1. What are the major growth drivers for the Chondroitin Sulfate market by Type market?

Factors such as are projected to boost the Chondroitin Sulfate market by Type market expansion.

+1 2315155523

Chondroitin Sulfate market by Type

Chondroitin Sulfate market by Type

Market Lens IQ is a global market intelligence and strategic consulting firm delivering advanced syndicated research reports, customized industry analysis, competitive intelligence, and data-driven advisory solutions to organizations across international markets. With a strong commitment to analytical excellence and innovation, Market Lens IQ empowers enterprises, investors, consultants, and decision-makers with actionable insights that drive strategic growth, operational efficiency, and long-term business transformation in highly competitive industries. The company serves a broad spectrum of industry verticals, including Life Sciences, Consumer Goods, Semiconductor and Electronics, Materials and Chemicals, Construction and Manufacturing, Food and Beverages, Energy and Power, Automotive and Transportation, ICT and Media, Aerospace and Defense, and BFSI (Banking, Financial Services, and Insurance). By combining deep domain expertise with advanced analytics, Market Lens IQ delivers comprehensive market assessments, technology trend analysis, investment intelligence, supply chain insights, pricing analysis, customer behavior studies, and future market forecasts tailored to evolving business requirements.

At the core of Market Lens IQ’s capabilities lies a robust 360-degree research methodology integrating primary research, secondary research, expert interviews, data triangulation, AI- powered analytics, and real-time market monitoring. Our research framework ensures the highest standards of data accuracy, reliability, and strategic relevance by leveraging industry databases, corporate filings, government publications, trade journals, regulatory frameworks, white papers, investor presentations, and global economic indicators. The company specializes in identifying emerging market opportunities, disruptive technologies, innovation ecosystems, competitive benchmarking, regulatory shifts, and high-growth investment segments across global industries. Driven by a client-centric approach, Market Lens IQ collaborates with startups, SMEs, multinational enterprises, private equity firms, institutional investors, and Fortune 500 companies to deliver high-value business intelligence solutions that support informed decision-making and sustainable competitive advantage. Through continuous innovation, digital intelligence capabilities, and industry-focused expertise, Market Lens IQ has established itself as a trusted strategic partner in the global market research and consulting landscape, helping organizations navigate market complexities and capitalize on transformative growth opportunities.

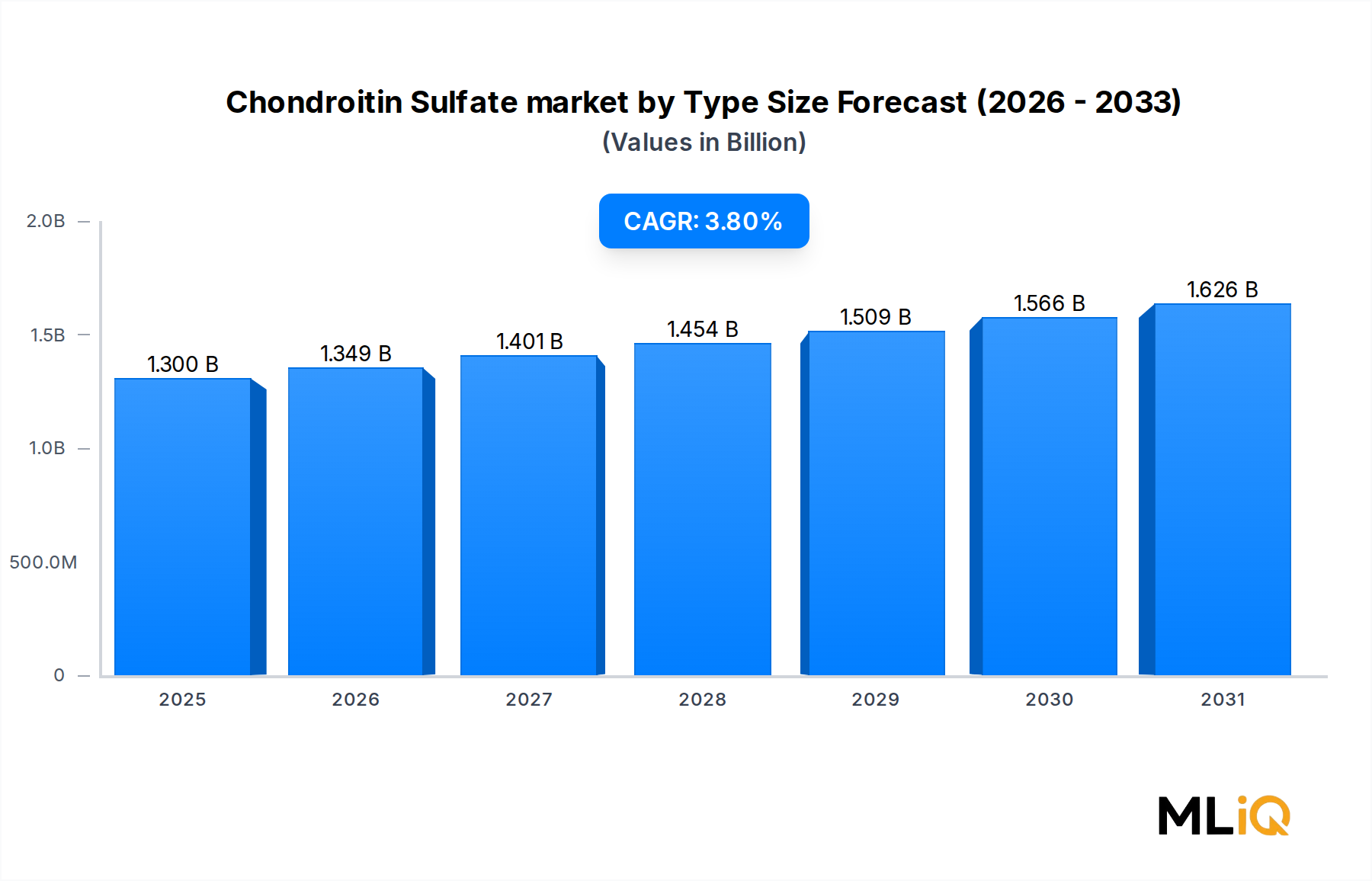

The global Chondroitin Sulfate market by Type is valued at $1.3 billion in 2025 and is projected to expand at a compound annual growth rate (CAGR) of 3.8% through the forecast horizon. This steady progression reflects a confluence of aging demographics, rising awareness of musculoskeletal health, and broadening applications across pharmaceutical, nutraceutical, cosmetic, and veterinary end-use segments.

Demand for chondroitin sulfate continues to be anchored by its proven efficacy in osteoarthritis management, a condition affecting over 500 million individuals globally according to the World Health Organization. As the global population aged 60 and above is expected to double by 2050, the structural demand for joint health modalities remains robust. The Dietary Supplements Market is directly intertwined with chondroitin sulfate's commercial trajectory, given that the compound is predominantly consumed in supplement form across North America, Europe, and increasingly Asia Pacific.

Key demand drivers include escalating healthcare expenditures, greater consumer inclination toward preventive health management, and favorable clinical evidence supporting chondroitin sulfate's role in cartilage protection. The market is also benefiting from expansion in the pet care industry, where chondroitin sulfate formulations are increasingly prescribed for canine joint conditions, creating meaningful cross-segment revenue diversification.

Macro tailwinds such as rising disposable incomes in emerging economies, e-commerce-driven accessibility of nutraceutical products, and an expanding base of health-conscious millennial consumers are accelerating market penetration beyond traditional pharmaceutical channels. Furthermore, investment in bioavailability enhancement technologies — including nano-encapsulation and sustained-release formats — is elevating product premiumization opportunities.

From a type-segmentation perspective, capsule form currently commands the largest revenue share, driven by consumer preference for convenient, pre-dosed formats and favorable shelf-life characteristics. Tablet form occupies a secondary position, while powder form is gaining traction in sports nutrition and functional food applications.

Restrictive factors include raw material price volatility, particularly for bovine and shark-derived chondroitin, as well as regulatory scrutiny over sourcing transparency and species-specific labeling standards. Nevertheless, the Nutraceuticals Market at large is providing a sustained platform for market growth, with chondroitin sulfate positioned as a cornerstone active ingredient.

The forward-looking outlook remains constructive. Innovation in synthetic and fermentation-derived chondroitin sulfate is expected to mitigate supply-chain dependencies on animal-sourced raw materials, while expanding the addressable market among vegan and vegetarian consumer cohorts. Overall, the market is poised for consistent, moderate growth through the end of the decade.

Among the three primary type segments — capsule form, tablet form, and powder form — capsule form has consistently asserted dominance in the Chondroitin Sulfate market by Type. This segment commands an estimated revenue share exceeding 45% of total market value in 2025, driven by a combination of consumer preference, manufacturing scalability, and distribution channel alignment.

Capsule form's leadership is rooted in its superior swallowability and taste-masking properties relative to tablets. For a compound such as chondroitin sulfate, which carries a characteristic odor and flavor profile derived from its animal-source precursors, encapsulation provides an essential palatability advantage that directly influences consumer compliance rates. Clinical adherence studies in nutraceutical categories consistently show that capsule-format supplements record higher long-term consumption rates than tablet equivalents, a factor that resonates with healthcare providers recommending chondroitin sulfate for chronic joint conditions.

From a manufacturing standpoint, capsule production workflows at scale offer flexibility in fill weight and combination formulation. Many commercially successful joint health products combine chondroitin sulfate with glucosamine, methylsulfonylmethane (MSM), or hyaluronic acid within a single capsule, enhancing perceived value and enabling premium pricing strategies. This co-formulation capability has been a decisive factor in the expansion of the Joint Health Supplements Market, where combination products now account for a growing majority of new product launches.

Key players actively reinforcing the capsule segment's dominance include Bioiberica, which leverages proprietary BCHS (bovine chondroitin high-specification) material in capsule-format pharmaceutical-grade products; Seikagaku Corporation, whose pharmaceutical-grade chondroitin sulfate is deployed in capsule formulations distributed through hospital and clinic channels in Japan and Europe; and TSI Group, a major supplier of bulk chondroitin sulfate to branded supplement manufacturers who predominantly favor capsule output formats.

The share of capsule form is showing consolidation rather than rapid expansion, as tablet form exhibits a moderate recovery trajectory in markets where tablet manufacturing infrastructure is deeply embedded — particularly in South and Southeast Asia. However, capsule form's structural advantages, including compatibility with liquid-fill formats for enhanced bioavailability variants, are expected to sustain its dominant position through at least 2030.

Powder form, while the smallest segment by current revenue share, is experiencing the fastest sub-segment growth rate, estimated at a CAGR of approximately 5.2%, owing to its incorporation into functional beverages, sports nutrition powders, and bulk compounding applications. This growth does not threaten capsule dominance in the near term but signals an ongoing diversification of delivery-format preferences.

Regionally, North America and Europe are the primary markets for capsule-format chondroitin sulfate, reflecting mature supplement industries where soft-gel and hard-shell capsule technologies are widely standardized. Asia Pacific, particularly China and Japan, presents a hybrid landscape where both capsule and tablet forms coexist across pharmaceutical and nutraceutical channels, reflecting distinct regulatory classification norms that influence dosage format selection.

In summary, the capsule form segment's dominance in the Chondroitin Sulfate market by Type is structurally underpinned by consumer preference, co-formulation versatility, and distribution alignment, and is expected to maintain its leading position throughout the forecast period.

The Chondroitin Sulfate market by Type is shaped by a set of quantifiable drivers and measurable constraints that collectively define its 3.8% CAGR trajectory through the projection period.

Driver 1 — Aging Global Population and Osteoarthritis Prevalence: With more than 500 million people affected by osteoarthritis globally and the WHO projecting the condition to be among the top ten causes of disability by 2030, the therapeutic demand for chondroitin sulfate remains structurally elevated. This driver is particularly acute in North America and Europe, where geriatric populations constitute a rising proportion of national demographics.

Driver 2 — Expansion of Pet Care and Veterinary Applications: The global pet supplement industry exceeded $700 million in 2024, with joint health products for dogs representing the single largest sub-category. Chondroitin sulfate's use in pet food and veterinary supplements is a high-growth channel, with animal-use formulations growing at an estimated CAGR of 6.1% — significantly outpacing the overall market rate. The Animal Feed Ingredients Market expansion is a key macro tailwind supporting this driver.

Driver 3 — Integration into Cosmetics and Personal Care: Chondroitin sulfate's moisturizing and film-forming properties have attracted interest from dermatological formulators. Its incorporation into anti-aging serums and topical biomaterials represents a newer but expanding revenue channel. The Cosmeceuticals Market is increasingly recognizing chondroitin sulfate as a bioactive ingredient with functional differentiation value.

Constraint 1 — Raw Material Supply Volatility: Approximately 70% of global chondroitin sulfate is still derived from bovine trachea and porcine cartilage. Disease events such as bovine spongiform encephalopathy (BSE) outbreaks and African swine fever have historically disrupted supply chains, contributing to price spikes exceeding 20–30% within short windows. The Bovine-Derived Ingredients Market is particularly sensitive to such disruptions.

Constraint 2 — Regulatory Heterogeneity: Chondroitin sulfate is classified as a pharmaceutical drug in several European jurisdictions (notably Germany, France, and Italy) but as a dietary supplement in the United States. This classification divergence increases compliance costs, elongates time-to-market in regulated geographies, and complicates harmonized global launch strategies.

Constraint 3 — Competition from Synthetic Alternatives: Advances in fermentation-based hyaluronic acid and synthetic glycosaminoglycan analogs are providing formulators with lower-cost, non-animal-sourced alternatives, creating substitution pressure especially in cost-sensitive Asian and Latin American markets.

The competitive landscape of the Chondroitin Sulfate market by Type is characterized by a mix of vertically integrated API manufacturers, specialized biochemical producers, and branded supplement suppliers operating across global and regional scales.

Sioux Pharm: A U.S.-based pharmaceutical manufacturer with established capabilities in chondroitin sulfate API production, supplying bulk material to branded nutraceutical and pharmaceutical formulators across North America and Europe. The company maintains strong quality certifications aligned with USP and EP monograph standards.

Yantai Ruikangda Biochemical Products: A leading Chinese producer of chondroitin sulfate derived from bovine and porcine sources, benefiting from vertically integrated raw material access and cost-competitive manufacturing infrastructure. The company is a significant exporter to the European and North American markets.

Synutra Ingredients: Operates as a supplier of specialty nutritional ingredients including chondroitin sulfate, with a focus on pharmaceutical-grade purity levels suitable for both human and veterinary applications. The company has invested in expanding its extraction and purification capabilities.

S.A.U. Seikagaku Corporation: A Japanese biopharmaceutical company recognized as a global authority in glycosaminoglycan science. Seikagaku's chondroitin sulfate products are deployed in pharmaceutical formulations in addition to research applications, and the company holds a strong intellectual property portfolio in glycosaminoglycan derivatives.

Summit Nutritionals International: A U.S.-based supplier specializing in joint health ingredients, with chondroitin sulfate positioned as a flagship offering within its portfolio. The company serves contract manufacturers and branded supplement companies through reliable supply chain management.

Bioiberica: A Spanish biotechnology company with a global footprint, recognized for its high-purity BCHS chondroitin sulfate derived from bovine sources. Bioiberica maintains significant investment in clinical research supporting the evidence base for its ingredients across human and animal health applications.

Shandong Runxin Biotechnology: A Chinese biochemical manufacturer focusing on large-volume production of chondroitin sulfate and related glycosaminoglycans, serving both domestic and export markets with competitive pricing on pharmaceutical and food-grade material.

TSI Group: A vertically integrated U.S. company with proprietary branded chondroitin sulfate ingredients marketed under recognized trade names, combining API supply capabilities with branded ingredient marketing to finished goods manufacturers.

Pacific Rainbow International: A supplier and distributor of specialty nutritional ingredients including chondroitin sulfate, with a focus on serving the North American nutraceutical industry through customized sourcing and quality assurance services.

January 2025: Bioiberica announced the expansion of its clinical evidence program for BCHS chondroitin sulfate in veterinary applications, initiating a multi-center canine osteoarthritis trial across veterinary clinics in Spain and the United States to support label claims in regulated markets.

March 2025: Seikagaku Corporation published peer-reviewed findings in a leading rheumatology journal demonstrating the cartilage-protective mechanisms of pharmaceutical-grade chondroitin sulfate in a Phase II clinical setting, reinforcing the compound's regulatory standing in European pharmaceutical classifications.

May 2025: TSI Group launched a new branded chondroitin sulfate product targeting the sports recovery segment, formulated for inclusion in post-exercise functional beverages, reflecting the expanding application scope beyond traditional joint health positioning.

July 2025: Shandong Runxin Biotechnology received updated EU GMP certification for its chondroitin sulfate manufacturing facility, enabling expanded exports to European pharmaceutical customers previously constrained by regulatory documentation requirements.

September 2025: Yantai Ruikangda Biochemical Products announced a capacity expansion investment of approximately $15 million in upgraded extraction and purification infrastructure to meet rising global demand and reduce batch-to-batch variability.

November 2025: Summit Nutritionals International entered a long-term supply agreement with a major North American contract manufacturer to provide pharmaceutical-grade chondroitin sulfate for a new branded arthritis support product line planned for launch in Q1 2026.

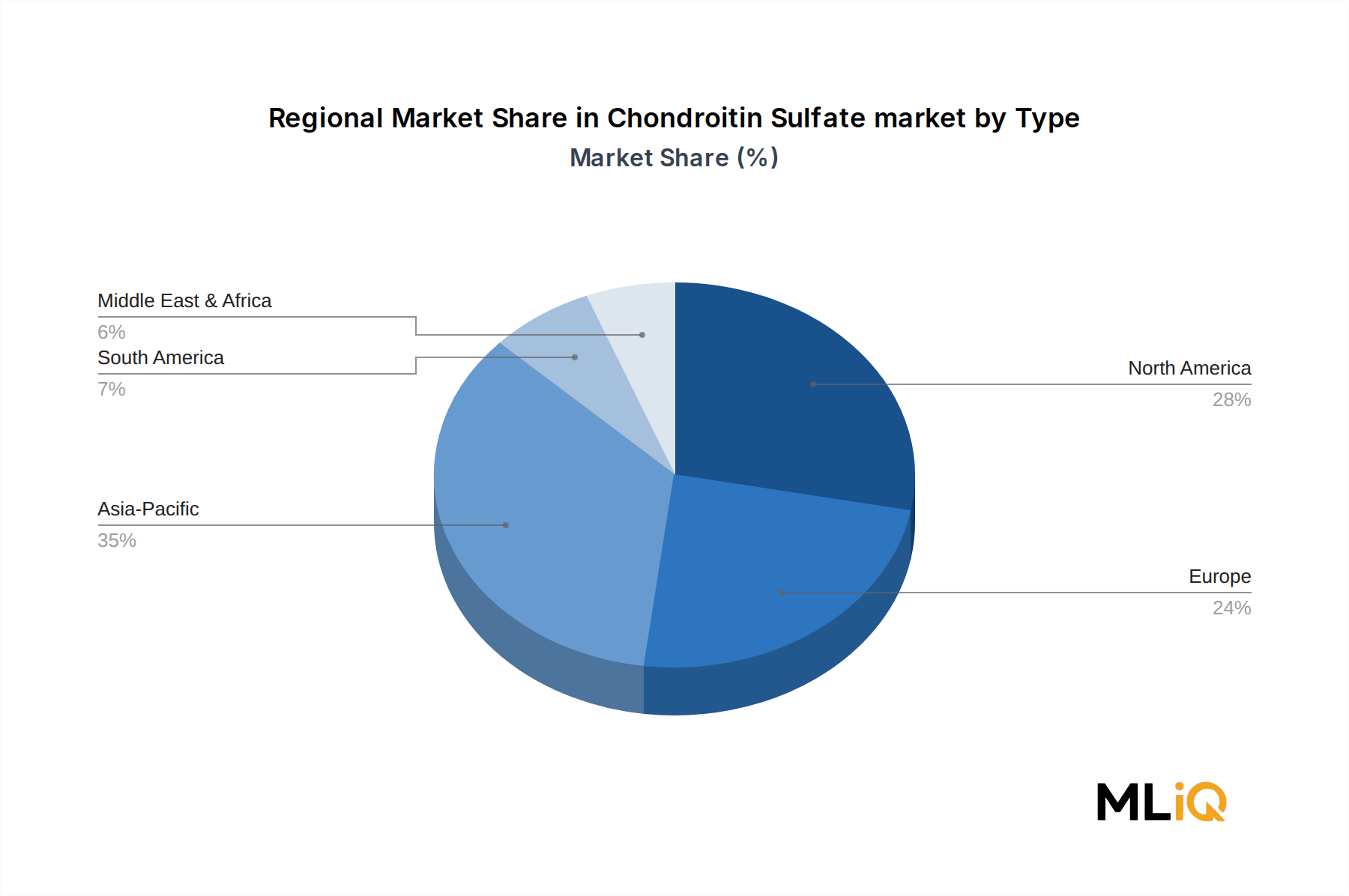

The Chondroitin Sulfate market by Type exhibits distinct regional growth dynamics, with mature markets in North America and Europe contrasting with high-growth trajectories in Asia Pacific and emerging momentum in South America.

North America accounts for the largest regional revenue share, estimated at approximately 35% of global market value in 2025, equivalent to approximately $455 million. The United States is the primary contributor, driven by a large and well-established dietary supplement industry, high consumer awareness of osteoarthritis management, and a robust e-commerce distribution infrastructure. Regional CAGR is estimated at 3.2%, reflecting market maturity and moderate saturation in core consumer demographics. Canada and Mexico contribute incrementally, with Mexico showing greater growth potential tied to expanding middle-class health expenditure.

Europe is the second-largest regional market, accounting for approximately 28% of global revenue. The pharmaceutical classification of chondroitin sulfate in key markets such as Germany, France, Italy, and Spain elevates the average selling price and supports strong revenue generation despite volume constraints relative to the supplement channel. Regional CAGR is estimated at 3.5%. The United Kingdom, following regulatory divergence post-Brexit, presents a distinct regulatory environment that has facilitated some product reclassification and market access adjustments.

Asia Pacific is the fastest-growing region, with an estimated CAGR of 5.1% through the forecast horizon. China is both the largest producer and a rapidly expanding consumer market, driven by urbanization, rising healthcare spending, and government initiatives promoting traditional and integrative medicine. Japan maintains a mature pharmaceutical-grade chondroitin sulfate market, while India, South Korea, and ASEAN nations represent high-potential emerging consumer bases. The region benefits from proximity to raw material supply chains and lower cost manufacturing.

South America is an emerging market, estimated to account for approximately 7% of global revenue in 2025, with Brazil and Argentina as the primary markets. Regional CAGR is estimated at 4.3%, supported by growing awareness of joint health supplements and expanding pharmacy retail networks. Regulatory frameworks in Brazil, governed by ANVISA, are evolving to provide clearer pathways for nutraceutical and pharmaceutical chondroitin sulfate products.

Middle East and Africa represent the smallest regional share at approximately 5%, with Turkey, GCC nations, and South Africa as the most active markets. Regional CAGR is estimated at 3.9%, driven by increasing health consciousness and growing import-dependent supplement retail sectors.

The regulatory environment governing the Chondroitin Sulfate market by Type is notably heterogeneous across geographies, creating both market access complexities and competitive differentiation opportunities for compliant manufacturers.

In the United States, chondroitin sulfate is regulated as a dietary supplement under the Dietary Supplement Health and Education Act (DSHEA) of 1994, administered by the FDA. Manufacturers must comply with Current Good Manufacturing Practices (cGMP) and are restricted from making disease-specific health claims.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 3.8% from 2020-2034 |

| Segmentation |

|

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Comprehensive validation mechanisms ensuring market intelligence accuracy, reliability, and adherence to international standards.

500+ data sources cross-validated

200+ industry specialists validation

NAICS, SIC, ISIC, TRBC standards

Continuous market tracking updates

Factors such as are projected to boost the Chondroitin Sulfate market by Type market expansion.

Key companies in the market include Sioux Pharm, Yantai Ruikangda Biochemical Products, Synutra Ingredients, S.A.U. Seikagaku Corporation, Summit Nutritionals International, Bioiberica., Shandong Runxin Biotechnology, TSI Group, Pacific Rainbow International.

The market segments include Type, Sources, End users.

The market size is estimated to be USD 1.3 billion as of 2022.

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3690, USD 5820, and USD 9870 respectively.

The market size is provided in terms of value, measured in billion and volume, measured in .

Yes, the market keyword associated with the report is "Chondroitin Sulfate market by Type," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Chondroitin Sulfate market by Type, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.