1. What are the major growth drivers for the Data Warehouse-as-a-Service Market market?

Factors such as are projected to boost the Data Warehouse-as-a-Service Market market expansion.

+1 2315155523

Data Warehouse-as-a-Service Market

Data Warehouse-as-a-Service Market

Market Lens IQ is a global market intelligence and strategic consulting firm delivering advanced syndicated research reports, customized industry analysis, competitive intelligence, and data-driven advisory solutions to organizations across international markets. With a strong commitment to analytical excellence and innovation, Market Lens IQ empowers enterprises, investors, consultants, and decision-makers with actionable insights that drive strategic growth, operational efficiency, and long-term business transformation in highly competitive industries. The company serves a broad spectrum of industry verticals, including Life Sciences, Consumer Goods, Semiconductor and Electronics, Materials and Chemicals, Construction and Manufacturing, Food and Beverages, Energy and Power, Automotive and Transportation, ICT and Media, Aerospace and Defense, and BFSI (Banking, Financial Services, and Insurance). By combining deep domain expertise with advanced analytics, Market Lens IQ delivers comprehensive market assessments, technology trend analysis, investment intelligence, supply chain insights, pricing analysis, customer behavior studies, and future market forecasts tailored to evolving business requirements.

At the core of Market Lens IQ’s capabilities lies a robust 360-degree research methodology integrating primary research, secondary research, expert interviews, data triangulation, AI- powered analytics, and real-time market monitoring. Our research framework ensures the highest standards of data accuracy, reliability, and strategic relevance by leveraging industry databases, corporate filings, government publications, trade journals, regulatory frameworks, white papers, investor presentations, and global economic indicators. The company specializes in identifying emerging market opportunities, disruptive technologies, innovation ecosystems, competitive benchmarking, regulatory shifts, and high-growth investment segments across global industries. Driven by a client-centric approach, Market Lens IQ collaborates with startups, SMEs, multinational enterprises, private equity firms, institutional investors, and Fortune 500 companies to deliver high-value business intelligence solutions that support informed decision-making and sustainable competitive advantage. Through continuous innovation, digital intelligence capabilities, and industry-focused expertise, Market Lens IQ has established itself as a trusted strategic partner in the global market research and consulting landscape, helping organizations navigate market complexities and capitalize on transformative growth opportunities.

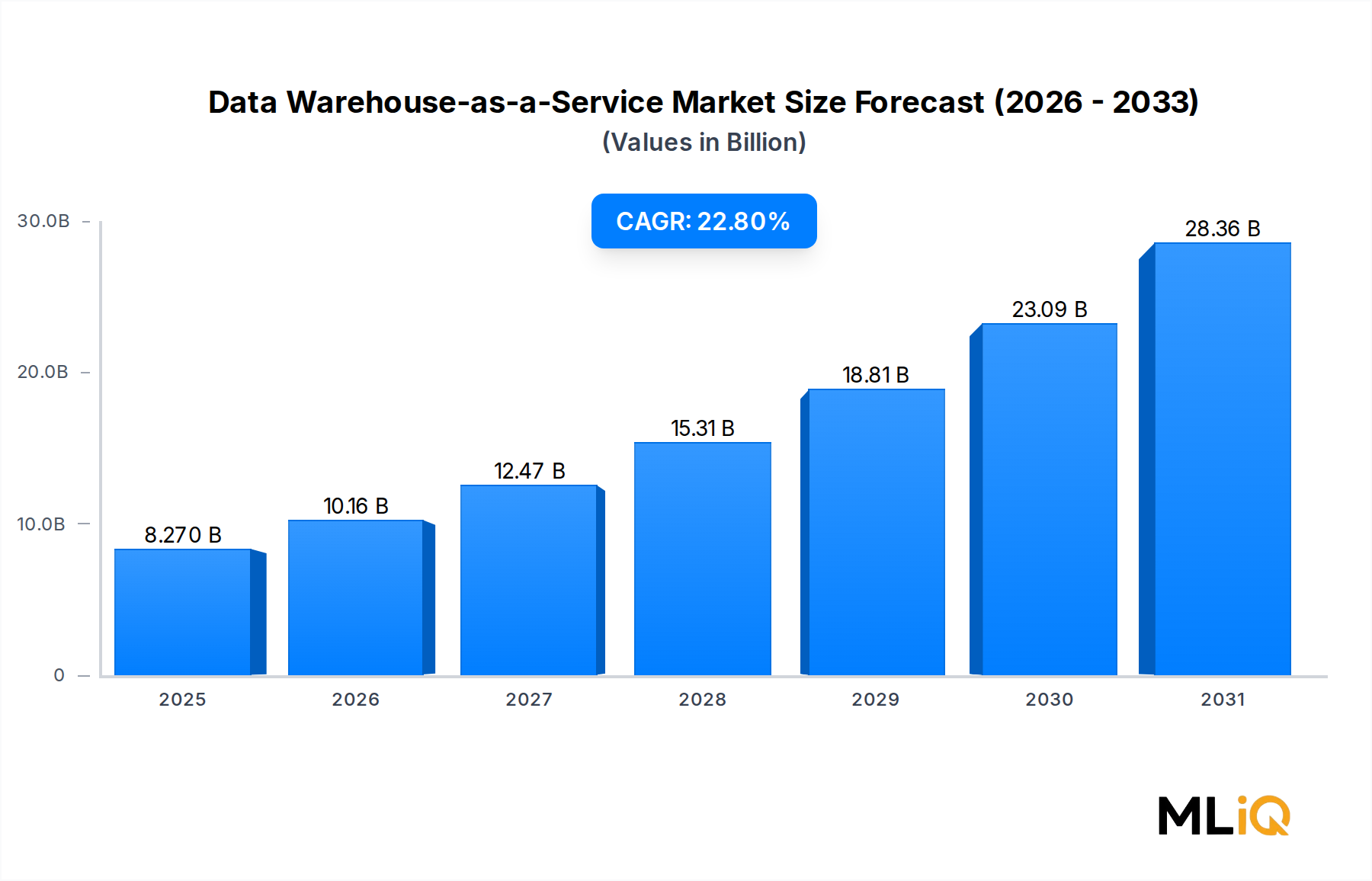

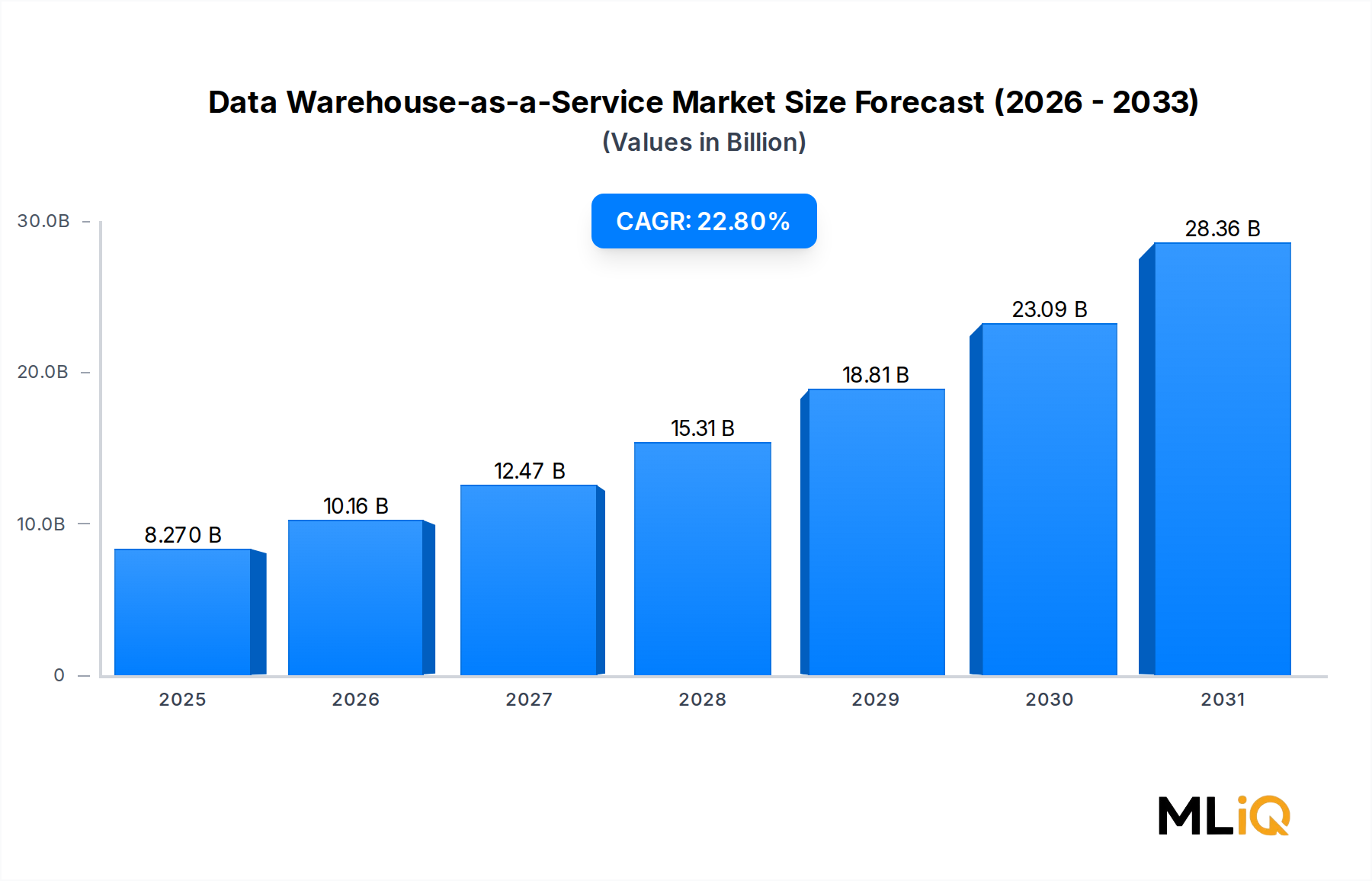

The global Data Warehouse-as-a-Service Market was valued at $8.27 billion in 2024 and is projected to expand at a compound annual growth rate (CAGR) of 22.8% through the forecast period, positioning it as one of the fastest-scaling segments within enterprise cloud infrastructure. This exceptional growth trajectory is underpinned by widespread enterprise migration away from on-premises data architectures toward fully managed, elastic, and consumption-based warehousing solutions that eliminate capital expenditure and reduce operational complexity.

A confluence of macro tailwinds is accelerating adoption across every major vertical. The exponential growth of structured and semi-structured enterprise data, driven by IoT proliferation, digital commerce, and real-time transactional systems, is overwhelming legacy on-premises warehouses that were not designed for modern throughput volumes. Simultaneously, the broader maturation of the Cloud Computing Market is reducing latency, improving data sovereignty options, and enabling multi-cloud interoperability, all of which remove historical barriers to cloud warehousing adoption.

Organizational agility demands are reshaping procurement behavior. Finance, retail, and healthcare enterprises are prioritizing platforms that allow analysts and data engineers to provision, scale, and decommission compute resources within minutes rather than weeks. This shift dramatically shortens time-to-insight cycles and aligns infrastructure spend with actual usage, a model particularly attractive to mid-market organizations operating under constrained IT budgets.

The rise of embedded analytics and the growing sophistication of self-serve business intelligence tooling are further embedding Data Warehouse-as-a-Service solutions into the daily workflows of non-technical business users. As the Big Data Market continues to expand, enterprises require warehousing platforms that can ingest, transform, and serve petabyte-scale datasets without performance degradation, pushing vendors to invest heavily in columnar storage engines, vectorized query execution, and intelligent workload management.

Geopolitically, regulatory frameworks such as GDPR, CCPA, and sector-specific mandates in financial services and healthcare are compelling organizations to adopt warehousing solutions with granular access controls, audit logging, and regional data residency options — capabilities that cloud-native platforms are uniquely positioned to deliver. Looking ahead, the convergence of large language model interfaces with data warehousing query layers, the integration of streaming pipelines, and the emergence of the lakehouse architecture are expected to sustain the 22.8% CAGR well into the latter half of the decade, as enterprises prioritize unified, governed, and cost-optimized data platforms.

The Enterprise Data Warehouse (EDW) sub-segment commands the largest revenue share within the Data Warehouse-as-a-Service Market, reflecting the longstanding primacy of centralized, schema-enforced, query-optimized repositories in large organizational data strategies. EDW deployments serve as the authoritative data layer for executive dashboards, regulatory reporting, financial consolidation, and strategic planning cycles — functions that demand the highest levels of consistency, performance, and governance.

Historically, on-premises EDW solutions from vendors such as Teradata Corp. and Oracle Corp. anchored enterprise data architectures for decades. The transition to cloud-native EDW delivery has not eroded demand for this sub-segment; rather, it has dramatically expanded the addressable market by making enterprise-grade warehousing capabilities accessible to organizations that previously lacked the capital or infrastructure expertise to deploy and maintain traditional EDW appliances. Snowflake Computing Inc. has been particularly transformative in this regard, decoupling compute from storage and enabling concurrent workloads to scale independently — a technical breakthrough that directly addressed the most persistent pain point of legacy EDW architectures.

Microsoft Corp., through Azure Synapse Analytics, has leveraged its dominant position in enterprise productivity and cloud infrastructure to embed warehousing capabilities directly into existing enterprise agreements, significantly lowering procurement friction. Google LLC's BigQuery has distinguished itself through serverless query execution and per-query pricing, attracting data engineering teams that prioritize cost transparency and operational simplicity. Amazon Web Service Inc. reinforces the EDW segment through Redshift, which benefits from deep integration with the broader AWS ecosystem including S3, Glue, and SageMaker.

The EDW sub-segment's dominance is consolidating rather than fragmenting. As organizations mature their cloud data strategies, they are converging on fewer, more capable platforms rather than maintaining fragmented warehouse estates. This consolidation dynamic benefits hyperscalers and pure-play cloud warehouse vendors that can offer end-to-end data lifecycle management — ingestion, transformation, storage, query, and governed sharing — within a single platform boundary.

The Enterprise Data Management Market dynamics are also reinforcing EDW segment leadership. Chief Data Officers are increasingly mandated to implement enterprise-wide data governance frameworks, master data management policies, and lineage tracking. Cloud EDW platforms that natively integrate data catalog, data quality, and role-based access control capabilities are winning competitive evaluations over point-solution alternatives, further entrenching the EDW sub-segment's revenue dominance.

From a deployment mode perspective, public cloud EDW deployments constitute the majority of new workloads, though regulated industries including banking, insurance, and government continue to invest in private cloud EDW deployments where data sovereignty and network isolation requirements cannot be met by shared infrastructure. Hybrid architectures that federate queries across public and private environments are emerging as the preferred long-term architecture for Global 2000 enterprises navigating complex compliance landscapes.

Organizational size segmentation reveals that large enterprises currently generate the highest absolute revenue within the EDW sub-segment, given their scale of data volumes and the complexity of their analytical workloads. However, the fastest incremental growth is being recorded among small and medium enterprises, which are adopting cloud EDW solutions for the first time, bypassing the on-premises era entirely and entering the market at a modern cloud-native baseline.

The Data Warehouse-as-a-Service Market is propelled by a set of quantifiable, structurally durable drivers that are collectively redefining enterprise data infrastructure investment priorities.

Data volume explosion constitutes the primary demand catalyst. Global data creation is projected to surpass 120 zettabytes by 2023 according to industry estimates, and enterprise-generated structured data is growing at roughly 23% annually. Legacy on-premises warehouses, typically provisioned for a fixed capacity ceiling, cannot accommodate this growth without expensive hardware refresh cycles. Cloud warehousing eliminates this constraint through elastic scaling, directly translating data volume growth into platform adoption.

Cloud migration momentum is measurable and accelerating. Enterprise cloud infrastructure spending surpassed $270 billion globally in 2023, with data and analytics workloads representing one of the highest-priority migration categories. Organizations that have already migrated core applications to cloud environments naturally extend their data infrastructure to cloud warehousing to eliminate cross-environment data movement latency and simplify networking architectures.

The Database Management System Market evolution is also a critical driver. As traditional relational database vendors pivot to cloud delivery models, the boundaries between transactional databases and analytical warehouses are blurring, pushing enterprises toward unified platforms that can serve both operational and analytical workloads simultaneously — a capability inherent to modern Data Warehouse-as-a-Service offerings.

Key constraints include data security and compliance complexity. Organizations operating across multiple jurisdictions face conflicting data residency mandates, creating architectural constraints that limit the use of single-region public cloud warehousing. Additionally, skills shortages in cloud data engineering are slowing deployment timelines, particularly in emerging markets. Vendor lock-in concerns remain a persistent procurement objection, as proprietary query dialects and storage formats create switching costs that dampen competitive dynamism.

Google LLC: Offers BigQuery, a serverless, multi-cloud analytical warehouse that leverages Google's global infrastructure and AI capabilities. Google has differentiated through Duet AI integration within BigQuery, enabling natural language querying for non-technical analysts.

IBM Corp.: Provides IBM Db2 Warehouse on Cloud and integrates warehousing capabilities within its broader IBM Cloud Pak for Data platform. IBM's competitive strength lies in hybrid cloud deployments serving regulated industries with existing IBM infrastructure commitments.

Snowflake Computing Inc.: Operates as the leading pure-play cloud data platform, known for its multi-cloud architecture spanning AWS, Azure, and Google Cloud. Snowflake's Data Cloud ecosystem and Marketplace differentiate it through cross-organization data sharing and monetization capabilities.

EMC Corp.: Contributes foundational storage and data management infrastructure that underpins cloud warehousing architectures. EMC's integration within the Dell Technologies portfolio supports enterprise hybrid data infrastructure strategies.

Oracle Corp.: Delivers Oracle Autonomous Data Warehouse, which uses machine learning to automate database tuning, security patching, and scaling. Oracle's entrenched position in enterprise ERP and financial applications provides a captive base for warehousing upsell.

Microsoft Corp.: Anchors enterprise cloud warehousing through Azure Synapse Analytics, combining data integration, big data analytics, and data warehousing in a unified workspace. Microsoft's integration with Power BI and Microsoft Fabric creates a deeply embedded analytics ecosystem.

Amazon Web Service Inc.: Markets Amazon Redshift as its primary warehousing offering, continuously enhanced through features like Redshift Serverless and Amazon Redshift ML. AWS's ecosystem breadth and customer base provide unmatched distribution leverage.

Teradata Corp.: Positions Teradata Vantage as a hybrid multi-cloud analytics platform targeting enterprises with complex, mixed-workload environments. Teradata's installed base in Fortune 500 financial and telecommunications accounts provides a stable revenue foundation.

Infobright Inc.: Specializes in columnar database technology optimized for high-compression analytical workloads. Infobright targets use cases requiring fast query performance on large datasets within cost-constrained environments.

SAP SE: Integrates warehousing capabilities through SAP Datasphere and SAP HANA Cloud, serving enterprises deeply invested in SAP ERP and supply chain ecosystems. SAP's business data fabric architecture enables governed data federation across heterogeneous sources.

March 2024: Snowflake Computing Inc. announced general availability of Snowflake Arctic, an open-source large language model optimized for enterprise SQL query generation, directly embedded within the Snowflake platform to accelerate natural language data access.

November 2023: Microsoft Corp. launched Microsoft Fabric, a unified analytics platform that consolidates Azure Synapse Analytics, Power BI, and Azure Data Factory into a single SaaS experience, representing the most significant Azure data platform restructuring in five years.

August 2023: Google LLC introduced BigQuery Studio, unifying data engineering, analytics, and machine learning development workflows within a single interface, reducing context-switching for data teams and deepening platform stickiness.

June 2023: Amazon Web Service Inc. released Amazon Redshift Serverless enhancements enabling automatic workload isolation and improved price-performance benchmarks, directly competing with Snowflake's separation-of-compute-and-storage model.

January 2024: SAP SE expanded SAP Datasphere with native integration to third-party cloud data platforms including Databricks and Google BigQuery, signaling a federated data fabric strategy rather than a closed warehousing ecosystem.

September 2023: Teradata Corp. announced Teradata VantageCloud Lake, a cloud-native tier of its platform optimized for open table formats including Apache Iceberg, targeting the growing lakehouse architecture adoption trend.

April 2024: Oracle Corp. released new Autonomous Data Warehouse capabilities featuring integrated vector search, positioning Oracle's platform for AI-augmented analytical workloads requiring both structured and unstructured data processing.

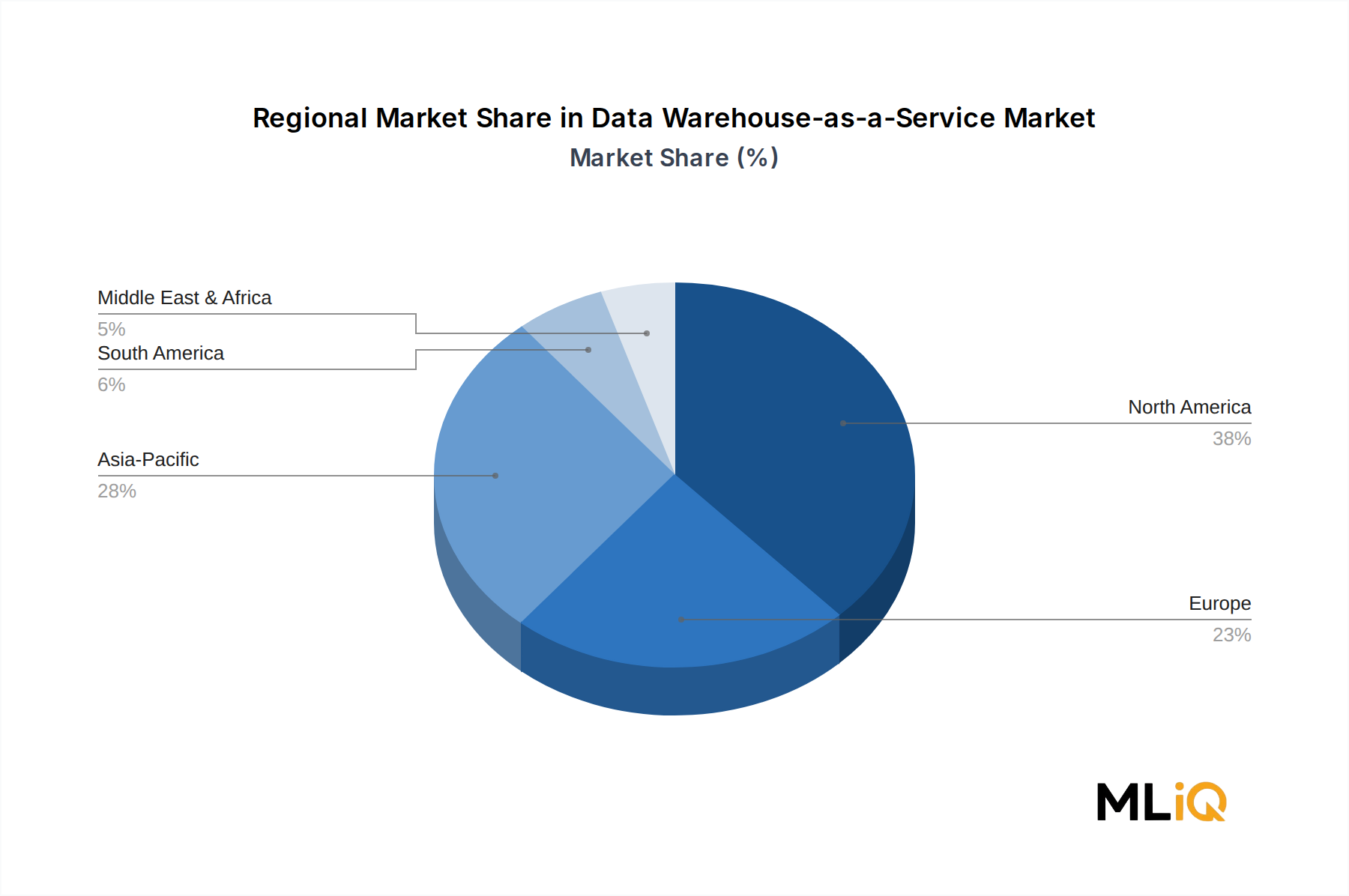

North America remains the most mature and highest-revenue region within the Data Warehouse-as-a-Service Market, accounting for an estimated 38% of global market revenue in 2024. The United States is the primary growth engine, driven by the concentration of hyperscaler headquarters, the density of Fortune 500 enterprises with large analytical workload budgets, and a highly developed cloud services procurement infrastructure. Canada contributes incremental growth through financial services and government digital modernization initiatives. The regional CAGR for North America is estimated at approximately 19%, reflecting a mature but still-expanding base as enterprises deepen platform utilization rather than accelerating new-logo acquisition.

Europe represents the second-largest regional market, with Germany, the United Kingdom, and France collectively driving the majority of regional revenue. GDPR compliance requirements have historically created procurement complexity but are increasingly acting as a demand accelerator, as cloud warehousing vendors invest in EU-sovereign cloud regions and data processing agreements that satisfy regulatory requirements. The European regional CAGR is estimated at 20.5%, with energy and utilities, banking, and manufacturing verticals leading adoption.

Asia Pacific is the fastest-growing region, with a projected CAGR of 27.3% through the forecast period. China, India, Japan, and South Korea are the primary contributors, each driven by distinct demand dynamics. India's IT and ITeS sector is a significant adopter due to its role in serving global analytics delivery. China's domestic cloud providers are investing heavily in warehousing capabilities to serve local enterprises constrained by data localization regulations. Japan and South Korea exhibit strong demand from manufacturing and telecommunications verticals embracing digital transformation mandates.

The Middle East and Africa region is emerging as a high-potential market, with GCC nations including Saudi Arabia and the UAE investing in data infrastructure as part of national digital economy strategies. The regional CAGR is estimated at 24.1%, with government and public sector and BFSI verticals leading adoption. South America, anchored by Brazil and Argentina, is growing at an estimated 21.8% CAGR, supported by expanding cloud infrastructure availability from hyperscalers establishing local data center regions and a growing base of digital-native enterprises in retail and fintech sectors. The Customer Data Platform Market dynamics are particularly influential in South America's retail-driven warehousing adoption patterns.

The supply chain underpinning the Data Warehouse-as-a-Service Market is fundamentally defined by the availability, cost, and performance characteristics of cloud infrastructure hardware — specifically high-density server processors, NAND flash storage, DRAM memory modules, and high-bandwidth networking equipment. Unlike traditional manufactured goods markets, the upstream dependencies of cloud warehousing are concentrated within a small number of semiconductor manufacturers and hyperscaler infrastructure operators, creating both scale advantages and systemic concentration risks.

NAND flash storage pricing is a particularly sensitive variable. Between 2021 and 2023, NAND flash prices experienced significant volatility, declining by over 50% from peak levels due to oversupply conditions among major manufacturers including Samsung, SK Hynix, and Micron. This price deflation directly reduced the per-terabyte cost of cloud storage, improving the economics of consumption-based warehousing pricing models and enabling vendors to offer more competitive storage rates without margin compression.

The global semiconductor shortage of 2021–2022 temporarily constrained hyperscaler capacity expansion plans, creating waitlist conditions for new Data Warehouse-as-a-Service customers in some regions. While this constraint has largely normalized, the concentration of advanced semiconductor fabrication at TSMC in Taiwan introduces ongoing geopolitical supply chain risk, particularly for GPU-class processors increasingly used in AI-augmented warehousing workloads.

The Cloud Data Integration Market's supply chain intersects directly with warehousing infrastructure, as data ingestion pipeline tooling relies on the same underlying compute and networking substrate. Disruptions in networking equipment supply chains, such as the extended lead times for Ethernet switching infrastructure experienced during 2022, demonstrated the cascading effects that component shortages can have on data center buildout timelines.

Energy costs represent a significant and increasingly scrutinized operational input. Data center power consumption directly influences cloud service pricing, and regional electricity price inflation — particularly acute in Europe during 2022–2023 — introduced upward cost pressure on cloud providers operating in those geographies. Hyperscalers are responding through long-term renewable energy purchase agreements and investments in liquid cooling technology to improve power usage effectiveness ratios.

The Data Warehouse-as-a-Service Market has attracted substantial and sustained capital investment across venture funding, strategic M&A, and hyperscaler organic investment over the 2022–2024 period, reflecting investor conviction in the market's long-term growth trajectory.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 22.8% from 2020-2034 |

| Segmentation |

|

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Comprehensive validation mechanisms ensuring market intelligence accuracy, reliability, and adherence to international standards.

500+ data sources cross-validated

200+ industry specialists validation

NAICS, SIC, ISIC, TRBC standards

Continuous market tracking updates

Factors such as are projected to boost the Data Warehouse-as-a-Service Market market expansion.

Key companies in the market include Google LLC, IBM Corp., Snowflake Computing Inc., EMC Corp., Oracle Corp., Microsoft Corp., Amazon Web Service Inc., Teradata Corp., Infobright Inc., SAP SE.

The market segments include Type, Operational Data Store, Deployment Mode, Application, Organizational Size, Industry Vertical.

The market size is estimated to be USD 8.27 billion as of 2022.

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3690, USD 5820, and USD 9870 respectively.

The market size is provided in terms of value, measured in billion and volume, measured in .

Yes, the market keyword associated with the report is "Data Warehouse-as-a-Service Market," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Data Warehouse-as-a-Service Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.