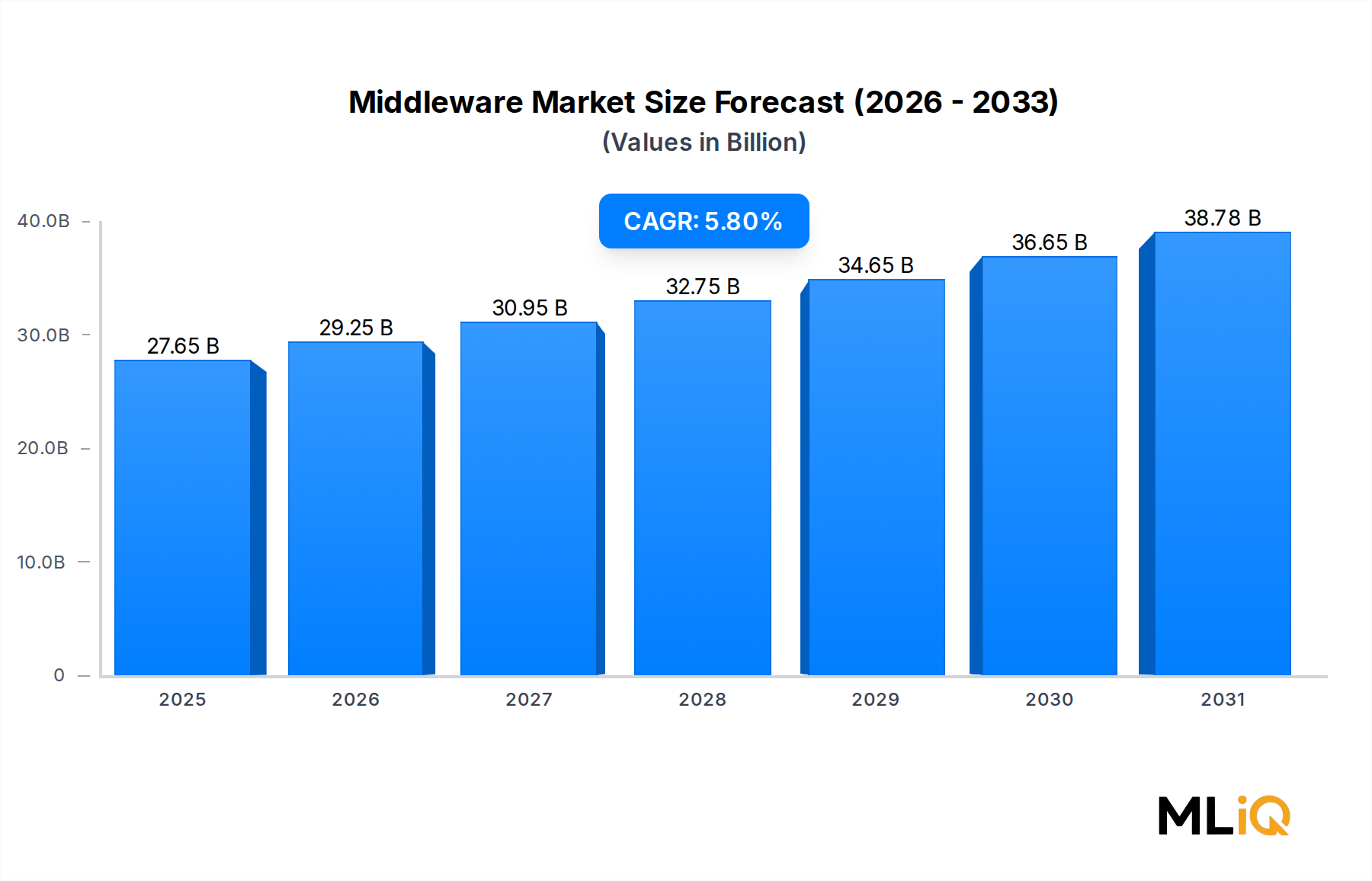

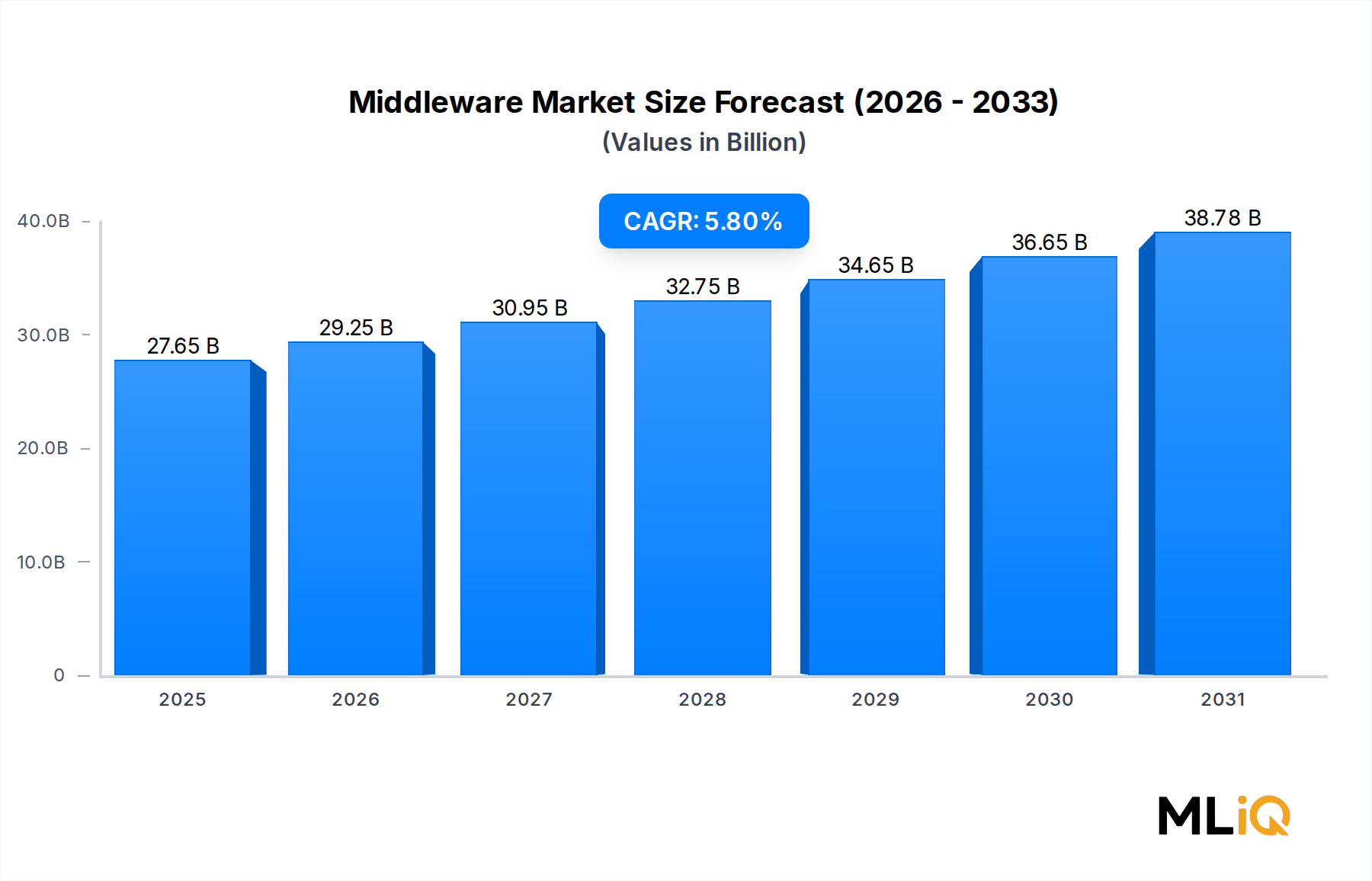

The global Middleware Market is valued at $27.65 billion in 2025 and is projected to expand at a compound annual growth rate (CAGR) of 5.8% through 2033, reflecting sustained and broad-based investment in enterprise software integration infrastructure. This growth trajectory is underpinned by accelerating digital transformation initiatives across industries, the proliferation of cloud-native architectures, and rising enterprise demand for seamless application interoperability in increasingly heterogeneous IT environments.

At its core, middleware serves as the connective tissue of modern enterprise IT — bridging operating systems, databases, applications, and network layers. As organizations transition from monolithic architectures to microservices and containerized deployments, the demand for robust middleware platforms has intensified considerably. The shift from on-premise deployments to hybrid and multi-cloud environments is particularly driving middleware adoption, as enterprises require standardized communication layers that can span multiple cloud providers and legacy systems simultaneously.

Key demand drivers include the explosive growth of API ecosystems, where middleware platforms serve as orchestration hubs for thousands of API interactions per second in large enterprises. The BFSI sector remains one of the most significant end-use verticals, leveraging middleware for real-time transaction processing, regulatory compliance reporting, and core banking system modernization. Healthcare digital transformation — including electronic health record (EHR) integration and telemedicine platform connectivity — represents another high-growth demand segment for middleware providers.

Macro tailwinds supporting the Middleware Market include widespread enterprise investment in DevOps toolchains, the maturation of Kubernetes and containerization ecosystems, and escalating data sovereignty requirements that necessitate sophisticated multi-region integration platforms. Furthermore, the global expansion of 5G infrastructure is creating new integration challenges and opportunities at the network edge, where middleware solutions are increasingly deployed to manage latency-sensitive workloads.

From a competitive standpoint, the market is moderately consolidated among a handful of large platform vendors — including IBM Corporation, Microsoft Corporation, Oracle Corporation, and SAP SE — while a vibrant ecosystem of specialized vendors competes aggressively on performance, cloud-nativeness, and vertical-specific functionality. The competitive intensity is expected to increase through 2033 as hyperscale cloud providers deepen their native middleware offerings, potentially commoditizing certain integration layers.

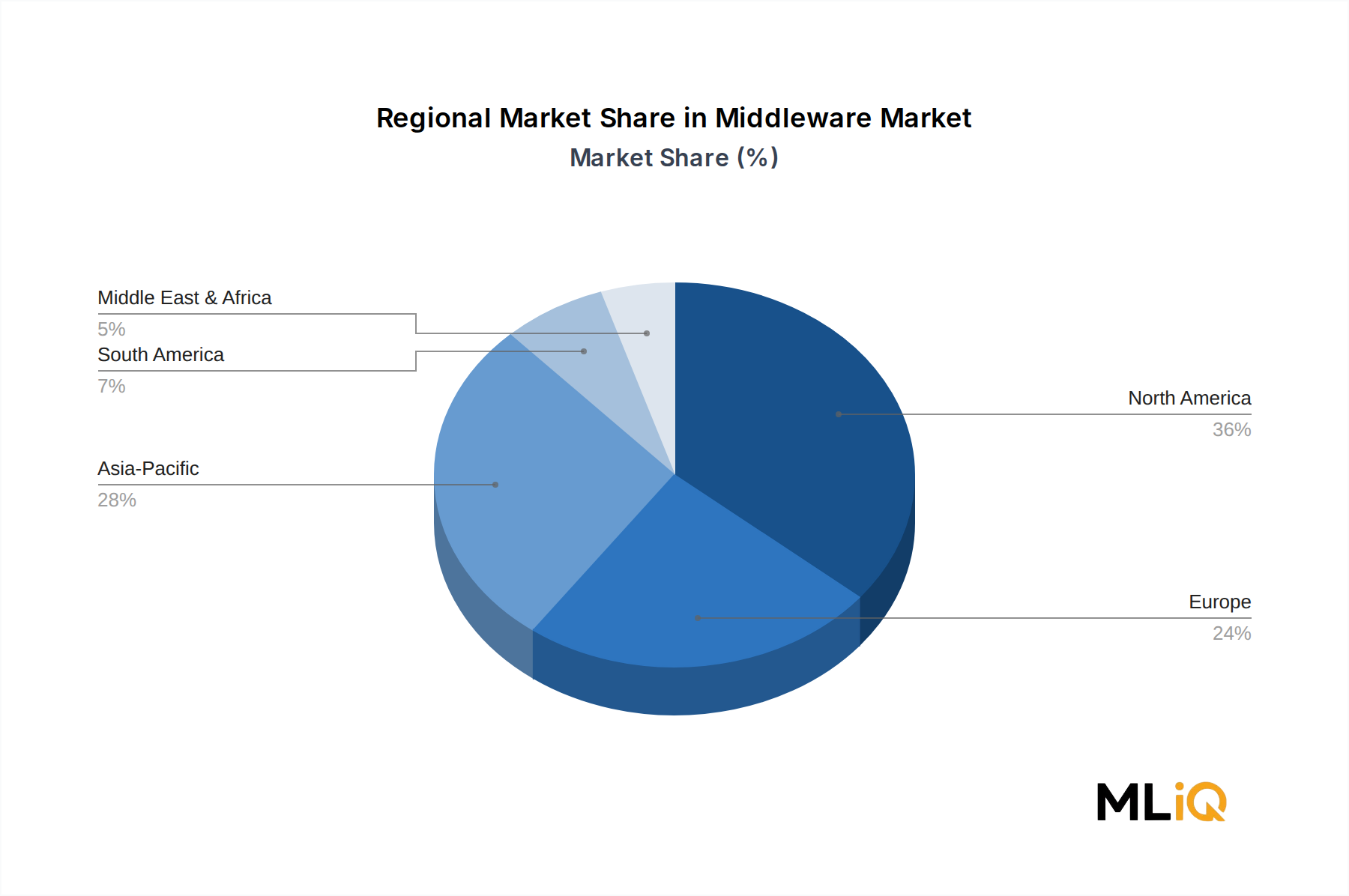

Geographically, North America holds the largest revenue share, while Asia Pacific is the fastest-growing region, driven by rapid enterprise digitalization in China, India, and Southeast Asia. Europe's market is characterized by strong regulatory compliance requirements that elevate middleware spending in financial and healthcare sectors. Overall, the Middleware Market is positioned for sustained, multi-year expansion as integration complexity continues to rise across every major industry vertical globally.

Among all segmentation dimensions in the Middleware Market, the cloud deployment model has emerged as the dominant and fastest-expanding category, commanding the largest revenue share in 2025 and expected to sustain its leadership position through 2033. This dominance is a direct consequence of enterprise-wide cloud migration strategies, the evolution of platform-as-a-service (PaaS) ecosystems, and the operational efficiencies that cloud-delivered middleware provides compared to traditional on-premise alternatives.

Cloud-based middleware solutions offer elastic scalability, consumption-based pricing, reduced infrastructure management overhead, and faster deployment cycles — all attributes that align directly with the operational priorities of modern IT organizations. Enterprises migrating workloads to hyperscale platforms such as Amazon Web Services (AWS), Microsoft Azure, and Google Cloud Platform find that cloud-native middleware is not merely convenient but architecturally essential, as it enables consistent integration patterns across distributed, geographically dispersed application landscapes.

The transition is particularly pronounced in large enterprises, where the volume and complexity of application integration requirements make cloud middleware platforms economically superior to maintaining proprietary on-premise integration servers. Large enterprises typically manage hundreds to thousands of internal and external application interfaces, and cloud middleware platforms provide centralized governance, monitoring, and lifecycle management capabilities that reduce total cost of ownership substantially.

Key players driving the cloud deployment segment include Amazon Web Services Inc., which offers a comprehensive suite of managed integration services including Amazon MQ, AWS Step Functions, and Amazon EventBridge. Microsoft Corporation's Azure Integration Services portfolio — encompassing Azure Logic Apps, Azure Service Bus, and Azure API Management — has gained significant enterprise traction. IBM Corporation continues to evolve its cloud middleware stack through the IBM Cloud Pak for Integration platform, targeting enterprises with complex hybrid integration requirements. Oracle Corporation competes aggressively with its Oracle Integration Cloud, particularly within its installed base of ERP and database customers. SAP SE's SAP Integration Suite addresses the needs of customers running SAP application ecosystems, while TIBCO Software Inc. provides a widely deployed cloud and hybrid integration platform.

The competitive dynamics within the cloud deployment segment are shaped by several structural forces. First, the hyperscale cloud providers have the advantage of native integration with their own compute, storage, and database services, creating platform lock-in economics that favor bundled middleware consumption. Second, independent software vendors (ISVs) like TIBCO, Software AG, and MuleSoft (Salesforce.com Inc.) compete on the basis of multi-cloud neutrality, advanced API management, and superior developer experience — positioning themselves as integration layers that sit above any single cloud provider.

On-premise middleware deployment, while declining as a share of new deployments, retains significance in sectors with stringent data residency requirements — notably government, defense, and certain financial services use cases where regulatory constraints prevent workload migration to public cloud environments. Hybrid deployment architectures, which combine on-premise middleware nodes with cloud-based integration platforms, represent a significant transitional category that bridges both segments.

The cloud deployment segment's share is expected to continue growing as small and medium enterprises (SMEs) increasingly adopt SaaS-delivered middleware solutions that require minimal upfront investment and infrastructure expertise. This democratization of integration capabilities is opening new addressable market segments that were historically underserved by middleware vendors focused primarily on large enterprise customers. Overall, the cloud deployment model's dominance in the Middleware Market reflects a structural and irreversible shift in enterprise IT architecture preferences.

The Middleware Market is propelled by several quantifiable and strategically significant drivers, while simultaneously facing constraints that moderate growth in specific segments and geographies.

Primary Driver — Digital Transformation Investment: Global enterprise digital transformation spending exceeded $2.3 trillion in 2024 according to industry estimates, with application integration and middleware infrastructure representing a critical spending category. Organizations undergoing digital transformation require middleware to connect legacy systems with modern cloud-native applications — a technical necessity that directly translates into middleware procurement decisions. Enterprises in the BFSI, healthcare, and retail sectors are particularly active in this regard.

Primary Driver — API Economy Expansion: The API Management Market has grown in parallel with middleware adoption, as organizations expose internal services through standardized APIs that require robust gateway, orchestration, and monitoring capabilities. The average large enterprise now manages more than 900 APIs, a figure that has tripled over five years, creating structural demand for middleware platforms capable of governing high-volume API traffic.

Primary Driver — IoT and Edge Integration Requirements: The Internet of Things Platform Market is generating unprecedented volumes of device-generated data that must be ingested, processed, and routed to enterprise applications in real time. Middleware platforms serve as the integration layer between IoT edge nodes and backend systems, and with connected device counts projected to exceed 30 billion by 2030, this represents a durable demand driver.

Key Constraint — Complexity and Integration Fatigue: Despite strong demand, middleware deployment projects frequently encounter implementation complexity, skill shortages, and integration debt from accumulated legacy configurations. These factors can extend deployment timelines and increase total cost of ownership, creating hesitation among budget-constrained organizations.

Key Constraint — Hyperscaler Competition: As Amazon Web Services Inc., Microsoft Corporation, and Google deepen their native integration services, the Enterprise Service Bus Market and traditional message-oriented middleware vendors face pricing pressure and competitive displacement risk, particularly in greenfield cloud deployments.

Key Constraint — Data Sovereignty and Regulatory Fragmentation: Varying data localization laws across the European Union, China, India, and other jurisdictions complicate multi-region middleware deployments, increasing architectural complexity and compliance costs for global enterprises.

The Middleware Market features a mix of large diversified technology conglomerates, specialized integration platform vendors, and hyperscale cloud providers. The following profiles outline the strategic positioning of the market's key participants:

Software AG: A Germany-based integration and IoT software specialist, Software AG competes through its webMethods integration platform and ARIS process intelligence suite, targeting enterprise customers with complex hybrid integration requirements and process automation needs.

Microsoft Corporation: One of the most broadly deployed middleware providers globally, Microsoft delivers integration capabilities through its Azure Integration Services portfolio, benefiting from deep installed base penetration across enterprise productivity, ERP, and cloud infrastructure segments.

Oracle Corporation: Oracle's middleware strategy is tightly coupled with its database and cloud application ecosystem, with Oracle Integration Cloud and Oracle SOA Suite serving customers running Oracle Fusion Applications, enabling seamless application-to-application connectivity within Oracle-centric architectures.

TIBCO Software Inc.: TIBCO is a long-standing specialist in enterprise integration, messaging, and analytics middleware, with its TIBCO BusinessWorks and EBX platforms widely deployed in financial services, energy, and telecommunications industries globally.

Salesforce.com Inc.: Through its MuleSoft subsidiary, Salesforce.com Inc. operates one of the most recognized API-led integration platforms in the market, with Anypoint Platform serving thousands of enterprise customers across industries requiring multi-cloud and hybrid integration architectures.

Fujitsu Ltd: Fujitsu contributes middleware solutions primarily within its broader IT services and infrastructure business, serving government, manufacturing, and financial services clients predominantly in Japan and select international markets.

Amazon Web Services Inc.: As the world's largest cloud provider, Amazon Web Services Inc. offers a comprehensive portfolio of managed integration services — including Amazon MQ, EventBridge, and Step Functions — that directly compete with traditional middleware vendors on cloud-native integration use cases.

IBM Corporation: IBM Corporation holds a significant position in the Middleware Market through its IBM MQ, IBM App Connect, and IBM Cloud Pak for Integration platforms, with particular strength in regulated industries including banking, insurance, and government.

SAP SE: SAP SE's integration middleware strategy centers on SAP Integration Suite and SAP Event Mesh, designed to connect SAP and non-SAP applications across hybrid environments, with a large installed base of enterprise ERP customers providing a captive demand base.

Unisys Corporation: Unisys positions its middleware and integration capabilities as part of its broader IT services portfolio, focusing on public sector, logistics, and financial services clients that require secure, high-availability integration infrastructure.

January 2025: IBM Corporation announced an enhanced version of IBM App Connect Enterprise with native support for generative AI-assisted integration mapping, reducing integration development time by a claimed 40% in enterprise pilot programs.

February 2025: Salesforce.com Inc. (MuleSoft) launched Anypoint Code Builder with AI-powered flow generation capabilities, targeting developer productivity improvements in complex multi-cloud integration scenarios.

March 2025: Amazon Web Services Inc. expanded Amazon EventBridge to support cross-account and cross-region event routing with enhanced encryption controls, addressing data sovereignty concerns for enterprise customers operating in regulated industries.

April 2025: Microsoft Corporation introduced Azure Integration Environments, a new deployment boundary feature for Azure Integration Services, enabling teams to group and manage integration resources with environment-level governance controls.

April 2025: SAP SE announced a strategic partnership extension with Hyperscaler providers to deepen SAP Integration Suite's native connectors for multi-cloud environments, targeting migration acceleration for S/4HANA customers.

May 2025: TIBCO Software Inc. (now part of Cloud Software Group) released TIBCO BusinessWorks 3.0 with containerized, Kubernetes-native deployment support, signaling a full architectural transition from legacy on-premise deployment models to cloud-native paradigms.

May 2025: Software AG completed the integration of its recently acquired StreamSets data pipeline platform into the webMethods ecosystem, creating a unified hybrid integration and data streaming portfolio targeting real-time analytics use cases.

The Middleware Market exhibits distinct regional growth profiles shaped by enterprise IT maturity, cloud adoption rates, regulatory environments, and vertical industry composition.

North America remains the most mature and largest revenue-generating region, accounting for an estimated 38% of global Middleware Market revenue in 2025. The United States is the primary driver, underpinned by high enterprise cloud adoption, a dense concentration of technology vendors and financial institutions, and sustained investment in digital infrastructure modernization. Canada and Mexico contribute incrementally, with Mexico's growing manufacturing and fintech sectors representing emerging middleware demand vectors. North America's CAGR is estimated at 4.9% through 2033, reflecting market maturity rather than deceleration.

Europe represents approximately 27% of global revenue, with Germany, the United Kingdom, and France as the leading national markets. The European market is characterized by strong demand from BFSI and healthcare verticals, where regulatory compliance requirements — particularly under GDPR, DORA (Digital Operational Resilience Act), and NIS2 — mandate robust and auditable integration architectures. Europe's middleware CAGR is estimated at 5.2%, with regulatory-driven spending acting as a consistent demand stabilizer.

Asia Pacific is the fastest-growing region, with a projected CAGR of 7.6% through 2033, driven by rapid enterprise digitalization in China, India, Japan, and the ASEAN bloc. China's domestic middleware market is growing rapidly, fueled by government-backed digital infrastructure investment and the expansion of domestic cloud platforms. India's IT services sector and expanding startup ecosystem are generating strong demand for cloud-native integration platforms. Japan and South Korea contribute mature, high-value demand, particularly in manufacturing and automotive sectors adopting Industry 4.0 architectures.

The Middle East and Africa region is emerging as a meaningful growth market, with GCC countries — particularly Saudi Arabia and the UAE — investing heavily in digital government and smart city infrastructure that requires sophisticated integration middleware. The regional CAGR is estimated at 6.8%, albeit from a smaller base.

South America, led by Brazil and Argentina, represents a developing market with a CAGR of approximately 5.5%, primarily driven by financial services digitalization and retail sector e-commerce integration requirements.

The Middleware Market, as a software-centric industry, does not rely on physical raw materials in the traditional manufacturing sense. However, it has critical upstream dependencies on hardware infrastructure, semiconductor supply chains, and cloud computing capacity — all of which experienced significant disruption between 2020 and 2023 and continue to influence market dynamics.

The most significant upstream dependency is on server hardware and data center infrastructure, which underpins both on-premise middleware deployments and the hyperscale cloud platforms through which cloud middleware is delivered. The global semiconductor shortage that peaked in 2021-2022 created extended lead times for server procurement, delaying on-premise middleware deployment projects and accelerating the shift toward cloud-delivered middleware as enterprises sought to avoid capital expenditure on constrained hardware. This supply chain disruption paradoxically accelerated cloud middleware adoption, a trend that has proved structurally durable.

The IT Infrastructure Market remains a critical adjacency — fluctuations in server processor pricing, memory DRAM costs, and storage media prices directly affect the total cost of ownership for on-premise middleware deployments. DRAM prices, for instance, declined significantly through 2023 before stabilizing, reducing per-unit infrastructure costs for organizations maintaining on-premise middleware environments.

For cloud-delivered middleware, the supply chain dynamics are concentrated in hyperscaler data center capacity — specifically the availability of GPU and CPU compute nodes, power infrastructure, and fiber connectivity. The surge in demand for AI compute capacity in 2023-2025 has created competitive pressure on data center capacity allocation, with implications for cloud middleware performance SLAs in high-traffic environments.

Open-source software components represent another critical input for the Middleware Market. Apache Kafka, RabbitMQ, ActiveMQ, and Kubernetes form the technical foundation of numerous commercial middleware platforms. Disruptions to open-source project governance, licensing changes (as seen with HashiCorp's BSL license transition in 2023), or security vulnerabilities in foundational libraries can create supply-side risk for middleware vendors that build commercial products on open-source foundations.

The Digital Transformation Services Market is also tightly linked to middleware supply chains, as system integrators and consulting firms represent the primary channel through which middleware solutions are implemented and deployed. Talent short

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.8% from 2020-2034 |

| Segmentation |

|

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Comprehensive validation mechanisms ensuring market intelligence accuracy, reliability, and adherence to international standards.

500+ data sources cross-validated

200+ industry specialists validation

NAICS, SIC, ISIC, TRBC standards

Continuous market tracking updates

Factors such as are projected to boost the Middleware Market market expansion.

Key companies in the market include Software AG, Microsoft Corporation, Oracle Corporation, TIBCO Software Inc., Salesforce.com Inc., Fujitsu Ltd, Amazon Web Services Inc., IBM Corporation, SAP SE, Unisys Corporation.

The market segments include Deployment Model, Organization Size, Industry Vertical.

The market size is estimated to be USD 27.65 billion as of 2022.

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3690, USD 5820, and USD 9870 respectively.

The market size is provided in terms of value, measured in billion and volume, measured in .

Yes, the market keyword associated with the report is "Middleware Market," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Middleware Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.