1. What are the major growth drivers for the Skin Cancer Diagnostics and Therapeutics Market market?

Factors such as are projected to boost the Skin Cancer Diagnostics and Therapeutics Market market expansion.

Skin Cancer Diagnostics and Therapeutics Market

Skin Cancer Diagnostics and Therapeutics Market

Market Lens IQ is a global market intelligence and strategic consulting firm delivering advanced syndicated research reports, customized industry analysis, competitive intelligence, and data-driven advisory solutions to organizations across international markets. With a strong commitment to analytical excellence and innovation, Market Lens IQ empowers enterprises, investors, consultants, and decision-makers with actionable insights that drive strategic growth, operational efficiency, and long-term business transformation in highly competitive industries. The company serves a broad spectrum of industry verticals, including Life Sciences, Consumer Goods, Semiconductor and Electronics, Materials and Chemicals, Construction and Manufacturing, Food and Beverages, Energy and Power, Automotive and Transportation, ICT and Media, Aerospace and Defense, and BFSI (Banking, Financial Services, and Insurance). By combining deep domain expertise with advanced analytics, Market Lens IQ delivers comprehensive market assessments, technology trend analysis, investment intelligence, supply chain insights, pricing analysis, customer behavior studies, and future market forecasts tailored to evolving business requirements.

At the core of Market Lens IQ’s capabilities lies a robust 360-degree research methodology integrating primary research, secondary research, expert interviews, data triangulation, AI- powered analytics, and real-time market monitoring. Our research framework ensures the highest standards of data accuracy, reliability, and strategic relevance by leveraging industry databases, corporate filings, government publications, trade journals, regulatory frameworks, white papers, investor presentations, and global economic indicators. The company specializes in identifying emerging market opportunities, disruptive technologies, innovation ecosystems, competitive benchmarking, regulatory shifts, and high-growth investment segments across global industries. Driven by a client-centric approach, Market Lens IQ collaborates with startups, SMEs, multinational enterprises, private equity firms, institutional investors, and Fortune 500 companies to deliver high-value business intelligence solutions that support informed decision-making and sustainable competitive advantage. Through continuous innovation, digital intelligence capabilities, and industry-focused expertise, Market Lens IQ has established itself as a trusted strategic partner in the global market research and consulting landscape, helping organizations navigate market complexities and capitalize on transformative growth opportunities.

+1 2315155523

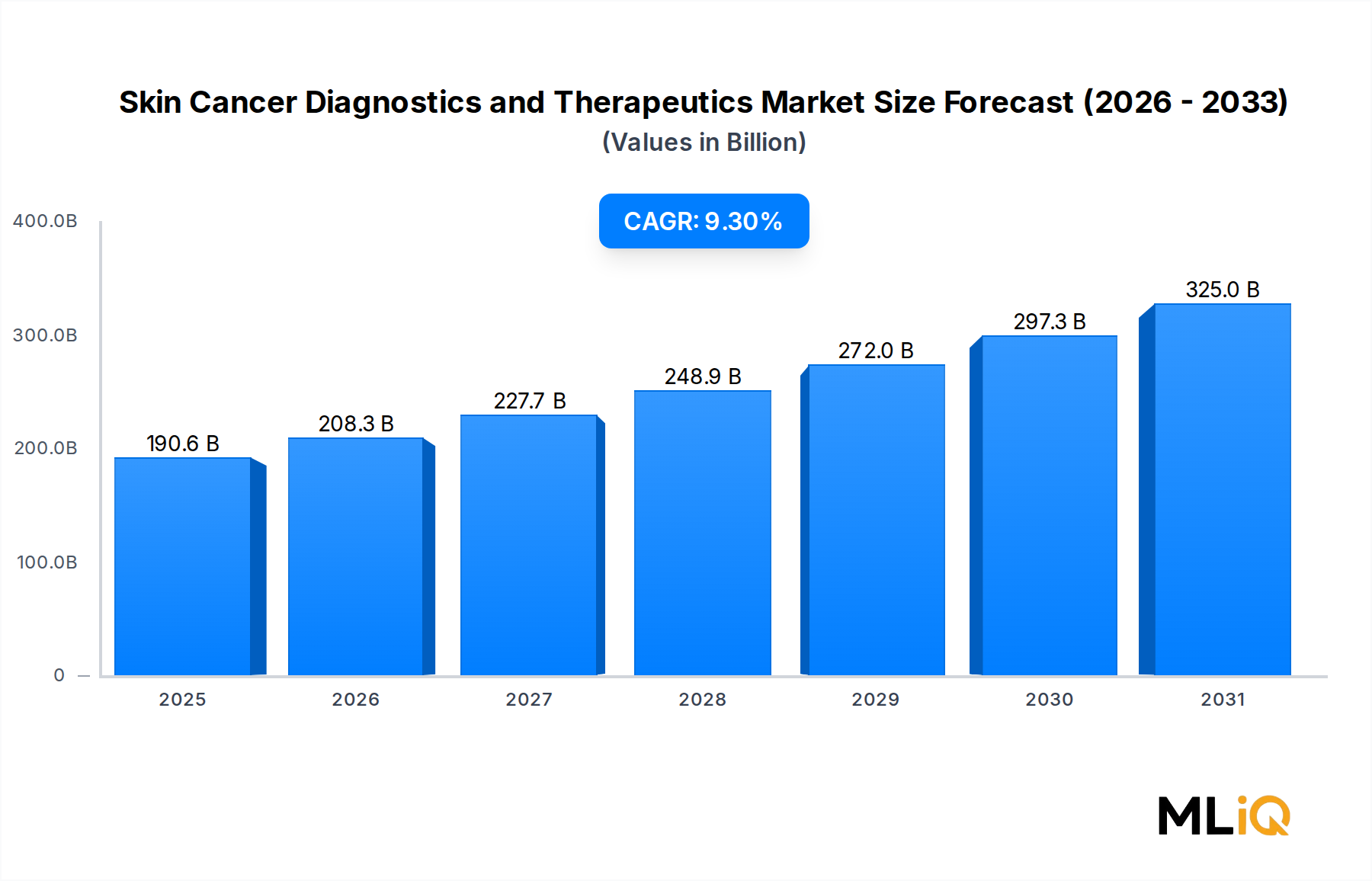

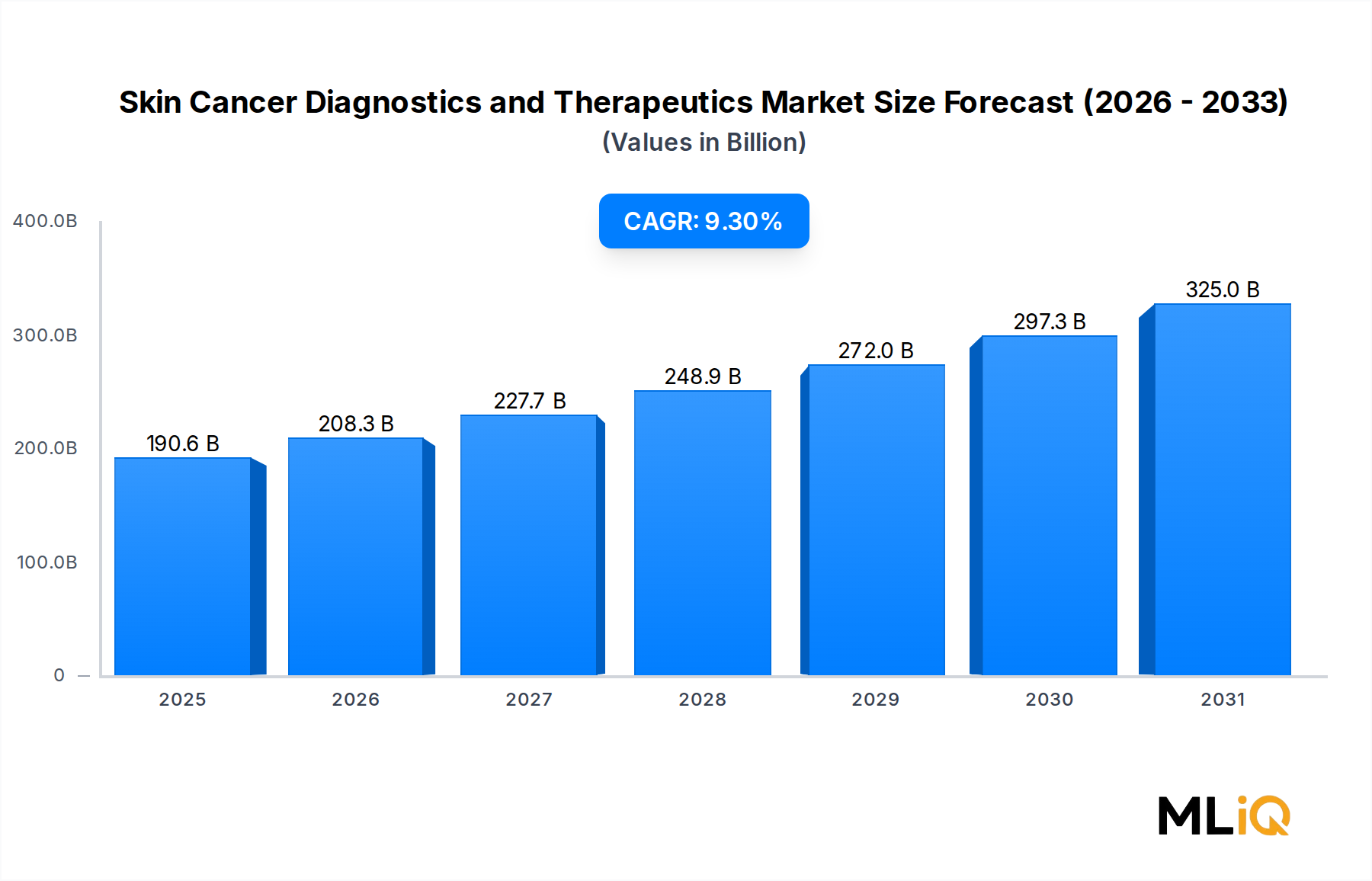

The global Skin Cancer Diagnostics and Therapeutics Market is valued at $190.6 billion in 2025 and is projected to expand at a compound annual growth rate (CAGR) of 9.3% through 2033, positioning it as one of the most dynamically growing segments within the broader life sciences sector. This robust growth trajectory is underpinned by a confluence of epidemiological, technological, and regulatory forces that are simultaneously expanding patient pools and accelerating clinical innovation.

Skin cancer remains the most commonly diagnosed malignancy worldwide, with melanoma, basal cell carcinoma (BCC), and squamous cell carcinoma (SCC) collectively accounting for millions of new diagnoses annually. The World Health Organization estimates that ultraviolet (UV) radiation-driven incidence rates are rising at approximately 3% per year in several high-income nations, particularly in North America and Oceania, creating a sustained and predictable demand pipeline for both diagnostic tools and therapeutic interventions.

Key demand drivers include the rapid commercialization of checkpoint inhibitor immunotherapies, the growing adoption of AI-assisted dermatoscopic imaging platforms, and the expanding use of sentinel lymph node biopsy techniques that improve staging accuracy and treatment selection. Regulatory agencies such as the U.S. FDA and EMA have accelerated approval pathways for novel immuno-oncology agents, compressing the time-to-market for next-generation therapies and incentivizing continued pipeline investment by leading pharmaceutical and diagnostics firms.

Macro tailwinds strengthening the market's outlook include heightened skin cancer screening awareness campaigns, improved reimbursement frameworks in North America and Western Europe, and the increasing integration of liquid biopsy and blood-test-based early detection modalities into standard clinical workflows. Furthermore, the aging global population—projected to see individuals aged 65 and above constitute over 16% of the global population by 2050—directly correlates with elevated skin cancer incidence, particularly for actinic keratoses (AK) and BCC.

From an investment perspective, the Skin Cancer Diagnostics and Therapeutics Market is attracting significant capital allocation across the pharmaceutical, medical device, and digital health subsectors. Companies are pivoting toward combination therapy regimens and companion diagnostic co-development strategies that improve patient stratification and treatment outcomes. The convergence of genomics, proteomics, and imaging-based diagnostics is reshaping the clinical landscape and creating new monetization avenues.

Looking ahead to 2033, the market is expected to surpass $390 billion in cumulative revenue contribution, driven by both volume growth in emerging economies and premium pricing dynamics in established markets for novel biologics and targeted agents. The next phase of market evolution will be defined by precision oncology integration, real-world evidence generation, and cross-sector collaborations between pharmaceutical companies and technology firms.

Among all therapeutic modalities available in the Skin Cancer Diagnostics and Therapeutics Market, immunotherapy has emerged as the dominant and fastest-consolidating segment by revenue share. As of 2025, immunotherapy-based treatments—primarily immune checkpoint inhibitors (ICIs) targeting the PD-1/PD-L1 and CTLA-4 pathways—account for an estimated 38% of total therapeutic revenues, a share that has grown from approximately 22% in 2019, reflecting a steep and sustained upward trajectory.

The dominance of immunotherapy is rooted in its clinical superiority over traditional modalities for advanced and metastatic melanoma, which historically carried a median overall survival of less than 12 months with chemotherapy alone. The introduction of agents such as pembrolizumab and nivolumab transformed the treatment paradigm by demonstrating five-year survival rates exceeding 40% in certain metastatic melanoma cohorts, outcomes that were previously inconceivable. This clinical differentiation has translated directly into high adoption rates among oncologists and premium reimbursement status in most developed healthcare systems.

Within the immunotherapy segment, combination regimens—pairing a PD-1 inhibitor with a CTLA-4 inhibitor—are gaining traction, particularly for patients with high tumor mutational burden (TMB-high) profiles. Bristol-Myers Squibb has been a pivotal architect of this approach, leveraging the nivolumab/ipilimumab combination across multiple skin cancer indications. AstraZeneca has similarly advanced its durvalumab portfolio into non-melanoma skin cancers, including cutaneous SCC, addressing a historically underserved patient population.

The non-melanoma immunotherapy pipeline is also accelerating. Cemiplimab, developed by Regeneron and marketed under Libtayo, received FDA approval for advanced cutaneous SCC and locally advanced BCC, significantly expanding the addressable immunotherapy market beyond melanoma. This approval catalyzed a wave of clinical trial activity targeting actinic keratoses (AK) progression prevention—a largely untapped preventive immunotherapy opportunity.

The segment's growing revenue share is also supported by expanding indications and geographic approvals. Regulatory filings in Japan, South Korea, and China for established checkpoint inhibitors are opening new revenue streams in Asia Pacific, where skin cancer incidence is rising due to changing lifestyle patterns and increased UV exposure. Reimbursement in these markets, while still evolving, is improving with health technology assessment (HTA) bodies increasingly recognizing the long-term cost-effectiveness of immunotherapy over repeated palliative chemotherapy cycles.

Key players consolidating their position within the immunotherapy-dominant segment include Eli Lilly, which has been investing in next-generation bispecific antibody platforms; Amgen, with its T-cell engager (BiTE) technology being evaluated in skin cancer; and Roche, which maintains a diversified immuno-oncology portfolio. Daiichi Sankyo has also entered the space through antibody-drug conjugate (ADC) platforms that combine the precision of targeted therapy with immunological mechanisms.

From a margin perspective, immunotherapy commands some of the highest average selling prices in the oncology space, with annual therapy costs routinely ranging from $120,000 to $250,000 per patient in the United States. These premium economics are expected to persist through the forecast period, supported by strong intellectual property protection and high barriers to biosimilar entry for large-molecule biologics. The segment's dominance is expected to further consolidate as adjuvant and neoadjuvant immunotherapy settings gain regulatory approval, adding incremental patient volume to an already expansive commercial base.

The Skin Cancer Diagnostics and Therapeutics Market is propelled by a set of well-quantified, structurally durable growth drivers, while simultaneously navigating constraints that moderate overall expansion velocity.

Driver 1: Rising Incidence and Screening Penetration. Global skin cancer incidence has increased by an estimated 24% over the past decade, with the American Cancer Society reporting over 100,000 new melanoma cases in the United States alone in 2024. Expanded national screening programs in Australia, Germany, and the UK have increased early-stage detection rates, directly expanding the diagnostics revenue base by bringing previously undiagnosed patients into clinical pathways.

Driver 2: Innovation in Targeted and Immuno-Oncology Pipelines. As of 2025, the FDA's oncology pipeline includes over 60 active IND applications for skin cancer indications, reflecting a historically high level of clinical investment. The Melanoma Therapeutics Market continues to attract the majority of this pipeline activity, given melanoma's high immunogenicity and biomarker tractability. BRAF/MEK inhibitor combinations, approved for BRAF V600E/K mutant melanoma, now serve an estimated 50% of eligible advanced melanoma patients.

Driver 3: Digital Diagnostics Adoption. Dermatoscopy-based AI platforms have achieved sensitivity rates exceeding 90% in clinical validation studies for melanoma detection, comparable to board-certified dermatologists. This is driving institutional adoption in primary care and teledermatology settings, broadening the diagnostic market footprint beyond specialist centers.

Constraint 1: High Therapy Costs and Reimbursement Gaps. Despite clinical efficacy, immunotherapy's annual cost burden of $120,000–$250,000 per patient creates access barriers in price-controlled markets across Asia Pacific, Latin America, and parts of Central and Eastern Europe, limiting total addressable market penetration.

Constraint 2: Resistance Mechanisms and Treatment Durability. Approximately 30–40% of patients treated with front-line checkpoint inhibitors develop acquired resistance within 18–24 months, necessitating costly second-line interventions and compressing long-term therapy revenues. This clinical reality drives R&D spending upward while introducing uncertainty in payer willingness-to-pay frameworks.

Constraint 3: Regulatory Fragmentation. Divergent approval timelines across the FDA, EMA, PMDA (Japan), and NMPA (China) create revenue recognition delays of 12–36 months for globally launched products, affecting cash flow cycles for mid-sized biopharmaceutical companies.

The competitive landscape of the Skin Cancer Diagnostics and Therapeutics Market is highly concentrated at the top, with a blend of large-cap pharmaceutical companies, diversified diagnostics players, and specialty oncology firms competing across therapeutic modalities and diagnostic platforms.

Eli Lilly: A growing oncology force leveraging its acquisition of Loxo Oncology's kinase inhibitor expertise; Lilly has positioned its pipeline to address BRAF-mutant and RAS-driven skin cancers, with multiple mid-stage clinical programs targeting novel resistance mechanisms.

AstraZeneca: Advancing durvalumab and its broader immuno-oncology portfolio into cutaneous malignancies, with particular emphasis on combination regimens co-developed with its AZ-MedImmune biologics platform targeting PD-L1 and CD73 pathways.

Bristol-Myers Squibb: The incumbent leader in melanoma immunotherapy through its Opdivo (nivolumab) and Yervoy (ipilimumab) franchise; BMS continues to define standard-of-care in advanced melanoma while expanding into neoadjuvant settings to capture earlier-stage patient populations.

Aqua Pharmaceuticals: Specializes in dermatology-specific pharmaceutical formulations, with a commercial portfolio targeting actinic keratoses (AK) and superficial BCC through topical and photodynamic therapy modalities.

GSK: Leveraging its oncology and vaccines infrastructure to develop novel therapeutic approaches in Merkel cell carcinoma and cutaneous SCC, while its BLENREP platform is being explored in antibody-based skin cancer applications.

Agilent: A critical enabler of the diagnostics segment through its genomic profiling instruments, next-generation sequencing (NGS) reagents, and SureSelect target enrichment systems used in companion diagnostic development and tumor mutational burden (TMB) quantification.

Roche: Commands a dual competitive advantage through its Genentech therapeutics division (atezolizumab pipeline) and its diagnostics division's cobas-based NGS and immunohistochemistry (IHC) platforms used in PD-L1 companion diagnostics.

Amgen: Deploying its talimogene laherparepvec (T-VEC) oncolytic virus platform for in-transit melanoma, while investing in BiTE antibody constructs that engage T-cells against skin cancer antigens.

Daiichi Sankyo: Entering the skin cancer space through its HER2-targeted and TROP2-targeted ADC platforms, with early clinical signals supporting efficacy in certain cutaneous malignancies with relevant antigen expression.

Elekta: A leading radiation oncology technology provider supplying stereotactic radiotherapy systems used in the treatment of primary and metastatic skin cancer lesions, particularly for patients ineligible for systemic therapy.

January 2025: Bristol-Myers Squibb received FDA Breakthrough Therapy Designation for a neoadjuvant nivolumab plus ipilimumab regimen in resectable stage III melanoma, signaling a potential paradigm shift toward pre-surgical immunotherapy applications.

February 2025: Roche announced positive Phase III data for its tiragolumab combined with atezolizumab in cutaneous SCC, demonstrating a 32% improvement in progression-free survival versus pembrolizumab monotherapy in PD-L1-high patients.

March 2025: Agilent Technologies launched its updated SureSelect Cancer All-In-One panel with enhanced TMB and microsatellite instability (MSI) co-detection capabilities, directly addressing skin cancer companion diagnostic requirements.

April 2025: AstraZeneca and Daiichi Sankyo announced an expanded co-development agreement to evaluate their TROP2-targeted ADC in combination with durvalumab for second-line cutaneous SCC patients post-ICI failure.

May 2025: The European Medicines Agency (EMA) granted a conditional marketing authorization for Amgen's T-VEC in combination with pembrolizumab for injectable unresectable melanoma lesions, expanding its approved geographic footprint beyond the United States.

June 2025: GSK reported interim Phase II results for its belantamab mafodotin derivative in Merkel cell carcinoma, with an objective response rate of 41% in a heavily pretreated cohort, generating significant clinical and investor interest.

August 2025: Elekta received CE marking for its next-generation Harmony Pro linear accelerator system optimized for superficial and cutaneous tumor radiotherapy, enhancing treatment precision for non-resectable skin cancers in European clinical settings.

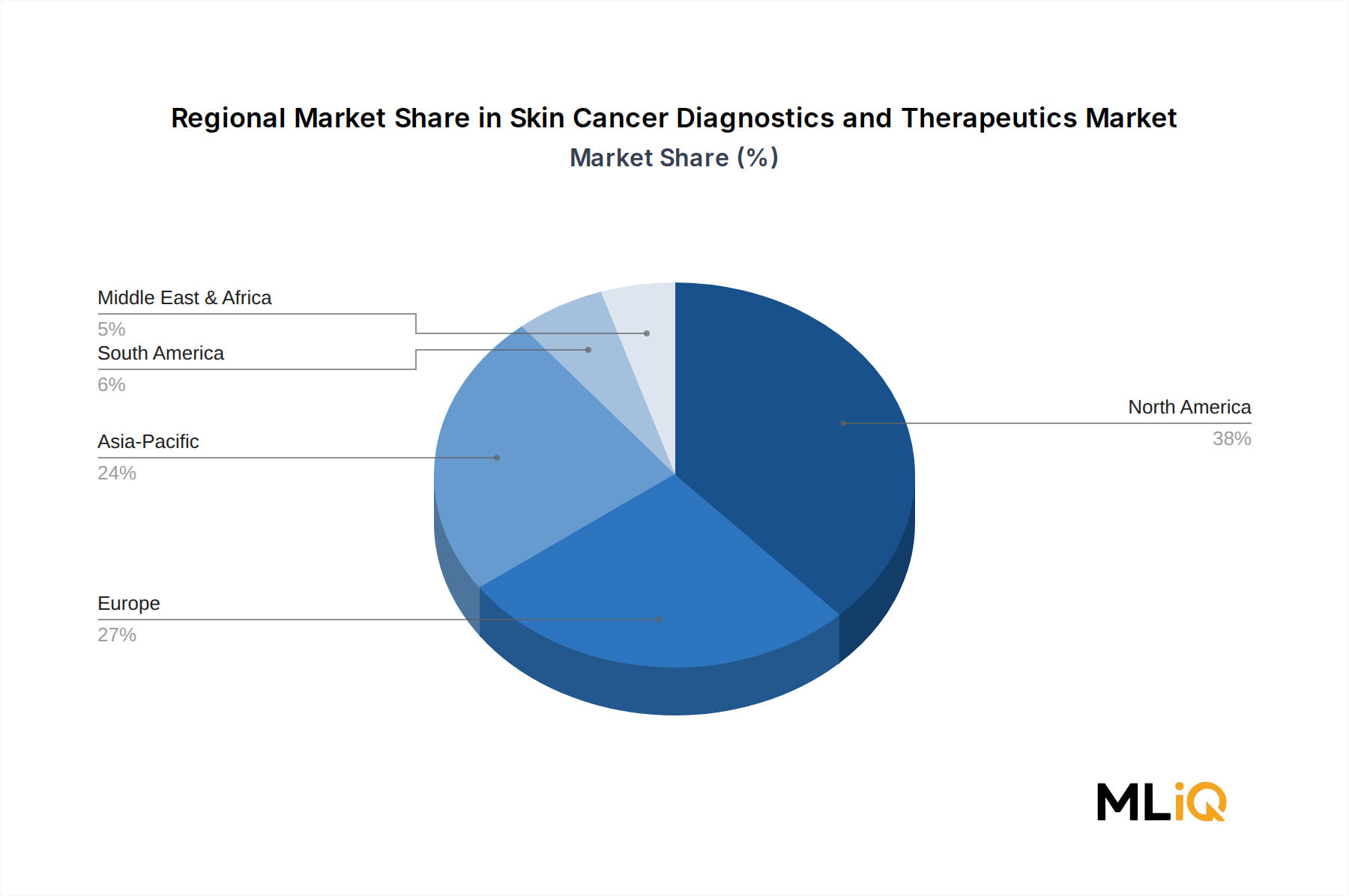

The Skin Cancer Diagnostics and Therapeutics Market exhibits substantial regional heterogeneity driven by differences in incidence rates, healthcare infrastructure, reimbursement policy, and pipeline access.

North America: North America dominates the global market, accounting for approximately 42% of total revenues in 2025, translating to roughly $80 billion in absolute value. The United States remains the single largest national market, driven by the highest per-capita spending on oncology therapeutics, robust FDA approval activity, and a well-established private insurance reimbursement ecosystem that supports premium immunotherapy pricing. Canada and Mexico contribute modestly, with Mexico showing accelerating growth linked to improved public healthcare oncology coverage. The regional CAGR is estimated at 8.6% through 2033.

Europe: Europe is the second-largest region, representing approximately 28% of global revenues. Germany, France, and the United Kingdom collectively anchor European demand, with well-funded national health systems providing structured reimbursement for approved immunotherapy agents. However, Health Technology Assessment (HTA) processes—particularly in Germany (G-BA) and France (HAS)—impose price negotiation timelines that compress manufacturer margins by an estimated 15–25% relative to U.S. list prices. Europe's regional CAGR stands at approximately 8.1%, moderated by pricing pressure but sustained by high incidence in sun-exposed populations in Southern Europe and Scandinavia.

Asia Pacific: Asia Pacific is the fastest-growing regional segment, with a projected CAGR of 11.4% through 2033, driven by rapidly rising skin cancer incidence in Australia, India, China, and South Korea. Australia remains the highest per-capita melanoma incidence country globally, supporting a disproportionately advanced diagnostics and therapeutics ecosystem relative to its population size. China and India present the largest volume-growth opportunities, as national health authorities expand oncology drug formularies and NGS-based diagnostics coverage. The region currently accounts for approximately 18% of global market revenues.

Latin America: Brazil and Argentina lead the Latin American segment, which represents approximately 6% of global revenues. Regional growth at a CAGR of 9.8% is supported by expanding private oncology hospital networks and growing biosimilar immunotherapy adoption that is improving access without full originator pricing burdens.

Middle East & Africa: This region

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 9.3% from 2020-2034 |

| Segmentation |

|

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Comprehensive validation mechanisms ensuring market intelligence accuracy, reliability, and adherence to international standards.

500+ data sources cross-validated

200+ industry specialists validation

NAICS, SIC, ISIC, TRBC standards

Continuous market tracking updates

Factors such as are projected to boost the Skin Cancer Diagnostics and Therapeutics Market market expansion.

Key companies in the market include Eli Lilly, AstraZeneca, Bristol-Myers Squibb, Aqua Pharmaceuticals, GSK, Agilent, Roche, Amgen, Daiichi Sankyo, Elekta.

The market segments include Type, Based Cell Carcinoma, Squamous Cell Carcinoma, Therapy, Diagnosis, End User.

The market size is estimated to be USD 190.6 billion as of 2022.

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3690, USD 5820, and USD 9870 respectively.

The market size is provided in terms of value, measured in billion and volume, measured in .

Yes, the market keyword associated with the report is "Skin Cancer Diagnostics and Therapeutics Market," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Skin Cancer Diagnostics and Therapeutics Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.