1. What are the major growth drivers for the Data Visualization Software Market market?

Factors such as are projected to boost the Data Visualization Software Market market expansion.

Market Lens IQ is a global market intelligence and strategic consulting firm delivering advanced syndicated research reports, customized industry analysis, competitive intelligence, and data-driven advisory solutions to organizations across international markets. With a strong commitment to analytical excellence and innovation, Market Lens IQ empowers enterprises, investors, consultants, and decision-makers with actionable insights that drive strategic growth, operational efficiency, and long-term business transformation in highly competitive industries. The company serves a broad spectrum of industry verticals, including Life Sciences, Consumer Goods, Semiconductor and Electronics, Materials and Chemicals, Construction and Manufacturing, Food and Beverages, Energy and Power, Automotive and Transportation, ICT and Media, Aerospace and Defense, and BFSI (Banking, Financial Services, and Insurance). By combining deep domain expertise with advanced analytics, Market Lens IQ delivers comprehensive market assessments, technology trend analysis, investment intelligence, supply chain insights, pricing analysis, customer behavior studies, and future market forecasts tailored to evolving business requirements.

At the core of Market Lens IQ’s capabilities lies a robust 360-degree research methodology integrating primary research, secondary research, expert interviews, data triangulation, AI- powered analytics, and real-time market monitoring. Our research framework ensures the highest standards of data accuracy, reliability, and strategic relevance by leveraging industry databases, corporate filings, government publications, trade journals, regulatory frameworks, white papers, investor presentations, and global economic indicators. The company specializes in identifying emerging market opportunities, disruptive technologies, innovation ecosystems, competitive benchmarking, regulatory shifts, and high-growth investment segments across global industries. Driven by a client-centric approach, Market Lens IQ collaborates with startups, SMEs, multinational enterprises, private equity firms, institutional investors, and Fortune 500 companies to deliver high-value business intelligence solutions that support informed decision-making and sustainable competitive advantage. Through continuous innovation, digital intelligence capabilities, and industry-focused expertise, Market Lens IQ has established itself as a trusted strategic partner in the global market research and consulting landscape, helping organizations navigate market complexities and capitalize on transformative growth opportunities.

Data Visualization Software Market

Data Visualization Software Market+1 2315155523

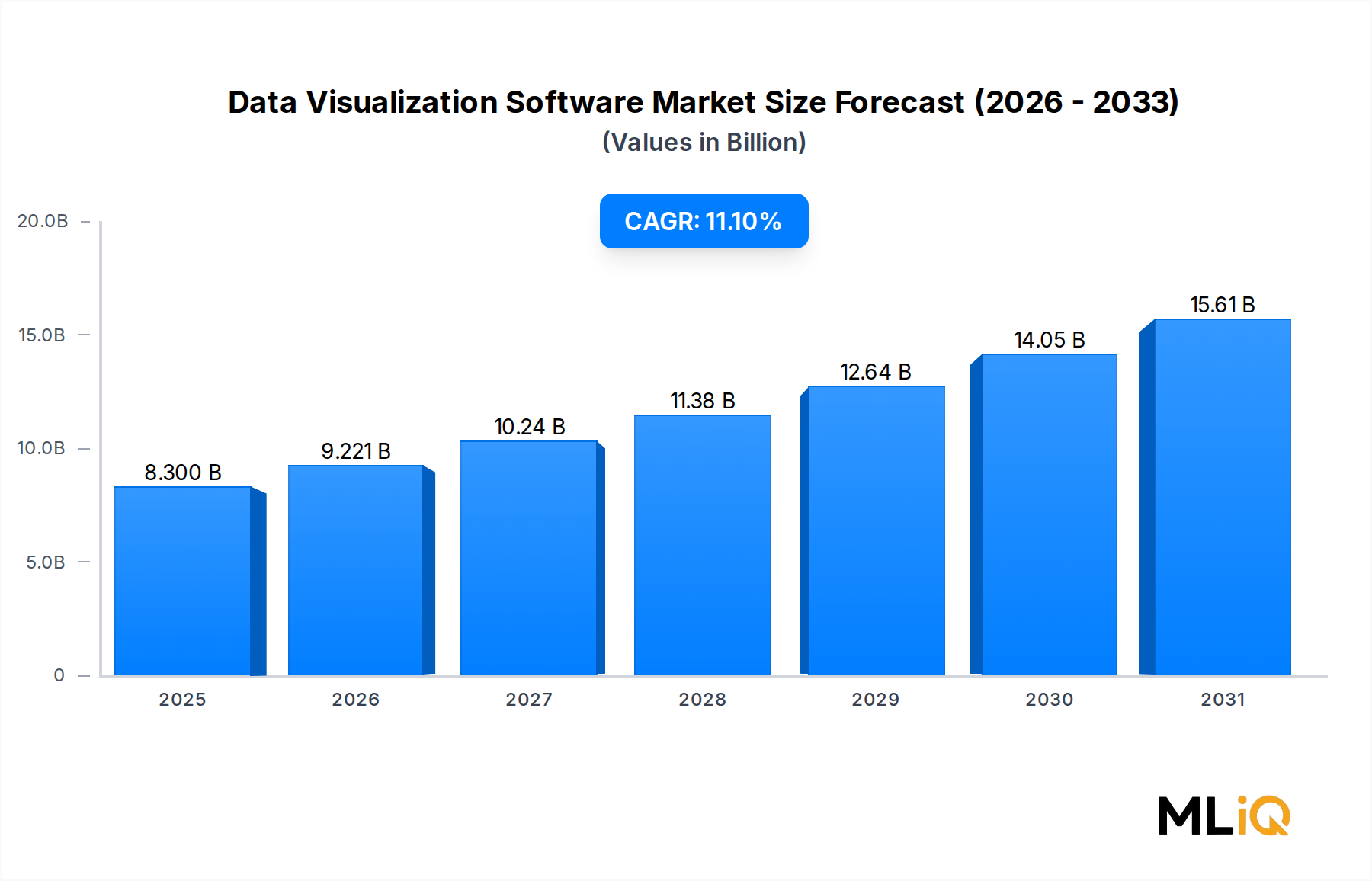

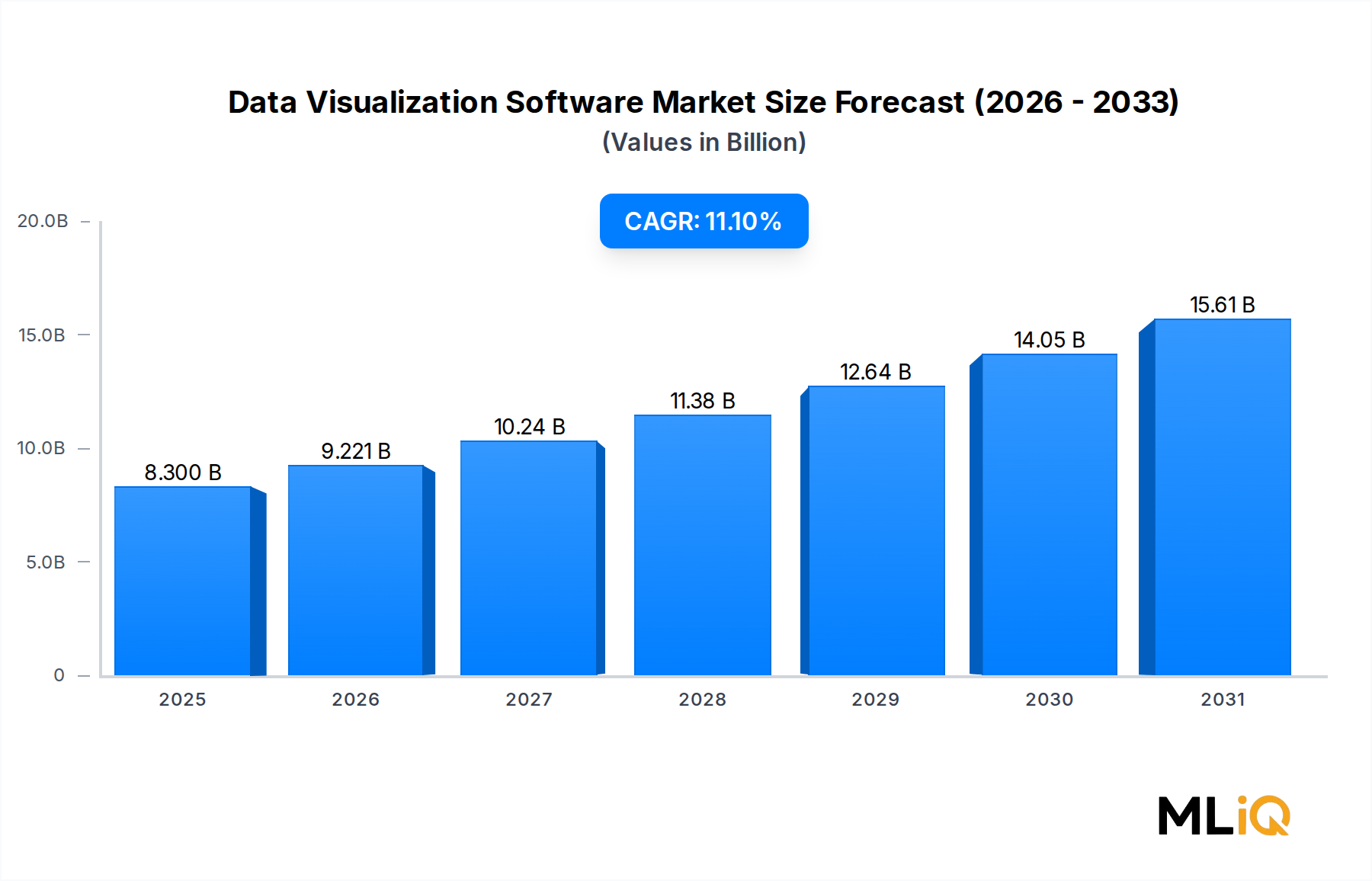

The global Data Visualization Software Market was valued at $8.3 billion in 2023 and is projected to expand at a compound annual growth rate (CAGR) of 11.1% through the forecast period, reaching an estimated $21.4 billion by 2033. This robust trajectory reflects the accelerating enterprise need to convert vast volumes of raw data into actionable, visual intelligence that supports faster and more confident decision-making at every organizational level.

Several macro-level forces are converging to fuel this expansion. First, the proliferation of cloud infrastructure has dramatically reduced the barriers to deploying sophisticated visualization platforms, enabling small and mid-sized enterprises to access capabilities once reserved for large corporations. Second, the explosion of data generated across industries — from IoT sensor networks and e-commerce transaction logs to electronic health records and financial trading feeds — has made intuitive data storytelling a strategic necessity rather than an optional capability. Third, the rise of self-service analytics culture has shifted demand toward platforms that empower non-technical business users to build interactive dashboards without deep programming expertise.

From a vertical perspective, the BFSI sector leads adoption owing to regulatory reporting requirements and risk management imperatives. Healthcare and life sciences follow closely, driven by the need to visualize patient outcomes, clinical trial data, and genomic information at scale. The retail and e-commerce segment is experiencing particularly rapid uptake as personalization engines and supply chain dashboards become standard operating tools.

Geographically, North America commands the largest revenue share, anchored by early enterprise adoption and a dense ecosystem of software vendors. However, Asia Pacific is emerging as the fastest-growing region, fueled by digital transformation mandates in China, India, and Southeast Asian economies.

Looking ahead, the integration of artificial intelligence and natural language processing into visualization interfaces represents the most transformative near-term catalyst. AI-powered features — including automated chart recommendations, anomaly spotlighting, and conversational query interfaces — are redefining the user experience and widening the addressable market. Vendors that successfully embed these capabilities while maintaining governance, security, and interoperability will be best positioned to capture disproportionate growth through the forecast horizon.

Among all deployment and tool modalities within the Data Visualization Software Market, cloud-based and Software-as-a-Service (SaaS) delivery has emerged as the single largest and fastest-consolidating revenue segment. As of 2023, cloud and SaaS deployments collectively account for more than 55% of total market revenue, a proportion that is expected to widen further as organizations accelerate migration away from legacy on-premise architectures.

The dominance of cloud-based visualization tools stems from several interlocking advantages. First, cloud delivery eliminates the capital expenditure associated with on-premise server provisioning and maintenance, replacing it with predictable operational expenditure models that align with modern enterprise IT budgeting frameworks. Second, cloud platforms enable seamless, real-time collaboration — allowing geographically distributed teams to co-author dashboards and share live data views without file-export workflows. Third, cloud vendors can push updates, security patches, and new feature releases continuously, ensuring customers always operate on the latest version without disruptive upgrade cycles.

Within the cloud segment, the SaaS sub-tier is particularly dynamic. SaaS-based visualization platforms have lowered the total cost of ownership sufficiently to attract customers in sectors that have historically been conservative technology adopters, including government agencies and regulated financial institutions. The pay-per-seat or consumption-based pricing models of SaaS offerings have proven especially attractive to organizations with seasonal or project-based analytics workloads.

Mobile delivery — both Android Native and iOS Native — represents a growing adjunct to the cloud segment. As C-suite executives increasingly demand executive dashboard access on mobile devices, vendors have invested heavily in mobile-responsive design frameworks and native application development. Mobile-native visualization clients now support full interactivity, drill-down navigation, and push-notification alerting, bringing the full analytical experience to handheld form factors.

Key players driving the cloud segment include Tableau Software Inc., which offers Tableau Cloud as its primary SaaS delivery vehicle with deep integration into the Salesforce ecosystem; Microsoft Corporation, whose Power BI service is embedded within Microsoft 365 and Azure, giving it unparalleled distribution leverage; and Sisense Inc., which has distinguished itself through its embedded analytics API framework designed for cloud-native application developers.

The competitive dynamics within the cloud segment are intensifying. Established vendors are defending market share through aggressive bundling strategies — packaging visualization capabilities within broader enterprise suites — while pure-play SaaS challengers are competing on specialization, user experience, and faster time-to-insight. The net effect is sustained pricing pressure on legacy on-premise tools, which now face an existential migration imperative.

On-premise deployments retain relevance in highly regulated environments — particularly within government and defense sectors where data sovereignty requirements prohibit cloud hosting. However, even within these segments, hybrid deployment architectures are gaining traction, allowing organizations to maintain sensitive data on-premise while pushing less sensitive workloads to cloud-based rendering engines. This hybrid model is expected to serve as a transitional bridge, gradually pulling even the most compliance-constrained organizations toward predominantly cloud-based operations by the end of the forecast period.

The Data Visualization Software Market is propelled by a set of quantifiable structural drivers while simultaneously contending with material constraints that moderate growth velocity.

Driver 1 — Exponential Data Volume Growth: Global data creation is projected to reach 120 zettabytes by 2023 and exceed 180 zettabytes by 2025 according to leading industry tracking bodies. This data deluge has made automated, visual summarization tools indispensable for organizations seeking to operationalize insights at machine-generated scale. Industries including manufacturing (IoT telemetry), retail (clickstream analytics), and healthcare (wearable device data) are primary contributors.

Driver 2 — Enterprise Digital Transformation Budgets: Global spending on digital transformation was estimated at over $2.3 trillion in 2023, with analytics and data platforms representing one of the top three investment categories. Visualization software is a downstream beneficiary of this capital allocation, as transformed business processes require visual interfaces to monitor performance and detect deviations.

Driver 3 — Democratization of Analytics: The self-service analytics movement has expanded the buyer population from data scientists and IT professionals to line-of-business managers and frontline workers. Platforms with drag-and-drop interfaces and natural language query capabilities are capturing new user tiers that were previously unaddressed, effectively widening the total addressable market.

Constraint 1 — Data Privacy and Security Concerns: Regulations including GDPR in Europe and CCPA in California impose strict requirements on how personal data may be processed, stored, and visualized. Compliance overhead increases deployment complexity, particularly for cloud-hosted platforms that process cross-border data flows, acting as a friction point for adoption in privacy-sensitive sectors.

Constraint 2 — Integration Complexity: Many enterprises operate heterogeneous data environments spanning legacy ERP systems, modern cloud data warehouses, and semi-structured data lakes. The effort required to connect visualization tools to these disparate sources — and to maintain those connections as underlying schemas evolve — represents a significant implementation barrier that prolongs sales cycles and increases total cost of ownership.

Constraint 3 — Skills Gap: Despite the push toward self-service analytics, effective use of advanced visualization features still requires analytical literacy that is unevenly distributed across workforces. Organizations frequently cite inadequate internal skills as a constraint on realizing full platform value.

The competitive landscape of the Data Visualization Software Market is characterized by a blend of large enterprise software conglomerates, specialized pure-play analytics vendors, and emerging cloud-native challengers. Below is a structured profile of the primary participants:

Tableau Software Inc.: A pioneer in self-service visual analytics, Tableau has built one of the largest community ecosystems in the market with over 1 million active users globally. Its acquisition by Salesforce in 2019 has enabled deep CRM-to-dashboard integration, giving it a privileged distribution channel into Salesforce's vast enterprise customer base.

Microsoft Corporation: Microsoft leverages its Power BI platform as a cornerstone of the Azure and Microsoft 365 ecosystem. Its freemium model and native integration with Excel, Teams, and Azure Synapse give it unmatched distribution reach, making it the default visualization choice for organizations already committed to the Microsoft stack.

IBM Corporation: IBM's Cognos Analytics platform targets large enterprise customers with complex governance, security, and compliance requirements. IBM's hybrid cloud strategy, underpinned by its Red Hat OpenShift platform, allows Cognos to deploy across on-premise, private cloud, and public cloud environments seamlessly.

Oracle Corporation: Oracle's analytics suite is deeply integrated with its database and ERP product lines, making it a natural choice for Oracle-centric enterprise environments. The company has been actively embedding AI-driven augmented analytics features to modernize the platform's user experience.

SAS Institute Inc.: SAS remains a dominant force in regulated industries — particularly pharmaceuticals, financial services, and government — where its statistical rigor and audit-trail capabilities are differentiating. Its Viya platform represents a significant architectural modernization toward cloud-native deployment.

Tibco Software Inc.: Tibco's Spotfire platform is widely deployed in life sciences and energy sectors, where it is valued for its advanced statistical visualization capabilities and real-time streaming data integration. Tibco's recent merger activity has expanded its data management portfolio.

Microstrategy Inc: MicroStrategy targets the enterprise business intelligence segment with a focus on large-scale deployments and hyper-scalable dashboard infrastructure. The company has also made headlines for its aggressive corporate Bitcoin treasury strategy, which has elevated its public profile.

Hitachi Vantara: Hitachi Vantara combines visualization software with its broader data infrastructure and IoT platform offerings, targeting industrial and operational technology use cases where shop-floor data must be surfaced to management dashboards in real time.

Sisense Inc.: Sisense differentiates through its embedded analytics capabilities, enabling software vendors and digital product teams to integrate white-labeled, interactive dashboards directly into their applications via API. This developer-centric positioning has driven rapid adoption in SaaS product companies.

January 2024: Microsoft announced the general availability of Copilot integration within Power BI, enabling users to generate DAX formulas, create report summaries, and build visuals through natural language prompts, marking a pivotal step in AI-augmented visualization.

March 2024: Tableau Software Inc. unveiled Tableau Pulse, an AI-driven feature that proactively surfaces personalized data insights to business users in their workflow tools including Slack and email, reducing the reliance on manually constructed dashboards.

June 2023: Sisense Inc. completed a strategic restructuring and announced a renewed focus on its embedded analytics platform, exiting certain professional services lines to concentrate R&D investment on its API-first architecture.

September 2023: IBM Corporation launched an updated version of Cognos Analytics with enhanced natural language generation capabilities, allowing users to auto-generate written commentary alongside visual dashboards for board-level reporting.

November 2023: SAS Institute Inc. announced expanded partnerships with cloud hyperscalers including Microsoft Azure and Amazon Web Services to offer Viya as a managed cloud service, reducing deployment friction for regulated-industry customers.

February 2024: Oracle Corporation integrated its Analytics Cloud platform with Oracle Fusion Data Intelligence, enabling pre-built visualization templates for ERP, HCM, and SCM workflows, accelerating time-to-value for Oracle application customers.

April 2024: Tibco Software Inc. released Spotfire 14, introducing collaborative annotation features and enhanced support for Python and R script embedding within the visual canvas, reinforcing its position among data science practitioners.

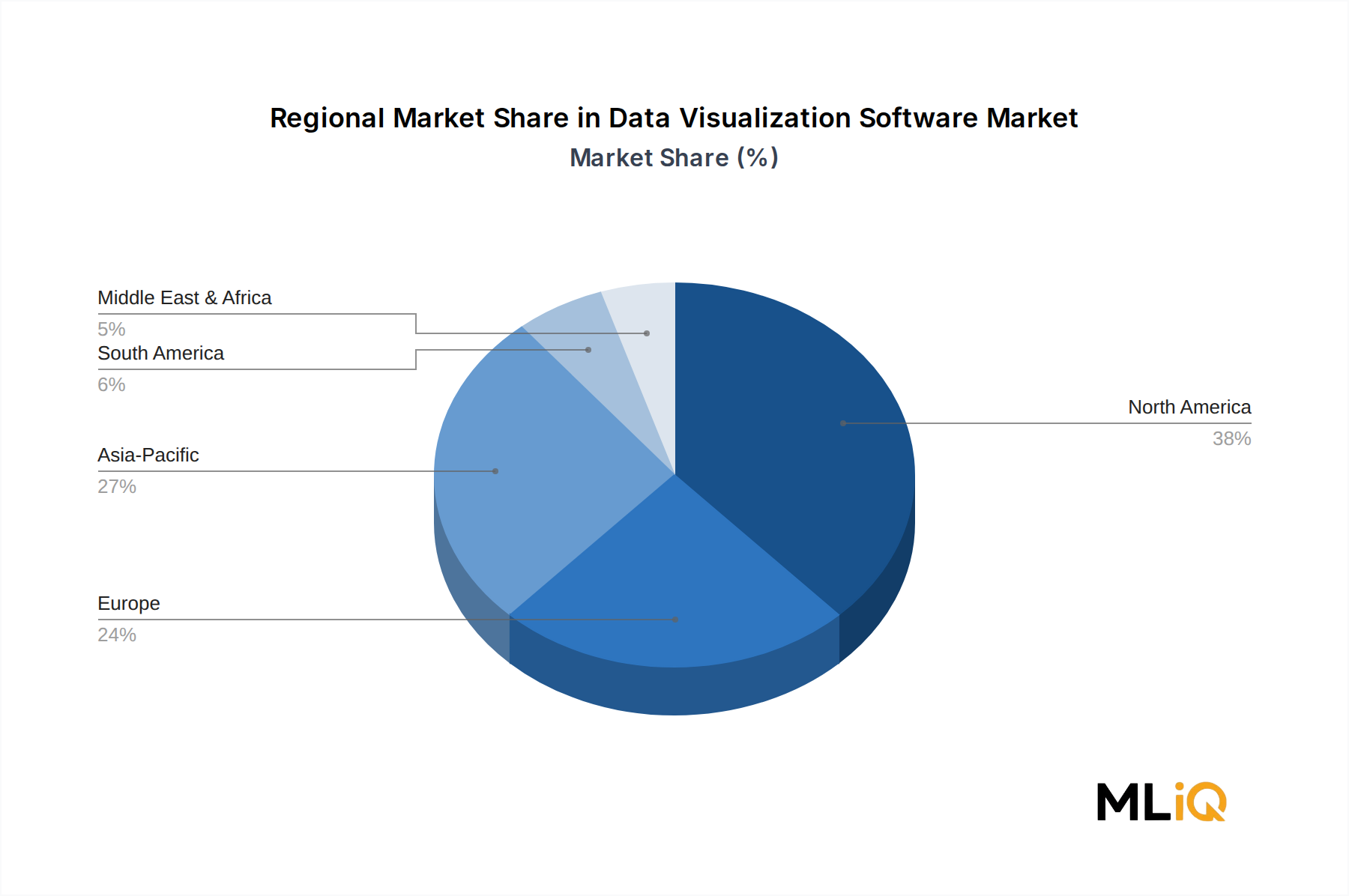

The Data Visualization Software Market exhibits significant regional variation in maturity, growth velocity, and demand drivers, with five major geographic zones each presenting distinct competitive dynamics.

North America remains the most mature and highest-revenue region, accounting for approximately 38% of global market revenue in 2023, equating to roughly $3.2 billion. The United States is the dominant contributor, driven by a deep enterprise technology adoption culture, a high concentration of Fortune 500 headquarters requiring sophisticated analytics infrastructure, and the presence of nearly all major visualization software vendors. The North American market is growing at an estimated CAGR of 9.4%, slightly below the global average, reflecting its relative saturation and the high baseline from which growth is measured. Canada and Mexico contribute incremental growth, particularly in financial services and manufacturing sectors respectively.

Europe represents the second-largest region with an estimated revenue share of 24% in 2023. Germany, the United Kingdom, and France are the anchor markets, with strong demand from automotive manufacturing analytics, financial services reporting, and public sector data transparency initiatives. The European market is uniquely shaped by GDPR compliance requirements, which drive demand for visualization platforms with robust data lineage, access control, and audit logging features. The regional CAGR is estimated at 9.8%, with the Nordics emerging as a high-growth sub-cluster due to advanced digital government initiatives.

Asia Pacific is the fastest-growing region, projected to expand at a CAGR of 14.2% through the forecast period, outpacing the global average by more than 3 percentage points. China and India are the primary growth engines. China's push toward domestic data sovereignty and smart manufacturing under its national industrial policy is generating substantial investment in analytics platforms built on domestic cloud infrastructure. India's burgeoning IT services sector and rapidly expanding startup ecosystem are creating high-velocity demand for SaaS-based visualization tools. Japan and South Korea contribute steady growth from manufacturing intelligence and financial analytics applications.

Latin America, led by Brazil and Argentina, represents an emerging opportunity with a regional CAGR of approximately 11.5%. Adoption is concentrated in the financial services and retail sectors, where e-commerce growth has created urgent demand for customer behavior analytics dashboards.

The Middle East and Africa region, while currently the smallest contributor at approximately 5% of global revenue, is exhibiting accelerating growth driven by government-led smart city programs in the GCC nations and expanding telecommunications infrastructure across Sub-Saharan Africa.

The Data Visualization Software Market operates within an increasingly complex and geographically fragmented regulatory environment that shapes product architecture decisions, data residency requirements, and vendor go-to-market strategies.

In Europe, the General Data Protection Regulation (GDPR), enforced since May 2018, remains the most consequential regulatory framework affecting visualization platforms. GDPR mandates that personal data be processed lawfully, transparently, and for specified purposes — requirements that extend to how data is rendered in dashboards and who is permitted to view visualized personal information. Vendors operating in European markets have been compelled to invest heavily in role-based access controls, data masking features, and audit trail logging to support GDPR compliance for enterprise customers. The proposed EU Data Act, advancing through European legislative processes in 2023-2024, is expected to further regulate data sharing and portability, with downstream implications for how visualization tools handle cross-organizational data flows.

In the United States, the regulatory landscape is more sectoral than comprehensive. The Health Insurance Portability and Accountability Act (HIPAA) governs visualization platforms deployed in healthcare settings, requiring that protected health information displayed in dashboards be subject to strict access controls and encryption standards. The Sarbanes-Oxley Act (SOX) mandates financial reporting integrity, indirectly driving demand for visualization tools with certified data lineage and immutable audit capabilities in the BFSI sector. The California Consumer Privacy Act (CCPA) and its successor, the California Privacy Rights Act (CPRA), impose consent and disclosure obligations that are increasingly adopted as de facto national standards by enterprise compliance teams.

In Asia Pacific, China's Personal Information Protection Law (PIPL), effective November 2021, and its Data Security Law impose data localization requirements that restrict cross-border data flows, compelling international visualization vendors to establish domestic cloud infrastructure or partner with local cloud providers to serve the Chinese market. India's Digital Personal Data Protection Act (2023) introduces similar consent-based frameworks with localization provisions that will shape enterprise deployment architecture decisions.

Standards bodies including ISO and NIST are increasingly active in defining frameworks for data governance and AI transparency that intersect with visualization software deployment, particularly as AI-generated insights embedded in dashboards come under scrutiny for explainability and algorithmic accountability.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 11.1% from 2020-2034 |

| Segmentation |

|

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Comprehensive validation mechanisms ensuring market intelligence accuracy, reliability, and adherence to international standards.

500+ data sources cross-validated

200+ industry specialists validation

NAICS, SIC, ISIC, TRBC standards

Continuous market tracking updates

Factors such as are projected to boost the Data Visualization Software Market market expansion.

Key companies in the market include Tableau Software Inc., Tibco Software Inc., Microstratergy Inc, Hitachi Vantara., Microsoft Corporation, SAS Institute Inc., IBM Corporation, Oracle Corporation, Sisense Inc..

The market segments include Tool, Deployment Model, End User.

The market size is estimated to be USD 8.3 billion as of 2022.

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3690, USD 5820, and USD 9870 respectively.

The market size is provided in terms of value, measured in billion and volume, measured in .

Yes, the market keyword associated with the report is "Data Visualization Software Market," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Data Visualization Software Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.