1. What are the major growth drivers for the Cloud Workflow Market market?

Factors such as are projected to boost the Cloud Workflow Market market expansion.

+1 2315155523

Market Lens IQ is a global market intelligence and strategic consulting firm delivering advanced syndicated research reports, customized industry analysis, competitive intelligence, and data-driven advisory solutions to organizations across international markets. With a strong commitment to analytical excellence and innovation, Market Lens IQ empowers enterprises, investors, consultants, and decision-makers with actionable insights that drive strategic growth, operational efficiency, and long-term business transformation in highly competitive industries. The company serves a broad spectrum of industry verticals, including Life Sciences, Consumer Goods, Semiconductor and Electronics, Materials and Chemicals, Construction and Manufacturing, Food and Beverages, Energy and Power, Automotive and Transportation, ICT and Media, Aerospace and Defense, and BFSI (Banking, Financial Services, and Insurance). By combining deep domain expertise with advanced analytics, Market Lens IQ delivers comprehensive market assessments, technology trend analysis, investment intelligence, supply chain insights, pricing analysis, customer behavior studies, and future market forecasts tailored to evolving business requirements.

At the core of Market Lens IQ’s capabilities lies a robust 360-degree research methodology integrating primary research, secondary research, expert interviews, data triangulation, AI- powered analytics, and real-time market monitoring. Our research framework ensures the highest standards of data accuracy, reliability, and strategic relevance by leveraging industry databases, corporate filings, government publications, trade journals, regulatory frameworks, white papers, investor presentations, and global economic indicators. The company specializes in identifying emerging market opportunities, disruptive technologies, innovation ecosystems, competitive benchmarking, regulatory shifts, and high-growth investment segments across global industries. Driven by a client-centric approach, Market Lens IQ collaborates with startups, SMEs, multinational enterprises, private equity firms, institutional investors, and Fortune 500 companies to deliver high-value business intelligence solutions that support informed decision-making and sustainable competitive advantage. Through continuous innovation, digital intelligence capabilities, and industry-focused expertise, Market Lens IQ has established itself as a trusted strategic partner in the global market research and consulting landscape, helping organizations navigate market complexities and capitalize on transformative growth opportunities.

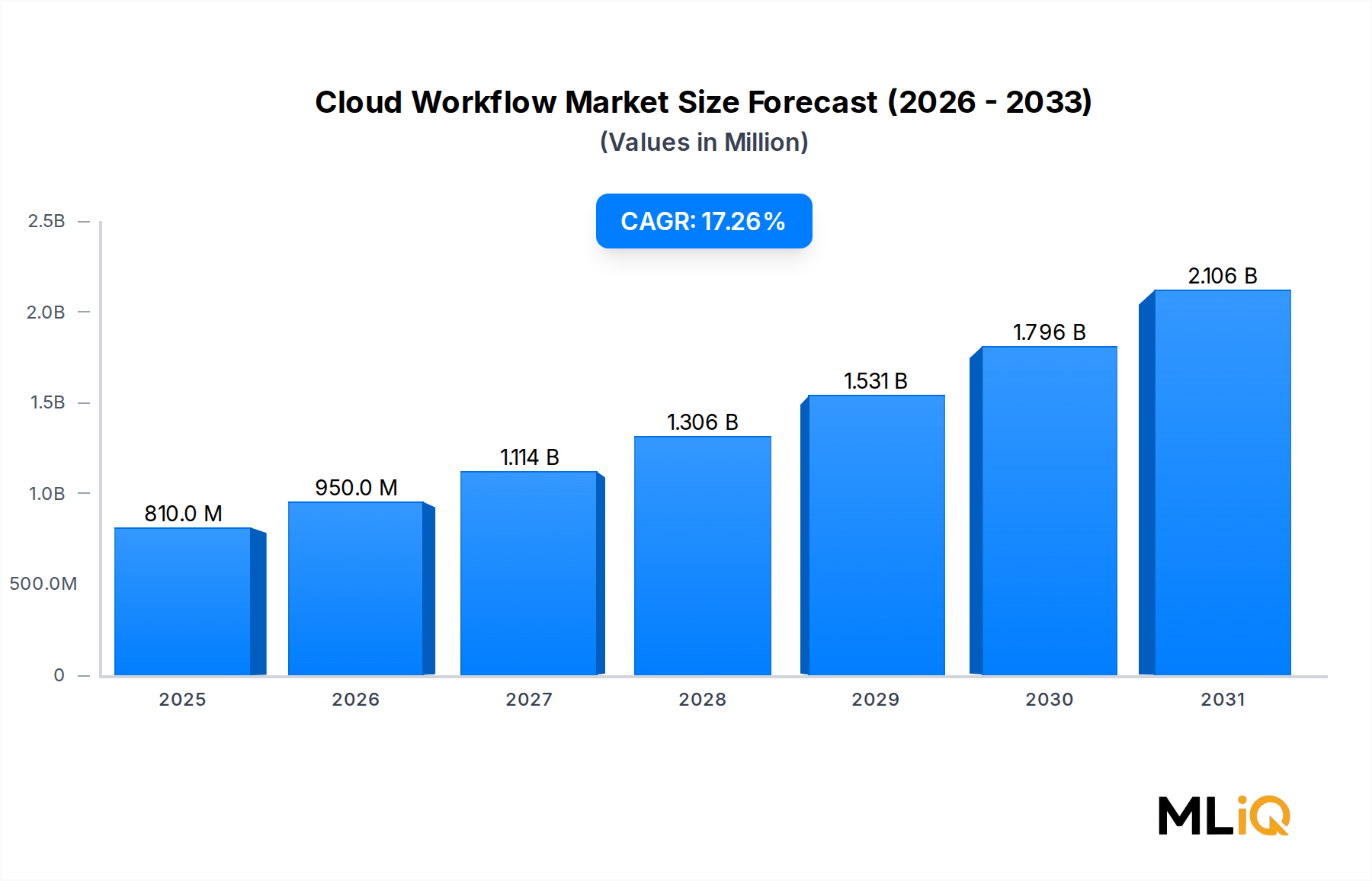

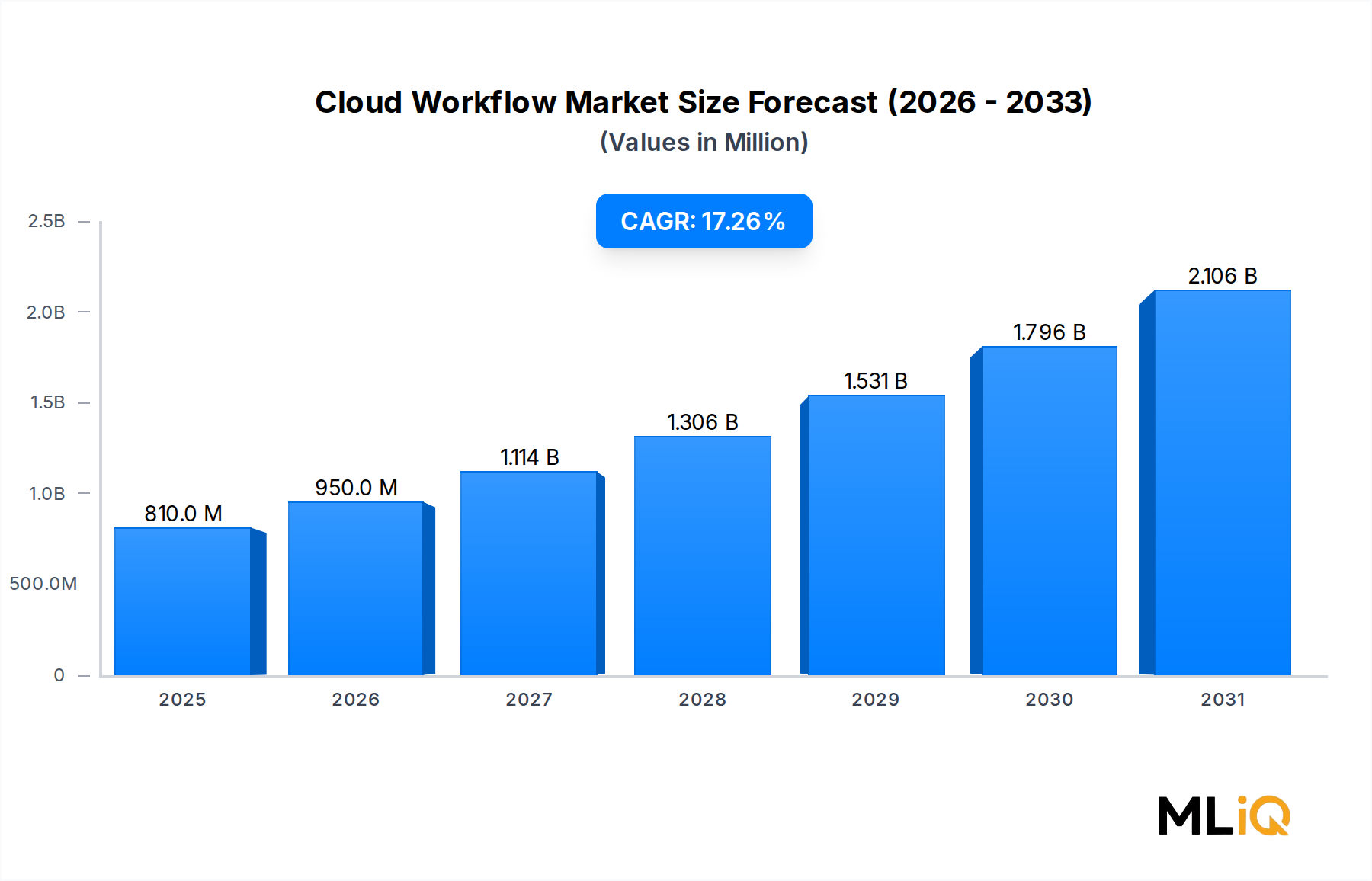

The global Cloud Workflow Market was valued at $0.81 billion in 2023 and is projected to expand at a compound annual growth rate (CAGR) of 17.26% over the forecast period, underscoring the accelerating enterprise shift toward cloud-native operational architectures. This robust growth trajectory is fueled by the convergence of digital transformation imperatives, the proliferation of remote and hybrid work models, and the sustained enterprise demand for cost-efficient, scalable process orchestration.

At its core, cloud workflow platforms enable organizations to automate, monitor, and optimize multi-step business processes across distributed environments without the capital expenditure burdens associated with on-premises infrastructure. As enterprises increasingly migrate their IT estates to hyperscale cloud providers, the need for integrated workflow orchestration layers has become mission-critical. The post-pandemic normalization of distributed workforces has further catalyzed investment in cloud-based coordination tools that provide real-time visibility into task execution, approval chains, and cross-departmental handoffs.

Macroeconomic tailwinds reinforcing this market include the global push for operational efficiency amid inflationary cost pressures, the proliferation of Software-as-a-Service (SaaS) ecosystems, and the regulatory emphasis on auditability and compliance documentation across verticals such as BFSI, healthcare, and government. Enterprises are increasingly recognizing that manual workflow management creates bottlenecks, compliance gaps, and scalability ceilings that cloud-based orchestration tools are uniquely positioned to resolve.

Additionally, the integration of artificial intelligence and machine learning capabilities into workflow platforms is redefining the value proposition of this market. Intelligent routing, predictive bottleneck identification, and natural language processing-based task assignment are transitioning cloud workflow solutions from passive process conduits to active decision-support systems. Vendors are embedding generative AI features that allow non-technical users to design and modify workflows through conversational interfaces, dramatically reducing deployment timelines.

From a segmentation perspective, the platform segment commands the largest revenue share, while the services segment is growing rapidly as enterprises require implementation, customization, and managed services support. HR and finance workflows represent the highest-penetration use cases, though customer service support and supply chain automation are emerging as high-growth verticals.

Looking ahead, the market is expected to benefit from the continued maturation of no-code and low-code development paradigms, deeper API interoperability across enterprise software stacks, and the expansion of cloud infrastructure into emerging economies across Asia Pacific, Latin America, and the Middle East. The competitive landscape is intensifying as both established enterprise software vendors and specialized workflow automation startups compete for platform consolidation opportunities.

Within the Cloud Workflow Market, the platform segment consistently commands the largest share of total revenues and is expected to maintain its dominant position throughout the forecast horizon. Platform-based offerings encompass the core cloud workflow orchestration engines, including visual workflow designers, rule-based automation engines, integration middleware, analytics dashboards, and user permission frameworks. These comprehensive technology stacks address the full lifecycle of workflow creation, deployment, monitoring, and iteration, making them the preferred procurement choice for enterprises seeking end-to-end process governance.

The dominance of the platform segment is rooted in several structural factors. First, platform deployments generate recurring subscription revenues under SaaS licensing models, which enterprises favor for their predictability and lower upfront capital requirements. Second, platform vendors benefit from strong switching costs once workflows are embedded within organizational processes; the complexity of migrating multi-layered workflow logic across vendors creates durable customer retention dynamics. Third, platforms serve as the foundational layer upon which adjacent services revenue — including professional services, training, and managed operations — is layered, creating compounding revenue per account over time.

Key players operating within the platform segment include Workday, Inc., which has integrated cloud workflow capabilities deeply within its human capital management and financial management suites, enabling seamless process automation across HR lifecycle events such as onboarding, payroll approval, and performance reviews. SAP SE similarly leverages its workflow engine within its broader enterprise resource planning ecosystem, allowing customers to orchestrate procurement, finance, and operations workflows with native ERP data context. IBM Corporation competes through its IBM Cloud Pak portfolio, offering workflow automation capabilities that are particularly strong in regulated industries such as banking, insurance, and government, where auditability and security controls are paramount.

WorkForce Software, LLC differentiates its platform through deep specialization in workforce management workflows, including shift scheduling, time and attendance automation, and compliance tracking for labor regulations across multiple jurisdictions. Ultimate Software has built a strong installed base within mid-market and large enterprise HR departments, where its platform automates benefits enrollment, performance management cycles, and employee lifecycle events. Ascentis Corporation addresses the small and medium enterprise segment with a modular cloud workflow platform that integrates HR, payroll, and talent management functions, lowering the complexity of adoption for resource-constrained organizations.

The platform segment's share is not merely holding steady — it is actively consolidating as vendors pursue platform-of-platforms strategies, acquiring point solution providers to expand their workflow coverage across previously unaddressed business domains. The trend toward super-platforms, capable of orchestrating workflows across HR, finance, procurement, and customer service from a unified interface, is driving a wave of consolidation that further entrenches platform-centric vendor relationships.

The growing integration of AI-assisted workflow design within platform offerings is also extending the addressable market by lowering the technical barrier to deployment. Users without coding skills can now construct complex multi-step workflows using drag-and-drop interfaces, template libraries, and AI-generated suggestions, which expands the total potential user base from IT departments to line-of-business managers across every functional domain. This democratization of workflow creation is accelerating platform adoption rates and increasing the frequency of workflow deployment events per enterprise account.

Furthermore, platform vendors are competing aggressively on the breadth and depth of their pre-built connector ecosystems, enabling workflows that span across third-party CRM, ERP, ITSM, and collaboration tools without requiring custom integration development. The richness of a vendor's integration marketplace has become a primary competitive differentiator, directly influencing enterprise procurement decisions in competitive evaluation processes.

The Cloud Workflow Market is shaped by a set of quantifiable drivers and material constraints that collectively define the pace and direction of market expansion.

The most significant demand driver is the accelerating enterprise adoption of digital transformation initiatives. According to industry intelligence, global spending on digital transformation technologies and services exceeded $2.5 trillion in 2023, with cloud workflow automation identified as a core enabling capability. Enterprises undergoing digital transformation consistently cite manual process elimination and cross-system orchestration as top investment priorities, directly feeding demand for cloud workflow platforms.

The proliferation of remote and hybrid work models represents a second structural driver. With distributed teams requiring coordinated task management across time zones and organizational boundaries, cloud workflow platforms provide the synchronization layer that replaces office-based, paper-driven approval processes. Organizations with more than 500 employees have been particularly active buyers of cloud workflow solutions, as the complexity of cross-departmental coordination scales non-linearly with headcount.

Regulatory compliance requirements across the BFSI, healthcare, and government verticals are a third significant driver. Enterprises in these sectors must maintain detailed audit trails for process execution, approvals, and data handling. Cloud workflow platforms with built-in compliance logging capabilities directly address this requirement, reducing the manual documentation burden and mitigating regulatory risk exposure.

On the constraint side, data security and sovereignty concerns represent the most material barrier to cloud workflow adoption, particularly among organizations in highly regulated industries and in regions with strict data localization laws such as the European Union, Russia, and China. Enterprises with sensitive operational data are cautious about routing workflow metadata through third-party cloud infrastructure, creating adoption friction that vendors must address through regional data residency options and enhanced security certifications.

Integration complexity with legacy on-premises systems represents a second significant constraint. Many enterprises operate heterogeneous IT environments where core transactional systems — such as mainframe-based ERP platforms or proprietary manufacturing execution systems — lack modern API interfaces, making it technically challenging to extend cloud workflow orchestration into these environments without significant middleware investment.

Finally, talent shortages in cloud architecture and workflow design expertise constrain the speed at which enterprises can deploy and optimize cloud workflow platforms, particularly in mid-market and emerging-market contexts where technical staff availability is limited.

The competitive landscape of the Cloud Workflow Market is characterized by a diverse set of participants spanning large enterprise software conglomerates, specialized workforce management vendors, and emerging AI-native automation platforms. The following profiles outline the strategic positioning of key participants:

Ascentis Corporation: A cloud-based human capital management platform provider focused on mid-market enterprises, Ascentis integrates workflow automation across HR, payroll, and talent management, offering modular deployment options that reduce time-to-value for resource-constrained organizations.

Verint Systems Inc.: Specializing in customer engagement intelligence, Verint embeds cloud workflow capabilities within its workforce engagement management suite, enabling automated routing of customer service interactions and quality monitoring workflows for contact center environments.

SAP SE: One of the largest enterprise software vendors globally, SAP integrates cloud workflow orchestration deeply within its S/4HANA and Business Technology Platform ecosystems, serving multinational enterprises with complex cross-functional process automation requirements across finance, procurement, and HR domains.

MPEX Solutions: A provider of HR and payroll workflow solutions targeting the mid-market, MPEX Solutions focuses on automating compliance-intensive processes such as time and attendance tracking, benefits administration, and workforce scheduling.

Synel: A workforce management technology specialist, Synel delivers cloud workflow automation capabilities focused on time and attendance management, access control integration, and labor compliance reporting across manufacturing and services industries.

WorkForce Software, LLC: A global leader in workforce management cloud platforms, WorkForce Software automates complex scheduling, time tracking, and compliance workflows for large enterprises operating in highly regulated and geographically distributed environments.

Ultimate Software: Known for its UltiPro platform, Ultimate Software provides cloud-based HR workflow automation covering the full employee lifecycle, with particular strength in benefits enrollment, performance management, and payroll processing automation.

The Hackett Group, Inc: A strategic advisory and technology services firm, The Hackett Group supports enterprises in designing and benchmarking cloud workflow transformation programs, with a focus on best-practice process architectures for finance and HR operations.

Workday, Inc.: A dominant platform vendor in cloud-based HR and financial management, Workday delivers native workflow automation capabilities that orchestrate approval chains, compliance checks, and cross-module process flows within its unified cloud architecture.

IBM Corporation: IBM brings enterprise-grade cloud workflow automation through its IBM Cloud Pak for Business Automation portfolio, offering AI-infused workflow orchestration, content management, and decision management capabilities targeted at regulated industries.

TALOS Workforce Solutions: A specialized workforce management solutions provider, TALOS focuses on automating time and attendance, scheduling, and compliance workflows for industries with complex shift-based labor models.

March 2024: SAP SE announced the general availability of Joule, its AI copilot embedded within SAP workflows, enabling natural language-driven workflow creation and modification across its S/4HANA and SuccessFactors platforms, significantly lowering deployment barriers for non-technical users.

January 2024: IBM Corporation expanded its IBM Cloud Pak for Business Automation portfolio with enhanced generative AI capabilities, integrating large language model-based document processing into workflow orchestration pipelines to accelerate case management automation in banking and insurance.

November 2023: Workday, Inc. unveiled its Workday AI Marketplace, allowing third-party AI model providers to embed their capabilities directly into Workday workflow automation sequences, expanding the ecosystem of intelligent automation options available to enterprise customers.

September 2023: WorkForce Software, LLC completed a significant platform update introducing predictive scheduling workflows powered by machine learning, enabling automated shift assignment and compliance risk flagging for enterprises operating under complex labor regulations.

July 2023: Verint Systems Inc. launched its Da Vinci AI-enhanced workflow routing engine, enabling contact center workflow automation platforms to dynamically assign customer interactions based on real-time agent skill availability and predicted resolution complexity.

May 2023: Ultimate Software released expanded API connectivity features within its cloud workflow platform, enabling deeper integration with third-party payroll processors, benefits providers, and talent acquisition systems, reducing manual data transfer workflows.

February 2023: The Hackett Group, Inc published its annual Digital World Class study indicating that organizations leveraging cloud workflow automation in finance and HR operations achieved 25–40% lower process costs compared to peers relying on manual or on-premises workflow management.

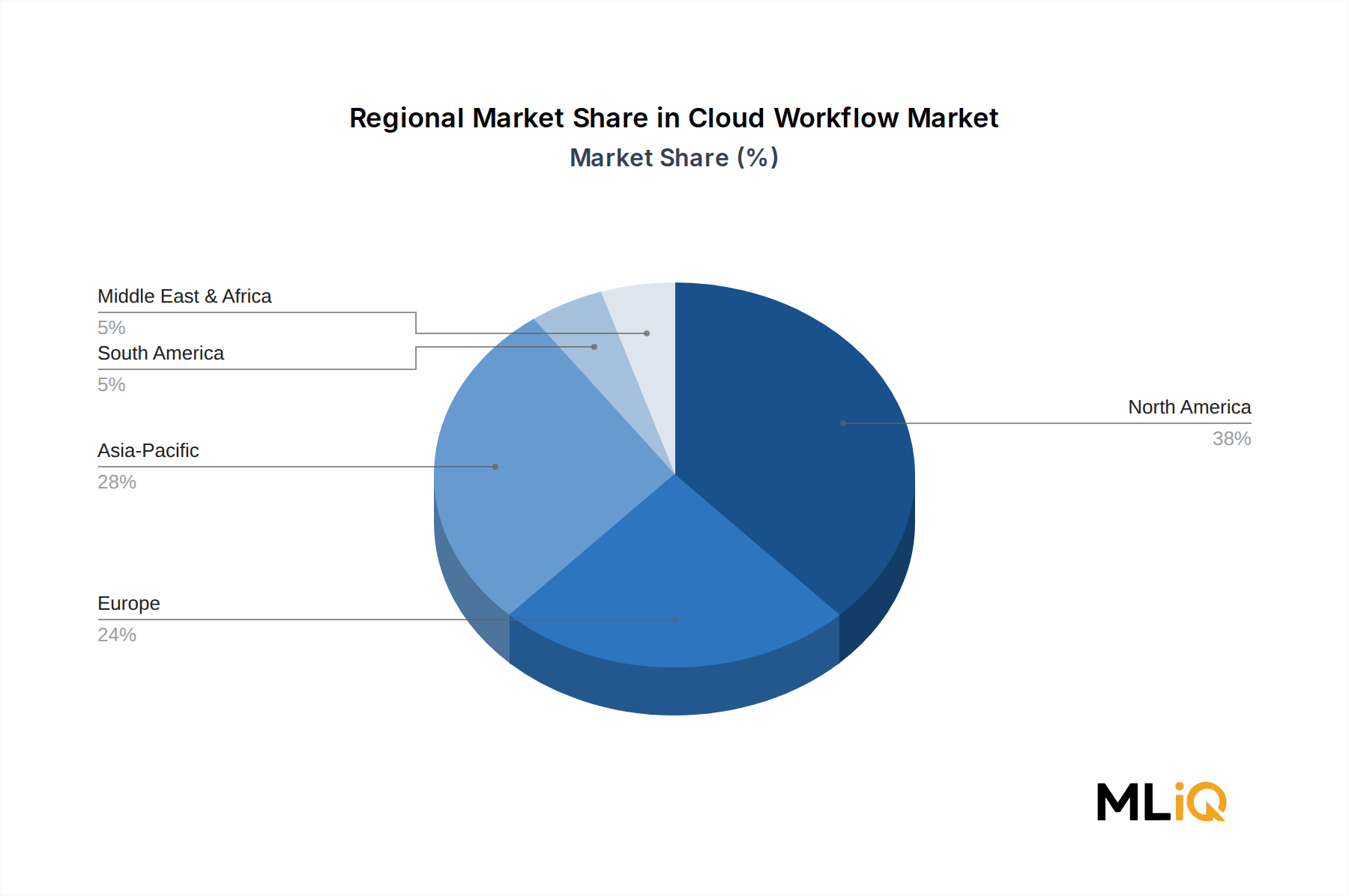

The Cloud Workflow Market exhibits meaningful regional variation in terms of adoption maturity, growth velocity, and primary demand drivers, reflecting differences in enterprise IT spending capacity, regulatory environments, and cloud infrastructure readiness.

North America represents the most mature and largest regional market, accounting for an estimated 38–42% of global revenues in 2023. The United States is the dominant contributor, driven by high enterprise cloud penetration, substantial IT budgets across BFSI, healthcare, and technology sectors, and a well-developed ecosystem of cloud workflow platform vendors headquartered in the region. Canada and Mexico contribute incrementally, with Canadian financial services and government agencies representing active buyers. North America's CAGR is estimated at approximately 14–15%, reflecting a market that is growing but from a comparatively larger base with established platform relationships.

Europe represents the second-largest regional market, with Germany, the United Kingdom, and France leading adoption among enterprise buyers. European market growth is materially influenced by GDPR compliance requirements, which have elevated demand for cloud workflow platforms with robust data lineage and audit trail capabilities. The region's CAGR is estimated at 15–16%, with the Nordics exhibiting above-average adoption rates driven by high digital maturity and public sector digitization programs.

Asia Pacific is identified as the fastest-growing regional market, with an estimated CAGR of 20–22% through the forecast period. China, India, Japan, and South Korea are the primary demand centers. India's large IT services sector and rapidly digitalizing BFSI and retail industries are driving particularly strong platform adoption. China's domestic cloud ecosystem and government-driven enterprise digitization programs are generating significant workflow automation investment, while Japan and South Korea represent mature but growing markets with strong manufacturing and telecommunications sector demand.

The Middle East and Africa region is an emerging market for cloud workflow adoption, with GCC countries — particularly Saudi Arabia and the UAE — leading investment driven by Vision 2030-aligned digital government and smart enterprise programs. South Africa represents the most developed sub-Saharan market. Regional CAGR is estimated at 18–19%, supported by sovereign cloud infrastructure investments and increasing enterprise IT maturity.

South America, led by Brazil and Argentina, represents the smallest but increasingly relevant regional segment, with cloud workflow adoption accelerating among retail, financial services, and manufacturing enterprises seeking operational efficiency gains. Infrastructure constraints and currency volatility temper growth, but the region's CAGR is estimated at 16–17% as cloud penetration deepens.

The Cloud Workflow Market has attracted sustained and diversifying investment activity over the 2022–2024 period, reflecting investor confidence in the long-term structural demand for process automation capabilities across enterprise verticals.

Venture capital flows have been particularly concentrated in AI-native workflow automation startups that differentiate through intelligent process discovery, autonomous task execution, and generative AI-powered workflow design. Platforms integrating large language models into workflow creation and optimization interfaces have commanded premium valuations, with several Series B and Series C rounds in the $50–$150 million range closed by specialized vendors during 2023 and 2024.

Strategic M&A activity has been dominated by large platform vendors seeking to acquire point solution capabilities in adjacent domains. Acquisitions targeting document intelligence, robotic process automation, and API management capabilities have been particularly common, as workflow platform vendors seek to expand the breadth of automation they can deliver natively within their platforms rather than relying on third-party integrations.

The sub-segments attracting the most capital include AI-enhanced workflow orchestration, customer service workflow automation, and HR process automation. Investors are drawn to these segments by their combination of large addressable markets, high switching costs once deployed, and demonstrated ROI metrics that support enterprise budget justification cycles.

Private equity activity has also increased, with several workflow automation platform vendors receiving growth equity investments to fund international expansion and product development acceleration. The convergence of cloud workflow capabilities with the broader Business Process Automation Market, the Workflow Automation Software Market, and the Robotic Process Automation Market

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 17.26% from 2020-2034 |

| Segmentation |

|

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Comprehensive validation mechanisms ensuring market intelligence accuracy, reliability, and adherence to international standards.

500+ data sources cross-validated

200+ industry specialists validation

NAICS, SIC, ISIC, TRBC standards

Continuous market tracking updates

Factors such as are projected to boost the Cloud Workflow Market market expansion.

Key companies in the market include Ascentis Corporation, Verint Systems Inc., SAP SE, MPEX Solutions, Synel, WorkForce Software, LLC, Ultimate Software, The Hackett Group, Inc, Workday, Inc., IBM Corporation, TALOS Workforce Solutions.

The market segments include Type, Business Workflow, Enterprise Size, Industry Vertical.

The market size is estimated to be USD 0.81 billion as of 2022.

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3690, USD 5820, and USD 9870 respectively.

The market size is provided in terms of value, measured in billion and volume, measured in .

Yes, the market keyword associated with the report is "Cloud Workflow Market," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Cloud Workflow Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.