1. What are the major growth drivers for the Cloud Application Security Market market?

Factors such as are projected to boost the Cloud Application Security Market market expansion.

+1 2315155523

Cloud Application Security Market

Cloud Application Security Market

Market Lens IQ is a global market intelligence and strategic consulting firm delivering advanced syndicated research reports, customized industry analysis, competitive intelligence, and data-driven advisory solutions to organizations across international markets. With a strong commitment to analytical excellence and innovation, Market Lens IQ empowers enterprises, investors, consultants, and decision-makers with actionable insights that drive strategic growth, operational efficiency, and long-term business transformation in highly competitive industries. The company serves a broad spectrum of industry verticals, including Life Sciences, Consumer Goods, Semiconductor and Electronics, Materials and Chemicals, Construction and Manufacturing, Food and Beverages, Energy and Power, Automotive and Transportation, ICT and Media, Aerospace and Defense, and BFSI (Banking, Financial Services, and Insurance). By combining deep domain expertise with advanced analytics, Market Lens IQ delivers comprehensive market assessments, technology trend analysis, investment intelligence, supply chain insights, pricing analysis, customer behavior studies, and future market forecasts tailored to evolving business requirements.

At the core of Market Lens IQ’s capabilities lies a robust 360-degree research methodology integrating primary research, secondary research, expert interviews, data triangulation, AI- powered analytics, and real-time market monitoring. Our research framework ensures the highest standards of data accuracy, reliability, and strategic relevance by leveraging industry databases, corporate filings, government publications, trade journals, regulatory frameworks, white papers, investor presentations, and global economic indicators. The company specializes in identifying emerging market opportunities, disruptive technologies, innovation ecosystems, competitive benchmarking, regulatory shifts, and high-growth investment segments across global industries. Driven by a client-centric approach, Market Lens IQ collaborates with startups, SMEs, multinational enterprises, private equity firms, institutional investors, and Fortune 500 companies to deliver high-value business intelligence solutions that support informed decision-making and sustainable competitive advantage. Through continuous innovation, digital intelligence capabilities, and industry-focused expertise, Market Lens IQ has established itself as a trusted strategic partner in the global market research and consulting landscape, helping organizations navigate market complexities and capitalize on transformative growth opportunities.

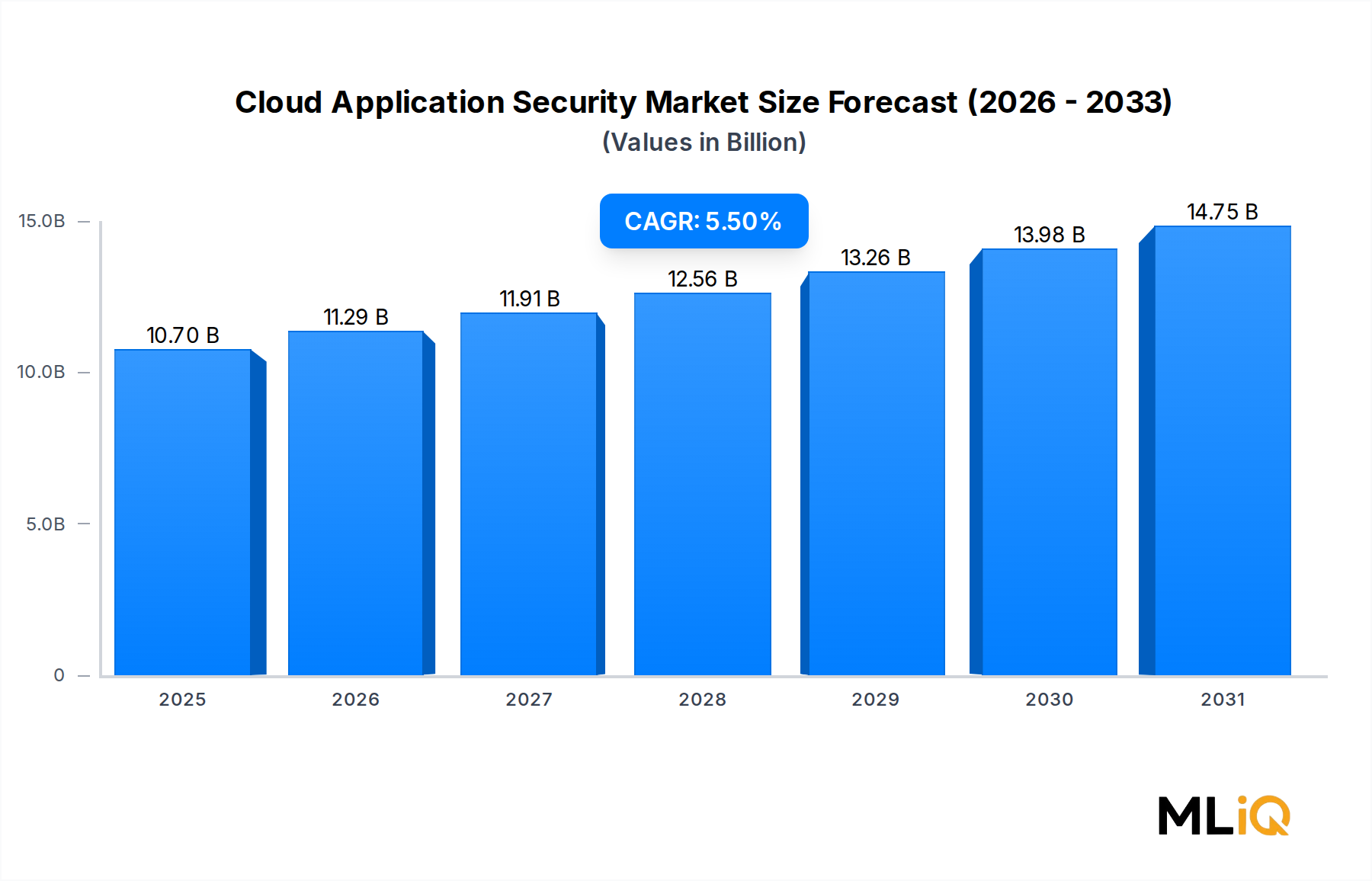

The global Cloud Application Security Market was valued at $10.7 billion in 2024 and is projected to expand at a compound annual growth rate (CAGR) of 5.5% through the forecast period, reflecting sustained and broad-based enterprise demand for robust cloud-native security frameworks. As organizations accelerate digital transformation initiatives and migrate critical workloads to multi-cloud and hybrid environments, the exposure surface for application-layer threats has widened substantially, making cloud application security a non-discretionary investment category for enterprises across verticals.

Several macro tailwinds are reinforcing the market's expansion trajectory. The proliferation of Software-as-a-Service (SaaS) applications has fundamentally altered the enterprise attack surface, with the average enterprise now deploying more than 130 SaaS applications according to industry surveys. Simultaneously, regulatory mandates — including the General Data Protection Regulation (GDPR) in Europe, HIPAA in the United States healthcare sector, and PCI DSS in financial services — are compelling organizations to implement application-level data protection controls that align with compliance requirements.

The rise of remote and hybrid work models, accelerated by the global pandemic, has also driven a structural shift in how security perimeters are defined. Traditional network-boundary defenses are increasingly inadequate as employees access cloud applications from unmanaged devices and external networks. This has catalyzed demand for cloud-native application protection platforms (CNAPPs), cloud workload protection platforms (CWPPs), and related tooling.

Artificial intelligence and machine learning integration within security solutions is emerging as a critical differentiator, enabling real-time anomaly detection, behavioral analytics, and automated threat response at scale. Vendors that embed AI-driven capabilities into their platforms are gaining traction, particularly among large enterprise customers with complex, distributed application portfolios.

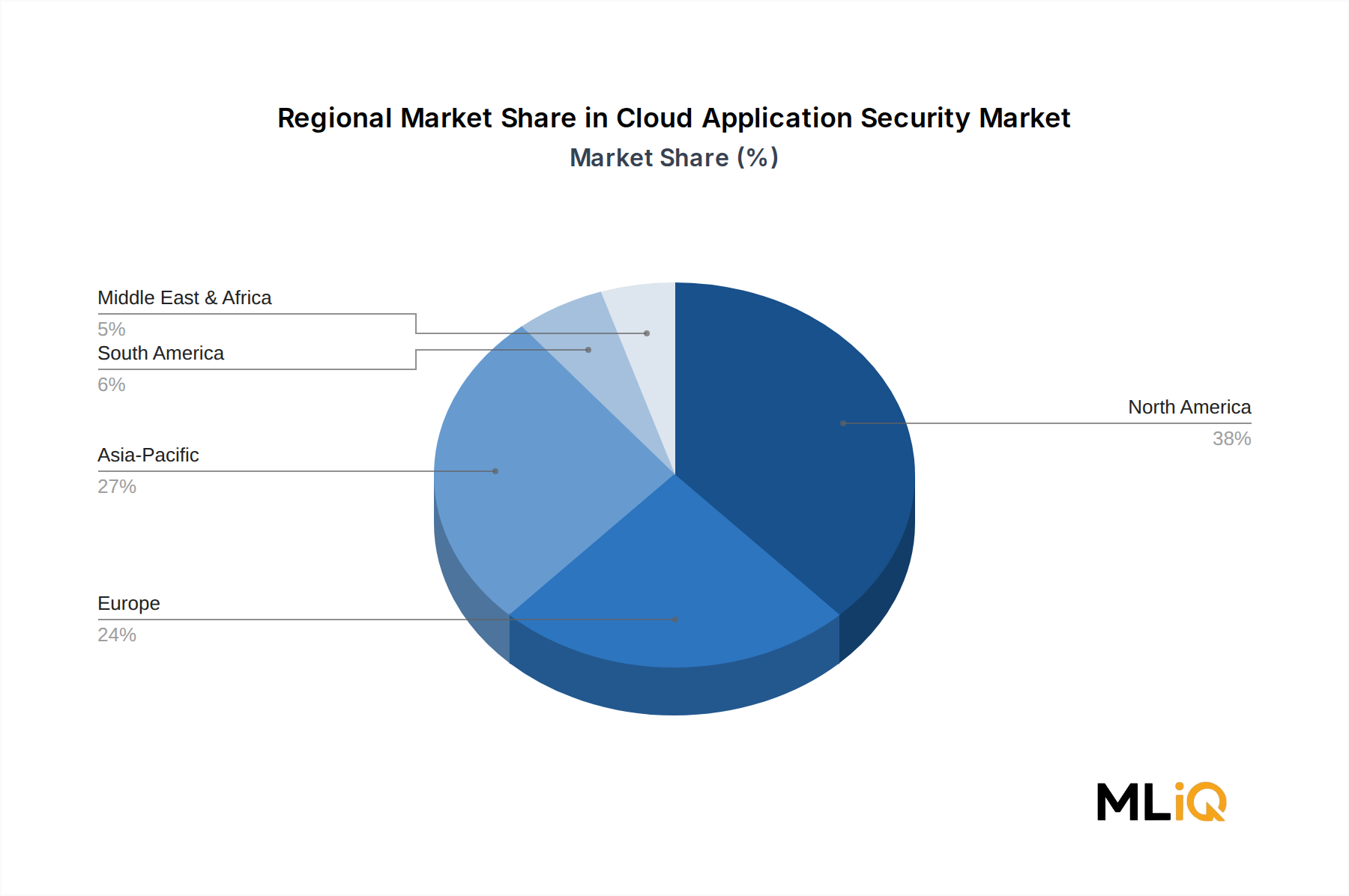

Geographically, North America remains the dominant revenue contributor, underpinned by high cloud adoption rates, a mature regulatory landscape, and significant enterprise IT security budgets. However, Asia Pacific is emerging as the fastest-growing region, driven by rapid digitalization in China, India, South Korea, and the broader ASEAN cluster. Europe maintains a stable mid-tier position, shaped significantly by GDPR compliance imperatives.

Looking forward, the convergence of cloud application security with adjacent disciplines — including the Cloud Access Security Broker Market, the Zero Trust Security Market, and the Identity and Access Management Market — is expected to reshape solution architectures, vendor positioning, and buyer procurement patterns through the latter half of the decade.

Within the component segmentation of the Cloud Application Security Market, the Solutions sub-segment commands the largest revenue share and is expected to maintain its dominance throughout the forecast period. This primacy reflects the fundamental reality that enterprises prioritize deploying technology platforms — spanning threat detection engines, data loss prevention (DLP) modules, encryption gateways, and API security tools — before procuring associated managed services or professional consulting engagements.

Cloud application security solutions encompass a broad and technically heterogeneous product landscape. Core categories include cloud-native application protection platforms (CNAPPs), which unify workload security, configuration management, and runtime protection into a single control plane. Additionally, web application firewalls (WAFs), API gateways with embedded security intelligence, and identity-aware proxy solutions constitute high-demand product categories. The Web Application Firewall Market, for example, represents a closely adjacent and sometimes overlapping solution segment that many cloud application security vendors have absorbed into broader platform offerings.

The dominance of the solutions segment is reinforced by several structural dynamics. First, enterprise security teams typically lead procurement cycles, and they prioritize technology platforms that offer measurable, auditable security outcomes — such as reduced mean time to detect (MTTD) and mean time to respond (MTTR) — over service-led engagements. Second, the SaaS delivery model for cloud security solutions dramatically lowers deployment friction, enabling enterprises to activate new security capabilities within days rather than months. Third, the solutions segment benefits from the compounding effect of platform consolidation: as enterprises seek to reduce the number of point solutions in their security stacks, integrated platforms that bundle multiple capabilities — such as CASB, DLP, and threat intelligence — generate higher per-customer revenue.

Key vendors driving the solutions segment include Palo Alto Networks, Cisco Systems, Microsoft, and Netskope, each of which has invested heavily in building platform-centric architectures that aggregate multiple cloud security capabilities under unified policy engines. Microsoft, in particular, leverages its native integration with Azure Active Directory and Microsoft 365 to provide seamless cloud application security controls for its vast installed base of enterprise customers, creating significant switching-cost moats.

Fortinet and Symantec (now part of Broadcom) maintain strong positions through their legacy enterprise customer relationships, using established distribution channels to cross-sell cloud application security solutions to on-premises security buyers transitioning to cloud environments.

The solutions segment's revenue share is not only growing in absolute terms but is also expanding relative to the services sub-segment, as automation and AI-driven orchestration reduce the manual intervention required to configure, tune, and manage cloud security platforms. However, the services segment is expected to post stronger growth rates in certain emerging markets, where in-house security expertise remains scarce and managed security service providers (MSSPs) fill the capability gap.

From a vertical perspective, the BFSI segment represents the largest end-user cluster for cloud application security solutions, driven by the sector's stringent regulatory requirements, high data sensitivity, and advanced IT maturity. The healthcare and IT/telecom verticals follow as significant solution consumers, each with distinct compliance and operational drivers.

The Cloud Application Security Market is shaped by a constellation of quantifiable drivers and countervailing constraints that collectively determine the pace and character of market expansion.

Primary driver: Accelerating cloud workload migration. Enterprise cloud spending surpassed $670 billion globally in 2023, with application workloads representing the single largest spending category. As more applications move to cloud-native architectures built on microservices and containers, the attack surface expands proportionally, creating direct demand for cloud application security tooling. The shift to DevSecOps methodologies — integrating security into CI/CD pipelines — is further broadening the addressable market.

Secondary driver: Regulatory compliance pressure. In 2023, the SEC in the United States introduced mandatory cybersecurity incident disclosure rules for public companies, requiring material breaches to be reported within four business days. This regulatory development has elevated board-level attention to cloud application security investments, accelerating budget approval cycles across publicly listed enterprises. Similarly, the EU's NIS2 Directive, effective October 2024, extended cybersecurity obligations to a wider range of critical infrastructure operators.

Third driver: Sophisticated threat landscape. The volume of API-targeted attacks increased by more than 300% between 2021 and 2023, according to security intelligence reports, reflecting adversaries' recognition that application layers represent the path of least resistance in cloud environments. This threat escalation is a direct procurement catalyst for API security and WAF solutions.

Primary constraint: Talent scarcity. The global cybersecurity workforce gap stood at approximately 4 million unfilled positions as of 2023, limiting enterprises' ability to deploy, configure, and operationalize increasingly complex cloud security platforms. This constraint particularly affects small and medium-sized enterprises (SMEs), which lack the internal expertise to maximize ROI from sophisticated solutions.

Secondary constraint: Integration complexity. The average enterprise security stack comprises more than 45 discrete tools, and integrating cloud application security solutions with existing SIEM, SOAR, and identity management platforms introduces significant implementation overhead that can delay deployment timelines and suppress adoption velocity.

The competitive landscape of the Cloud Application Security Market is characterized by a mix of diversified cybersecurity conglomerates, specialized cloud security pure-plays, and technology hyperscalers with embedded security offerings.

Cisco Systems: A diversified networking and security conglomerate that offers cloud application security capabilities through its Duo Security, Umbrella, and Secure Access Service Edge (SASE) portfolios, leveraging its massive enterprise installed base for cross-sell penetration.

Proofpoint: Focused primarily on cloud email security and information protection, Proofpoint delivers application-layer data loss prevention and insider threat detection capabilities with particular strength in regulated industries such as financial services and healthcare.

Netskope: A cloud-native CASB and SASE leader that provides real-time data and threat protection for cloud applications, web traffic, and private applications, with a platform architecture designed specifically for multi-cloud enterprise environments.

Symantec: Operating as part of Broadcom's enterprise software division, Symantec maintains a broad cloud security portfolio encompassing web security, cloud DLP, and endpoint-to-cloud access control, with strong penetration among global Fortune 500 accounts.

CensorNet: A UK-based cybersecurity vendor offering unified cloud security covering web filtering, cloud application control, email security, and multi-factor authentication, with a focus on the European SME and mid-market segments.

Oracle: Differentiates through native integration of cloud application security capabilities within its Oracle Cloud Infrastructure (OCI) platform, offering identity-centric security controls tightly coupled to its ERP and database application ecosystems.

Skyhigh Networks: Now operating within the McAfee/Trellix security ecosystem, Skyhigh Networks pioneered the CASB category and continues to offer cloud data protection and shadow IT visibility solutions for enterprise clients.

Fortinet: Delivers cloud application security through its FortiGate and FortiWeb product lines, leveraging its Security Fabric architecture to provide unified policy management across on-premises and cloud environments.

Bitglass: A cloud access security broker specializing in agentless security for unmanaged devices and BYOD environments, with particular strength in securing third-party contractor access to cloud applications.

CipherCloud: Focused on cloud information protection through encryption, tokenization, and data masking technologies, enabling enterprises to maintain sovereignty over sensitive data in third-party SaaS applications.

Palo Alto Networks: The market's broadest cloud security platform vendor, offering Prisma Cloud as a comprehensive CNAPP that spans workload protection, CSPM, and application security across AWS, Azure, and GCP.

Microsoft: Leverages its Defender for Cloud Apps (formerly MCAS) platform and deep Azure and Microsoft 365 integration to deliver cloud application security at hyperscale, with native identity and conditional access controls.

January 2024: Palo Alto Networks announced the expansion of its Prisma Cloud platform with AI-powered code-to-cloud security capabilities, integrating application security testing directly into developer IDE environments to address shift-left security imperatives.

March 2024: Microsoft introduced enhanced Defender for Cloud Apps integrations with Microsoft Sentinel, enabling unified SIEM/SOAR workflows for cloud application threat investigation and automated response playbooks.

May 2024: Netskope completed a significant product update to its Intelligent SSE platform, adding generative AI activity monitoring capabilities to detect and control enterprise use of consumer-grade AI applications such as ChatGPT within corporate environments.

July 2024: The European Union's NIS2 Directive implementation guidance was finalized by ENISA, providing detailed technical requirements for cloud application security controls applicable to operators of essential services across 18 critical sectors.

September 2024: Cisco Systems announced the acquisition of a cloud security analytics firm to bolster its XDR (Extended Detection and Response) capabilities, with a strategic intent to correlate cloud application telemetry with network and endpoint signals.

November 2024: Fortinet released FortiWeb Cloud 3.0, introducing machine learning-based API discovery and protection features designed to address the escalating volume of API-layer attacks targeting cloud-native applications.

February 2025: The U.S. Cybersecurity and Infrastructure Security Agency (CISA) published updated cloud security guidelines for federal agencies, mandating enhanced application-layer security controls for all FedRAMP-authorized SaaS deployments.

The Cloud Application Security Market exhibits pronounced regional heterogeneity, with distinct growth profiles, demand drivers, and competitive dynamics across major geographies.

North America: North America represents the largest regional market, accounting for approximately 38% of global revenue in 2024. The United States is the primary contributor, driven by a combination of high cloud adoption maturity, stringent federal and state-level cybersecurity regulations, and the concentration of technology-intensive enterprise sectors. Canada and Mexico contribute incrementally, with the former benefiting from cross-border regulatory alignment with U.S. data protection standards. The region's CAGR is estimated at 4.8%, reflecting its relative maturity and baseline saturation in enterprise cloud security spending.

Europe: Europe is the second-largest regional market, with Germany, the United Kingdom, and France collectively representing the bulk of regional demand. GDPR compliance requirements and, increasingly, the NIS2 Directive are the dominant procurement catalysts. The region's CAGR is estimated at 5.2%, slightly above North America's, as mid-market enterprises — which lag large corporates in cloud security maturity — accelerate adoption. The Benelux and Nordic clusters are notable sub-regional outperformers, reflecting high cloud penetration and advanced regulatory frameworks.

Asia Pacific: Asia Pacific is the fastest-growing regional market, projected to achieve a CAGR of 7.1% through the forecast period. China, India, Japan, and South Korea drive the bulk of regional demand, with India and Southeast Asian ASEAN nations representing the highest incremental growth opportunities. Rapid digitalization of financial services, government e-services, and manufacturing in these economies is generating substantial new application workloads requiring security. Oceania, while smaller in absolute terms, is characterized by high per-enterprise security spending driven by Australia's stringent Privacy Act and the Australian Signals Directorate's Essential Eight framework.

Middle East and Africa: The Middle East and Africa region is emerging as a high-potential market, anchored by the GCC countries' ambitious digital transformation agendas, including Saudi Arabia's Vision 2030 and the UAE's digital economy initiatives. Government and defense verticals are the primary demand drivers. The region's CAGR is estimated at 6.3%, with Israel representing a disproportionate technology innovation hub within the regional ecosystem.

South America: South America represents the smallest regional segment, with Brazil dominating regional demand. Cloud adoption is accelerating across Brazilian financial services and retail sectors, driving early-stage cloud application security investments. The region's CAGR is estimated at 5.7%, constrained by macroeconomic volatility and nascent regulatory frameworks.

Three disruptive technology vectors are fundamentally reshaping the Cloud Application Security Market's architecture, vendor positioning, and enterprise adoption patterns.

First, AI-native threat detection and response. The integration of large language models (LLMs) and foundation models into cloud security platforms represents the most transformative near-term innovation. Unlike rule-based detection systems, AI-native engines can identify zero-day exploits, behavioral anomalies, and multi-stage attack sequences across complex cloud application environments with substantially lower false-positive rates. Vendors including Palo Alto Networks and Microsoft are investing hundreds of millions of dollars annually in AI security R&D. Enterprise adoption of AI-powered cloud security is expected to reach 60% of large enterprises by 2027, up from approximately 28% in 2024. This technology reinforces incumbent vendors' positions — as training large security models requires massive proprietary telemetry datasets that new entrants cannot easily replicate — while threatening point-solution vendors whose narrow data sets limit model efficacy.

Second, Cloud-Native Application Protection Platforms (CNAPPs). The consolidation of previously discrete security functions — including CSPM (Cloud Security Posture Management), CWPP, and CIEM (Cloud Infrastructure Entitlement Management) — into unified CNAPP platforms is reshaping the vendor landscape. CNAPPs enable security teams to correlate risks across the entire application development and runtime lifecycle, from infrastructure-as-code (IaC) templates to production workloads. Gartner identified CNAPP as one of the top security technology categories by enterprise investment priority through 2026. This architectural shift threatens standalone CSPM and CWPP vendors while advantaging platform-centric players.

Third, API security intelligence. With APIs now mediating the majority of cloud application interactions, dedicated API security platforms — offering discovery, schema validation,

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.5% from 2020-2034 |

| Segmentation |

|

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Comprehensive validation mechanisms ensuring market intelligence accuracy, reliability, and adherence to international standards.

500+ data sources cross-validated

200+ industry specialists validation

NAICS, SIC, ISIC, TRBC standards

Continuous market tracking updates

Factors such as are projected to boost the Cloud Application Security Market market expansion.

Key companies in the market include Cisco Systems, Proofpoint, Netskope, Symantec, CensorNet, Oracle, Skyhigh Networks, Fortinet, Bitglass, CipherCloud, Palo Alto Networks, Microsoft.

The market segments include Component, Organization Size, Vertical.

The market size is estimated to be USD 10.7 billion as of 2022.

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3690, USD 5820, and USD 9870 respectively.

The market size is provided in terms of value, measured in billion and volume, measured in .

Yes, the market keyword associated with the report is "Cloud Application Security Market," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Cloud Application Security Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.