1. What are the major growth drivers for the Customer Relationship Management Market market?

Factors such as are projected to boost the Customer Relationship Management Market market expansion.

Customer Relationship Management Market

Customer Relationship Management Market

Market Lens IQ is a global market intelligence and strategic consulting firm delivering advanced syndicated research reports, customized industry analysis, competitive intelligence, and data-driven advisory solutions to organizations across international markets. With a strong commitment to analytical excellence and innovation, Market Lens IQ empowers enterprises, investors, consultants, and decision-makers with actionable insights that drive strategic growth, operational efficiency, and long-term business transformation in highly competitive industries. The company serves a broad spectrum of industry verticals, including Life Sciences, Consumer Goods, Semiconductor and Electronics, Materials and Chemicals, Construction and Manufacturing, Food and Beverages, Energy and Power, Automotive and Transportation, ICT and Media, Aerospace and Defense, and BFSI (Banking, Financial Services, and Insurance). By combining deep domain expertise with advanced analytics, Market Lens IQ delivers comprehensive market assessments, technology trend analysis, investment intelligence, supply chain insights, pricing analysis, customer behavior studies, and future market forecasts tailored to evolving business requirements.

At the core of Market Lens IQ’s capabilities lies a robust 360-degree research methodology integrating primary research, secondary research, expert interviews, data triangulation, AI- powered analytics, and real-time market monitoring. Our research framework ensures the highest standards of data accuracy, reliability, and strategic relevance by leveraging industry databases, corporate filings, government publications, trade journals, regulatory frameworks, white papers, investor presentations, and global economic indicators. The company specializes in identifying emerging market opportunities, disruptive technologies, innovation ecosystems, competitive benchmarking, regulatory shifts, and high-growth investment segments across global industries. Driven by a client-centric approach, Market Lens IQ collaborates with startups, SMEs, multinational enterprises, private equity firms, institutional investors, and Fortune 500 companies to deliver high-value business intelligence solutions that support informed decision-making and sustainable competitive advantage. Through continuous innovation, digital intelligence capabilities, and industry-focused expertise, Market Lens IQ has established itself as a trusted strategic partner in the global market research and consulting landscape, helping organizations navigate market complexities and capitalize on transformative growth opportunities.

+1 2315155523

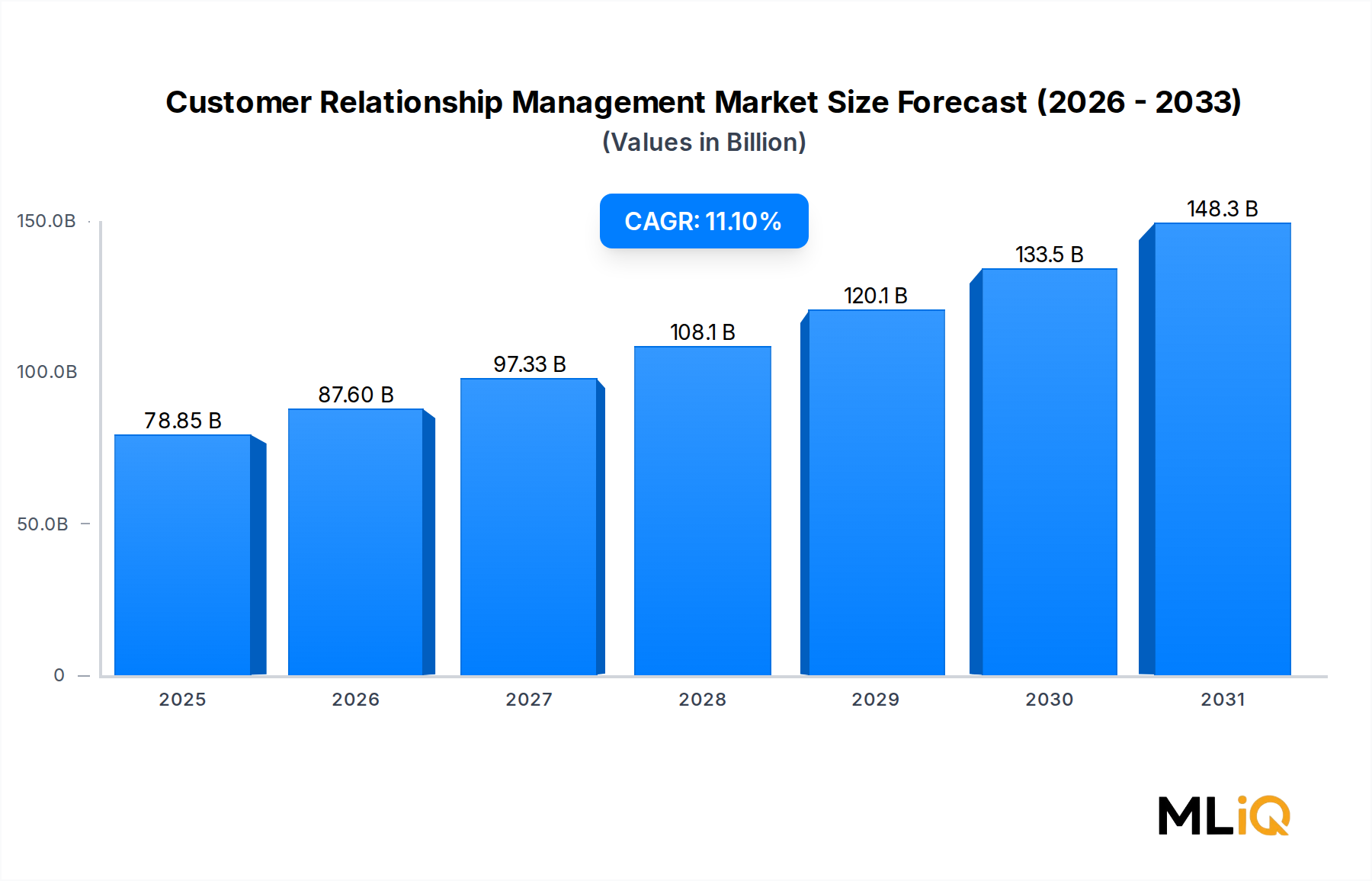

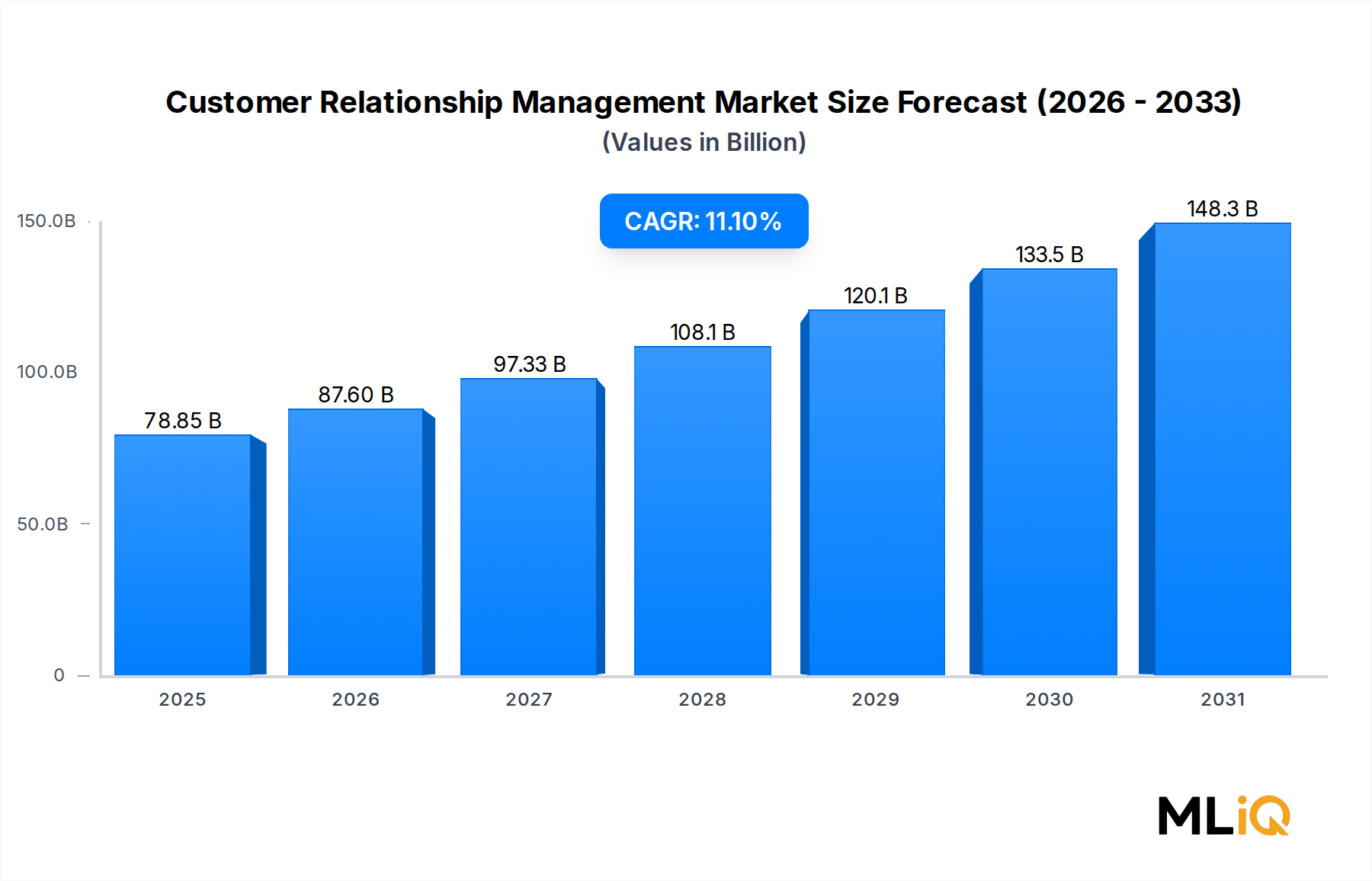

The global Customer Relationship Management Market is positioned at a pivotal inflection point, reflecting the accelerating convergence of digital transformation imperatives and enterprise demand for unified customer engagement platforms. As of the base assessment period, the market is valued at $78.85 billion, with projections indicating robust expansion through 2033 driven by a compound annual growth rate (CAGR) of 11.1%. This trajectory places the market among the most dynamic segments within the broader ICT and Media category, surpassing many adjacent technology verticals in sustained momentum.

At the macroeconomic level, enterprises across industries are redirecting capital toward customer-centric technologies as competitive differentiation increasingly hinges on data-driven engagement rather than product features alone. The proliferation of omnichannel customer journeys, the maturation of cloud infrastructure, and the integration of artificial intelligence into CRM workflows are the primary catalysts shaping near- and medium-term demand. Businesses are no longer treating CRM platforms as back-office tools; they are now strategic nerve centers for revenue operations, customer lifecycle management, and predictive analytics.

The shift toward subscription-based, cloud-native deployment models has fundamentally altered the cost structure for buyers, enabling small and medium-sized enterprises (SMEs) to access enterprise-grade CRM capabilities that were previously cost-prohibitive. This democratization of CRM access is expanding the total addressable market significantly, particularly in emerging economies across Asia Pacific, Latin America, and the Middle East.

Key demand drivers include the surge in e-commerce and digital retail, regulatory pressure around data privacy compliance, and the rising expectation from consumers for hyper-personalized interactions. Organizations in the BFSI, healthcare, and retail sectors are allocating disproportionately higher CRM budgets relative to other IT expenditures, reflecting the mission-critical nature of customer data management in these verticals.

Looking forward through 2033, the market is expected to benefit from deepening AI and machine learning integration, the mainstreaming of conversational interfaces, and the proliferation of industry-specific CRM solutions tailored for verticals such as manufacturing, government, and media. The competitive landscape is intensifying as both established vendors and emerging challengers race to offer differentiated capabilities in areas such as predictive lead scoring, sentiment analysis, and real-time customer journey orchestration. The overall outlook for the Customer Relationship Management Market remains strongly positive, with secular tailwinds reinforcing sustained double-digit growth across the forecast horizon.

Among all deployment models within the Customer Relationship Management Market, the cloud segment commands the largest revenue share and continues to consolidate its position as the de facto standard for enterprise CRM deployment. This dominance is attributable to a confluence of structural, economic, and operational factors that collectively make cloud-based CRM superior for the majority of organizational profiles.

Cloud-based CRM solutions offer compelling advantages over legacy on-premise systems, including lower upfront capital expenditure, automatic updates and feature rollouts, seamless scalability, and native integration with other cloud-native applications such as marketing automation suites, data analytics platforms, and communication tools. The managed-service model eliminates the burden of internal IT maintenance, which is particularly valuable for organizations with lean technology teams.

The transition from on-premise to cloud CRM has been further accelerated by the widespread adoption of remote and hybrid work models, which require that customer-facing teams access CRM data from geographically dispersed locations. Cloud infrastructure inherently supports this mobility without the complex virtual private network configurations and security overhead associated with on-premise systems.

Salesforce.com, Inc. remains the uncontested leader within the cloud CRM sub-segment, holding the largest share of cloud-based CRM revenue globally. Its platform ecosystem, anchored by products such as Sales Cloud, Service Cloud, and Marketing Cloud, continues to expand through acquisitions and native AI capability enhancements under the Salesforce Einstein and Agentforce initiatives. Microsoft Corporation's Dynamics 365 suite has gained substantial ground by leveraging deep integration with the Microsoft 365 productivity stack and Azure cloud infrastructure, creating a compelling bundled value proposition for enterprise customers already embedded in the Microsoft ecosystem.

Oracle Corporation and SAP SE serve the upper tier of the enterprise market, offering cloud CRM modules tightly coupled with their broader ERP and data management platforms. This bundling strategy creates high switching costs and reinforces existing enterprise relationships, enabling both vendors to maintain stable revenue within large account segments. Zoho Corporation Pvt. Ltd. has carved a significant niche in the SME cloud CRM segment, offering a competitively priced yet feature-rich platform that competes directly with Salesforce and HubSpot at the mid-market level.

The hybrid deployment sub-segment is gaining traction among regulated industries such as BFSI and government, where data residency and sovereignty requirements mandate that certain customer data remain on-premise while still enabling cloud-based analytics and engagement layers. This architectural flexibility is prompting vendors to build more sophisticated hybrid orchestration capabilities into their platforms.

From a revenue concentration standpoint, cloud CRM now accounts for the dominant share of total market revenue and is projected to sustain its growth premium relative to on-premise through the forecast period ending 2033. The ongoing retirement of legacy CRM licenses and the migration of enterprise workloads to cloud environments will continue to funnel incremental spend into cloud platforms. Additionally, the emergence of industry cloud models — where CRM functionality is pre-configured for specific verticals such as financial services, healthcare, and retail — is creating new growth vectors within the cloud segment by reducing implementation complexity and time-to-value for buyers in those sectors.

Overall, the cloud segment's dominance reflects a market in structural maturation, where the debate over deployment model has been decisively resolved in favor of cloud-native architectures for the vast majority of use cases.

The Customer Relationship Management Market is propelled by several quantifiable and structurally durable drivers, while also navigating meaningful constraints that modulate the pace of adoption across segments and regions.

AI and machine learning integration is the most consequential current driver. Enterprises deploying AI-augmented CRM systems report measurable improvements in lead conversion rates, customer retention scores, and service resolution times. Vendors are embedding generative AI capabilities into core CRM workflows, including automated email drafting, real-time call summarization, and predictive churn modeling. This AI-driven value creation is compressing sales cycles and elevating the average contract value per CRM deployment.

The exponential growth of customer touchpoint data is a second structural driver. Modern consumers interact with brands across an average of six or more channels simultaneously, generating data volumes that manual CRM processes cannot efficiently process. Automated data ingestion, enrichment, and segmentation capabilities within advanced CRM platforms directly address this complexity, making CRM investment a necessity rather than an option for data-mature organizations.

Rising customer experience expectations are quantifiably reshaping enterprise software budgets. Industry surveys consistently indicate that organizations prioritizing customer experience outperform peers on revenue growth metrics. This business case clarity is driving CRM budget allocations upward, particularly in retail, financial services, and healthcare verticals where customer lifetime value is a primary performance metric.

On the constraint side, data privacy and sovereignty regulations represent a significant friction factor. Frameworks such as the General Data Protection Regulation in Europe and the California Consumer Privacy Act in the United States impose strict requirements on how CRM systems collect, store, and process personal data. Compliance overhead increases implementation complexity and ongoing operational costs, creating a barrier particularly for SMEs with limited legal and technical resources.

High implementation costs and integration complexity remain persistent challenges, especially for mid-market organizations migrating from legacy systems. The total cost of ownership for enterprise CRM deployments, when accounting for customization, training, and ongoing administration, can substantially exceed the headline software licensing or subscription cost, creating budget overruns and delayed ROI realization that temper adoption enthusiasm.

The competitive landscape of the Customer Relationship Management Market is characterized by a tiered structure of global platform vendors, specialized niche providers, and fast-growing regional challengers. The following profiles reflect the strategic positioning of key participants:

AUREA SOFTWARE INC: Aurea Software focuses on delivering high-volume customer engagement and communication management solutions, with particular strength in email marketing and lifecycle automation capabilities targeted at enterprises with complex customer base management requirements.

INSIGHTLY, INC: Insightly positions itself as a unified CRM and project management platform tailored for growing mid-market businesses, differentiating through seamless integration of post-sale project delivery workflows with traditional sales and marketing CRM functions.

MICROSOFT CORPORATION: Microsoft Corporation leverages its dominant enterprise productivity ecosystem, integrating Dynamics 365 CRM deeply with Teams, Outlook, and Azure to offer a differentiated workflow-embedded CRM experience that reduces context-switching friction for enterprise users.

ORACLE CORPORATION: Oracle Corporation offers the Oracle Fusion CX suite as part of its broader cloud applications portfolio, targeting large enterprises with complex multi-channel customer engagement requirements and tight integration needs with Oracle ERP and data management infrastructure.

PEGASYSTEMS: Pegasystems differentiates through its AI-driven decisioning engine and low-code application development platform, enabling enterprises to build highly customized CRM workflows without extensive custom coding, with particular strength in financial services and insurance verticals.

SAGE GROUP: Sage Group serves small and medium-sized businesses with integrated CRM and accounting solutions, leveraging its existing financial management customer base to drive CRM cross-sell adoption particularly in the United Kingdom and European markets.

SALESFORCE.COM, INC: Salesforce.com, Inc. maintains the largest global market share in enterprise CRM, driven by its expansive AppExchange ecosystem, aggressive AI investment through the Einstein and Agentforce platforms, and a comprehensive suite spanning sales, service, marketing, and commerce functions.

SAP SE: SAP SE integrates CRM functionality within its SAP Customer Experience suite, targeting large enterprises already operating on SAP S/4HANA ERP platforms and seeking unified front-office and back-office data consistency.

SUGARCRM: SugarCRM focuses on delivering flexible, open-architecture CRM for mid-market organizations that require high configurability and on-premise or private cloud deployment options, competing on total cost of ownership advantages relative to Salesforce.

ZOHO CORPORATION PVT. LTD: Zoho Corporation Pvt. Ltd. has built one of the fastest-growing CRM platforms globally by offering a comprehensive suite of over 45 integrated business applications at highly competitive price points, with particular momentum in SME and emerging market segments.

January 2025: Salesforce.com, Inc. announced the general availability of Agentforce 2.0, expanding autonomous AI agent capabilities within its CRM platform to support proactive customer outreach, case resolution, and pipeline management without human intervention.

February 2025: Microsoft Corporation introduced enhanced Copilot AI features within Dynamics 365, enabling natural language querying of CRM data and automated meeting summary generation directly within the CRM workflow interface.

March 2025: Oracle Corporation launched new Oracle Fusion CX industry accelerators for financial services and healthcare, offering pre-built data models and compliance workflows designed to reduce CRM implementation timelines by up to 40% for regulated industry clients.

April 2025: Zoho Corporation Pvt. Ltd. expanded its data center footprint by announcing new regional cloud infrastructure in the Middle East and South Asia, addressing data residency requirements for enterprise customers in those geographies.

April 2025: Pegasystems released an updated version of its Pega Customer Decision Hub, incorporating real-time next-best-action recommendations powered by large language model integration, targeting financial services and telecommunications verticals.

May 2025: SAP SE deepened its partnership with Databricks to enable native CRM data lakehouse connectivity within SAP Customer Experience, allowing enterprises to run advanced analytics and AI models directly on unified customer data.

May 2025: SugarCRM announced a strategic integration partnership with LinkedIn Sales Navigator, enabling automated prospect data enrichment and engagement tracking directly within the SugarCRM platform for sales teams.

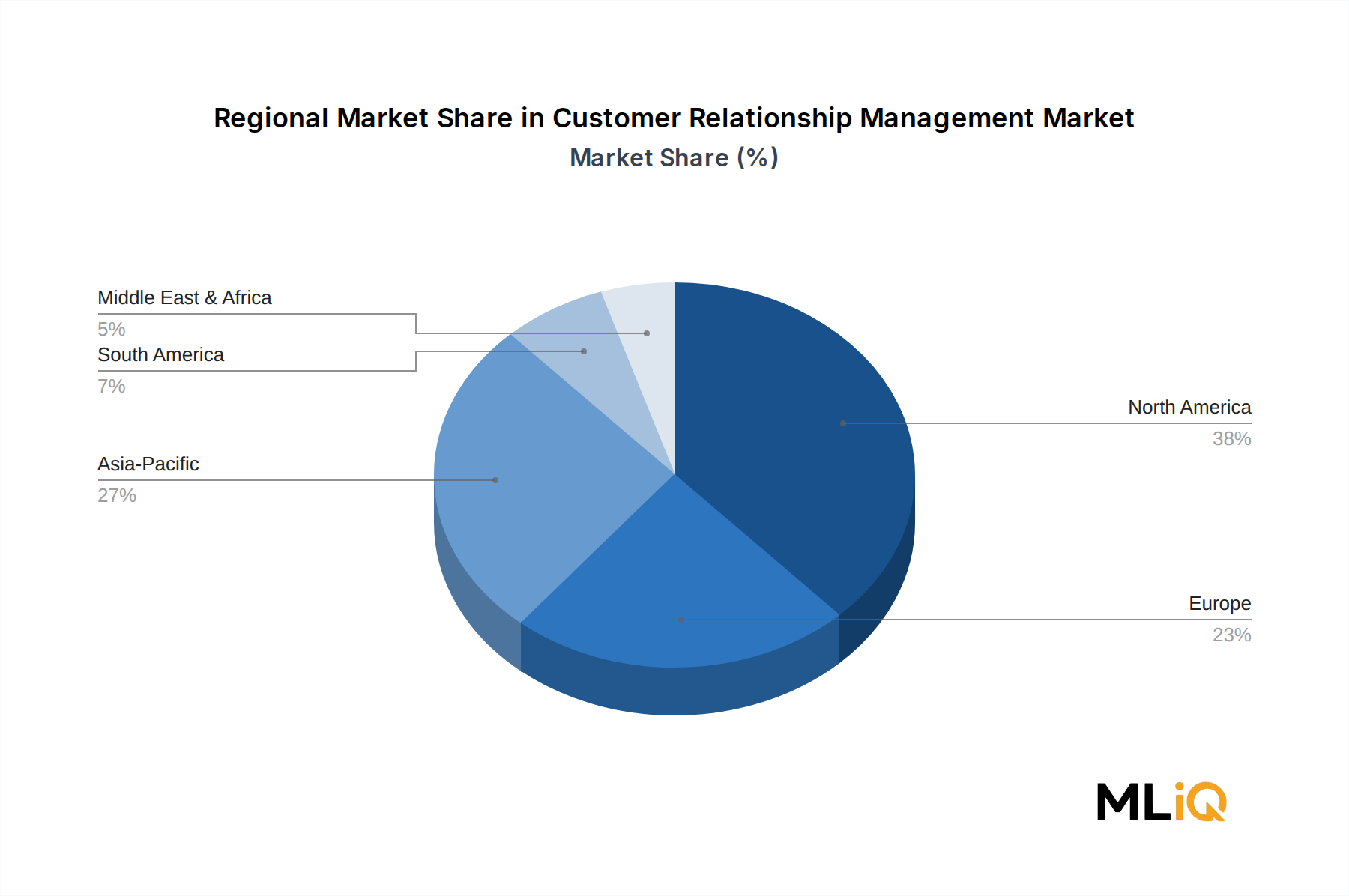

The Customer Relationship Management Market exhibits meaningful regional heterogeneity in terms of growth rates, adoption maturity, and demand drivers, with North America, Europe, Asia Pacific, and the Middle East and Africa representing distinct investment and growth profiles.

North America is the most mature and largest revenue-generating region in the Customer Relationship Management Market, accounting for the largest share of global revenue. The United States alone represents the single largest national market, driven by high enterprise technology spending, early cloud adoption, and the headquarters concentration of major CRM vendors including Salesforce, Oracle, and Microsoft. Growth in North America is characterized by upsell and expansion dynamics within existing customer bases, AI feature monetization, and vertical cloud adoption across financial services and healthcare. The regional CAGR for North America tracks slightly below the global average, reflecting market saturation in large enterprise segments, though SME penetration continues to drive incremental volume.

Europe represents the second-largest regional market, with Germany, the United Kingdom, and France as the primary contributors. European growth is moderated by stringent data privacy regulations under the GDPR framework, which adds compliance complexity to CRM deployments. However, demand from the BFSI and manufacturing sectors remains robust, and the ongoing digitalization of public sector services is creating new government CRM opportunities. European CRM adoption is also characterized by a preference for hybrid and on-premise deployment models among regulated industries.

Asia Pacific is the fastest-growing regional segment within the Customer Relationship Management Market, with a regional CAGR materially above the global average. China, India, Japan, and South Korea are the leading national markets, each exhibiting distinct demand characteristics. India's growth is driven by the expansion of domestic technology services companies and SME digitalization, while China's market reflects rising enterprise CRM adoption among multinational corporations and domestic platforms. The ASEAN cluster is emerging as a high-potential sub-region driven by e-commerce expansion and financial services modernization.

The Middle East and Africa region, while smaller in absolute terms, is exhibiting accelerating growth supported by government-led digital transformation initiatives, particularly in GCC countries such as Saudi Arabia and the UAE. South Africa leads African CRM adoption, with financial services and telecommunications as primary verticals.

Latin America, anchored by Brazil and Argentina, is growing steadily, with cloud CRM adoption rising among retail and financial services firms seeking to improve customer retention amid competitive market dynamics.

The Customer Relationship Management Market, as a software-centric industry, does not face the same raw material dependencies as manufacturing-intensive sectors; however, it is deeply embedded within a complex technology supply chain that introduces meaningful upstream risks and cost dynamics.

The primary upstream dependency for CRM platforms is cloud infrastructure, which itself relies on semiconductor components, data center hardware, and energy inputs. Semiconductor shortages, which significantly disrupted global technology supply chains during 2021 and 2022, had downstream effects on cloud infrastructure expansion timelines. Reduced availability of advanced processors and memory chips constrained data center buildout by major hyperscalers including Amazon Web Services, Microsoft Azure, and Google Cloud, creating temporary capacity constraints that affected CRM platform scalability and new customer onboarding speeds.

Server hardware and data center cooling systems represent critical physical inputs for the cloud infrastructure on which CRM SaaS platforms operate. Prices for server-grade DRAM and NAND flash memory experienced significant volatility between 2020 and 2024, with price fluctuations of up to 30–40% year-over-year influencing the capital expenditure forecasts of cloud providers, and by extension the cost structures of CRM vendors hosting on those platforms.

Energy costs are an increasingly significant input for data center operations supporting CRM workloads. Rising electricity prices in Europe following 2022 geopolitical disruptions increased operational costs for data centers hosting European CRM workloads, prompting some vendors to accelerate investments in renewable energy sourcing and energy-efficient cooling technologies to protect margin profiles.

Talent supply chains represent a non-physical but equally critical input for the CRM market. Software engineers, AI/ML researchers, and implementation consultants are in sustained high demand, creating wage inflation pressures that affect both vendor R&D costs and the partner ecosystem fees charged to customers for CRM implementation services.

The broader Data Analytics Market and Business Intelligence Market supply chain dynamics also influence CRM platform development, as data processing frameworks, open-source libraries, and third-party API integrations form foundational components of modern CRM analytics functionality. Licensing cost changes or deprecation events within these dependency layers can create unexpected development cost escalations for CRM vendors.

Vendors are responding to supply chain risk by increasing

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 11.1% from 2020-2034 |

| Segmentation |

|

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Comprehensive validation mechanisms ensuring market intelligence accuracy, reliability, and adherence to international standards.

500+ data sources cross-validated

200+ industry specialists validation

NAICS, SIC, ISIC, TRBC standards

Continuous market tracking updates

Factors such as are projected to boost the Customer Relationship Management Market market expansion.

Key companies in the market include AUREA SOFTWARE INC, INSIGHTLY, INC, MICROSOFT CORPORATION, ORACLE CORPORATION, PEGASYSTEMS, SAGE GROUP, SALESFORCE.COM, INC, SAP SE, SUGARCRM, ZOHO CORPORATION PVT. LTD.

The market segments include Component, Deployment Model, Organization size, Application, Industry Vertical.

The market size is estimated to be USD 78.85 billion as of 2022.

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3713, USD 5770, and USD 10665 respectively.

The market size is provided in terms of value, measured in billion and volume, measured in .

Yes, the market keyword associated with the report is "Customer Relationship Management Market," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Customer Relationship Management Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.