1. What are the major growth drivers for the Supplier Relationship Management Software Market market?

Factors such as are projected to boost the Supplier Relationship Management Software Market market expansion.

Market Lens IQ is a global market intelligence and strategic consulting firm delivering advanced syndicated research reports, customized industry analysis, competitive intelligence, and data-driven advisory solutions to organizations across international markets. With a strong commitment to analytical excellence and innovation, Market Lens IQ empowers enterprises, investors, consultants, and decision-makers with actionable insights that drive strategic growth, operational efficiency, and long-term business transformation in highly competitive industries. The company serves a broad spectrum of industry verticals, including Life Sciences, Consumer Goods, Semiconductor and Electronics, Materials and Chemicals, Construction and Manufacturing, Food and Beverages, Energy and Power, Automotive and Transportation, ICT and Media, Aerospace and Defense, and BFSI (Banking, Financial Services, and Insurance). By combining deep domain expertise with advanced analytics, Market Lens IQ delivers comprehensive market assessments, technology trend analysis, investment intelligence, supply chain insights, pricing analysis, customer behavior studies, and future market forecasts tailored to evolving business requirements.

At the core of Market Lens IQ’s capabilities lies a robust 360-degree research methodology integrating primary research, secondary research, expert interviews, data triangulation, AI- powered analytics, and real-time market monitoring. Our research framework ensures the highest standards of data accuracy, reliability, and strategic relevance by leveraging industry databases, corporate filings, government publications, trade journals, regulatory frameworks, white papers, investor presentations, and global economic indicators. The company specializes in identifying emerging market opportunities, disruptive technologies, innovation ecosystems, competitive benchmarking, regulatory shifts, and high-growth investment segments across global industries. Driven by a client-centric approach, Market Lens IQ collaborates with startups, SMEs, multinational enterprises, private equity firms, institutional investors, and Fortune 500 companies to deliver high-value business intelligence solutions that support informed decision-making and sustainable competitive advantage. Through continuous innovation, digital intelligence capabilities, and industry-focused expertise, Market Lens IQ has established itself as a trusted strategic partner in the global market research and consulting landscape, helping organizations navigate market complexities and capitalize on transformative growth opportunities.

+1 2315155523

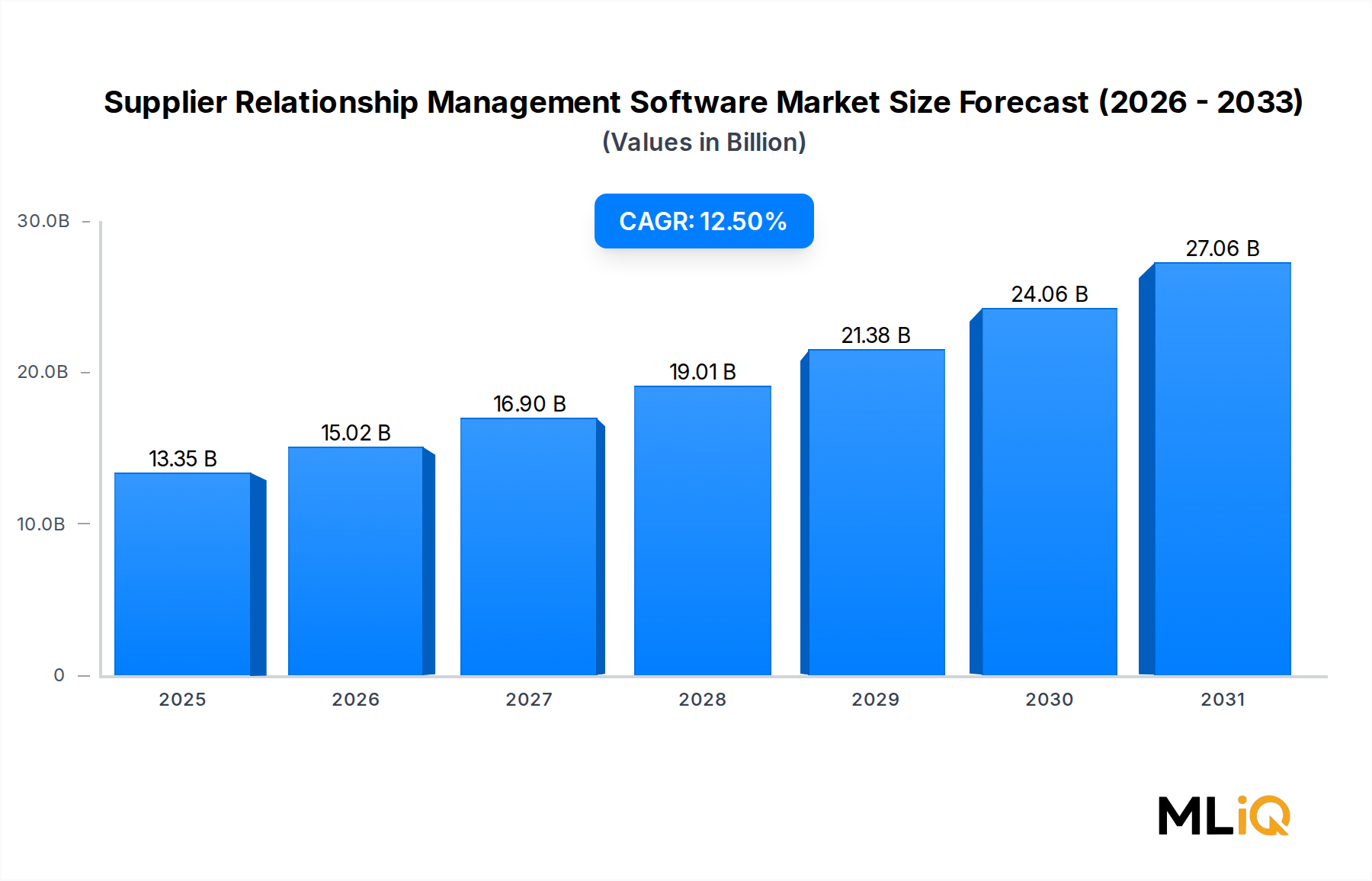

The global Supplier Relationship Management Software Market is valued at $13.35 billion in 2025 and is projected to expand at a compound annual growth rate of 12.5% through 2033, reaching an estimated valuation of approximately $34.1 billion by the end of the forecast period. This sustained growth trajectory reflects a structural shift in how organizations perceive supplier networks — transitioning from transactional engagements to strategic, data-driven partnerships that underpin operational resilience and competitive differentiation.

The primary demand catalyst is the intensifying pressure on enterprises to build supply chain agility in the aftermath of global disruptions that exposed the fragility of single-source and geographically concentrated procurement models. Organizations across manufacturing, retail, automotive, and BFSI verticals are deploying supplier relationship management platforms to centralize supplier data, automate performance scoring, track compliance obligations, and enable proactive risk mitigation — capabilities that are no longer viewed as discretionary investments but as operational imperatives.

Macro tailwinds reinforcing this expansion include accelerating digital transformation initiatives, rising regulatory scrutiny around supply chain transparency (notably the EU Corporate Sustainability Due Diligence Directive and U.S. supply chain disclosure mandates), and the proliferation of cloud-native deployment architectures that dramatically reduce time-to-value and total cost of ownership. The convergence of artificial intelligence and machine learning into supplier scoring, anomaly detection, and predictive analytics is further differentiating next-generation platforms from legacy solutions, creating premium pricing opportunities for technology vendors with mature AI roadmaps.

On the demand side, large enterprises continue to dominate adoption, driven by complex, multi-tier supplier networks that require sophisticated orchestration. However, small and medium-sized enterprises represent the fastest-growing buyer cohort as cloud deployment models eliminate historical barriers related to capital expenditure and IT infrastructure complexity. The ongoing convergence of supplier relationship management functionality with adjacent domains — including the Procurement Management Software Market, the Spend Analytics Software Market, and the Contract Lifecycle Management Software Market — is creating powerful suite-based value propositions that increase platform stickiness and average contract values.

Geographically, North America holds the largest revenue share, supported by early enterprise technology adoption and a dense ecosystem of established vendors. Asia Pacific is the fastest-growing region, with digital procurement transformation accelerating in China, India, and ASEAN economies. Looking ahead through 2033, the market is expected to benefit from continued platform consolidation, increased public sector adoption, and the growing integration of supplier relationship management capabilities within broader Supply Chain Management Software Market ecosystems. The outlook remains firmly constructive, with demand exceeding supply-side capacity for skilled implementation partners in several high-growth corridors.

Within the segmentation framework of the Supplier Relationship Management Software Market, deployment mode stands as a foundational dimension, and the cloud segment has emerged as the unambiguous revenue leader — accounting for a dominant share of total market billings in 2025 and continuing to widen its lead over on-premise alternatives. This dominance is structural rather than cyclical, rooted in a convergence of economic, operational, and strategic factors that align with the procurement transformation agenda of modern enterprises.

Cloud-based supplier relationship management platforms offer immediate and compelling advantages over traditional on-premise deployments. Foremost among these is the elimination of upfront capital expenditure for hardware, database licensing, and dedicated IT operations staff. In a procurement environment where finance leaders are scrutinizing technology ROI with increasing rigor, the subscription-based, opex-aligned cost model of cloud platforms resonates strongly across enterprise segments. Implementation timelines are also substantially compressed — cloud deployments typically go live in weeks rather than months, a critical consideration for organizations seeking rapid capability deployment in response to supply chain disruptions or compliance deadlines.

Scalability is a second structural advantage that cloud deployment delivers without equivalent investment friction. As organizations expand their supplier bases — whether through organic growth, mergers and acquisitions, or geographic diversification — cloud platforms scale seamlessly to accommodate thousands of additional supplier profiles, transaction records, and performance data points without requiring infrastructure re-architecture. This elasticity is particularly valuable in industries such as automotive and retail, where supplier network complexity is a defining operational characteristic.

The integration architecture of cloud-native platforms represents a third competitive differentiator. Modern cloud-based supplier relationship management solutions are built on open API frameworks that facilitate pre-built connectors to enterprise resource planning systems, e-procurement portals, logistics platforms, and external risk data feeds — enabling the real-time, bidirectional data flows that sophisticated supplier performance management requires. This connectivity advantage is difficult and costly to replicate in on-premise environments.

Key vendors driving cloud segment leadership include Oracle, Ariba (an SAP company), and Zycus Inc., each of which has made substantial investments in cloud-native architecture, AI-powered analytics, and mobile-accessible interfaces. Oracle's cloud suite integrates supplier relationship management with financial controls and compliance workflows, creating multi-functional value that justifies enterprise-tier pricing. Ariba's network-centric model leverages one of the world's largest supplier connectivity ecosystems, providing customers with pre-validated supplier data and benchmarking intelligence. Zycus Inc. has differentiated through its Merlin AI platform, which embeds machine learning across sourcing, procurement, and supplier management workflows.

The on-premise segment retains relevance in highly regulated industries such as defense, government procurement, and certain financial services verticals where data sovereignty, air-gapped security requirements, or existing ERP investment protection justify continued on-premise operation. However, even within these conservative buyer segments, hybrid cloud architectures — which maintain sensitive data processing on-premise while leveraging cloud infrastructure for analytics and collaboration — are gaining adoption, effectively blurring the categorical boundary.

The cloud segment's share is not merely stable — it is actively consolidating. Migration projects converting legacy on-premise deployments are generating a secondary wave of cloud billings on top of new greenfield implementations, a dynamic that sustains above-market growth rates for cloud-focused vendors and compresses the addressable market for on-premise specialists. Vendors that have failed to invest in credible cloud migration pathways are experiencing accelerating customer attrition, reinforcing the winner-take-most dynamics characteristic of enterprise SaaS markets. The trajectory strongly suggests that by 2033, cloud deployment will represent the overwhelming majority of total Supplier Relationship Management Software Market revenue.

The growth dynamics of the Supplier Relationship Management Software Market are governed by a well-defined set of quantifiable drivers and constraints that practitioners and investors must assess with precision.

Supply chain risk visibility has become the single most cited investment rationale for supplier relationship management platform adoption. Following the disruptions of 2020–2022, a majority of Fortune 500 procurement functions initiated formal supplier risk programs, creating urgent demand for platforms capable of aggregating financial health scores, geopolitical exposure data, ESG compliance metrics, and operational performance KPIs into unified supplier risk dashboards. This driver is durable because supply chain risk has been permanently re-rated as a board-level concern rather than an operational one.

Regulatory compliance pressure constitutes a second high-velocity driver. The EU's Corporate Sustainability Due Diligence Directive, scheduled for phased enforcement from 2026 onward, imposes legally binding supplier due diligence obligations on large enterprises operating in EU markets. Non-compliance penalties reach up to 5% of global net turnover, creating a compelling quantifiable ROI case for platforms that automate audit trails, supplier self-assessments, and corrective action workflows. Similar mandates are advancing in the United Kingdom, Australia, and Canada, creating a global compliance-driven procurement technology spending wave.

The integration of AI and machine learning represents the most transformative technology driver currently reshaping competitive positioning. Platforms incorporating predictive analytics for supplier financial distress scoring, NLP-powered contract risk extraction, and automated performance benchmarking command pricing premiums of 15%–25% relative to functionally equivalent platforms without AI capabilities, according to procurement technology research benchmarks.

On the constraint side, data quality and integration complexity remain the primary implementation friction points. Enterprises with fragmented ERP landscapes — common in organizations that have grown through acquisition — face multi-year data harmonization programs before supplier relationship management platforms can deliver their design-state analytical value. This extends payback periods and creates implementation abandonment risk that suppresses net-new adoption velocity among mid-market buyers. Additionally, vendor consolidation within the broader Enterprise Resource Planning Software Market is reshaping the competitive dynamics of standalone supplier relationship management vendors, as suite-based buyers deprioritize best-of-breed point solutions.

The competitive landscape of the Supplier Relationship Management Software Market is characterized by a mix of global enterprise software leaders, specialized procurement technology vendors, and emerging AI-native challengers competing across deployment model, vertical specialization, and functional depth dimensions.

Biznet Solutions: Provides configurable supplier management and procurement workflow automation tools, primarily serving mid-market enterprises in North America and Latin America with rapid-deployment cloud modules.

JDA Software Group, Inc.: Leverages its deep supply chain planning heritage to position supplier relationship management as an integrated component of end-to-end supply chain visibility suites, with particular strength in retail and consumer goods verticals.

Intelex Technologies Inc.: Differentiates through its focus on quality management and environmental, health, and safety compliance integration within supplier management workflows, serving regulated manufacturing and industrial sectors.

Ariba, Inc.: Operates as the network-centric market leader with one of the largest supplier connectivity ecosystems globally, offering customers pre-validated supplier data, benchmarking intelligence, and deep SAP ERP integration as structural competitive moats.

Zycus Inc.: Competes on AI-driven procurement intelligence through its Merlin AI platform, which spans sourcing, contract management, accounts payable, and supplier performance management in a unified suite targeting large and mid-enterprise buyers.

Epicor Software Corporation: Addresses manufacturing and distribution sector buyer needs with supplier management capabilities tightly embedded within its industry-specific ERP and supply chain platforms, reducing integration friction for existing Epicor customers.

DXC Technology Company: Brings systems integration scale and managed services capabilities to large enterprise supplier management transformation programs, often serving as a strategic implementation and outsourcing partner for complex multi-ERP environments.

Determine, Inc.: Provides contract and supplier management platform capabilities with a modular architecture designed to enable phased adoption, targeting procurement organizations seeking incremental digital transformation pathways.

Oracle: Competes at the enterprise tier with a deeply integrated supplier management cloud suite that connects procurement, financial controls, supply chain planning, and compliance workflows within a unified data model, supporting global multi-entity deployments.

NEOCASE SOFTWARE: Focuses on shared services and HR-adjacent supplier management workflows, bringing process automation and case management capabilities to procurement service delivery functions within large enterprises.

January 2025: Oracle announced an expanded AI capabilities roadmap for its Fusion Cloud Procurement suite, incorporating generative AI-powered supplier risk summarization and automated compliance scoring features targeted at enterprise procurement teams managing thousands of active supplier relationships.

February 2025: Zycus Inc. completed a significant product integration update connecting its Merlin AI supplier risk module with third-party ESG data providers, enabling real-time supplier sustainability scoring against GRI and CDP reporting frameworks within the procurement workflow.

March 2025: The European Commission issued updated guidance on supplier due diligence documentation requirements under the Corporate Sustainability Due Diligence Directive framework, triggering accelerated procurement technology evaluation cycles among European multinationals.

April 2025: DXC Technology Company announced a strategic partnership with a leading cloud hyperscaler to deploy managed supplier relationship management transformation programs for public sector and defense procurement organizations across North America and Europe.

May 2025: Ariba, Inc. expanded its supplier network onboarding automation capabilities, reducing average supplier registration cycle times and improving data completeness scores, directly addressing one of the most frequently cited implementation friction points among enterprise buyers in the Supplier Relationship Management Software Market.

June 2025: Intelex Technologies Inc. launched an enhanced supplier quality audit module with mobile-first inspection workflows and AI-assisted non-conformance root cause analysis, targeting automotive and aerospace manufacturer quality procurement functions.

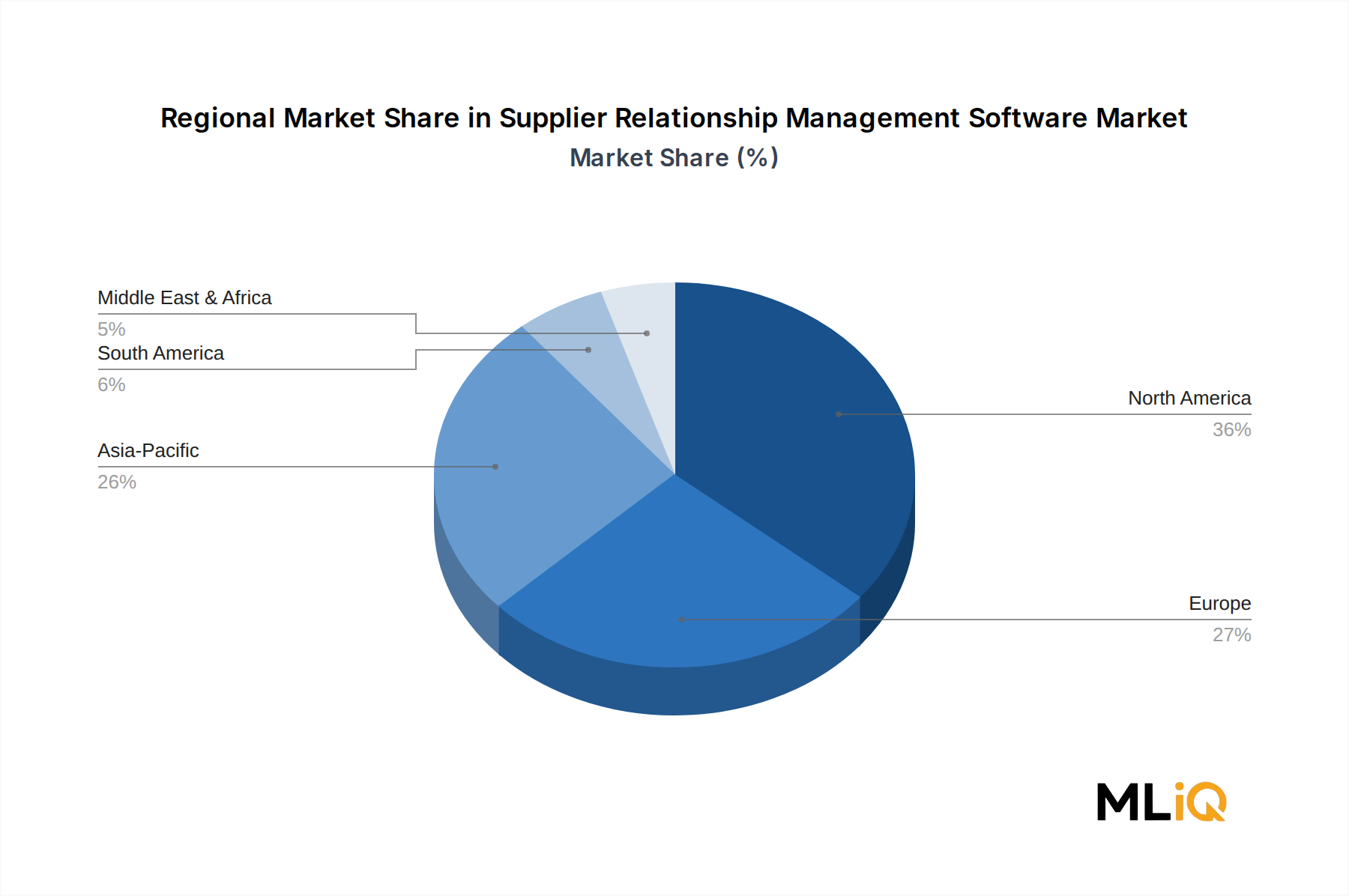

Regional dynamics within the Supplier Relationship Management Software Market reveal a clear bifurcation between mature, high-penetration markets in North America and Europe, and high-velocity growth corridors in Asia Pacific and the Middle East.

North America commands the largest regional revenue share, estimated at approximately 38% of global market value in 2025, reflecting the region's early enterprise technology adoption cycles, the concentration of Global 2000 procurement headquarters, and the dense local ecosystem of specialized implementation partners. The United States is the dominant national market within the region, driven by large-scale digital procurement transformation programs in manufacturing, retail, BFSI, and healthcare verticals. Canada contributes meaningfully through resource sector and government procurement technology investments, while Mexico is an emerging adoption center tied to nearshoring-driven supply chain complexity.

Europe represents the second-largest regional market, with a revenue share of approximately 28% in 2025. The region's growth is uniquely catalyzed by regulatory compliance pressure — specifically the EU Corporate Sustainability Due Diligence Directive and the German Supply Chain Due Diligence Act (LkSG), which have elevated supplier management technology from operational to legal necessity for enterprises headquartered or operating in EU jurisdictions. Germany, France, and the United Kingdom are the leading national markets. The region's CAGR through 2033 is estimated at 11.2%, slightly below global average due to relative market maturity.

Asia Pacific is the fastest-growing regional market, with a projected CAGR of 15.8% through 2033, driven by accelerating digital procurement adoption in China, India, South Korea, and ASEAN economies. China's manufacturing sector digitization programs and India's GST-compliant procurement infrastructure investments are generating substantial greenfield demand. Japan and South Korea contribute premium-tier enterprise adoption, particularly in automotive and electronics supply chain applications. The region's revenue share is expected to surpass Europe's by 2030 on current trajectory.

The Middle East and Africa region, led by GCC countries investing in economic diversification programs, is experiencing above-average CAGR of approximately 13.4% through 2033, with government-mandated supplier development programs driving public sector procurement technology investment. South America, anchored by Brazil and Argentina, represents a smaller but growing market, with adoption primarily concentrated in manufacturing and agribusiness supply chain applications.

Pricing structures within the Supplier Relationship Management Software Market have undergone significant evolution as the deployment mix has shifted toward cloud-based subscription models, fundamentally altering revenue recognition patterns, competitive pricing benchmarks, and margin profiles across the vendor ecosystem.

For cloud-based platforms, pricing is predominantly structured on a per-user per-month or per-managed-supplier per-year basis, with enterprise-tier contracts typically negotiated as multi-year committed annual recurring revenue arrangements. Average contract values for large enterprise deployments range from $150,000 to $1.2 million annually, depending on functional scope, user count, managed supplier volume, and the depth of AI and analytics capabilities included. Mid-market deployments typically price in the $30,000–$150,000 annual range, a segment experiencing intensifying competitive pressure as an expanding set of vendors targets procurement digitization budgets.

Margin dynamics vary materially across the value chain. Pure-play software vendors with cloud-native architectures and high subscription renewal rates command gross margins in the 70%–80% range, reflecting the operating leverage inherent in SaaS delivery models. However, net margin realization is significantly compressed by customer acquisition costs, which remain elevated due to long enterprise procurement evaluation cycles, high implementation complexity, and intense competition for a limited pool of procurement technology decision-makers.

Implementation services — provided either directly by vendors or through a certified partner ecosystem — create a secondary margin dynamic. Professional services engagements carry gross margins of 20%–35%, diluting blended company margins for vendors with high services attach rates. Vendors that successfully shift implementation volume to system integrator partners can protect software margins while scaling total implementation capacity. The Vendor Management Software Market and the E-Procurement Software Market face similar margin compression dynamics as competitive intensity increases.

Commodity and infrastructure cost cycles affect the underlying cost structures of cloud platform operators primarily through hyperscaler compute and storage pricing, which has exhibited a long-term deflationary trend of approximately 20%–30% per unit per year, partially offsetting the

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 12.5% from 2020-2034 |

| Segmentation |

|

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Comprehensive validation mechanisms ensuring market intelligence accuracy, reliability, and adherence to international standards.

500+ data sources cross-validated

200+ industry specialists validation

NAICS, SIC, ISIC, TRBC standards

Continuous market tracking updates

Factors such as are projected to boost the Supplier Relationship Management Software Market market expansion.

Key companies in the market include Biznet Solutions, JDA Software Group, Inc., Intelex Technologies Inc., Ariba, Inc., Zycus Inc., Epicor Software Corporation, DXC Technology Company, Determine, Inc., Oracle, NEOCASE SOFTWARE.

The market segments include Deployment Mode, Enterprise Size, Industry Vertical.

The market size is estimated to be USD 13.35 billion as of 2022.

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3690, USD 5820, and USD 9870 respectively.

The market size is provided in terms of value, measured in billion and volume, measured in .

Yes, the market keyword associated with the report is "Supplier Relationship Management Software Market," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Supplier Relationship Management Software Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.