1. What are the major growth drivers for the Conversion Rate Optimization Software Market market?

Factors such as are projected to boost the Conversion Rate Optimization Software Market market expansion.

+1 2315155523

Conversion Rate Optimization Software Market

Conversion Rate Optimization Software Market

Market Lens IQ is a global market intelligence and strategic consulting firm delivering advanced syndicated research reports, customized industry analysis, competitive intelligence, and data-driven advisory solutions to organizations across international markets. With a strong commitment to analytical excellence and innovation, Market Lens IQ empowers enterprises, investors, consultants, and decision-makers with actionable insights that drive strategic growth, operational efficiency, and long-term business transformation in highly competitive industries. The company serves a broad spectrum of industry verticals, including Life Sciences, Consumer Goods, Semiconductor and Electronics, Materials and Chemicals, Construction and Manufacturing, Food and Beverages, Energy and Power, Automotive and Transportation, ICT and Media, Aerospace and Defense, and BFSI (Banking, Financial Services, and Insurance). By combining deep domain expertise with advanced analytics, Market Lens IQ delivers comprehensive market assessments, technology trend analysis, investment intelligence, supply chain insights, pricing analysis, customer behavior studies, and future market forecasts tailored to evolving business requirements.

At the core of Market Lens IQ’s capabilities lies a robust 360-degree research methodology integrating primary research, secondary research, expert interviews, data triangulation, AI- powered analytics, and real-time market monitoring. Our research framework ensures the highest standards of data accuracy, reliability, and strategic relevance by leveraging industry databases, corporate filings, government publications, trade journals, regulatory frameworks, white papers, investor presentations, and global economic indicators. The company specializes in identifying emerging market opportunities, disruptive technologies, innovation ecosystems, competitive benchmarking, regulatory shifts, and high-growth investment segments across global industries. Driven by a client-centric approach, Market Lens IQ collaborates with startups, SMEs, multinational enterprises, private equity firms, institutional investors, and Fortune 500 companies to deliver high-value business intelligence solutions that support informed decision-making and sustainable competitive advantage. Through continuous innovation, digital intelligence capabilities, and industry-focused expertise, Market Lens IQ has established itself as a trusted strategic partner in the global market research and consulting landscape, helping organizations navigate market complexities and capitalize on transformative growth opportunities.

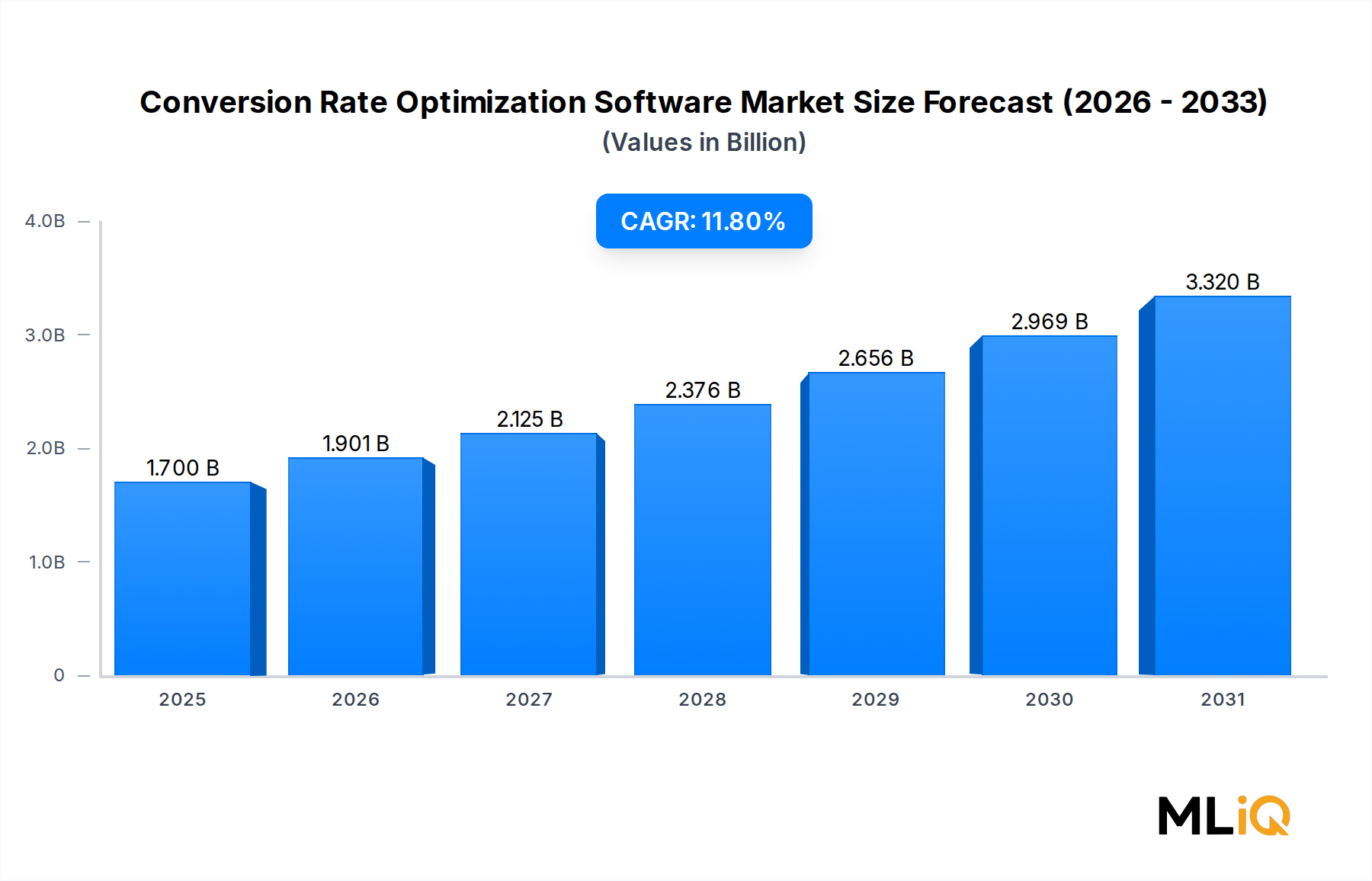

The global Conversion Rate Optimization Software Market is valued at $1.7 billion in 2025, and is forecast to expand at a compound annual growth rate (CAGR) of 11.8% through the latter part of the decade. This robust trajectory reflects an accelerating enterprise shift toward data-driven digital marketing, where measurable return on digital investment has become a board-level imperative rather than a departmental goal.

Organizations across verticals—from financial services to retail—are under mounting pressure to extract more value from existing traffic rather than simply increasing paid acquisition spend. As customer acquisition costs on major platforms continue to rise, conversion optimization has emerged as a high-leverage alternative: improving on-site or in-app experiences to lift conversion metrics without proportional increases in media budget. This structural dynamic is one of the most powerful demand engines sustaining market momentum.

Macro tailwinds reinforcing growth include the global proliferation of e-commerce infrastructure, the rapid adoption of cloud-native SaaS tools among small and medium enterprises (SMEs), and the maturation of artificial intelligence (AI)-powered analytics that enable real-time behavioral segmentation and multivariate experimentation. The integration of large language models (LLMs) into CRO platforms for automated copy testing and personalization recommendations represents a frontier that is already reshaping product roadmaps among leading vendors.

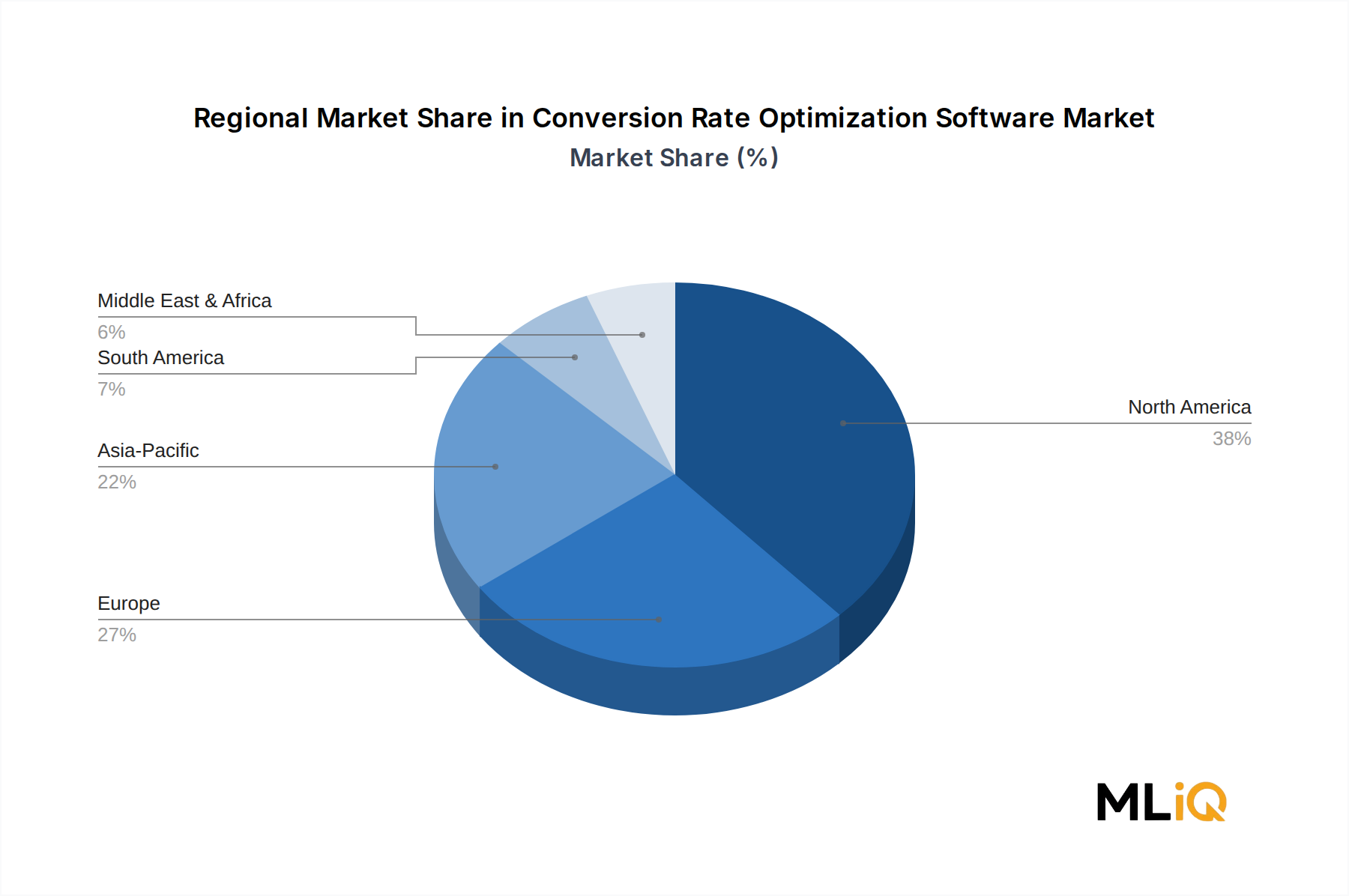

From a regional perspective, North America retains the largest revenue share, anchored by a dense concentration of technology-native enterprises and an established culture of conversion-led growth marketing. However, Asia Pacific is emerging as the fastest-growing region, driven by rapid digitalization of commerce in China, India, and Southeast Asia. Europe maintains a strong position, supported by GDPR-era investments in first-party data strategies that naturally dovetail with CRO tooling.

The competitive landscape is moderately fragmented, with a mix of dedicated CRO platforms, full-stack digital experience players, and embedded analytics suites competing for wallet share. Strategic differentiation increasingly centers on integrations with customer data platforms (CDPs), no-code experimentation interfaces, and AI-driven recommendation engines.

Looking forward, the market is expected to benefit from increasing adoption among SMEs previously priced out of enterprise-grade solutions, as cloud deployment models drive down total cost of ownership. By the end of the forecast period, the market is projected to approach or exceed $3.5 billion in annual revenues, underpinned by broad-based digitalization and a secular shift toward performance marketing disciplines.

Among all segmentation dimensions within the Conversion Rate Optimization Software Market, the deployment model axis—specifically the cloud segment—represents the single largest revenue contributor and continues to consolidate its lead. Cloud-based CRO software accounted for the majority of market revenues in 2025 and is expected to maintain a disproportionate share through the end of the forecast horizon, growing at a pace that consistently outstrips on-premises counterparts.

The dominance of cloud deployment is rooted in several structural advantages that align precisely with the operational profile of modern digital marketing teams. First, cloud platforms enable continuous software updates, ensuring that users always access the latest AI models, integrations, and testing frameworks without manual patching cycles. For a market where algorithmic sophistication directly translates into conversion lift, this evergreen delivery model is a decisive competitive advantage.

Second, cloud CRO tools offer elastic scalability that accommodates the highly variable traffic patterns inherent to digital commerce—peak season spikes, campaign-driven surges, and event-triggered demand—without requiring enterprise customers to provision excess on-premises capacity. This operational flexibility is particularly compelling for large e-commerce players and media companies whose conversion funnels experience orders-of-magnitude traffic variation across a calendar year.

Third, the subscription-based pricing structure of cloud deployment lowers the barrier to entry for SMEs, which represent a growing portion of the addressable market. As vendors such as Unbounce, Instapage Inc., and Hotjar Ltd have demonstrated, affordable monthly subscription tiers with self-serve onboarding can unlock a long tail of digital businesses previously unable to afford enterprise CRO platforms. This democratization dynamic is a key factor in why the cloud segment not only dominates in absolute revenue terms but is also expanding its share within the overall market.

Key players driving cloud segment leadership include Alphabet Inc., which embeds CRO-adjacent capabilities within its Google Optimize and broader analytics ecosystem; BloomReach Inc., which offers cloud-native personalization and search capabilities tightly coupled with conversion workflows; and Algolia, whose API-first, cloud-delivered search and discovery platform enables developers to build conversion-optimized experiences at scale. Momentive Inc. complements this group with cloud-based survey and user feedback tools that feed directly into CRO hypothesis generation.

The on-premises segment, while declining as a share of total market revenues, retains relevance in highly regulated industries such as banking, insurance, and government-adjacent digital services, where data sovereignty requirements and compliance mandates create structural demand for locally hosted solutions. However, even within these verticals, the trajectory is toward private cloud and hybrid architectures that preserve data control while capturing the operational benefits of cloud delivery.

From a geographic standpoint, cloud deployment dominance is most pronounced in North America and Western Europe, where enterprise IT infrastructure is already heavily cloud-shifted. In contrast, certain Asia Pacific and Middle East markets still exhibit meaningful on-premises adoption, reflecting earlier stages of cloud migration maturity and, in some cases, regulatory environments that have historically favored local data hosting.

The consolidation of cloud's dominant position is unlikely to reverse. Vendor R&D investment, partnership ecosystems, and go-to-market strategies are overwhelmingly oriented toward cloud-native architectures, meaning the gap between cloud and on-premises capabilities will widen over time, further cementing the deployment model's role as the market's primary growth engine.

The Conversion Rate Optimization Software Market is shaped by a confluence of quantifiable demand drivers and measurable constraints that together define the market's growth trajectory.

Primary driver: rising customer acquisition costs. Digital advertising costs on major platforms have increased materially over the past three years, with average cost-per-click (CPC) rates on search and social channels rising by an estimated 15–25% annually in competitive verticals. This inflation compels digital marketers to maximize the conversion efficiency of existing traffic, making CRO software a defensively positioned investment even in recessionary environments.

Secondary driver: AI and machine learning integration. The embedding of predictive analytics, behavioral clustering, and automated experimentation engines into CRO platforms has dramatically shortened the time-to-insight for optimization campaigns. Vendors now offer AI-driven hypothesis generation that can reduce manual A/B test design time by an estimated 40–60%, accelerating ROI timelines and lowering the skill threshold required to operate enterprise-grade tools. The A/B Testing Software Market is directly benefiting from this trend as experimentation capabilities become more sophisticated.

Tertiary driver: first-party data imperatives. The deprecation of third-party cookies and tightening privacy regulations (GDPR, CCPA, and emerging equivalents in Asia Pacific) have accelerated enterprise investment in first-party data infrastructure. CRO platforms that can leverage on-site behavioral signals—session recordings, heatmaps, form analytics—without reliance on third-party identifiers are positioned as essential components of a privacy-compliant analytics stack.

Primary constraint: implementation complexity and talent scarcity. Despite improvements in no-code interfaces, deploying CRO tools effectively still requires expertise in statistical methodology, UX design, and digital analytics. A shortage of qualified CRO practitioners constrains adoption, particularly among SMEs that lack dedicated optimization teams. This skill gap acts as a meaningful drag on the pace of new customer activation.

Secondary constraint: integration fragmentation. Enterprise marketing stacks typically comprise 15–30 discrete tools, and CRO platforms must integrate cleanly with CDPs, CRM systems, tag management solutions, and analytics platforms. Integration failures or data synchronization latency can undermine the accuracy of experimentation results, creating risk aversion among potential buyers.

These drivers and constraints collectively define a market that is growing robustly but unevenly, with the largest gains accruing to vendors that combine ease of use with deep integration capabilities.

The competitive landscape of the Conversion Rate Optimization Software Market features a diverse array of vendors spanning pure-play CRO specialists, integrated digital experience platforms, and analytics-first entrants. The following profiles outline the strategic positioning of key participants:

Momentive Inc.: Specializes in survey-based user feedback and market research tools that provide qualitative conversion intelligence; its SurveyMonkey platform is widely used to supplement quantitative CRO data with voice-of-customer insights.

I-on interactive Inc: Focuses on digital experience optimization through web content management and personalization capabilities, serving mid-market clients seeking integrated CRO and content management in a single platform.

BloomReach Inc.: Offers a composable digital experience platform combining AI-powered search, merchandising, and content personalization; particularly strong in e-commerce verticals where product discovery is a primary conversion lever.

Hotjar Ltd: Provides behavior analytics tools including heatmaps, session recordings, and feedback widgets; widely adopted by SMEs and growth-stage companies as an accessible entry point into CRO analytics without heavy technical implementation.

Instapage Inc.: Delivers a cloud-based landing page creation and optimization platform with built-in A/B testing and personalization; particularly valued by performance marketing teams managing high-volume paid traffic campaigns.

Alphabet Inc.: Integrates CRO-relevant capabilities through Google Analytics 4, Google Optimize (and its successor integrations), and the broader Google Marketing Platform; commands significant influence due to its ubiquity in digital measurement infrastructure.

Algolia: Provides an API-first search and discovery platform that enables developers to build conversion-optimized product and content discovery experiences; strong in developer-centric organizations and headless commerce architectures.

Smartlook: Offers qualitative analytics through session recordings, event tracking, and funnel analysis; targets product and UX teams seeking granular insight into user behavior to inform conversion hypotheses.

Unbounce: Specializes in AI-powered landing page building and traffic routing, with Smart Traffic technology that dynamically routes visitors to the highest-converting page variant based on historical performance data.

Landingi: Provides a no-code landing page builder with integrated A/B testing and analytics; positioned as an accessible, cost-effective solution for SMEs and marketing agencies managing multiple client campaigns.

Q1 2025: Unbounce launched an expanded version of its Smart Traffic AI engine, incorporating large language model-based copy recommendations that allow marketers to auto-generate and test headline variants directly within the platform interface.

Q1 2025: Hotjar Ltd announced a strategic integration partnership with a leading customer data platform vendor, enabling unified behavioral data streams to flow between session recording analytics and downstream personalization engines.

Q2 2025: Algolia released a new composable commerce optimization layer, allowing e-commerce operators to run multivariate experiments on search result rankings and product recommendation carousels without engineering intervention.

Q2 2025: BloomReach Inc. completed a significant product update to its Experience Platform, embedding generative AI tools for automated content personalization tied directly to on-site conversion metrics.

Q3 2024: Instapage Inc. introduced dynamic text replacement capabilities powered by real-time audience signal processing, enabling more granular message-match between paid search ads and destination landing pages.

Q3 2024: Smartlook expanded its analytics platform to include mobile app session analysis, broadening its addressable market to include native app development teams seeking cross-platform conversion intelligence.

Q4 2024: Momentive Inc. announced the integration of AI-powered survey logic that automatically surfaces statistically significant response patterns relevant to conversion barrier identification.

Q4 2024: Landingi launched a new agency tier with white-label capabilities, targeting digital marketing agencies managing conversion optimization campaigns across multiple client accounts simultaneously.

The Conversion Rate Optimization Software Market exhibits meaningful regional differentiation in terms of maturity, growth velocity, and demand composition.

North America represents the most mature and revenue-dense regional market, accounting for an estimated 38–42% of global revenues in 2025. The United States is the primary contributor, driven by a high density of technology-native enterprises, a well-developed digital marketing ecosystem, and strong venture capital investment in martech infrastructure. Canada and Mexico contribute incrementally, with Mexico showing above-average growth as e-commerce penetration accelerates. The regional CAGR for North America is estimated at approximately 9.5%, below the global average, reflecting market maturity rather than demand saturation.

Europe represents the second-largest regional market, with an estimated revenue share of 25–28% in 2025. The United Kingdom, Germany, and France are the three largest contributors. GDPR compliance requirements have paradoxically stimulated CRO investment in the region, as first-party behavioral analytics—the foundation of CRO tooling—became more strategically valuable as third-party data flows were curtailed. The regional CAGR is estimated at 10.2%, slightly below the global average but supported by strong enterprise digitalization programs.

Asia Pacific is the fastest-growing region, with a projected CAGR of 15.1% through the forecast period. China, India, Japan, and South Korea collectively anchor regional demand, with ASEAN markets (particularly Indonesia, Vietnam, and Thailand) emerging as high-growth secondary contributors. The primary demand driver is the rapid formalization of digital commerce across the region, with millions of SMEs establishing online sales channels for the first time and requiring accessible, affordable CRO tooling to compete effectively.

Middle East and Africa and South America each represent smaller but strategically significant markets. Brazil leads South American adoption, supported by a large and growing digital commerce sector. The GCC countries within the Middle East and Africa region are investing heavily in digital government and smart commerce initiatives that create adjacent demand for conversion optimization capabilities. Both regions are expected to grow at rates approximating 12–13% CAGR, broadly in line with the global average.

The Conversion Rate Optimization Software Market, as a software-dominant segment of the broader Digital Marketing Automation Market, does not rely on physical raw materials in the traditional manufacturing sense. However, it exhibits meaningful upstream dependencies on several technology infrastructure inputs whose availability, cost, and performance directly affect vendor economics and product capability.

Cloud infrastructure represents the most significant upstream input. CRO platforms deployed in cloud environments—the dominant deployment model—are fundamentally dependent on hyperscaler compute, storage, and networking capacity from providers such as Amazon Web Services, Microsoft Azure, and Google Cloud. Pricing dynamics in cloud infrastructure have experienced notable volatility: following a period of aggressive discounting in 2022–2023, hyperscaler pricing for GPU-intensive compute (critical for AI-powered CRO features) increased materially in 2024 as demand from generative AI workloads compressed available capacity. This has introduced margin pressure on CRO vendors that rely heavily on real-time machine learning inference.

Data labeling and AI model training represent a secondary upstream dependency. As CRO platforms increasingly differentiate on the quality of their AI recommendations, the cost and availability of high-quality labeled behavioral data—and the human annotation resources required to curate training datasets—have become a sourcing consideration. The Web Analytics Software Market, which generates much of the raw behavioral data that feeds CRO models, is therefore an adjacent upstream dependency.

Third-party data integrations, including identity resolution services and audience enrichment providers, have faced significant supply disruption following cookie deprecation timelines. CRO vendors that had embedded third-party data signals into their personalization and segmentation engines were required to undertake costly re-architecture efforts in 2023–2024, representing a non-trivial supply chain disruption analog in the software context.

Cybersecurity and compliance infrastructure—including data encryption libraries, privacy management SDKs, and audit logging systems—represent a growing input cost as regulatory complexity increases globally. Vendors operating across multiple jurisdictions face rising costs for compliance tooling, which are increasingly embedded into product development cycles rather than treated as discretionary expenditures.

The customer base of the Conversion Rate Optimization Software Market is heterogen

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 11.8% from 2020-2034 |

| Segmentation |

|

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Comprehensive validation mechanisms ensuring market intelligence accuracy, reliability, and adherence to international standards.

500+ data sources cross-validated

200+ industry specialists validation

NAICS, SIC, ISIC, TRBC standards

Continuous market tracking updates

Factors such as are projected to boost the Conversion Rate Optimization Software Market market expansion.

Key companies in the market include Momentive Inc., I-on interactive Inc, BloomReach Inc., Hotjar Ltd, Instapage Inc., Alphabet Inc., Algolia, Smartlook, Unbounce, Landingi.

The market segments include Component, Deployment Model, Enterprise Size, Type.

The market size is estimated to be USD 1.7 billion as of 2022.

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3690, USD 5820, and USD 9870 respectively.

The market size is provided in terms of value, measured in billion and volume, measured in .

Yes, the market keyword associated with the report is "Conversion Rate Optimization Software Market," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Conversion Rate Optimization Software Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.