1. What are the major growth drivers for the Anomaly Detection Market market?

Factors such as are projected to boost the Anomaly Detection Market market expansion.

Anomaly Detection Market

Anomaly Detection Market

Market Lens IQ is a global market intelligence and strategic consulting firm delivering advanced syndicated research reports, customized industry analysis, competitive intelligence, and data-driven advisory solutions to organizations across international markets. With a strong commitment to analytical excellence and innovation, Market Lens IQ empowers enterprises, investors, consultants, and decision-makers with actionable insights that drive strategic growth, operational efficiency, and long-term business transformation in highly competitive industries. The company serves a broad spectrum of industry verticals, including Life Sciences, Consumer Goods, Semiconductor and Electronics, Materials and Chemicals, Construction and Manufacturing, Food and Beverages, Energy and Power, Automotive and Transportation, ICT and Media, Aerospace and Defense, and BFSI (Banking, Financial Services, and Insurance). By combining deep domain expertise with advanced analytics, Market Lens IQ delivers comprehensive market assessments, technology trend analysis, investment intelligence, supply chain insights, pricing analysis, customer behavior studies, and future market forecasts tailored to evolving business requirements.

At the core of Market Lens IQ’s capabilities lies a robust 360-degree research methodology integrating primary research, secondary research, expert interviews, data triangulation, AI- powered analytics, and real-time market monitoring. Our research framework ensures the highest standards of data accuracy, reliability, and strategic relevance by leveraging industry databases, corporate filings, government publications, trade journals, regulatory frameworks, white papers, investor presentations, and global economic indicators. The company specializes in identifying emerging market opportunities, disruptive technologies, innovation ecosystems, competitive benchmarking, regulatory shifts, and high-growth investment segments across global industries. Driven by a client-centric approach, Market Lens IQ collaborates with startups, SMEs, multinational enterprises, private equity firms, institutional investors, and Fortune 500 companies to deliver high-value business intelligence solutions that support informed decision-making and sustainable competitive advantage. Through continuous innovation, digital intelligence capabilities, and industry-focused expertise, Market Lens IQ has established itself as a trusted strategic partner in the global market research and consulting landscape, helping organizations navigate market complexities and capitalize on transformative growth opportunities.

+1 2315155523

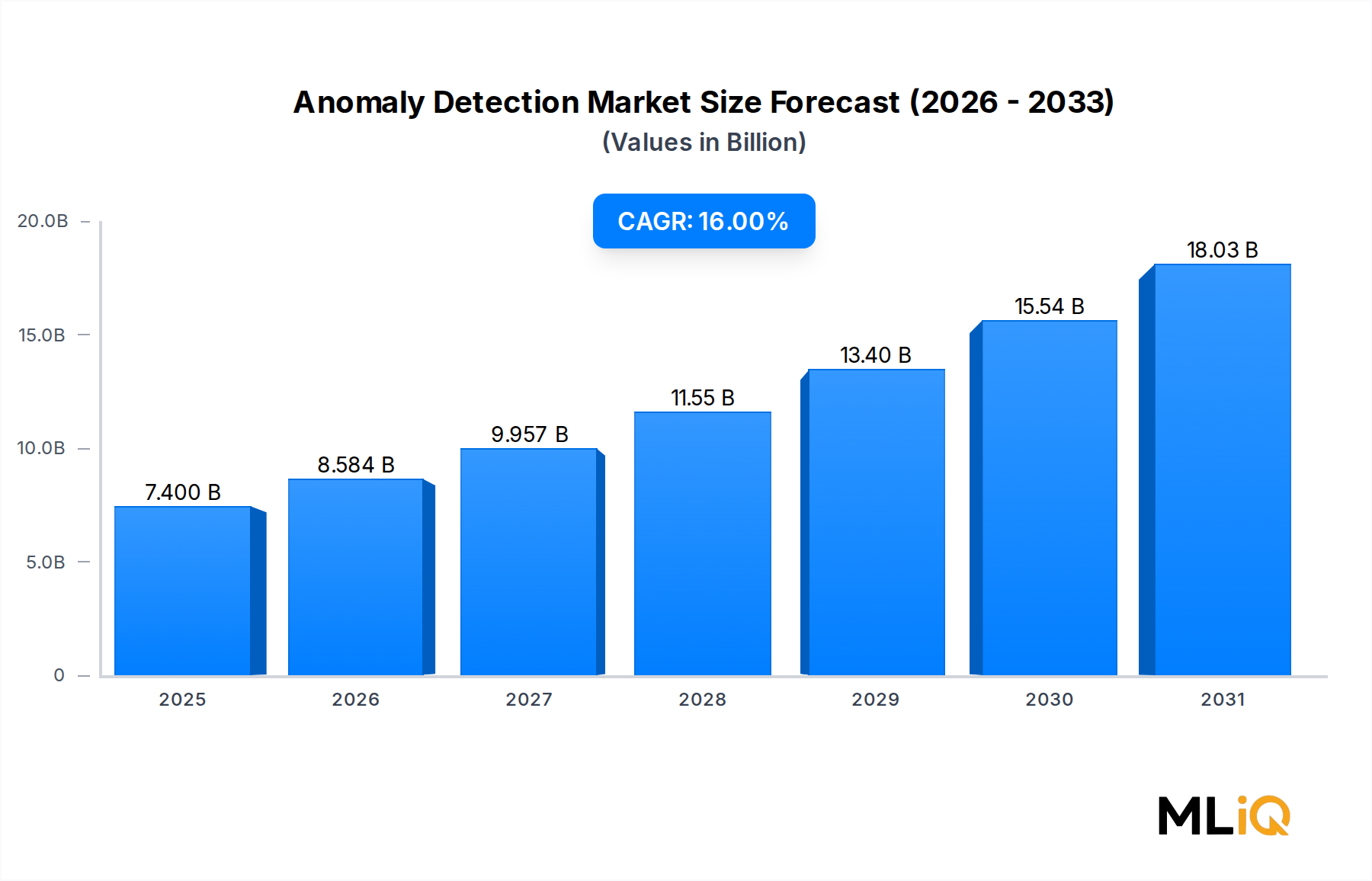

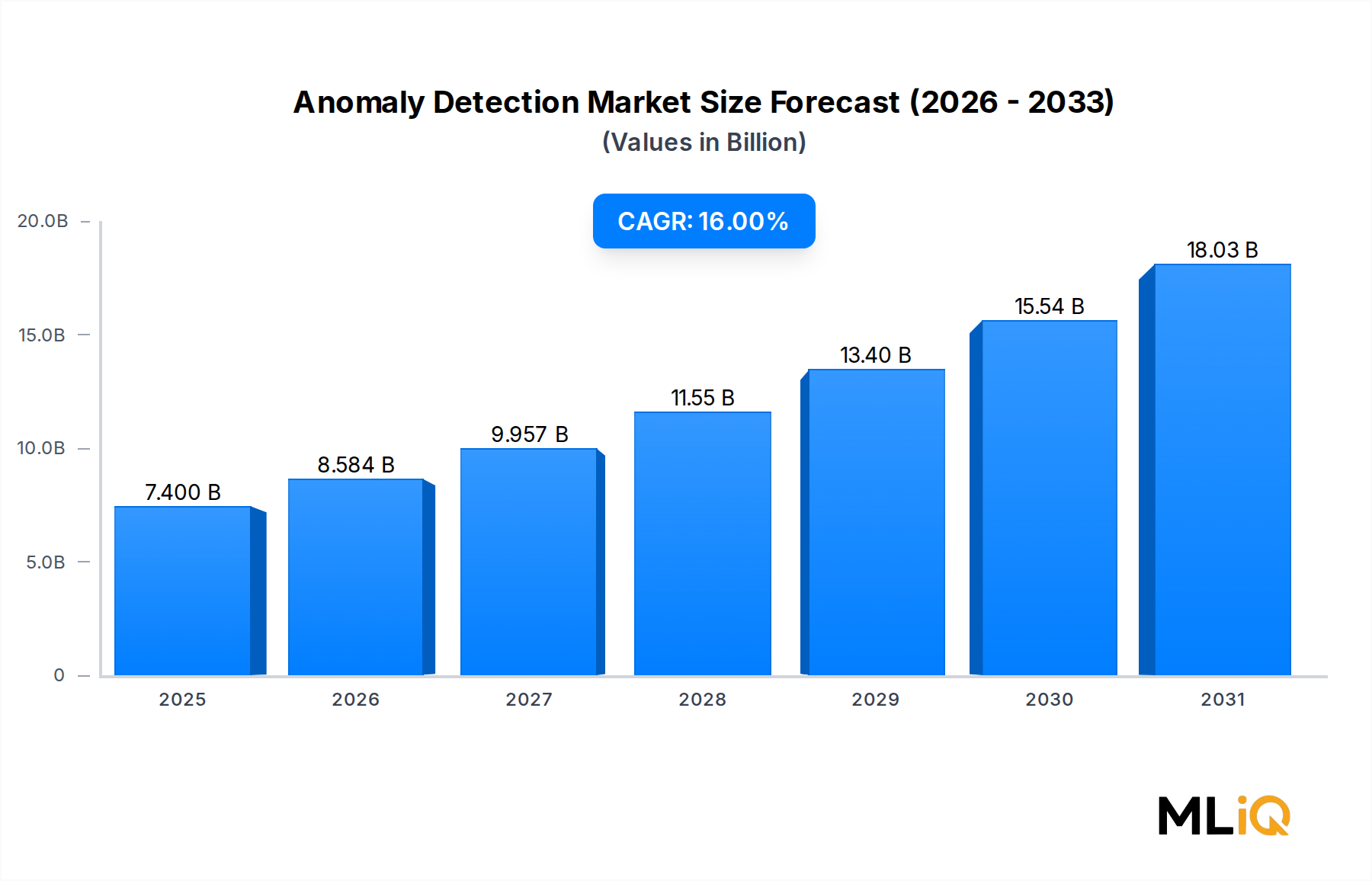

The global Anomaly Detection Market is valued at $7.4 billion in 2025 and is projected to expand at a compound annual growth rate (CAGR) of 16% through the forecast period, reflecting a strong and sustained upward trajectory driven by the convergence of digital transformation, escalating cybersecurity threats, and the rapid adoption of cloud-based analytical platforms. As organizations across every major industry vertical accelerate their migration to data-intensive environments, the imperative to identify irregular patterns—whether in network traffic, user behavior, financial transactions, or operational telemetry—has become a board-level priority rather than a purely technical concern.

Several macro tailwinds are reinforcing this growth. The global rise in sophisticated cyberattacks, including zero-day exploits and advanced persistent threats, has compelled enterprises to invest heavily in behavioral monitoring and real-time alerting systems. Regulatory mandates such as GDPR in Europe, HIPAA in healthcare, and PCI-DSS in financial services require organizations to demonstrate proactive data governance and breach detection capabilities, further cementing anomaly detection as a compliance tool as much as a security one.

The proliferation of connected devices under IoT and Industry 4.0 frameworks generates unprecedented volumes of machine-generated data, creating both the challenge of noise management and the opportunity for granular anomaly identification at the edge. Simultaneously, the maturation of machine learning algorithms—particularly unsupervised learning, autoencoders, and transformer-based architectures—has dramatically improved detection accuracy while reducing false-positive rates that historically undermined analyst confidence.

From a demand-side perspective, the BFSI sector remains the single largest end-use vertical, leveraging anomaly detection to combat fraud, money laundering, and insider threats in real time. Healthcare organizations are increasingly deploying these solutions for clinical data integrity and medical device security. Manufacturing enterprises use them for predictive maintenance and production quality assurance.

North America commands the largest revenue share globally, supported by a mature cybersecurity ecosystem, high enterprise IT spending, and a dense concentration of solution vendors. Asia Pacific is emerging as the fastest-growing regional market, propelled by rapid digitization in China, India, and Southeast Asian economies. Europe maintains steady growth underpinned by stringent data protection regulations.

Looking ahead, the integration of generative AI capabilities into anomaly detection pipelines, combined with the expansion of managed detection and response (MDR) services, will reshape the competitive landscape. Vendors that can deliver explainable AI outputs—allowing human analysts to understand and validate anomaly flags—will command premium positioning. The market is poised to surpass $20 billion by the early 2030s, with the next three years serving as a critical inflection point for platform consolidation and cross-domain analytics integration.

Within the Anomaly Detection Market, network behavior anomaly detection (NBAD) constitutes the dominant solution type by revenue share, accounting for the majority of deployments across enterprise, government, and critical infrastructure environments. This dominance is attributable to a combination of structural factors: the network layer remains the primary attack surface for external threat actors, it generates the highest density of observable data points, and it serves as the common integration plane across heterogeneous IT and OT environments.

NBAD solutions operate by establishing behavioral baselines for network traffic—volume, protocol distribution, peer communication patterns, and session duration—then flagging deviations that may indicate data exfiltration, lateral movement, command-and-control beaconing, or distributed denial-of-service activity. Unlike signature-based intrusion detection systems, NBAD does not require prior knowledge of specific attack patterns, making it particularly effective against novel threats and insider abuse.

The dominance of this segment is reinforced by the explosive growth of hybrid and multi-cloud network architectures, which dramatically expand the attack surface and make traditional perimeter-based defenses insufficient. Organizations now require visibility across on-premises data centers, public cloud workloads, and edge computing nodes simultaneously, driving demand for solutions capable of correlating telemetry across disparate environments in real time.

Key players leading within the NBAD segment include Cisco Systems, Inc., which leverages its deep network infrastructure footprint to deliver embedded anomaly detection through its Stealthwatch and SecureX platforms. IBM Corporation has integrated NBAD capabilities into its QRadar Security Intelligence platform, using machine learning to reduce alert fatigue. Securonix, Inc. applies advanced behavioral analytics to network data using UEBA (User and Entity Behavior Analytics) frameworks. Splunk, Inc. provides network telemetry ingestion and correlation at scale through its SIEM infrastructure. Symantec Corporation offers network threat protection as part of its integrated endpoint and network security portfolio.

The NBAD segment's share is not merely stable—it is actively consolidating. As enterprises rationalize their security vendor portfolios in response to budget pressures and analyst fatigue, they are gravitating toward comprehensive platforms that embed network anomaly detection alongside endpoint detection, identity analytics, and cloud security posture management. This platform consolidation dynamic favors incumbents with broad product suites over point-solution providers.

Technology investment within NBAD is increasingly focused on unsupervised machine learning models that can adapt to evolving network baselines without manual retraining cycles, as well as graph neural networks capable of mapping complex peer-to-peer communication topologies to identify subtle lateral movement patterns. The integration of threat intelligence feeds—both commercial and open-source—into NBAD engines is further enhancing contextual enrichment and prioritization accuracy.

From a deployment perspective, cloud-native NBAD solutions delivered as SaaS are gaining share over on-premise appliances, particularly among mid-market enterprises that lack the internal resources to manage hardware-based network probes. This shift is accelerating as network traffic increasingly bypasses traditional demarcation points in favor of direct cloud-to-cloud and branch-to-cloud pathways. Vendors that can provide agentless, API-driven network visibility across major cloud providers—AWS, Azure, and Google Cloud—are capturing disproportionate market share within this dominant segment.

The Anomaly Detection Market is shaped by a set of measurable, interconnected drivers and constraints that together define its growth trajectory and structural dynamics.

Escalating Cybersecurity Incidents: According to industry reporting, global cybercrime costs are projected to exceed $10.5 trillion annually by 2025, up from $3 trillion in 2015. This staggering figure encompasses ransomware payouts, regulatory fines, incident response costs, and reputational damage. The direct correlation between breach frequency and anomaly detection investment is well established: every high-profile breach that escapes signature-based defenses validates the business case for behavioral analytics.

Regulatory Compliance Mandates: The enforcement of GDPR since 2018 has imposed cumulative fines exceeding €4 billion on organizations found to have inadequate data protection mechanisms. HIPAA enforcement actions in the United States healthcare sector reached record levels in 2023, with settlements totaling hundreds of millions of dollars. These regulatory pressures create a non-discretionary demand category for anomaly detection, particularly in BFSI and healthcare verticals.

Proliferation of IoT Endpoints: Analyst projections place the number of active IoT connections at over 27 billion globally by 2025, each representing a potential anomaly source and threat vector. Manufacturing, energy, and smart city deployments are particularly exposed, driving procurement of operational technology (OT) anomaly detection capabilities.

AI and ML Algorithm Maturation: The widespread availability of pre-trained foundation models and AutoML frameworks has dramatically lowered the development cost of high-accuracy anomaly detection models, enabling smaller vendors and in-house teams to deploy competitive solutions.

Key Constraints: The primary restraint is the chronic shortage of skilled cybersecurity professionals—estimated at a global deficit of 3.5 million positions—which limits the operational capacity to act on anomaly detection outputs. Additionally, high false-positive rates in immature deployments generate analyst fatigue, leading to alert dismissal and reduced effectiveness. Data privacy regulations in certain jurisdictions also restrict the collection of the granular behavioral data that NBAD solutions require, creating geographic deployment limitations.

The Anomaly Detection Market features a diverse competitive ecosystem ranging from global technology conglomerates to specialized cybersecurity pure-plays. Below is a structured profile of key participants:

Splunk, Inc.: A leader in security information and event management (SIEM), Splunk delivers anomaly detection through its Enterprise Security and UEBA modules, processing petabyte-scale machine data with real-time behavioral analytics capabilities.

Guardian Analytics: Specializes in behavioral analytics for financial fraud detection, offering cloud-based solutions that model individual customer behavior to identify account takeover and payment fraud anomalies in real time.

Happiest Minds: An IT services and consulting firm that provides anomaly detection implementation services, particularly for mid-market enterprises in BFSI and healthcare, leveraging partnerships with leading platform vendors.

IBM Corporation: Through its QRadar platform and Watson AI capabilities, IBM delivers end-to-end anomaly detection across network, user, and application layers, with deep integration into its broader security operations center (SOC) ecosystem.

Hewlett Packard Enterprise Company: HPE's ArcSight platform provides network and user behavior anomaly detection for large enterprise and government clients, with strong on-premise deployment capabilities and compliance reporting features.

Trend Micro, Inc.: Integrates anomaly detection into its XDR (Extended Detection and Response) platform, providing correlated threat visibility across email, endpoint, server, cloud, and network vectors.

Cisco Systems, Inc.: Leverages its dominant networking infrastructure position to embed anomaly detection natively into network devices and cloud platforms, offering Encrypted Traffic Analytics (ETA) that identifies threats without decryption.

SAS Institute, Inc.: Provides advanced analytics and machine learning-based anomaly detection solutions with particular strength in financial services fraud analytics and healthcare claims anomaly identification.

Securonix, Inc.: A cloud-native SIEM and UEBA specialist, Securonix applies entity behavior analytics with long-term threat detection timelines, enabling identification of slow-moving insider threats that evade conventional rules-based systems.

Symantec Corporation: Now operating under Broadcom, Symantec delivers network and endpoint anomaly detection as part of its integrated enterprise security platform, with significant installed base in Fortune 500 organizations.

Wipro Limited: Provides anomaly detection as part of its managed security services portfolio, offering co-managed SOC capabilities that include behavioral analytics deployment and tuning for global enterprise clients.

Dell Technologies, Inc.: Integrates anomaly detection within its infrastructure security offerings, particularly for hybrid cloud environments, leveraging its hardware telemetry capabilities for OT and data center anomaly identification.

Gurucul: A specialized behavioral analytics vendor offering cloud-native UEBA and SIEM solutions with advanced machine learning models designed for insider threat detection and privileged account abuse identification.

January 2024: IBM Corporation announced the integration of generative AI-powered anomaly summarization into QRadar SIEM, enabling natural language explanations of detected behavioral anomalies to reduce analyst investigation time by an estimated 40%.

March 2024: Cisco Systems, Inc. completed its acquisition of Splunk, Inc. in a landmark $28 billion transaction, creating one of the largest security and observability platforms globally and consolidating significant anomaly detection capabilities under a single vendor umbrella.

June 2024: Securonix, Inc. launched its Autonomous Threat Sweeper (ATS) capability, incorporating unsupervised machine learning models that continuously re-evaluate historical log data against new threat intelligence without analyst intervention.

September 2023: The European Union's NIS2 Directive entered into force, expanding mandatory cybersecurity incident detection requirements to additional critical infrastructure sectors across EU member states, directly stimulating procurement of anomaly detection solutions.

November 2023: Gurucul raised a strategic funding round to accelerate its cloud SIEM and behavioral analytics platform expansion, targeting mid-market enterprises in North America and Europe.

February 2025: SAS Institute, Inc. unveiled enhanced anomaly detection modules within its Viya platform, embedding real-time streaming analytics capable of processing over 1 million events per second for high-frequency financial transaction monitoring.

April 2025: Trend Micro, Inc. announced a strategic partnership with a major hyperscaler to deliver cloud-native XDR anomaly detection as a managed service, targeting Asia Pacific enterprise clients across manufacturing and BFSI verticals.

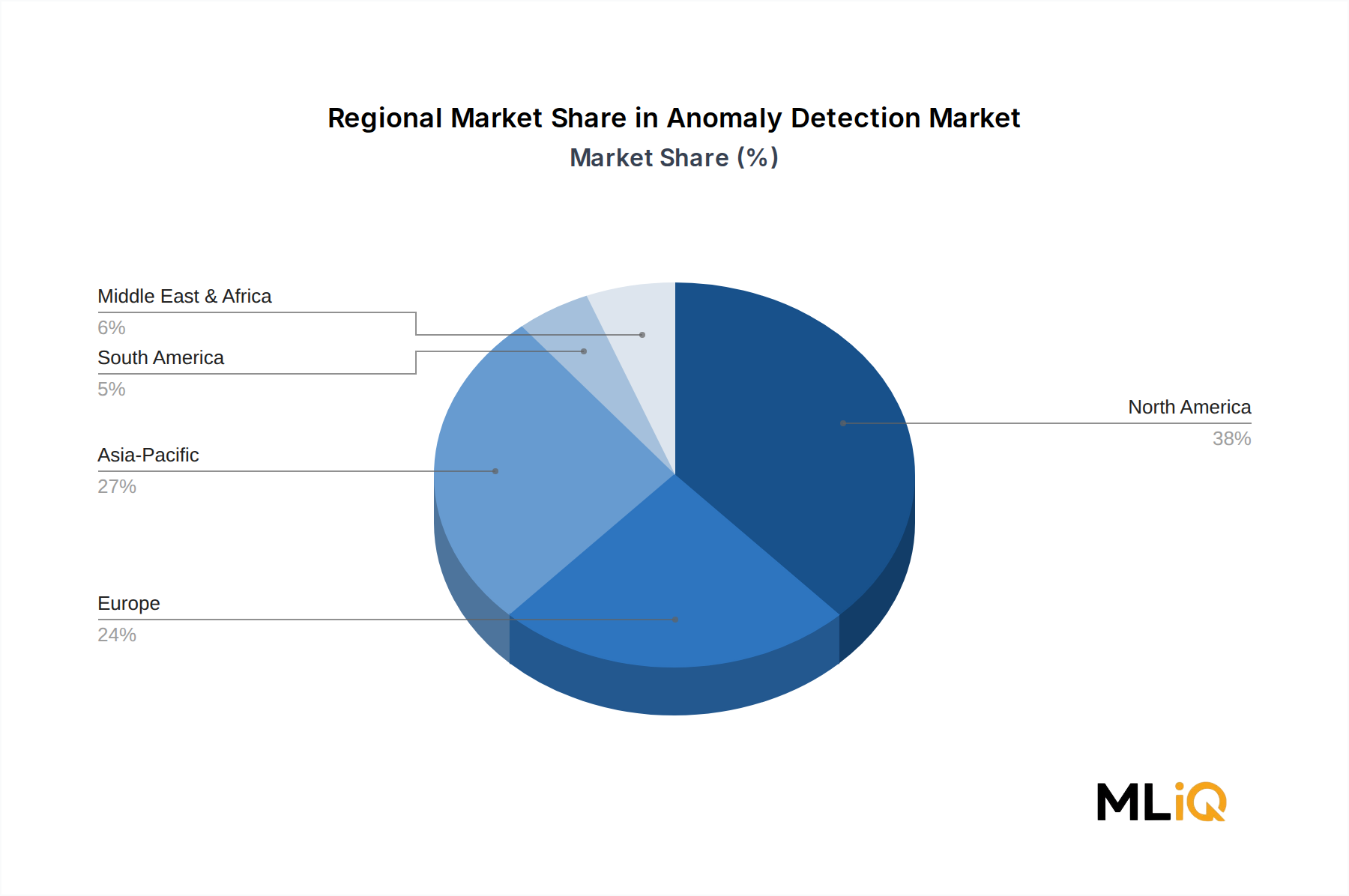

The Anomaly Detection Market exhibits pronounced regional heterogeneity in terms of maturity, growth velocity, and demand composition.

North America: North America accounts for the largest regional revenue share, estimated at approximately 38–40% of global market value in 2025. The United States is the primary contributor, driven by high enterprise IT security budgets, a mature managed security service provider (MSSP) ecosystem, and the concentration of major solution vendors including Splunk, Securonix, IBM, and Cisco. Canada and Mexico contribute incremental growth through cross-border enterprise deployments and nearshore IT services expansion. North America's regional CAGR is estimated at 14%, reflecting market maturity rather than deceleration.

Asia Pacific: The fastest-growing regional market, Asia Pacific is projected to expand at a CAGR of 19–21% through the forecast period. China's state-driven cybersecurity initiatives, India's digital infrastructure buildout under programs such as Digital India, and the rapid enterprise cloud adoption across ASEAN economies collectively drive demand. Japan and South Korea contribute through their advanced manufacturing and semiconductor sectors, where OT anomaly detection is a critical operational requirement.

Europe: Europe maintains steady growth at an estimated CAGR of 15%, underpinned by GDPR enforcement, NIS2 compliance mandates, and increasing defense-sector investment in cyber threat detection. Germany, the United Kingdom, and France lead regional adoption. The Nordics are notable for high per-capita cybersecurity investment relative to enterprise size.

Middle East & Africa: This region is experiencing accelerating adoption, particularly across GCC nations investing in smart city infrastructure and financial sector digitization. Israel maintains a disproportionate concentration of anomaly detection technology innovation relative to its market size. Regional CAGR is estimated at 17%.

South America: Brazil and Argentina represent the primary markets, with adoption concentrated in BFSI and government sectors. Regional growth is constrained by economic volatility but supported by increasing regulatory focus on data protection. CAGR is estimated at 13%.

The Anomaly Detection Market is predominantly a software and services market, meaning that traditional physical trade flows are less directly applicable than in hardware-intensive segments. Nonetheless, meaningful cross-border economic dynamics shape vendor revenue distribution, talent flows, and deployment patterns.

The United States is the dominant exporter of anomaly detection software platforms and intellectual property, with major vendors generating substantial export revenue from European, Asia Pacific, and Middle Eastern enterprise customers. U.S.-origin SaaS platforms account for an estimated 55–60% of globally deployed anomaly detection software licenses.

Export Control Implications: Certain advanced anomaly detection technologies—particularly those incorporating AI-driven behavioral analytics with dual-use potential—fall within the scope of U.S. Export Administration Regulations (EAR) and Bureau of Industry and Security (BIS) oversight. Export license requirements for specific AI software components to controlled destinations impose compliance costs and deployment delays, particularly affecting sales into China and certain Middle Eastern markets.

Data Localization Barriers: Non-tariff barriers in the form of data residency and localization requirements represent significant trade friction. The European Union's GDPR data transfer restrictions, Russia's data localization law, and China's Data Security Law collectively constrain the cross-border flow of behavioral telemetry data that cloud-based anomaly detection platforms depend upon. Vendors address these barriers through regional cloud infrastructure investments—establishing local data processing nodes in Frankfurt, Singapore, Mumbai, and São Paulo.

India's IT Services Export Role: India functions as a significant exporter of anomaly detection implementation and managed services, with firms such as Wipro Limited and Happiest Minds delivering global deployments from Indian delivery centers. This services trade flow is subject to H-1B visa restrictions and domestic tax treatment changes that periodically affect delivery economics.

Tariff Environment: Direct import tariffs on

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 16% from 2020-2034 |

| Segmentation |

|

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Comprehensive validation mechanisms ensuring market intelligence accuracy, reliability, and adherence to international standards.

500+ data sources cross-validated

200+ industry specialists validation

NAICS, SIC, ISIC, TRBC standards

Continuous market tracking updates

Factors such as are projected to boost the Anomaly Detection Market market expansion.

Key companies in the market include Splunk, Inc., Guardian Analytics, Happiest Minds, IBM Corporation, Hewlett Packard Enterprise Company, Trend Micro, Inc., Cisco Systems, Inc., SAS Institute, Inc., Securonix, Inc., Symantec Corporation, Wipro Limited, Dell Technologies, Inc., Gurucul.

The market segments include Component, Deployment Type, Enterprise Size, Industry Vertical, Solution Type, Service Type, Technology.

The market size is estimated to be USD 7.4 billion as of 2022.

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3690, USD 5820, and USD 9870 respectively.

The market size is provided in terms of value, measured in billion and volume, measured in .

Yes, the market keyword associated with the report is "Anomaly Detection Market," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Anomaly Detection Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.