1. What are the major growth drivers for the Endoscopy Fluid Management Market market?

Factors such as are projected to boost the Endoscopy Fluid Management Market market expansion.

+1 2315155523

Endoscopy Fluid Management Market

Endoscopy Fluid Management Market

Market Lens IQ is a global market intelligence and strategic consulting firm delivering advanced syndicated research reports, customized industry analysis, competitive intelligence, and data-driven advisory solutions to organizations across international markets. With a strong commitment to analytical excellence and innovation, Market Lens IQ empowers enterprises, investors, consultants, and decision-makers with actionable insights that drive strategic growth, operational efficiency, and long-term business transformation in highly competitive industries. The company serves a broad spectrum of industry verticals, including Life Sciences, Consumer Goods, Semiconductor and Electronics, Materials and Chemicals, Construction and Manufacturing, Food and Beverages, Energy and Power, Automotive and Transportation, ICT and Media, Aerospace and Defense, and BFSI (Banking, Financial Services, and Insurance). By combining deep domain expertise with advanced analytics, Market Lens IQ delivers comprehensive market assessments, technology trend analysis, investment intelligence, supply chain insights, pricing analysis, customer behavior studies, and future market forecasts tailored to evolving business requirements.

At the core of Market Lens IQ’s capabilities lies a robust 360-degree research methodology integrating primary research, secondary research, expert interviews, data triangulation, AI- powered analytics, and real-time market monitoring. Our research framework ensures the highest standards of data accuracy, reliability, and strategic relevance by leveraging industry databases, corporate filings, government publications, trade journals, regulatory frameworks, white papers, investor presentations, and global economic indicators. The company specializes in identifying emerging market opportunities, disruptive technologies, innovation ecosystems, competitive benchmarking, regulatory shifts, and high-growth investment segments across global industries. Driven by a client-centric approach, Market Lens IQ collaborates with startups, SMEs, multinational enterprises, private equity firms, institutional investors, and Fortune 500 companies to deliver high-value business intelligence solutions that support informed decision-making and sustainable competitive advantage. Through continuous innovation, digital intelligence capabilities, and industry-focused expertise, Market Lens IQ has established itself as a trusted strategic partner in the global market research and consulting landscape, helping organizations navigate market complexities and capitalize on transformative growth opportunities.

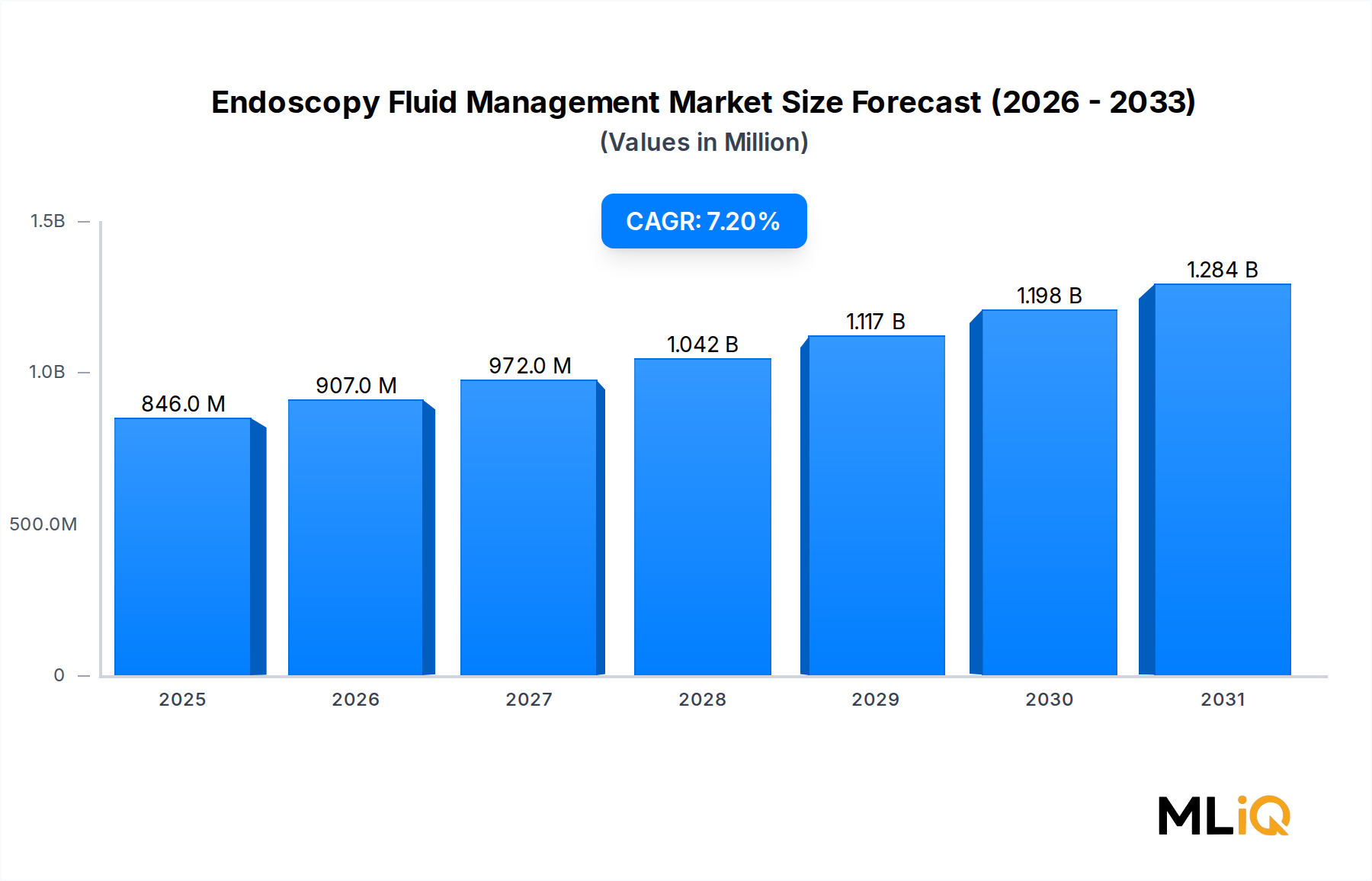

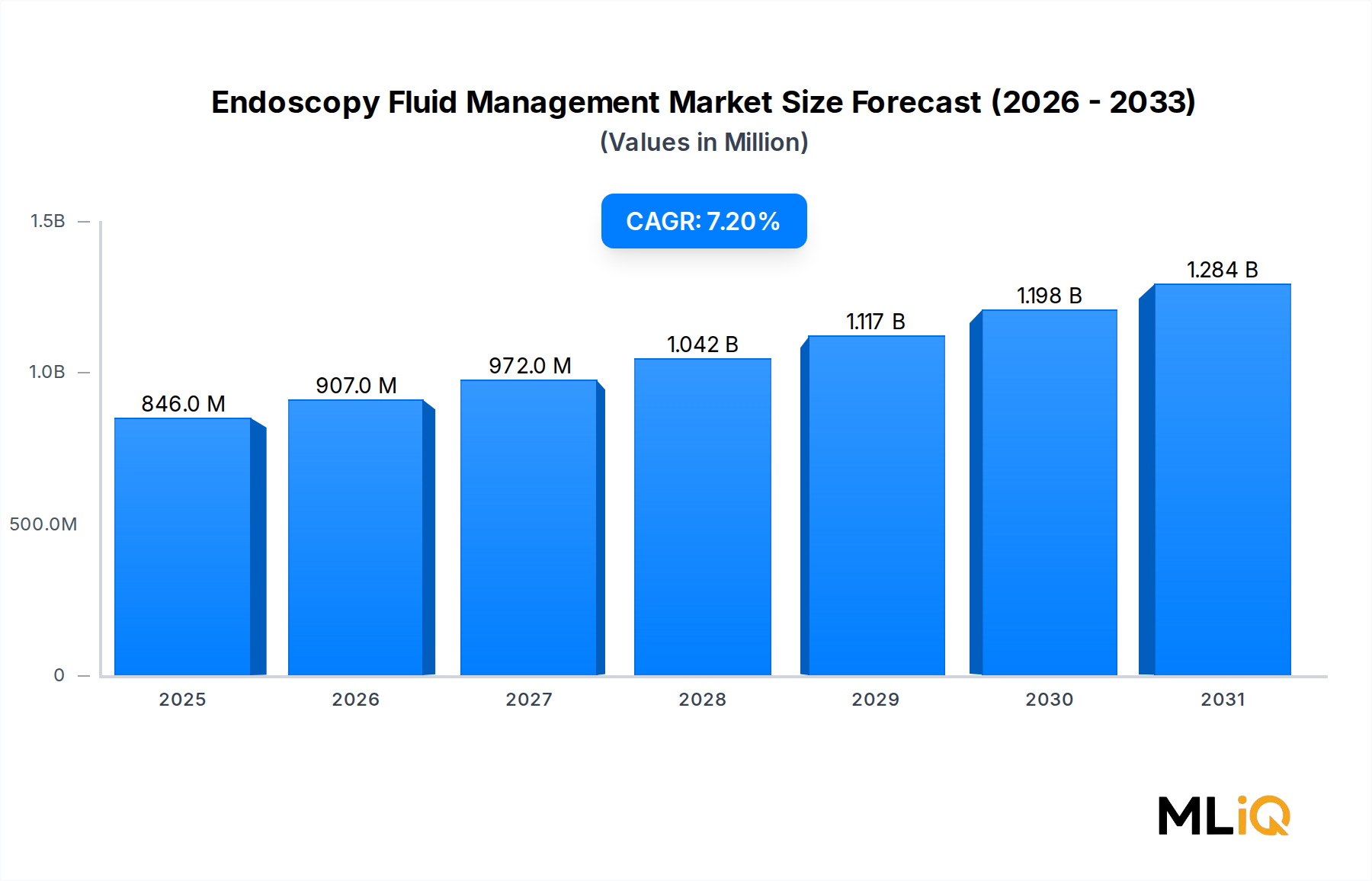

The global Endoscopy Fluid Management Market was valued at $845.99 million in the base assessment period and is projected to expand at a compound annual growth rate (CAGR) of 7.2% through 2033, underscoring robust, sustained demand across surgical disciplines worldwide. This valuation trajectory positions the market to surpass the $1.5 billion threshold by the early 2030s, driven by a convergence of clinical, demographic, and technological forces that are reshaping fluid management protocols in minimally invasive procedures.

At its core, endoscopy fluid management encompasses systems and accessories that regulate the instillation, pressure, flow, and evacuation of distension media and irrigation fluids during endoscopic procedures. The clinical imperative for precise fluid balance management has intensified as complication rates associated with fluid overload — including hyponatremia and pulmonary edema — remain measurable concerns in prolonged hysteroscopic and laparoscopic interventions. Regulatory bodies across North America and Europe have progressively tightened thresholds for permissible fluid deficit, compelling hospitals to upgrade manual or semi-automated systems to fully integrated, sensor-driven platforms.

Key macro tailwinds include the global rise in chronic diseases requiring endoscopic intervention, particularly colorectal cancer, uterine fibroids, and gastrointestinal disorders. The World Health Organization estimates that colorectal cancer alone accounts for over 1.9 million new cases annually, a figure that directly expands the endoscopic procedural base. Simultaneously, the aging population in North America, Western Europe, and Japan is generating structurally higher demand for diagnostic and therapeutic endoscopy, with patients over 65 representing a disproportionate share of endoscopic volume.

Technological advancements — including real-time fluid deficit monitoring, closed-loop pressure regulation, and integration with electronic medical records — are elevating average selling prices while reducing per-procedure complication costs, a dual dynamic that strengthens both market revenue and end-user adoption incentives. The migration from reusable to single-use accessories is accelerating, particularly in infection-sensitive environments post-pandemic, creating an ongoing consumables revenue stream that enhances market stickiness.

The competitive landscape is moderately consolidated, with the top five players commanding an estimated 55–60% of global revenue, yet meaningful white space exists in emerging markets where hospital infrastructure is expanding rapidly. Strategic partnerships between fluid management specialists and broader surgical platform companies are becoming common deal structures, as integrated operating room ecosystems gain preference over point-solution purchases.

Looking forward to 2033, the market outlook remains constructive. Procedure volume growth, premiumization of fluid management technology, and the broadening of endoscopic indications into previously open-surgery domains will collectively sustain the 7.2% CAGR, making this one of the more resilient sub-segments within the Endoscopic Devices Market.

Within the product segmentation of the Endoscopy Fluid Management Market, the endoscopy fluid management system sub-segment commands the largest share of revenue and is expected to maintain its leadership throughout the forecast period ending 2033. This dominance reflects the capital-intensive, high-value nature of integrated system platforms relative to standalone accessories, and the strategic priority hospitals place on acquiring comprehensive, validated solutions rather than assembling piecemeal configurations.

Endoscopy fluid management systems are purpose-built platforms that combine electronic pump mechanisms, pressure sensors, flow meters, deficit calculation algorithms, and user interface displays into a single cohesive unit. Their clinical value proposition is anchored in real-time fluid balance monitoring, which enables surgical teams to track inflow and outflow volumes continuously during procedures such as hysteroscopy and laparoscopy — applications where fluid absorption into the vascular system can precipitate life-threatening electrolyte disturbances if undetected. The shift from gravity-fed or manual pump systems to electronically controlled, closed-loop platforms has been a defining technological transition, with leading hospitals in North America and Europe having largely completed this upgrade cycle and markets in Asia Pacific and the Middle East now progressing through equivalent adoption curves.

Revenue concentration within the systems sub-segment is reinforced by several structural factors. First, average unit prices for fully integrated fluid management systems range from $15,000 to over $50,000 depending on feature complexity, procedure versatility, and connectivity capabilities — figures that dwarf accessory pricing and thus anchor segment revenue disproportionately even when unit volumes are lower. Second, replacement cycles of 5–8 years create predictable upgrade demand that sustains baseline revenue independent of procedure volume fluctuations. Third, system vendors typically bundle multi-year service contracts and software update agreements, generating annuity-like revenues that smooth cyclical volatility.

Key players maintaining strong positions in the systems sub-segment include Stryker Corporation, CONMED Corporation, and Olympus America Inc., each of which offers differentiated platforms targeting specific endoscopic specialties. Stryker's fluid management systems are particularly prominent in arthroscopy and laparoscopy, with pressure management precision cited as a competitive differentiator. CONMED has focused on integration with its broader visualization ecosystem, while Olympus leverages its dominant endoscope install base to drive co-adoption of compatible fluid management platforms.

The systems segment's share is not merely stable — it is gradually consolidating as hospitals consolidate vendor relationships, preferring single-source procurement for fluid management to simplify training, maintenance, and data integration. This vendor consolidation dynamic benefits incumbents with broad specialty coverage and penalizes niche or single-indication system providers.

Emerging within the systems segment is a class of next-generation platforms featuring AI-assisted deficit prediction, wireless connectivity for remote monitoring, and compatibility with robotic surgical systems. These premium-tier systems are currently commanding price premiums of 20–35% over standard electronic platforms and are gaining initial traction in tertiary-care academic medical centers. As the technology matures and manufacturing costs decline, broader adoption across community hospitals is expected to sustain systems segment growth at or above the overall market CAGR of 7.2% through 2033.

The accessories sub-segment — comprising tubing sets, distension media bags, collection canisters, and connectors — serves as a volume complement to the systems segment, generating recurring per-procedure revenue. However, its lower per-unit pricing means that even at significantly higher unit volumes, it represents a smaller share of total market revenue, confirming the systems segment's structural dominance.

Several high-impact drivers and quantifiable constraints define the growth trajectory of the Endoscopy Fluid Management Market through 2033.

Driver 1 — Rising Minimally Invasive Procedure Volume: Global laparoscopic procedure volumes have grown at approximately 6–8% annually over the past five years, driven by clinical preference, faster recovery times, and payer incentives favoring outpatient procedures. The Minimally Invasive Surgery Market is directly correlated with endoscopic fluid management demand, as every laparoscopic or hysteroscopic case requires dedicated fluid management support. The American College of Obstetricians and Gynecologists reports that hysteroscopy is now performed in over 600,000 procedures annually in the United States alone, each requiring fluid deficit monitoring.

Driver 2 — Patient Safety Regulations: Regulatory mandates in the United States, United Kingdom, Germany, and France now require quantitative fluid deficit tracking in hysteroscopic procedures, effectively mandating electronic fluid management systems over manual alternatives. Non-compliance carries reimbursement penalties and liability exposure, accelerating institutional upgrade cycles.

Driver 3 — Aging Demographics: Populations aged 65 and above in OECD countries are projected to grow by 35% between 2023 and 2040, directly expanding the endoscopic procedure base for conditions disproportionately affecting older patients, including polyps, fibroids, and gastrointestinal cancers.

Constraint 1 — High Capital Cost: System acquisition costs exceeding $30,000–$50,000 create significant budget barriers for smaller hospitals, outpatient surgery centers, and healthcare facilities in lower-middle-income countries. This constraint is partially offset by leasing and pay-per-procedure financing models, but upfront capital requirements remain a meaningful adoption inhibitor in price-sensitive geographies.

Constraint 2 — Reimbursement Fragmentation: Inconsistent coding and reimbursement structures for fluid management-intensive procedures across Asia Pacific and Latin American markets reduce financial incentives for facility investment in premium systems, constraining market penetration in these high-growth regions relative to their procedure volume potential.

The competitive landscape of the Endoscopy Fluid Management Market features a blend of large diversified medical device conglomerates and specialized endoscopy-focused companies, each pursuing differentiated strategies across product innovation, geographic expansion, and service integration.

B. Braun SE: A leading European medical device and pharmaceutical company, B. Braun maintains a strong portfolio of irrigation and fluid management solutions with particular depth in hospital infusion and surgical fluid systems, leveraging its broad hospital relationships across Europe and Asia Pacific to drive co-adoption.

Arthrex, Inc.: Arthrex is a dominant force in arthroscopic fluid management, offering the Continuous Wave pump system widely regarded as a benchmark for joint distension pressure control; its market position is reinforced by deep orthopedic surgeon relationships and an extensive global distribution network.

Olympus America Inc.: Olympus leverages its commanding share of the global endoscope install base to position compatible fluid management platforms as natural extensions of its integrated visualization ecosystem, creating strong switching cost advantages in gastrointestinal and gynecological endoscopy segments.

STERIS plc: STERIS integrates fluid management considerations within its broader operating room workflow and sterilization infrastructure, appealing to hospital systems seeking consolidated surgical environment solutions and infection control compliance.

Stryker Corporation: Stryker's fluid management offerings, particularly in the arthroscopy and laparoscopy domains, are distinguished by pressure precision technology and seamless integration with its camera and visualization platforms, making it a preferred systems vendor in North American tertiary care centers.

CONMED Corporation: CONMED has built a cohesive arthroscopy and laparoscopy fluid management portfolio that competes directly with Stryker and Arthrex, differentiating on pricing flexibility, service responsiveness, and a growing presence in international markets including Latin America and Southeast Asia.

Medtronic plc: Medtronic applies its scale and global regulatory expertise to offer fluid management solutions as part of integrated minimally invasive surgery suites, with particular strength in laparoscopic and robotic-assisted procedure environments.

Hologic Inc.: Hologic's fluid management presence is concentrated in gynecological endoscopy, where its hysteroscopy platform integrates fluid deficit management as a core procedural safety feature targeting women's health specialists globally.

KARL STORZ SE & Co. KG: A privately held endoscopy specialist with one of the broadest product portfolios in the sector, KARL STORZ integrates fluid management accessories and systems within its complete endoscopic tower configurations, benefiting from strong brand loyalty among surgeons.

COMEG medical technologies: A specialized European manufacturer focused on fluid management systems for endourology and gynecology, COMEG competes on clinical precision and regulatory compliance in European hospital markets.

January 2023: Stryker Corporation announced an expanded fluid management system line with integrated deficit alarm functionality designed for laparoscopic and hysteroscopic procedures, targeting upgrades at over 2,000 U.S. hospital accounts.

March 2023: CONMED Corporation received CE Mark approval for an updated fluid management pump with enhanced wireless data connectivity, enabling real-time fluid balance data transmission to hospital information systems across European markets.

June 2023: Arthrex, Inc. expanded its international distribution agreement for arthroscopic fluid management systems into 12 new Asia Pacific markets, including South Korea, Thailand, and Malaysia, aligning with rising orthopedic procedure volumes in the region.

September 2023: Hologic Inc. published clinical outcomes data demonstrating a 42% reduction in fluid overload complications when using its integrated hysteroscopy fluid management system versus manual measurement protocols, strengthening evidence-based adoption arguments.

November 2023: Medtronic plc announced a strategic collaboration with a robotic surgery platform developer to co-develop next-generation fluid management integration protocols compatible with robotic-assisted laparoscopic systems, expected to reach commercial availability by 2025.

February 2024: B. Braun SE completed a portfolio acquisition of a European single-use irrigation catheter manufacturer, expanding its consumables footprint in the Endoscopy Fluid Management Market.

May 2024: KARL STORZ SE & Co. KG introduced a modular fluid management tower system compatible with its complete endoscopy visualization suite, enabling hospitals to standardize fluid management across multiple surgical specialties within a single platform architecture.

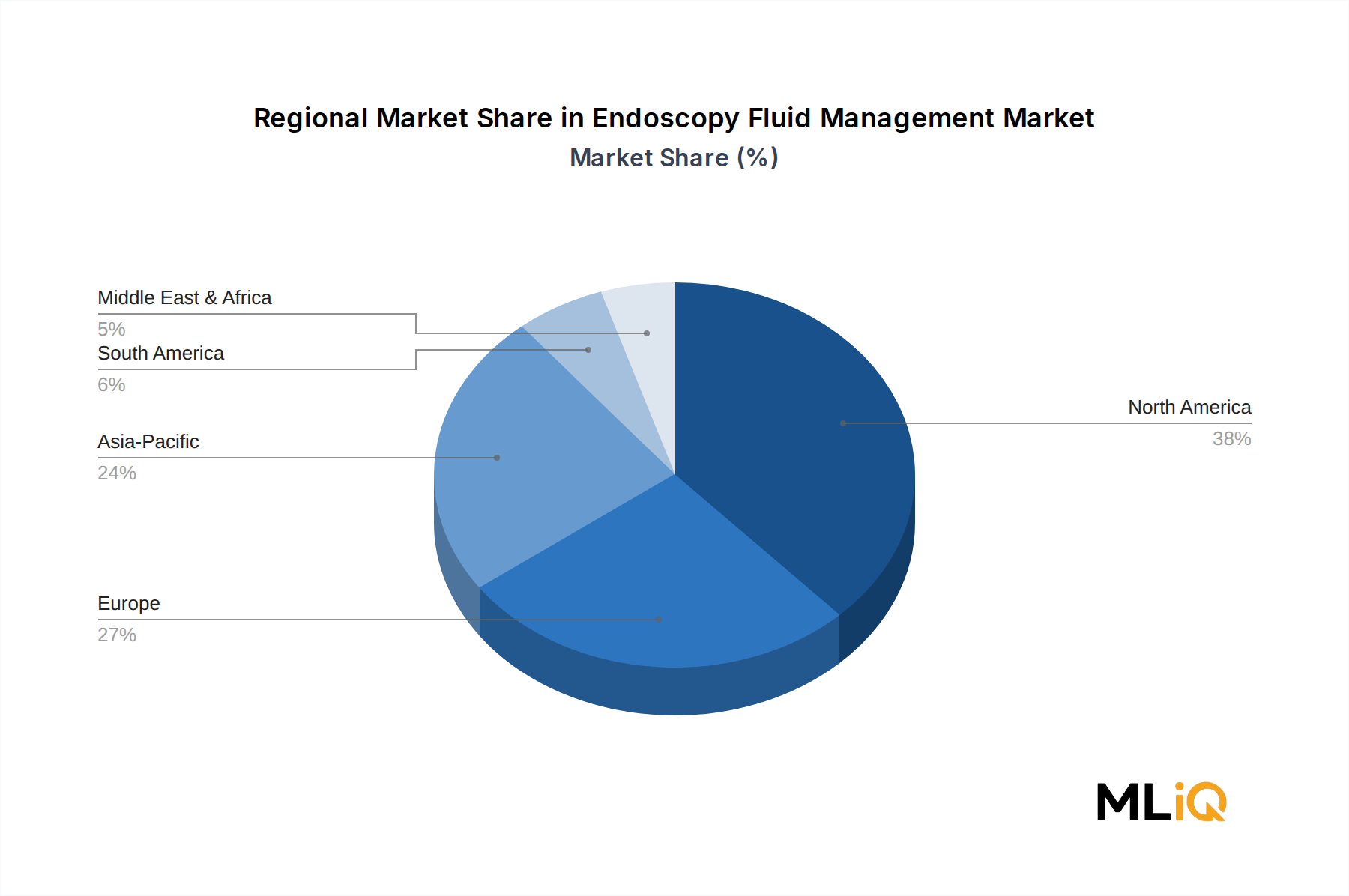

Geographic analysis of the Endoscopy Fluid Management Market reveals significant variation in market maturity, growth velocity, and demand drivers across the five major regions.

North America: North America represents the single largest regional market, accounting for an estimated 38–40% of global revenue. The United States anchors this position through a combination of high per-capita procedure volumes, established reimbursement infrastructure, and early adoption of premium fluid management technologies. The regional CAGR is estimated at 6.0–6.5% through 2033, reflecting a maturing but consistently high-value market. Canada and Mexico contribute incrementally, with Mexico showing above-average growth as private hospital infrastructure expands. The primary demand driver in North America is regulatory compliance pressure and liability management, which sustains institutional investment in advanced systems even during budget-constrained periods.

Europe: Europe constitutes approximately 28–30% of global market revenue, with Germany, the United Kingdom, and France serving as the dominant national markets. The European regional CAGR is estimated at 6.5–7.0%, slightly above North America, driven by ongoing hospital modernization programs and stringent EU Medical Device Regulation (MDR) compliance requirements that are accelerating replacement of legacy fluid management equipment. The Nordics and Benelux markets, while smaller in absolute terms, exhibit high adoption rates of premium systems aligned with their advanced healthcare infrastructure.

Asia Pacific: Asia Pacific is the fastest-growing regional market, projected to expand at a CAGR of 9.0–10.0% through 2033, the highest among all geographies. China and India are the primary volume drivers, supported by government-funded hospital expansion programs and rising private healthcare investment. Japan and South Korea contribute significant revenue from a smaller but highly sophisticated procedural base. The primary demand driver is infrastructure buildout and rising surgical procedure volumes in tier-2 and tier-3 cities.

Middle East & Africa: This region accounts for approximately 6–8% of global revenue but is growing at an estimated CAGR of 7.5–8.0%, fueled by healthcare infrastructure investment in GCC countries including Saudi Arabia and the UAE. Turkey is emerging as a significant market with modernizing hospital systems and growing endoscopy adoption.

South America: South America represents roughly 5–7% of global revenue, led by Brazil and Argentina. Regional growth is tempered by reimbursement inconsistencies and economic volatility, with a CAGR of approximately 6.0% projected through 2033.

The regulatory environment governing the Endoscopy Fluid Management Market is multifaceted, spanning device classification standards, clinical practice guidelines, and institutional safety mandates across key geographies.

In the United States, fluid management systems and accessories are regulated by the Food and Drug Administration (FDA) primarily under Class II medical device classifications, requiring 510(k) premarket notification clearance. The FDA's focus on software-enabled medical devices has intensified scrutiny of digitally integrated fluid management platforms, with updated guidance on Software as a Medical Device (SaMD) released in 2023 directly applicable to AI-assisted fluid deficit monitoring functions. Failure mode and data security requirements for networked hospital devices are adding regulatory complexity and development cost for next-generation platforms.

In

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 7.2% from 2020-2034 |

| Segmentation |

|

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Comprehensive validation mechanisms ensuring market intelligence accuracy, reliability, and adherence to international standards.

500+ data sources cross-validated

200+ industry specialists validation

NAICS, SIC, ISIC, TRBC standards

Continuous market tracking updates

Factors such as are projected to boost the Endoscopy Fluid Management Market market expansion.

Key companies in the market include B. Braun SE, Arthrex, Inc., Olympus america inc, STERIS plc, Stryker Corporation, CONMED Corporation, Medtronic plc, Hologic Inc., KARL STORZ SE & Co. KG, COMEG medical technologies.

The market segments include Product, Application, End User.

The market size is estimated to be USD 845.99 million as of 2022.

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3840, USD 6090, and USD 10500 respectively.

The market size is provided in terms of value, measured in million and volume, measured in .

Yes, the market keyword associated with the report is "Endoscopy Fluid Management Market," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Endoscopy Fluid Management Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.