1. What are the major growth drivers for the E-Waste Management Market market?

Factors such as are projected to boost the E-Waste Management Market market expansion.

+1 2315155523

E-Waste Management Market

E-Waste Management Market

Market Lens IQ is a global market intelligence and strategic consulting firm delivering advanced syndicated research reports, customized industry analysis, competitive intelligence, and data-driven advisory solutions to organizations across international markets. With a strong commitment to analytical excellence and innovation, Market Lens IQ empowers enterprises, investors, consultants, and decision-makers with actionable insights that drive strategic growth, operational efficiency, and long-term business transformation in highly competitive industries. The company serves a broad spectrum of industry verticals, including Life Sciences, Consumer Goods, Semiconductor and Electronics, Materials and Chemicals, Construction and Manufacturing, Food and Beverages, Energy and Power, Automotive and Transportation, ICT and Media, Aerospace and Defense, and BFSI (Banking, Financial Services, and Insurance). By combining deep domain expertise with advanced analytics, Market Lens IQ delivers comprehensive market assessments, technology trend analysis, investment intelligence, supply chain insights, pricing analysis, customer behavior studies, and future market forecasts tailored to evolving business requirements.

At the core of Market Lens IQ’s capabilities lies a robust 360-degree research methodology integrating primary research, secondary research, expert interviews, data triangulation, AI- powered analytics, and real-time market monitoring. Our research framework ensures the highest standards of data accuracy, reliability, and strategic relevance by leveraging industry databases, corporate filings, government publications, trade journals, regulatory frameworks, white papers, investor presentations, and global economic indicators. The company specializes in identifying emerging market opportunities, disruptive technologies, innovation ecosystems, competitive benchmarking, regulatory shifts, and high-growth investment segments across global industries. Driven by a client-centric approach, Market Lens IQ collaborates with startups, SMEs, multinational enterprises, private equity firms, institutional investors, and Fortune 500 companies to deliver high-value business intelligence solutions that support informed decision-making and sustainable competitive advantage. Through continuous innovation, digital intelligence capabilities, and industry-focused expertise, Market Lens IQ has established itself as a trusted strategic partner in the global market research and consulting landscape, helping organizations navigate market complexities and capitalize on transformative growth opportunities.

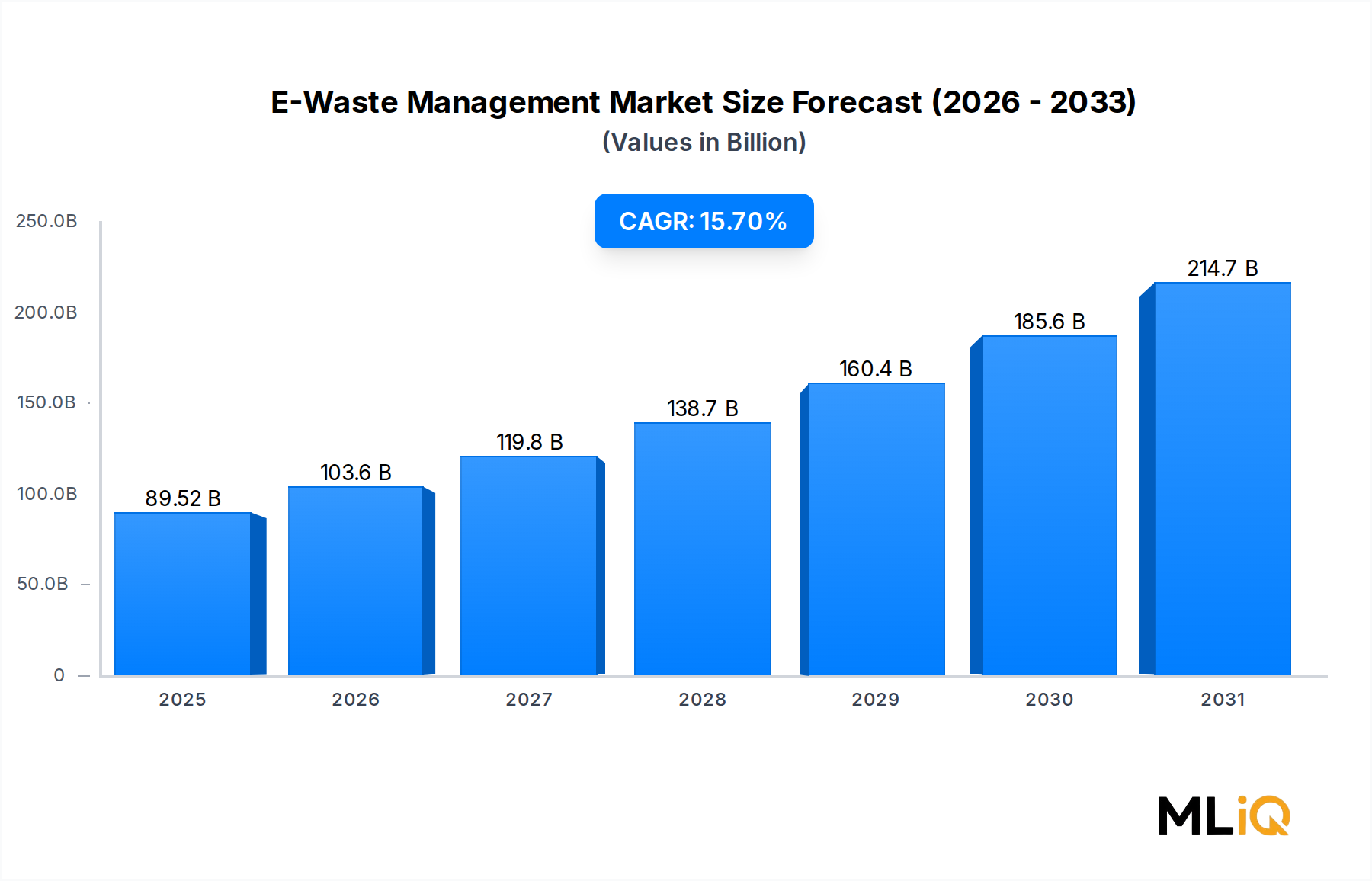

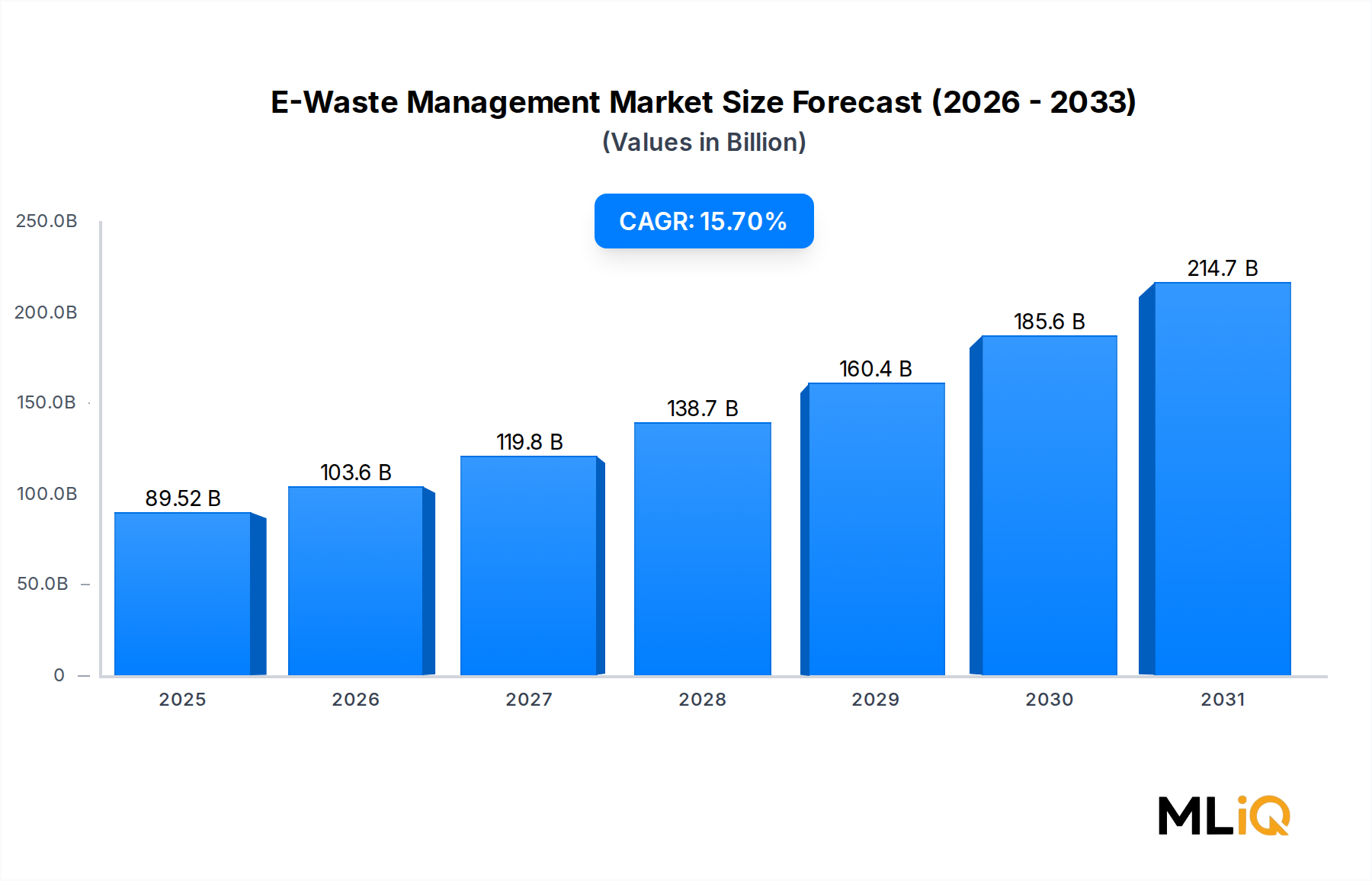

The global E-Waste Management Market is undergoing a period of accelerated structural transformation, driven by the convergence of regulatory mandates, surging consumer electronics penetration, and heightened awareness of critical material recovery. As of the base assessment period, the market is valued at $89.52 billion, with projections indicating a robust compound annual growth rate (CAGR) of 15.7% through the 2025–2033 forecast window. At this pace, the market is positioned to substantially surpass the $300 billion threshold by the terminal forecast year, cementing its status as one of the most consequential growth verticals within the ICT and Media sector.

Several macro tailwinds are reinforcing this trajectory. The proliferation of connected devices globally — including smartphones, laptops, wearables, and industrial IoT endpoints — is generating unprecedented volumes of discarded electronics. The International Telecommunication Union estimates that annual global e-waste generation has surpassed 60 million metric tonnes, yet formal recycling rates remain below 25%, underscoring the enormous latent opportunity. Governments across the European Union, North America, and the Asia Pacific region are tightening Extended Producer Responsibility (EPR) frameworks, compelling original equipment manufacturers to internalize end-of-life costs and fund certified recycling infrastructure.

Demand-side momentum is equally compelling. The transition to circular economy principles across enterprise supply chains is driving significant corporate investment in take-back programs and asset disposition services. Meanwhile, the financial value embedded in discarded electronics — particularly recoverable gold, silver, palladium, copper, and rare earth compounds — is incentivizing private-sector investment in advanced hydrometallurgical and pyrometallurgical recovery technologies.

From a segmentation standpoint, the recycled application sub-segment dominates revenue generation, reflecting the shift away from landfill disposal toward value-recovery processing. The metal material segment commands the largest share within the material taxonomy, underpinned by strong secondary commodity markets. Consumer electronics and household appliances represent the primary source type contributors, though industrial electronics waste is the fastest-growing sub-category.

Competitively, the market features a hybrid ecosystem of global environmental services conglomerates, specialized precious metal refiners, and vertically integrated recycling platforms. Strategic differentiation increasingly centers on technology capability — particularly in urban mining efficiency and data destruction certification — rather than geographic coverage alone. Looking ahead, the E-Waste Management Market is poised to evolve from a compliance-driven cost center into a strategic resource-recovery sector, with margin expansion opportunities concentrated among operators that can achieve high-purity material outputs at industrial scale.

Within the material segmentation of the E-Waste Management Market, the metal sub-segment commands the largest revenue share and exhibits the strongest margin profile across the value chain. Metals recoverable from discarded electronics — including copper, gold, silver, palladium, aluminum, and tin — represent the primary economic driver for recycling operators globally. Industry analyses consistently indicate that the metal segment accounts for approximately 40–45% of total material recovery revenue, a share that has been consolidating rather than diluting as commodity prices for critical metals trend upward.

The economic rationale for metal-centric recycling is compelling. A metric tonne of printed circuit boards can contain upward of 200–300 grams of gold, compared to roughly 5 grams per metric tonne in primary gold ore. This concentration differential, known as the urban mining premium, fundamentally underpins the financial viability of formal e-waste processing operations. As global primary ore grades continue to decline, the relative attractiveness of secondary metal sourcing from e-waste streams intensifies, creating a structural demand floor for certified recyclers operating at scale.

The dominance of the metal segment is further reinforced by the depth and liquidity of secondary commodity markets. Unlike recovered plastics or glass — which face quality degradation challenges and limited downstream buyer bases — secondary copper, gold, and silver are fungible commodities that trade at near-parity with primary equivalents when refined to LME-grade specifications. This market depth enables recyclers to hedge recovered material inventories using futures contracts, reducing revenue volatility and improving balance sheet predictability.

Key players with the greatest exposure to metal-dominant processing streams include Umicore, which operates one of the world's most sophisticated precious metal refining complexes in Hoboken, Belgium, capable of processing 350,000 tonnes of complex materials annually. Tetronics Technologies Limited specializes in plasma arc smelting systems that achieve exceptional metal recovery yields from low-grade e-waste fractions. Electronic Recyclers International focuses on integrated dismantling and shredding operations in North America, feeding downstream smelters with pre-processed metal-rich concentrates.

The metal segment's share is expected to consolidate further through the forecast period, driven by three reinforcing dynamics. First, the proliferation of electric vehicles and energy storage systems is generating a new wave of lithium-ion battery waste, introducing lithium, cobalt, nickel, and manganese into the recoverable metals taxonomy. Second, the geopolitical pressure to reduce dependence on primary critical mineral imports — particularly from China-dominated supply chains — is elevating government support for domestic secondary metal recovery programs in the United States, European Union, Japan, and South Korea. Third, advances in hydrometallurgical leaching and solvent extraction technologies are progressively improving recovery yields for platinum-group metals and rare earth elements that were previously uneconomical to extract from low-concentration e-waste fractions.

Plastic and glass sub-segments, while structurally important for volume throughput, generate substantially lower per-tonne revenue and face more complex downstream market dynamics. Glass from cathode ray tubes contains lead at concentrations exceeding 2 kg per unit, necessitating specialized handling and limiting resale optionality. Recovered plastics from e-waste are frequently contaminated with flame retardants, restricting their eligibility for food-contact or premium end-use applications. These material-specific constraints structurally entrench the metal segment's margin and revenue leadership within the E-Waste Management Market through at least 2033.

The E-Waste Management Market is shaped by a set of precisely quantifiable drivers and structural constraints that collectively determine its growth trajectory, investment attractiveness, and technological evolution.

Primary Driver — Regulatory Proliferation: The expansion of EPR legislation globally represents the single most powerful demand-creation force. The EU's revised Waste Electrical and Electronic Equipment (WEEE) Directive mandates collection rates of 65% of average electrical and electronic equipment placed on the market over the preceding three years. The United States has enacted state-level e-waste legislation in 25+ states, covering approximately 65% of the national population. China's Administration Measures on Pollution Prevention and Control of E-Waste directly incentivizes formal recycling through a fund-based subsidy mechanism.

Secondary Driver — Critical Mineral Supply Security: The European Commission's Critical Raw Materials Act designates 34 strategic raw materials, many of which are recoverable from e-waste streams. The United States Executive Order 14017 mandates domestic sourcing assessments for critical minerals including cobalt, lithium, and rare earths. These policy instruments translate directly into public funding streams for e-waste recycling infrastructure.

Tertiary Driver — Corporate Sustainability Commitments: Over 500 global corporations have committed to Science-Based Targets initiative (SBTi) pathways that explicitly include circular material use metrics. This is generating measurable contract volumes for certified e-waste processors.

Primary Constraint — Informal Sector Competition: Informal recycling operations in developing economies — particularly in South and Southeast Asia — process an estimated 40–50% of global e-waste volumes using hazardous open-burning and acid-bath techniques. These operations impose no labor, environmental, or health compliance costs, enabling them to outcompete formal recyclers on material acquisition pricing, particularly in regions with weak enforcement infrastructure.

Secondary Constraint — Logistics Cost Structure: The collection and transportation of diffuse, low-density e-waste streams represents a structurally high cost component, consuming an estimated 20–30% of total processing revenue for operators relying on consumer take-back programs. This constrains unit economics at lower collection density thresholds.

The competitive landscape of the E-Waste Management Market is characterized by a mix of multinational environmental services groups, specialized precious metal refiners, and regional integrated processors. Market share is increasingly determined by technological differentiation, certification breadth, and geographic processing network density.

SembCorp Industries: A Singapore-headquartered environmental and utilities conglomerate with significant industrial waste processing capabilities across Asia Pacific; its e-waste operations leverage integrated industrial park infrastructure to achieve logistics cost advantages.

TES Amm: One of Asia's largest technology lifecycle services providers, operating certified e-waste processing facilities across 20+ countries; the company differentiates through data security services bundled with hardware recycling, targeting enterprise and government clients.

Umicore: A Belgium-based materials technology and recycling group with world-class precious metal refining capabilities; Umicore's Battery Recycling unit is positioned to capture significant lithium-ion battery e-waste volumes as the EV fleet transitions to end-of-life, making it a key participant in the Secondary Precious Metals Market.

Enviro-Hub Holdings Ltd.: A Singapore-listed environmental services company specializing in precious metal recovery from printed circuit boards and spent catalysts; the company operates hydrometallurgical processing lines achieving high-purity gold and silver outputs.

WM Intellectual Property Holdings, LLC: The intellectual property arm associated with Waste Management's recycling operations; provides technology licensing and operational frameworks for e-waste stream integration within municipal solid waste systems.

Electronic Recyclers International: A leading U.S.-based electronics recycling company operating R2 and e-Stewards certified facilities; focuses on CRT glass processing, hard drive shredding, and bulk dismantling services for enterprise clients.

MRI Technologies: Specializes in the recycling of aerospace and defense electronics, with particular expertise in handling restricted and classified equipment under secure chain-of-custody protocols; serves a niche but high-margin government contractor segment.

Veolia: A global environmental services leader with integrated e-waste management capabilities embedded within its broader hazardous waste and industrial services divisions; operates across 45+ countries with strong EU regulatory compliance infrastructure.

Capital Environment Holdings Limited: A Hong Kong-listed environmental company with growing e-waste processing capacity in mainland China, benefiting directly from China's formal recycling fund subsidy system.

Tetronics Technologies Limited: A UK-based plasma treatment technology specialist providing high-temperature arc furnace systems for metal recovery from complex e-waste fractions; licenses technology to third-party processors globally.

January 2025: The European Commission published implementing regulations for the revised WEEE Directive, introducing digitalized producer registers and cross-border data-sharing requirements effective January 2026, directly affecting compliance costs for all EU-market participants.

February 2025: Umicore announced a capacity expansion of its Hoboken precious metals refinery, committing €150 million to increase battery recycling throughput capacity by 40% by 2027, reinforcing its position in secondary cathode material supply chains.

March 2025: The U.S. Environmental Protection Agency finalized updated hazardous waste export rules under the Basel Convention framework, restricting the export of untreated CRT glass and mixed e-waste to non-OECD countries, effectively raising compliance barriers for informal processors.

April 2025: Veolia signed a 10-year strategic partnership with a major European telecommunications operator for the collection, data destruction, and materials recovery of decommissioned network infrastructure, valued at an estimated €80 million over the contract term.

May 2025: India's Ministry of Environment, Forest and Climate Change notified amendments to the E-Waste Management Rules, mandating producer responsibility organization (PRO) registration for all electronics brands with annual turnover exceeding INR 10 crore, significantly expanding the formal recycling mandate.

June 2025: TES Amm announced the commissioning of a new automated dismantling facility in Singapore incorporating AI-powered component sorting technology capable of processing 5,000 tonnes per month, representing a 35% throughput increase over prior capacity.

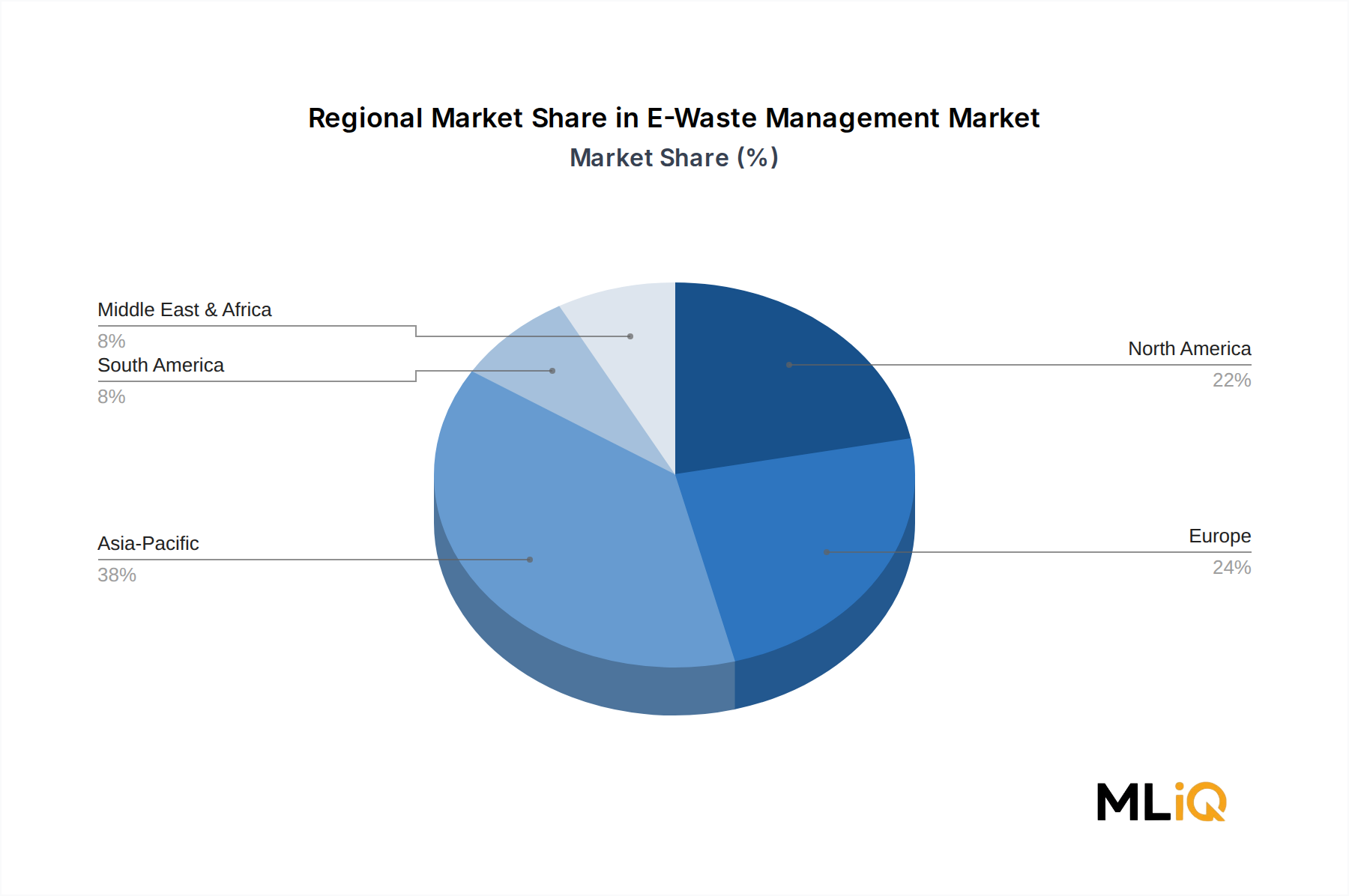

The E-Waste Management Market exhibits pronounced regional heterogeneity across regulatory maturity, infrastructure investment, and per-capita waste generation metrics.

Asia Pacific: The dominant regional market by both volume and increasingly by revenue, Asia Pacific accounts for an estimated 40–45% of global e-waste generation, driven by China, India, Japan, and South Korea. China's formal recycling subsidy fund has mobilized significant processing capacity, while India's amended e-waste rules are transitioning substantial informal volumes into the regulated sector. The region is projected to grow at a CAGR of approximately 17–18% through 2033, making it the fastest-growing geography globally. Key demand drivers include rapid urbanization, smartphone penetration exceeding 80% in urban centers, and national critical mineral security agendas.

Europe: The most mature regulatory market globally, with the WEEE Directive providing the world's most comprehensive producer responsibility framework. Europe generates approximately 12 million metric tonnes of e-waste annually, with formal collection rates averaging 35–40% across member states — the highest globally. The region is expected to grow at a CAGR of 12–13%, reflecting mature infrastructure offset by incremental regulatory tightening and rising battery e-waste volumes from EV adoption.

North America: The United States and Canada collectively represent a high-value market characterized by strong enterprise IT asset disposition demand and stringent data security requirements. The absence of a federal EPR framework in the U.S. creates regulatory fragmentation, though state-level legislation covers the majority of the population. North America is projected to grow at approximately 14–15% CAGR, with growth concentrated in certified processor capacity expansion and lithium battery recycling infrastructure.

Latin America: An emerging market with significant informal sector dominance, particularly in Brazil and Mexico. Formal e-waste recycling penetration remains below 15% regionally, but Brazil's National Solid Waste Policy is catalyzing infrastructure investment. The region is forecast at approximately 13–14% CAGR.

Middle East and Africa: The least mature formal market, yet the fastest-growing informal processing region. Sub-Saharan Africa receives significant volumes of improperly classified "second-hand" electronics that ultimately enter informal dismantling channels. Formal market development is nascent but accelerating in GCC nations, driven by smart city programs and sustainability mandates.

Pricing dynamics within the E-Waste Management Market are structurally bifurcated between upstream collection economics and downstream material recovery margins, with commodity cycle sensitivity serving as the primary volatility driver across both segments.

At the upstream collection tier, processors increasingly operate dual revenue models: charging service fees for data destruction and logistical collection, while simultaneously generating commodity revenue from recovered materials. Service fee structures have risen approximately 8–12% over the 2022–2024 period as enterprise clients intensify data security requirements, providing a partially non-cyclical revenue buffer against commodity price volatility.

Downstream material pricing is directly correlated with LME spot prices for copper, gold, silver, and palladium. The 2022–2023 commodity correction — during which gold temporarily declined from peak values and copper retraced from record highs — demonstrated margin compression of 15–20% at hydrometallurgical processing operators with limited hedging programs. Conversely, the 2024–2025 recovery in precious and industrial metal prices has restored processing margins toward historical averages.

Plastic and glass material streams continue to generate negative or near-zero margins at the material level, with revenue offset required from service fee income. This dynamic reinforces competitive consolidation, as smaller operators lacking sufficient service fee revenue cross-subsidization face structural margin erosion during commodity downturns.

The informal sector imposes structural pricing pressure on material acquisition. Informal collectors in price-sensitive markets offer higher per-kilogram acquisition prices than formal processors, subsidized by lower operational cost bases. This compresses formal operators' input material margins, particularly for consumer-sourced equipment with high-value component concentrations.

Looking forward, the integration of battery recycling streams — specifically lithium,

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 15.7% from 2020-2034 |

| Segmentation |

|

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Comprehensive validation mechanisms ensuring market intelligence accuracy, reliability, and adherence to international standards.

500+ data sources cross-validated

200+ industry specialists validation

NAICS, SIC, ISIC, TRBC standards

Continuous market tracking updates

Factors such as are projected to boost the E-Waste Management Market market expansion.

Key companies in the market include SembCorp Industries, TES Amm, Umicore, Enviro-Hub Holdings Ltd., WM Intellectual Property Holdings, LLC, Electronic Recyclers International, MRI Technologies, Veolia, Capital Environment Holdings Limited, Tetronics Technologies Limited.

The market segments include Material, Source Type, Application.

The market size is estimated to be USD 89.52 billion as of 2022.

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3570, USD 5730, and USD 9600 respectively.

The market size is provided in terms of value, measured in billion and volume, measured in .

Yes, the market keyword associated with the report is "E-Waste Management Market," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the E-Waste Management Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.