1. What are the major growth drivers for the Embedded Non-Volatile Memory Market market?

Factors such as are projected to boost the Embedded Non-Volatile Memory Market market expansion.

+1 2315155523

Market Lens IQ is a global market intelligence and strategic consulting firm delivering advanced syndicated research reports, customized industry analysis, competitive intelligence, and data-driven advisory solutions to organizations across international markets. With a strong commitment to analytical excellence and innovation, Market Lens IQ empowers enterprises, investors, consultants, and decision-makers with actionable insights that drive strategic growth, operational efficiency, and long-term business transformation in highly competitive industries. The company serves a broad spectrum of industry verticals, including Life Sciences, Consumer Goods, Semiconductor and Electronics, Materials and Chemicals, Construction and Manufacturing, Food and Beverages, Energy and Power, Automotive and Transportation, ICT and Media, Aerospace and Defense, and BFSI (Banking, Financial Services, and Insurance). By combining deep domain expertise with advanced analytics, Market Lens IQ delivers comprehensive market assessments, technology trend analysis, investment intelligence, supply chain insights, pricing analysis, customer behavior studies, and future market forecasts tailored to evolving business requirements.

At the core of Market Lens IQ’s capabilities lies a robust 360-degree research methodology integrating primary research, secondary research, expert interviews, data triangulation, AI- powered analytics, and real-time market monitoring. Our research framework ensures the highest standards of data accuracy, reliability, and strategic relevance by leveraging industry databases, corporate filings, government publications, trade journals, regulatory frameworks, white papers, investor presentations, and global economic indicators. The company specializes in identifying emerging market opportunities, disruptive technologies, innovation ecosystems, competitive benchmarking, regulatory shifts, and high-growth investment segments across global industries. Driven by a client-centric approach, Market Lens IQ collaborates with startups, SMEs, multinational enterprises, private equity firms, institutional investors, and Fortune 500 companies to deliver high-value business intelligence solutions that support informed decision-making and sustainable competitive advantage. Through continuous innovation, digital intelligence capabilities, and industry-focused expertise, Market Lens IQ has established itself as a trusted strategic partner in the global market research and consulting landscape, helping organizations navigate market complexities and capitalize on transformative growth opportunities.

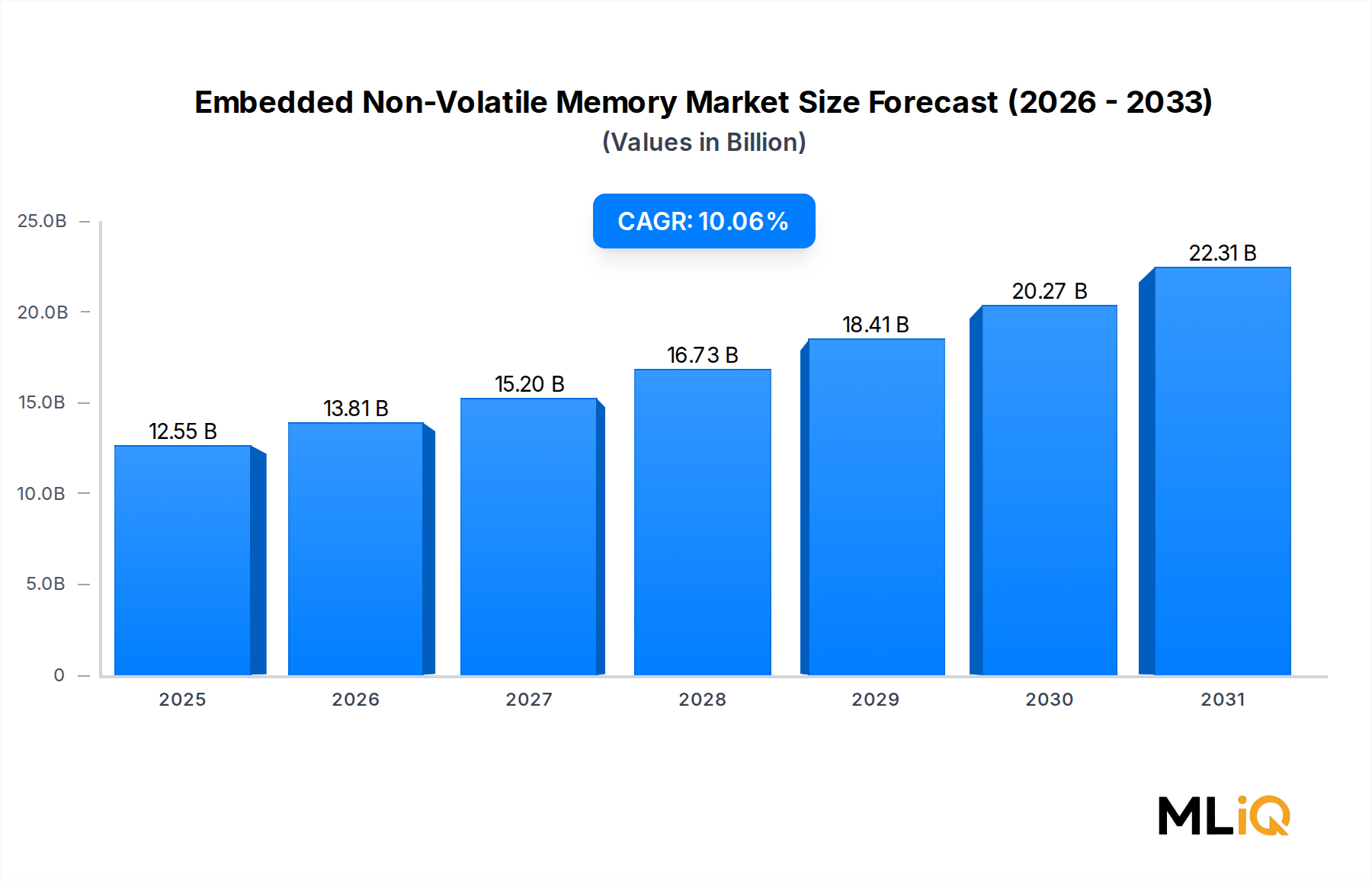

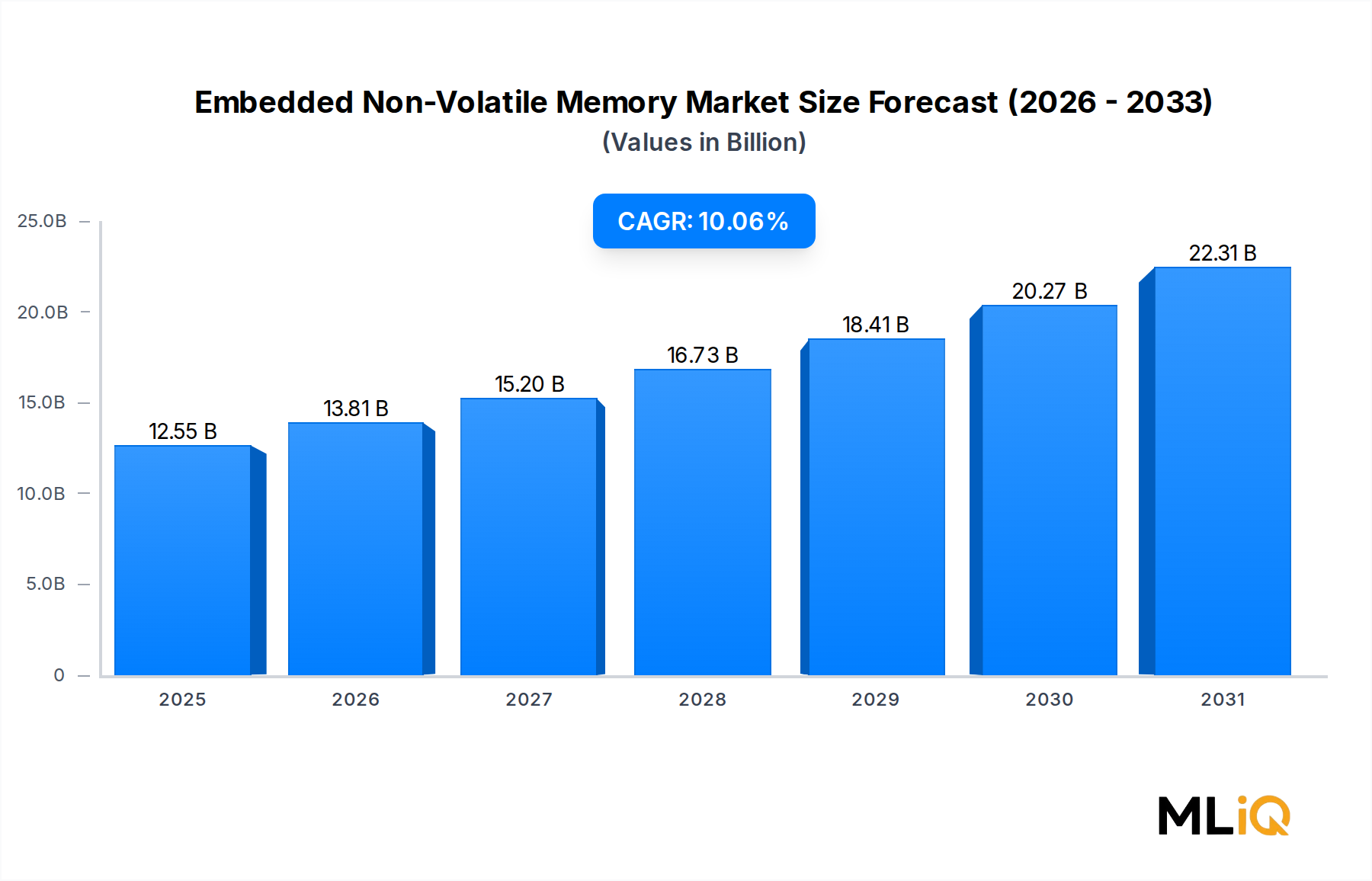

The global Embedded Non-Volatile Memory Market is valued at $12.55 billion in 2025 and is projected to expand at a compound annual growth rate (CAGR) of 10.06% through 2033, reflecting robust secular demand across consumer, automotive, and industrial verticals. This growth trajectory is underpinned by the accelerating integration of intelligent processing capabilities into edge devices, the proliferation of connected systems requiring persistent data storage, and an industry-wide transition toward more advanced process nodes that demand tighter on-chip memory integration.

Embedded non-volatile memory (eNVM) has become a cornerstone of modern system-on-chip (SoC) design, enabling microcontrollers, automotive ECUs, smart cards, and IoT edge nodes to store firmware, calibration data, and security credentials without relying on discrete external memory components. Unlike standalone Flash Memory Market products, eNVM is fabricated directly onto the logic die, reducing bill-of-materials complexity, lowering power consumption, and improving latency — characteristics increasingly valued as device architectures scale toward sub-28nm nodes.

Key demand drivers include the rapid electrification of vehicles, which multiplies the number of embedded controllers per platform; the global rollout of 5G infrastructure, which stimulates demand for network-edge processors with integrated firmware storage; and the structural shift toward secure element architectures in payment, identity, and industrial control applications. The EEPROM Market and the broader Internet of Things Semiconductor Market are both feeding upstream eNVM consumption, as designers increasingly prefer monolithic solutions over multi-chip module approaches.

From a macro perspective, semiconductor capital expenditure cycles, geopolitical tensions affecting foundry allocation, and supply-chain diversification strategies are reshaping where eNVM is manufactured and by whom. Government-backed semiconductor incentive programs in the United States, European Union, Japan, and India are expected to stimulate new foundry capacity that supports embedded memory process modules.

Looking ahead to 2033, the market is forecast to reach a valuation exceeding $27 billion under the base-case scenario, with upside potential driven by faster-than-expected automotive electrification rates, broader adoption of on-device AI inference requiring persistent model storage, and the maturation of embedded MRAM as a high-endurance, high-speed alternative to conventional eFlash. The competitive landscape will increasingly be shaped by IP licensing models and foundry-embedded IP partnerships, positioning specialized memory IP vendors as strategic kingmakers alongside leading-edge process providers.

Among all product segments within the Embedded Non-Volatile Memory Market — including eFlash, eOTP, eE2PROM, eMTP, eMRAM, and others — eFlash commands the largest revenue share, driven by its unmatched combination of read/write endurance, reprogrammability, and compatibility with mainstream CMOS process nodes ranging from 180nm down to sub-28nm. eFlash is embedded directly into microcontroller and SoC designs to store operating firmware, boot code, configuration parameters, and over-the-air (OTA) update payloads, making it indispensable across virtually every intelligent electronic system shipped today.

The dominance of eFlash is structurally reinforced by the sheer volume of microcontroller unit (MCU) shipments globally. The Microcontroller Market consumes eFlash in quantities that dwarf all other embedded memory types, as every general-purpose, automotive-grade, or industrial MCU typically integrates between 32 KB and 8 MB of embedded Flash. When multiplied across the billions of MCUs shipped annually for appliances, motor drives, HVAC systems, wearables, and vehicle body electronics, eFlash's revenue contribution becomes self-sustaining through design-win momentum and long product lifecycle commitments.

In the automotive vertical, eFlash is the memory of choice for AUTOSAR-compliant ECUs, ADAS processing nodes, and powertrain controllers. The Automotive Semiconductor Market's rapid expansion — driven by the industry's transition toward software-defined vehicles — is directly amplifying eFlash demand, as each new vehicle generation integrates more ECUs with larger firmware footprints. Functional safety requirements under ISO 26262 further favor eFlash due to its mature error correction and data retention characteristics, which have been validated over decades of automotive qualification testing.

From a process technology standpoint, eFlash integration faces a well-documented scaling challenge below 28nm: the tunnel oxide thickness required for reliable charge storage cannot be reduced proportionally with logic transistor dimensions, creating a thermal budget and process compatibility conflict. This constraint has catalyzed significant R&D investment by foundries and IP providers to develop floating-gate and charge-trap eFlash variants optimized for 22nm FD-SOI, 16nm FinFET, and even 7nm-class nodes. Companies such as eMemory Technology Inc. and Kilopass have developed proprietary eFlash and OTP IP blocks that are licensed to foundries and fabless customers, enabling continued eFlash deployment at advanced nodes without requiring customers to develop bespoke memory modules in-house.

The consolidation dynamics within the eFlash sub-segment are notable. While large integrated device manufacturers (IDMs) such as Renesas, STMicroelectronics, and Infineon develop proprietary eFlash processes for internal MCU production, the fabless-foundry ecosystem increasingly relies on third-party IP licensors to access eFlash capability on merchant process nodes. This bifurcation creates a dual competitive structure: vertically integrated IDMs competing on eFlash density and endurance per MCU family, and IP licensors competing on royalty terms, process node coverage, and qualification support.

Market share within eFlash is consolidating around a smaller number of process node-qualified IP providers, while the customer base for eFlash-bearing ICs continues to diversify across consumer, industrial, automotive, and communications verticals. Revenue concentration risk is moderate: no single end-market accounts for more than approximately 35% of eFlash consumption, providing resilience against sector-specific downturns. The eFlash segment's share of total eNVM revenue is expected to remain above 45% through the forecast period, even as eMRAM gains traction in high-endurance and high-temperature applications that stress conventional Flash oxide reliability.

The primary driver accelerating the Embedded Non-Volatile Memory Market is the proliferation of intelligent edge nodes across automotive, industrial, and consumer domains. Vehicle electrification and ADAS adoption are particularly impactful: modern battery electric vehicles integrate between 70 and 150 ECUs, each requiring embedded firmware storage, compared to approximately 30–50 ECUs in a conventional internal combustion engine vehicle manufactured a decade ago. This per-vehicle memory content increase, multiplied across global automotive production volumes of roughly 90 million units annually, represents a structurally durable demand vector.

The Consumer Electronics Market constitutes the second major demand pillar. Wearable devices, true wireless stereo earbuds, smart home controllers, and health monitoring gadgets collectively ship in the billions of units per year, each integrating an MCU or small SoC with embedded non-volatile memory for firmware and user data. As average firmware complexity and security certificate storage requirements grow, per-device eNVM density is expanding, translating to higher average selling prices even in commoditized device categories.

Security and cryptographic key storage requirements are an increasingly important driver. Regulatory mandates such as the EU Cyber Resilience Act and NIST post-quantum cryptography standards are compelling device manufacturers to provision larger and more endurance-rated embedded memory to store cryptographic material. This regulatory tailwind disproportionately benefits eMTP and eMRAM segments, which offer higher endurance than standard eOTP.

The principal constraint is process node scaling incompatibility. As the Advanced Logic Semiconductor Market migrates to 5nm and 3nm nodes for high-performance applications, embedding NVM at these nodes remains technically and economically prohibitive for most applications, forcing architects toward chiplet or 3D integration workarounds that partially commoditize eNVM's integration advantage. Additionally, supply chain concentration — with the majority of eNVM process capacity residing in Asia Pacific — introduces geopolitical risk that is difficult to hedge on short timescales, constraining foundry diversification for Western OEMs.

The competitive landscape of the Embedded Non-Volatile Memory Market is characterized by a mix of foundry service providers, specialized IP licensors, and vertically integrated semiconductor manufacturers. Key participants include:

eMemory Technology Inc.: A leading provider of embedded NVM intellectual property, eMemory licenses its NeoBit OTP, NeoFlash eFlash, and NeoMTP technologies to foundries and fabless chip designers globally, with IP ported to process nodes spanning 180nm through sub-14nm, making it one of the broadest coverage providers in the Semiconductor IP Market.

Kilopass: Specializing in antifuse OTP embedded memory IP, Kilopass serves fabless customers seeking compact, cost-effective one-time programmable solutions for trim, configuration, and unique ID storage on leading-edge CMOS nodes, competing primarily on area efficiency and leakage characteristics.

Global Foundries: As a major merchant foundry, GlobalFoundries offers embedded NVM process modules — including eFlash and eOTP — as standard platform options on its 22FDX and 12LP+ nodes, enabling customers to access eNVM integration without in-house process development, making it a critical infrastructure partner for the SRAM Market and adjacent memory integration segments.

HHGrace: A China-based specialty foundry focused on mature process nodes (180nm–55nm), HHGrace provides eFlash and eOTP process platforms serving domestic Chinese customers in automotive, smart card, and consumer MCU segments, benefiting from China's semiconductor self-sufficiency initiatives.

Semiconductor Manufacturing International Corporation (SMIC): As China's largest and most advanced domestic foundry, SMIC supports eFlash and embedded memory process modules across multiple nodes, serving a broad customer base in the consumer, communications, and automotive verticals, and playing an increasingly strategic role in the domestic supply chain for the Internet of Things Semiconductor Market.

United Microcontroller Corporation (UMC): A Taiwan-based foundry offering a comprehensive portfolio of embedded NVM process options including eFlash, eOTP, and eE2PROM on nodes from 150nm to 22nm, UMC serves global fabless MCU and analog IC designers seeking qualified embedded memory integration on mature and mid-range process nodes.

Q1 2024: eMemory Technology Inc. announced the porting of its NeoFlash embedded Flash IP to a 22nm FD-SOI process node in collaboration with a leading European foundry partner, expanding eFlash availability for automotive-grade SoC designs requiring sub-28nm integration.

Q2 2024: SMIC disclosed the successful qualification of a 55nm eFlash platform for automotive-grade customers, meeting AEC-Q100 Grade 1 requirements and enabling domestic Chinese automotive IC suppliers to reduce dependence on foreign foundry capacity for safety-critical embedded memory applications.

Q3 2024: GlobalFoundries expanded its 22FDX embedded NVM portfolio with the addition of a high-endurance eMRAM option co-developed with a strategic memory IP partner, targeting industrial IoT and automotive applications demanding greater than 10 million write cycles.

Q4 2024: UMC announced a licensing and process development agreement with a major fabless MCU vendor for a 40nm eFlash platform customized for motor control and power management IC applications, reinforcing its position in the mid-range embedded memory foundry segment.

Q1 2025: HHGrace completed qualification of a 40nm eE2PROM process module for smart meter and energy management IC customers, enabling byte-level rewrite capability on a cost-optimized process node aligned with the requirements of the Consumer Electronics Market.

Q2 2025: Industry consortium JEDEC published an updated standard for embedded NVM endurance and data retention characterization, providing a unified test methodology that is expected to accelerate automotive and industrial qualification timelines for next-generation eNVM technologies.

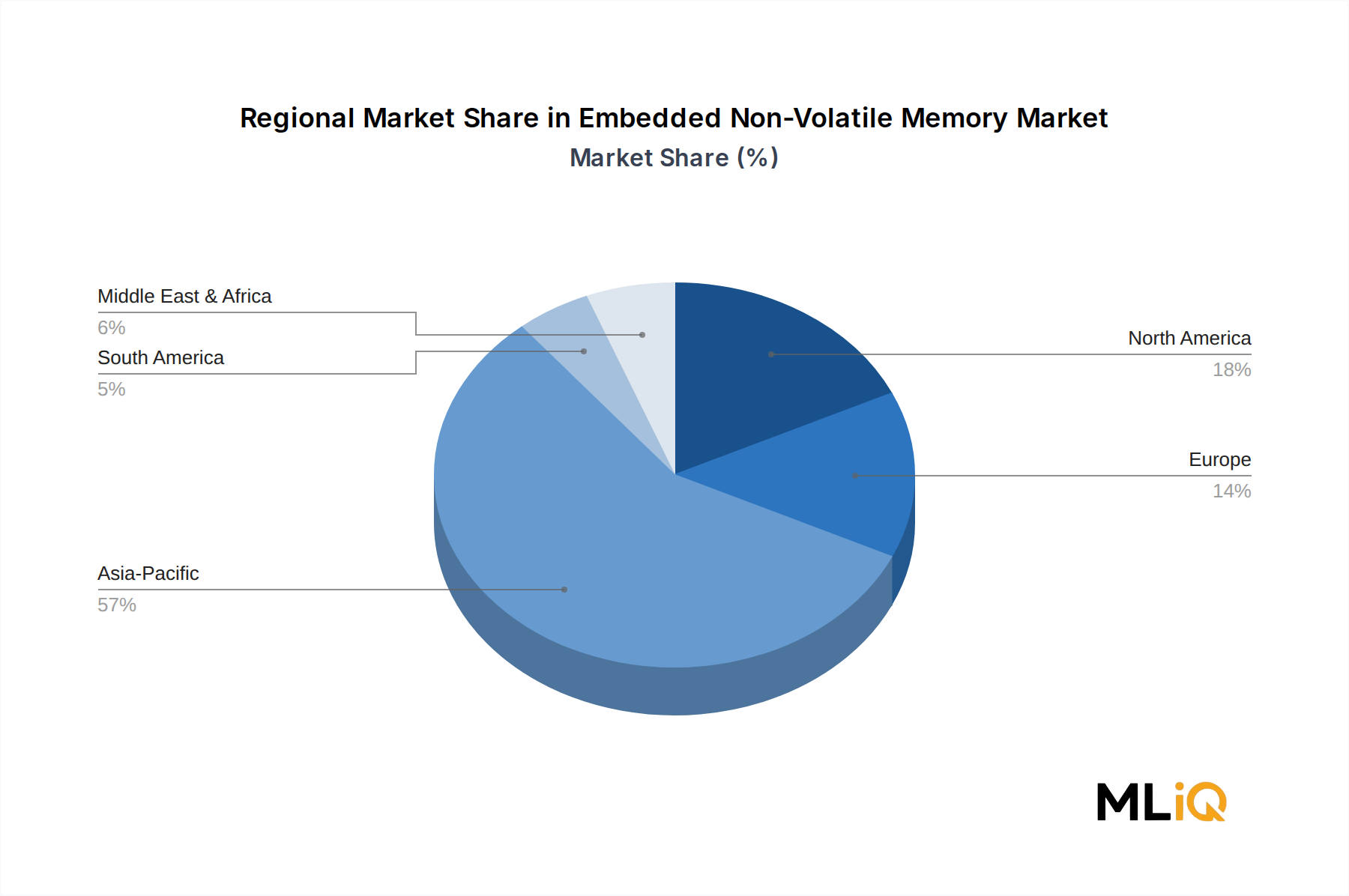

Asia Pacific is the dominant region in the Embedded Non-Volatile Memory Market, accounting for approximately 52% of global revenue in 2025. The region's leadership is rooted in its concentration of semiconductor foundry capacity, the world's largest consumer electronics manufacturing ecosystem, and China's accelerating domestic semiconductor development programs. China alone contributes an estimated 28–30% of Asia Pacific's regional eNVM revenue, driven by domestic MCU vendors, smart card manufacturers, and automotive IC suppliers supported by foundries including SMIC and HHGrace. Japan and South Korea contribute through their IDM and materials ecosystems, while ASEAN nations are emerging as secondary manufacturing hubs. The region's CAGR is estimated at 10.8% through 2033, making it the fastest-growing major region alongside its status as the largest by volume.

North America represents approximately 22% of global revenue, with the United States as the primary contributor through its large base of fabless semiconductor companies designing eNVM-bearing SoCs for automotive, defense, and industrial markets. The CHIPS and Science Act is catalyzing domestic foundry investment that will gradually expand North American eNVM process capacity. The region's CAGR is projected at 9.4%, driven by automotive electrification content growth and defense electronics modernization programs.

Europe accounts for approximately 18% of global revenue, anchored by Germany's automotive semiconductor ecosystem and the region's strong industrial automation sector. The EU Chips Act is supporting capacity expansion at European foundries capable of hosting eFlash process modules. European CAGR is estimated at 9.1%, with automotive-grade eNVM representing the primary growth vector, directly feeding into the Automotive Semiconductor Market.

South America and the Middle East & Africa collectively represent the remaining approximately 8% of revenue, with Brazil and the GCC nations leading consumption within their respective regions. These markets are primarily driven by consumer electronics and telecommunications equipment demand rather than domestic semiconductor production, and both are expected to grow at CAGRs in the 7.5–8.5% range through 2033, constrained by limited local foundry infrastructure but supported by expanding smart device adoption.

Pricing dynamics in the Embedded Non-Volatile Memory Market are structurally distinct from those governing standalone discrete memory markets because eNVM is sold as part of a foundry process module or integrated IP license rather than as a discrete component. The effective price of eNVM capability is therefore expressed through wafer surcharges, IP royalty rates, and per-unit licensing fees rather than component spot prices, insulating the market from the acute commodity cycles affecting the Flash Memory Market and the SRAM Market.

For foundries offering eFlash or eOTP process modules, the incremental wafer cost associated with embedding NVM typically adds between 8% and 25% to baseline logic wafer pricing, depending on the node and the complexity of the memory module (number of additional mask layers, implant steps, and thermal cycles required). At mature nodes (180nm–55nm), eNVM modules are well-characterized and process yields are high, supporting stable incremental margins for foundries. At advanced nodes (28nm and below), the process complexity and lower yields on eFlash-integrated wafers compress foundry margins on these splits, creating a competitive tension between eFlash and alternative embedded memory technologies such as eMRAM, which has a simpler integration path at sub-28nm.

IP licensors such as eMemory operate under a royalty-per-chip or paid-up license model, where margins are primarily software-like (high gross margins, low incremental cost of delivery), but revenue is tied to customer production volumes and the competitive dynamics of the Semiconductor IP Market. Pricing pressure from competing IP providers and from foundries developing in-house memory IP creates margin compression risk for pure-play licensors.

For end-customers (fabless MCU or SoC designers), the total cost of eNVM integration is weighed against the system-level savings from eliminating external memory components, reducing PCB area, and improving reliability. This value-capture dynamic gives eNVM solution providers pricing power relative to the system-level BOM savings delivered, moderating price erosion compared to more commoditized component

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 10.06% from 2020-2034 |

| Segmentation |

|

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Comprehensive validation mechanisms ensuring market intelligence accuracy, reliability, and adherence to international standards.

500+ data sources cross-validated

200+ industry specialists validation

NAICS, SIC, ISIC, TRBC standards

Continuous market tracking updates

Factors such as are projected to boost the Embedded Non-Volatile Memory Market market expansion.

Key companies in the market include eMemory Technology Inc., Kilopass, Global Foundries, HHGrace, Semiconductor Manufacturing International Corporation (SMIC), United Microcontroller Corporation (UMC).

The market segments include Product, Industry Vertical.

The market size is estimated to be USD 12.55 billion as of 2022.

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3690, USD 5820, and USD 9870 respectively.

The market size is provided in terms of value, measured in billion and volume, measured in .

Yes, the market keyword associated with the report is "Embedded Non-Volatile Memory Market," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Embedded Non-Volatile Memory Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.