1. What are the major growth drivers for the Esports Market market?

Factors such as are projected to boost the Esports Market market expansion.

Market Lens IQ is a global market intelligence and strategic consulting firm delivering advanced syndicated research reports, customized industry analysis, competitive intelligence, and data-driven advisory solutions to organizations across international markets. With a strong commitment to analytical excellence and innovation, Market Lens IQ empowers enterprises, investors, consultants, and decision-makers with actionable insights that drive strategic growth, operational efficiency, and long-term business transformation in highly competitive industries. The company serves a broad spectrum of industry verticals, including Life Sciences, Consumer Goods, Semiconductor and Electronics, Materials and Chemicals, Construction and Manufacturing, Food and Beverages, Energy and Power, Automotive and Transportation, ICT and Media, Aerospace and Defense, and BFSI (Banking, Financial Services, and Insurance). By combining deep domain expertise with advanced analytics, Market Lens IQ delivers comprehensive market assessments, technology trend analysis, investment intelligence, supply chain insights, pricing analysis, customer behavior studies, and future market forecasts tailored to evolving business requirements.

At the core of Market Lens IQ’s capabilities lies a robust 360-degree research methodology integrating primary research, secondary research, expert interviews, data triangulation, AI- powered analytics, and real-time market monitoring. Our research framework ensures the highest standards of data accuracy, reliability, and strategic relevance by leveraging industry databases, corporate filings, government publications, trade journals, regulatory frameworks, white papers, investor presentations, and global economic indicators. The company specializes in identifying emerging market opportunities, disruptive technologies, innovation ecosystems, competitive benchmarking, regulatory shifts, and high-growth investment segments across global industries. Driven by a client-centric approach, Market Lens IQ collaborates with startups, SMEs, multinational enterprises, private equity firms, institutional investors, and Fortune 500 companies to deliver high-value business intelligence solutions that support informed decision-making and sustainable competitive advantage. Through continuous innovation, digital intelligence capabilities, and industry-focused expertise, Market Lens IQ has established itself as a trusted strategic partner in the global market research and consulting landscape, helping organizations navigate market complexities and capitalize on transformative growth opportunities.

+1 2315155523

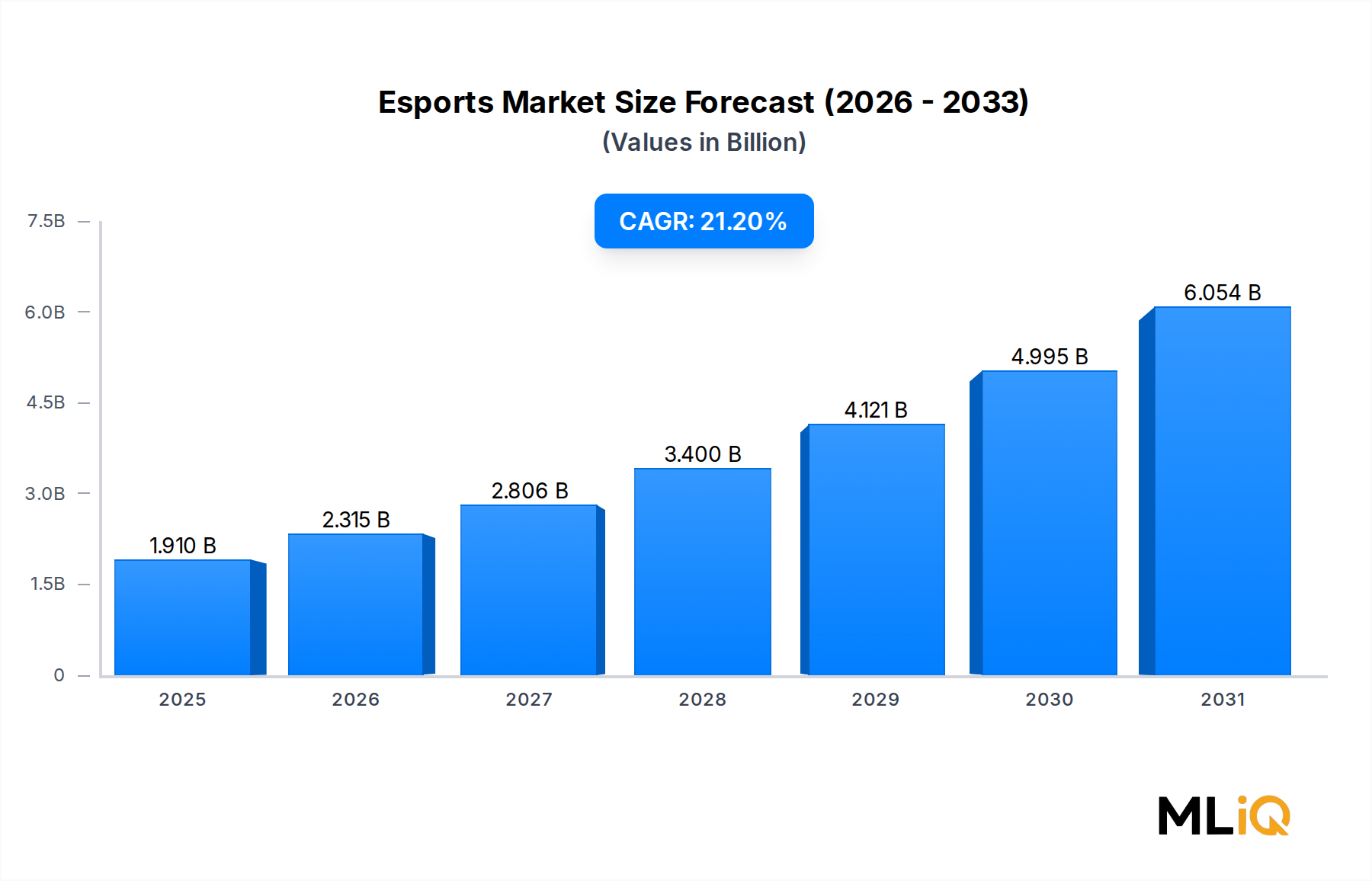

The global esports industry has entered a period of accelerated structural maturation, underpinned by rising viewership, diversifying revenue streams, and deepening institutional investment. As of the base assessment period, the Esports Market is valued at $1.91 billion and is forecast to expand at a compound annual growth rate (CAGR) of 21.2% over the projection horizon, positioning it among the fastest-growing segments within the broader ICT and Media category. This growth trajectory reflects a convergence of demographic tailwinds, technological enablement, and monetization sophistication that distinguishes esports from legacy sports entertainment models.

Primary demand drivers include the global proliferation of high-speed internet infrastructure, the mainstreaming of streaming platforms such as Twitch and YouTube Gaming, and an accelerating influx of sponsorship capital from non-endemic brands spanning consumer electronics, fast-moving consumer goods, and financial services. The 18–34 demographic cohort continues to anchor viewership, but data increasingly shows penetration into the 35–44 bracket, suggesting audience aging and retention rather than purely new acquisition.

On the macroeconomic front, the post-pandemic digital entertainment boom has catalyzed lasting behavioral shifts. Remote engagement, digital-first social interaction, and the normalization of screen-based recreation have structurally elevated the addressable audience for competitive gaming. Simultaneously, mobile device penetration in emerging economies across Southeast Asia, Latin America, and Sub-Saharan Africa is unlocking previously untapped viewer and participant pools, broadening the geographic base of the market beyond its traditional North American and East Asian strongholds.

Revenue diversification is a defining feature of the current market phase. While sponsorship has historically been the dominant revenue pillar, media rights deals are gaining momentum rapidly, mirroring the evolution seen in traditional sports leagues over the past three decades. Game publisher fees, digital advertisement income, and ticket and merchandise sales round out an increasingly resilient multi-channel revenue architecture.

Looking forward, the Esports Market is poised to benefit from continued convergence with adjacent technology ecosystems. Integrations with augmented and virtual reality platforms, AI-driven personalization of broadcast content, and blockchain-enabled fan engagement tools represent the next frontier of value creation. Institutional investors, league operators, and platform providers are collectively increasing capital allocation toward infrastructure that supports these capabilities, reinforcing a compounding growth dynamic through 2030 and beyond.

Among all revenue streams constituting the Esports Market's commercial architecture — including media rights, game publisher fees, tickets and merchandise — the sponsorship and digital advertisement segment commands the largest aggregate revenue share and represents the most strategically contested battleground for market participants. This dominance is not incidental; it reflects structural dynamics rooted in audience composition, content format adaptability, and the measurability advantages that digital-native platforms provide to brand advertisers.

Sponsorship revenue in esports operates through multiple modalities: jersey and peripheral branding, in-game item integrations, naming rights for tournaments and leagues, and activation partnerships during live events. Non-endemic sponsors — companies whose core products are unrelated to gaming hardware or software — have become increasingly prominent. Automotive brands, financial services firms, energy drink companies, and luxury goods houses have all entered multi-year sponsorship agreements with major esports organizations and tournament operators, validating the medium's capacity to deliver brand equity beyond the gaming-native audience.

Digital advertisement revenue is closely coupled with streaming platform traffic. As viewership hours on platforms such as Twitch, YouTube Gaming, and proprietary publisher streaming channels accumulate, pre-roll, mid-roll, and display advertising inventory scales commensurately. The interactive and participatory nature of esports content — chat engagement, real-time reaction, viewer prediction markets — generates above-average engagement metrics relative to passive video consumption, making esports inventory attractive to performance-focused advertisers who prize click-through rates and conversion attribution.

Key players operating within this revenue segment include Activision Blizzard, which has leveraged the Overwatch League and Call of Duty League as premium sponsorship vehicles with tiered partnership packages attracting global brands. Electronic Arts has similarly constructed sponsorship frameworks around its FIFA and Apex Legends competitive circuits, integrating brand placements into broadcast overlays and in-game cosmetic content. NVIDIA Corporation's presence in the segment is strategic and technology-forward, aligning its GPU hardware brand with high-performance competitive play through athlete endorsements and event hardware provisioning.

The segment's dominance is consolidating rather than fragmenting. As data measurement capabilities improve — enabling sponsors to track return on investment through digital attribution, social sentiment analysis, and second-screen engagement — brand confidence in esports sponsorship as a performance channel is strengthening. This is evidenced by the elongation of average contract durations, with multi-year commitments becoming the norm rather than single-event arrangements.

However, the segment faces a structural ceiling risk: audience ad fatigue and the adoption of ad-blocking tools among younger demographics necessitate innovation in integration formats. The industry is responding with native integrations — where brand messaging is woven organically into broadcast narratives or in-game economies — reducing friction while maintaining commercial yield. This format evolution is likely to sustain the segment's revenue leadership through the medium term, even as media rights revenues grow at a faster marginal rate from a lower base.

Gfinity and FACEIT, as tournament and league operators, play a critical intermediary role in this ecosystem, packaging audience access and inventory into structured commercial offerings for brand partners. Their ability to guarantee viewership thresholds and provide audience demographic data has elevated the professionalism of sponsorship procurement in esports, further accelerating capital inflows from mainstream advertisers into the Online Gaming Market and its competitive spectating layer.

The Esports Market's expansion is propelled by several quantifiable and structurally significant drivers, while a distinct set of constraints moderates the pace and sustainability of growth.

Driver 1 — Broadband and Mobile Infrastructure Expansion: Global mobile internet subscriptions surpassed 6.8 billion by 2023, with 5G network rollouts accelerating latency reduction to sub-20ms thresholds in major metropolitan markets. This infrastructure improvement directly enables competitive-quality online gaming and high-definition streaming on mobile devices, unlocking audience and participant growth in regions where fixed broadband penetration remains low. The Mobile Gaming Market expansion is directly correlated with esports audience growth in Southeast Asia and South Asia.

Driver 2 — Institutionalization of Media Rights: Following the model of the Online Gaming Market and traditional sports, esports properties are increasingly monetizing broadcast rights through exclusive platform deals. Viewership for marquee events such as the League of Legends World Championship has exceeded 73 million peak concurrent viewers, creating a rights valuation case that is attracting streaming platform bidders and linear television operators into competitive licensing negotiations.

Driver 3 — Youth Demographic Lock-In: Approximately 29% of global internet users aged 16–24 identify as active esports viewers, per cross-referenced digital audience surveys. This demographic's high lifetime value as both viewers and consumers of adjacent merchandise and digital goods reinforces the commercial investment thesis for sponsors and advertisers operating across the Digital Advertising Market.

Constraint 1 — Player Burnout and Roster Instability: Competitive esports organizations face structurally elevated roster turnover rates, with average professional player careers spanning just 3–5 years due to physical and psychological burnout. This instability undermines brand equity built around individual athletes and complicates long-term franchise valuation.

Constraint 2 — Regulatory Fragmentation: Jurisdictional inconsistencies in gambling, prize pool taxation, and data privacy regulations create compliance complexity for global tournament operators. The Sport Betting Market's adjacency to esports creates regulatory scrutiny that can constrain partnership models in certain markets.

Constraint 3 — Revenue Model Maturity Gap: Despite rapid growth, esports revenue per viewer remains a fraction of traditional sports equivalents. Bridging this gap requires further development of premium subscription tiers, expanded merchandise ecosystems, and deeper integration with the Media Rights Market infrastructure.

Electronic Arts: A dominant publisher whose competitive gaming titles — including FIFA, Apex Legends, and Battlefield — anchor multiple global esports circuits. The company has invested heavily in first-party tournament infrastructure and third-party league licensing to maximize IP monetization across the Media Rights Market.

Gfinity: A UK-based esports tournament organizer and technology platform provider, Gfinity operates both branded tournaments and white-label competitive gaming solutions for publishers and media companies. Its platform-as-a-service model positions it as infrastructure provider rather than pure content owner.

Modern Times Group: A Swedish media and entertainment conglomerate that has made strategic acquisitions across esports organizations and gaming platforms, positioning MTG as one of the most diversified holding entities in European competitive gaming.

Gameloft SE: A mobile game developer and publisher with an expanding focus on competitive mobile titles, Gameloft is capitalizing on Mobile Gaming Market growth in emerging economies by building lightweight esports formats compatible with low-end smartphone hardware.

Kabam Inc.: A developer of mid-core competitive mobile games, Kabam has integrated ranked ladder systems and tournament features into its titles to create organic esports ecosystems that retain competitive players and drive in-game purchase behavior.

Activision Blizzard, Inc.: One of the most institutionally sophisticated esports operators globally, Activision Blizzard created the franchised Overwatch League and Call of Duty League models, establishing city-based team ownership structures that mirror traditional professional sports franchises and attract stadium-level sponsorship investments.

FACEIT: A leading competitive gaming platform providing tournament infrastructure, matchmaking, and anti-cheat systems for PC esports titles. FACEIT's user-generated competition ecosystem spans millions of registered players across multiple game titles, making it a critical middleware layer between game publishers and competitive communities.

Nintendo Co. Ltd.: Nintendo's competitive gaming footprint spans its flagship titles including Super Smash Bros. and Splatoon, operating the Nintendo Open tournament series globally. Its approach prioritizes grassroots accessibility over franchised league monetization.

CJ Corporation: A South Korean conglomerate with significant esports investment through its gaming and media subsidiaries, CJ is deeply embedded in the Korean competitive gaming ecosystem — a market that has historically driven global esports format innovation.

NVIDIA Corporation: As the leading discrete GPU manufacturer, NVIDIA's hardware underpins the performance requirements of competitive esports and serves as the primary infrastructure component enabling high-refresh-rate gameplay. Its sponsorships and competitive gaming certifications reinforce the Gaming Hardware Market's alignment with esports development.

January 2024: Activision Blizzard finalized its acquisition integration with Microsoft, creating one of the largest combined gaming and esports content portfolios globally, with implications for cloud distribution of competitive gaming content through Xbox Game Pass infrastructure.

March 2024: FACEIT announced an expansion of its anti-cheat technology stack, incorporating machine learning-based behavioral analysis to detect subtle cheating patterns, addressing a long-standing integrity concern that has historically undermined viewer trust in online competitive formats.

May 2024: Electronic Arts disclosed a restructuring of its EA Sports FC competitive circuit, rebranding and expanding prize pool commitments for regional qualifiers across Europe and South America, reflecting a strategic emphasis on growing esports participation in emerging regional markets.

July 2024: NVIDIA launched a dedicated esports performance certification program for monitor manufacturers, establishing standardized latency and refresh rate benchmarks that serve as procurement criteria for tournament organizers seeking to maintain competitive hardware consistency across event venues.

September 2024: Modern Times Group completed divestiture of a minority stake in one of its esports holdings to a Southeast Asian media conglomerate, signaling the geographic reorientation of institutional capital toward Asia Pacific growth markets within the Cloud Gaming Market convergence zone.

November 2024: Nintendo Co. Ltd. announced an expanded Splatoon 3 competitive series for 2025, incorporating for the first time a paid spectator ticket model for regional finals, testing premium live event monetization frameworks that could inform broader esports industry practice.

February 2025: Gameloft SE entered a co-publishing agreement with a regional telecom operator in Southeast Asia to bundle competitive mobile gaming tournament access with 5G data packages, creating a distribution model that ties esports participation to mobile infrastructure adoption.

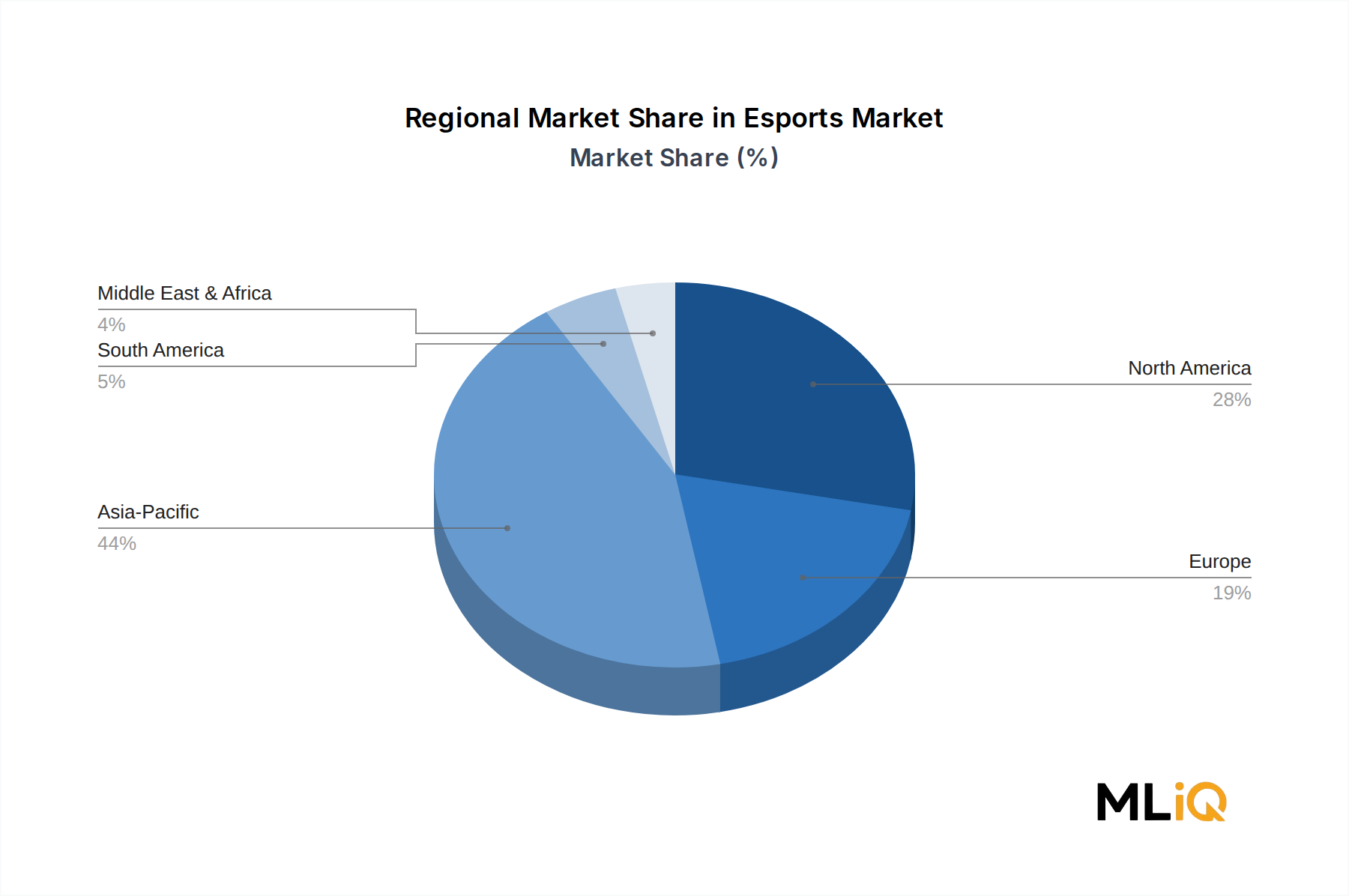

The Esports Market exhibits pronounced regional heterogeneity in both maturity and growth trajectory, driven by differing infrastructure profiles, regulatory environments, and cultural relationships with competitive gaming.

Asia Pacific: Asia Pacific commands the largest revenue share of the global Esports Market, accounting for an estimated 40–45% of total revenues. South Korea and China are the most mature sub-markets, characterized by deep professional league infrastructure, large endemic sponsor bases, and decades of competitive gaming culture. China's market alone is anchored by Tencent's ecosystem integrations across mobile and PC esports. India, Indonesia, and the Philippines represent the region's fastest internal growth frontiers, driven by mobile-first gaming adoption and rapidly expanding youth demographics. The Asia Pacific region is projected to sustain a CAGR above 23%, outpacing the global average, fueled by 5G rollout and the Game Streaming Market's regional expansion.

North America: North America represents the most monetized esports market on a per-viewer basis, particularly in the United States, where franchised league models pioneered by Activision Blizzard and Riot Games have attracted blue-chip non-endemic sponsorships. The region benefits from mature digital advertising infrastructure and premium media rights deal activity. CAGR for North America is estimated at approximately 18–19%, reflecting a more mature base. Canada and Mexico are secondary growth markets with rising mobile gaming adoption connecting to the broader Mobile Gaming Market.

Europe: Europe's esports market is characterized by geographic fragmentation across national audiences and regulatory diversity. The United Kingdom, Germany, and France are the largest individual country markets. FACEIT's European tournament network provides structural cohesion across the fragmented landscape. The region's CAGR is estimated at 17–18%, with growth tempered by data privacy compliance costs under GDPR affecting targeted digital advertising yield.

Latin America: Brazil is the dominant esports market in South America, supported by massive gaming communities and a passionate fan base for titles such as League of Legends and CS:GO. Infrastructure constraints — including inconsistent broadband quality — have historically limited growth, but mobile-first formats are bypassing this barrier. The region is projected to grow at approximately 24–25% CAGR, making it among the fastest-growing globally.

Middle East & Africa: This region represents the earliest-stage but strategically significant frontier. Saudi Arabia and the UAE have made sovereign-level investments in esports infrastructure, hosting major international tournaments and acquiring league stakes. The region's CAGR is estimated above 26%, driven by government-backed initiative spending and a young, digitally connected population eager to engage with competitive gaming content across the Virtual Reality Gaming Market and traditional streaming formats.

Technology disruption is reshaping the competitive, broadcast, and participation dimensions of the Esports Market across three primary vectors.

First, artificial intelligence and machine learning are being deployed across multiple layers of the esports value chain. AI-powered matchmaking algorithms improve competitive balance in ranked play, reducing churn among competitive participants. On the broadcast side, AI-generated highlight reels, real-time performance analytics overlays, and automated camera direction systems are reducing production costs while improving viewer experience quality. Companies such as NVIDIA Corporation are investing in AI inference hardware that enables real-time game enhancement and broadcast graphics rendering, positioning AI not as a future aspiration but as an active operational tool within current competitive gaming infrastructure.

Second, cloud gaming represents a structural transformation in access and hardware requirements. By offloading compute to remote server infrastructure, cloud gaming platforms promise to eliminate the Gaming Hardware Market as a participation barrier. Players without high-specification PCs or gaming consoles can access competitive-grade gaming experiences through low-latency cloud rendering, dramatically expanding the addressable participant pool. The Cloud Gaming Market is at an inflection point: latency performance in geographically optimal deployments has reached competitive viability thresholds, and major platform operators are investing billions in server infrastructure to extend geographic coverage. Adoption timelines project meaningful mainstream penetration by 2026–2027 for major metropolitan markets in developed economies.

Third, virtual and augmented reality technologies are beginning to influence both participation and spectating formats. While full VR competitive gaming remains technically and commercially premature for mainstream esports at scale, AR overlays in broadcast production and hybrid physical-digital event experiences are gaining traction. The Virtual Reality Gaming Market is attracting R&D investment from hardware manufacturers and platform operators who

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 21.2% from 2020-2034 |

| Segmentation |

|

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Comprehensive validation mechanisms ensuring market intelligence accuracy, reliability, and adherence to international standards.

500+ data sources cross-validated

200+ industry specialists validation

NAICS, SIC, ISIC, TRBC standards

Continuous market tracking updates

Factors such as are projected to boost the Esports Market market expansion.

Key companies in the market include Electronic Arts, Gfinity, Modern Times Group, Gameloft SE, Kabam Inc., Activision Blizzard, Inc., FACEIT, Nintendo Co. Ltd., CJ Corporation, FACEIT Ltd., NVIDIA Corporation.

The market segments include Application, Streaming type, Device Type, Revenue Stream.

The market size is estimated to be USD 1.91 billion as of 2022.

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3200, USD 4335, and USD 7261 respectively.

The market size is provided in terms of value, measured in billion and volume, measured in .

Yes, the market keyword associated with the report is "Esports Market," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Esports Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.