1. What are the major growth drivers for the Autoimmune and Inflammatory Immunomodulators Market market?

Factors such as are projected to boost the Autoimmune and Inflammatory Immunomodulators Market market expansion.

+1 2315155523

Autoimmune and Inflammatory Immunomodulators Market

Autoimmune and Inflammatory Immunomodulators Market

Market Lens IQ is a global market intelligence and strategic consulting firm delivering advanced syndicated research reports, customized industry analysis, competitive intelligence, and data-driven advisory solutions to organizations across international markets. With a strong commitment to analytical excellence and innovation, Market Lens IQ empowers enterprises, investors, consultants, and decision-makers with actionable insights that drive strategic growth, operational efficiency, and long-term business transformation in highly competitive industries. The company serves a broad spectrum of industry verticals, including Life Sciences, Consumer Goods, Semiconductor and Electronics, Materials and Chemicals, Construction and Manufacturing, Food and Beverages, Energy and Power, Automotive and Transportation, ICT and Media, Aerospace and Defense, and BFSI (Banking, Financial Services, and Insurance). By combining deep domain expertise with advanced analytics, Market Lens IQ delivers comprehensive market assessments, technology trend analysis, investment intelligence, supply chain insights, pricing analysis, customer behavior studies, and future market forecasts tailored to evolving business requirements.

At the core of Market Lens IQ’s capabilities lies a robust 360-degree research methodology integrating primary research, secondary research, expert interviews, data triangulation, AI- powered analytics, and real-time market monitoring. Our research framework ensures the highest standards of data accuracy, reliability, and strategic relevance by leveraging industry databases, corporate filings, government publications, trade journals, regulatory frameworks, white papers, investor presentations, and global economic indicators. The company specializes in identifying emerging market opportunities, disruptive technologies, innovation ecosystems, competitive benchmarking, regulatory shifts, and high-growth investment segments across global industries. Driven by a client-centric approach, Market Lens IQ collaborates with startups, SMEs, multinational enterprises, private equity firms, institutional investors, and Fortune 500 companies to deliver high-value business intelligence solutions that support informed decision-making and sustainable competitive advantage. Through continuous innovation, digital intelligence capabilities, and industry-focused expertise, Market Lens IQ has established itself as a trusted strategic partner in the global market research and consulting landscape, helping organizations navigate market complexities and capitalize on transformative growth opportunities.

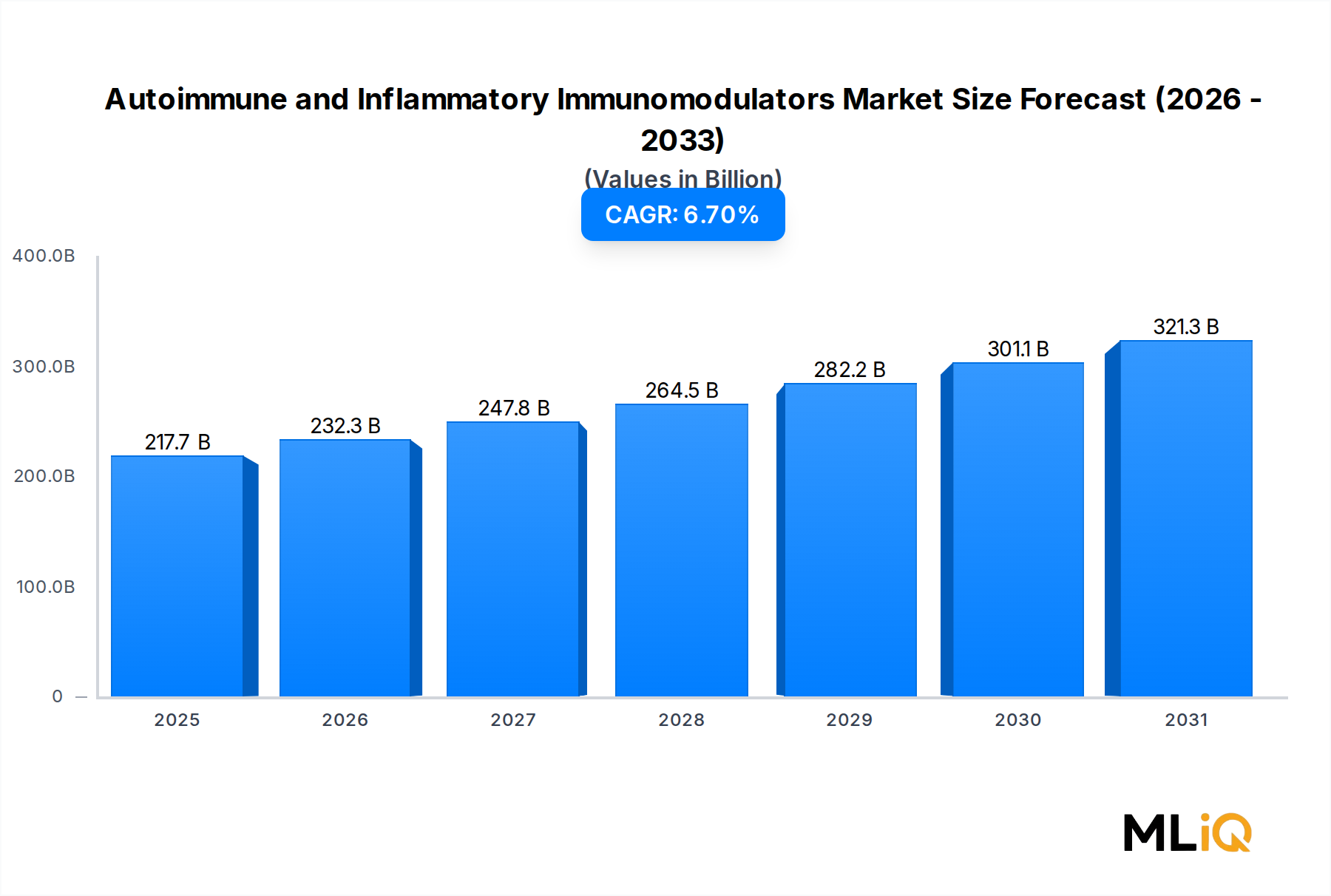

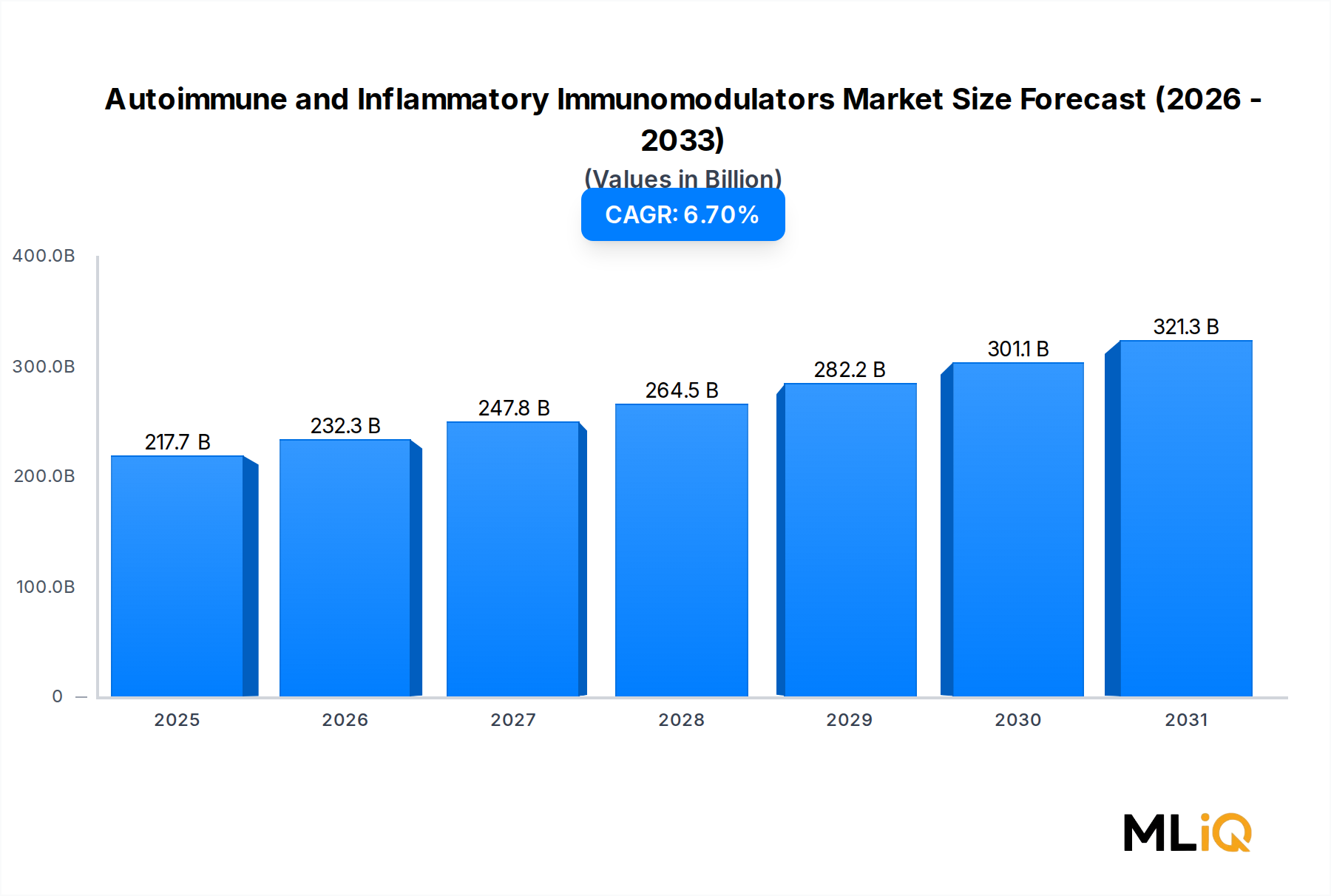

The global Autoimmune and Inflammatory Immunomodulators Market was valued at $217.7 billion in 2023 and is projected to expand at a compound annual growth rate (CAGR) of 6.7% through 2033, positioning this space as one of the most consequential segments in modern pharmaceutical and biotechnology development. By 2033, the market is expected to surpass $420 billion, driven by a confluence of rising autoimmune disease prevalence, accelerating biologics innovation, and broadening therapeutic indications across oncology, respiratory disease, HIV, and rheumatoid arthritis.

The epidemiological burden underpinning this market is substantial. Globally, autoimmune and inflammatory disorders affect an estimated 4–8% of the world's population, with conditions such as rheumatoid arthritis, lupus, multiple sclerosis, inflammatory bowel disease, and psoriasis accounting for the majority of immunomodulator prescriptions. Aging demographics in North America, Europe, and Asia Pacific are further amplifying the patient pool, with the World Health Organization projecting a 23% increase in chronic inflammatory disease diagnoses between 2023 and 2035.

Macro tailwinds are reinforcing demand across multiple dimensions. The expansion of biologic pipelines — particularly monoclonal antibodies, interleukin inhibitors, and JAK inhibitors — is reshaping treatment paradigms and improving clinical outcomes. Simultaneously, the entry of biosimilars into key segments is democratizing access to high-cost therapies and intensifying competitive pressure on originator manufacturers.

Investment activity in this space is accelerating. Global pharmaceutical R&D spending directed at immune-mediated diseases exceeded $38 billion in 2023, with immunomodulation representing the single largest therapeutic category by R&D allocation. Strategic mergers, licensing agreements, and co-development partnerships are reshaping competitive dynamics, with large-cap players such as AstraZeneca, Pfizer, and Novartis actively expanding their immunology portfolios through bolt-on acquisitions.

Geographically, North America retains the largest revenue share, supported by high per-capita healthcare spending, rapid regulatory approvals, and robust reimbursement infrastructure. Asia Pacific, however, is the fastest-growing region, fueled by healthcare modernization programs, rising diagnostic rates, and government-backed pharmaceutical manufacturing initiatives in China and India.

Looking forward, the integration of precision medicine, biomarker-guided therapy selection, and next-generation delivery platforms is expected to structurally elevate efficacy benchmarks and expand addressable patient populations. The Autoimmune and Inflammatory Immunomodulators Market is therefore positioned not merely as a growth story but as a fundamental pillar of the evolving global healthcare economy.

Within the Autoimmune and Inflammatory Immunomodulators Market, the biologics segment commands the largest revenue share, accounting for approximately 58–62% of total market value as of 2023. This dominance reflects a structural shift that has been underway since the early 2000s, when the approval of TNF-alpha inhibitors such as adalimumab and etanercept fundamentally altered the standard of care for conditions like rheumatoid arthritis and Crohn's disease.

Biologics — which encompass monoclonal antibodies, fusion proteins, cytokine inhibitors, interleukin blockers, and recombinant proteins — offer a level of mechanistic specificity that conventional small molecule therapies cannot replicate. By targeting discrete immune pathways rather than broadly suppressing immune function, biologics reduce systemic side effect profiles while delivering superior disease control in moderate-to-severe patient populations. This therapeutic precision is particularly valued in rheumatoid arthritis, psoriatic arthritis, ankylosing spondylitis, and inflammatory bowel disease, where biologic therapies have become the standard second- or third-line treatment option.

The revenue concentration within biologics is further reinforced by pricing dynamics. Biologic therapies command significantly higher price points than small molecules — average annual treatment costs for approved biologics in the United States range from $15,000 to over $60,000 per patient — translating into outsized revenue contribution even at equivalent unit volumes. These economics have historically insulated originator manufacturers from generic competition, though the biosimilars wave is beginning to erode this advantage in certain segments.

Key players driving biologics revenue within the Autoimmune and Inflammatory Immunomodulators Market include AbbVie (via adalimumab/Humira and upadacitinib), Janssen Biotech, Amgen, UCB, and Roche. Among the companies specifically profiled in this report, AstraZeneca has materially expanded its biologics immunology portfolio through the acquisition of Alexion and the development of monoclonal antibodies targeting complement pathways. Novartis maintains a strong position through secukinumab (Cosentyx), an IL-17A inhibitor that has captured significant market share in psoriasis and ankylosing spondylitis. Pfizer's biologics immunology pipeline includes several late-stage candidates targeting IL-23 and JAK signaling pathways.

The biologics segment's share is not merely holding steady — it is expanding. Several structural factors underpin this trajectory. First, regulatory agencies globally are approving biologics at an accelerating pace, with the U.S. FDA approving a record number of biologic license applications (BLAs) in immunology between 2021 and 2023. Second, indication expansion strategies — where approved biologics are evaluated for additional autoimmune conditions — are extending product lifecycles and broadening revenue bases. Third, subcutaneous formulation development is improving patient adherence and supporting premium pricing relative to intravenous alternatives.

The competitive dynamics within biologics are intensifying as biosimilar penetration grows. By 2023, over 40 biosimilar versions of key biologics had received regulatory approval in the United States and European Union, and payer pressure is increasingly directing formulary decisions toward lower-cost biosimilar options. Despite this, originator manufacturers are defending share through next-generation product launches, patient support programs, and contracting strategies.

The Biologics Market, as a standalone research category, intersects directly with immunomodulator development, and growth in biosimilar-enabled access is expected to expand the addressable patient population rather than simply substitute revenue. This dynamic suggests that biologics will remain the dominant and fastest-growing sub-segment of the Autoimmune and Inflammatory Immunomodulators Market through 2033.

Several high-magnitude forces are structuring the trajectory of the Autoimmune and Inflammatory Immunomodulators Market, spanning demand acceleration, pipeline innovation, pricing headwinds, and access barriers.

On the demand side, the primary driver is the escalating global burden of autoimmune and inflammatory disease. The Global Burden of Disease Study estimates that rheumatoid arthritis alone affects over 18 million people globally, with incidence rates rising at approximately 3% annually in developed markets. Inflammatory bowel disease affects an estimated 6.8 million people worldwide, with prevalence growing particularly rapidly in newly industrialized nations across Asia and Latin America. These epidemiological trends generate a structural, non-cyclical demand base that insulates the market from macroeconomic downturns.

R&D productivity is a second major driver. The pipeline for immunomodulatory therapies is among the most active in all of pharmaceutical development. As of 2023, there were over 500 clinical-stage immunomodulator candidates in development globally, spanning Phase I through Phase III. Approximately 35% of these candidates target novel mechanisms of action not addressed by currently approved therapies, suggesting meaningful near-term expansion of the addressable market.

On the constraint side, pricing pressure and reimbursement restriction represent the most significant near-term headwind. Legislative action in the United States — specifically the Inflation Reduction Act's drug price negotiation provisions — is expected to reduce net revenues for select high-volume immunomodulators by 10–25% over the next decade. Similar value-based pricing reforms in the UK, Germany, and France are compressing manufacturer margins in European markets.

Manufacturing complexity and cost represent a structural constraint unique to biologics-heavy segments. Biologic immunomodulators require sophisticated cell culture, purification, and cold-chain infrastructure that limits production scalability and creates supply chain vulnerabilities. These barriers have contributed to periodic drug shortages and elevated the strategic importance of the Pharmaceutical Contract Manufacturing Market as an outsourcing solution for mid-tier manufacturers.

The Rheumatoid Arthritis Treatment Market, as a primary application segment, is also facing a transition dynamic where early adoption of biologic therapies is reaching saturation in high-income markets, shifting incremental growth opportunities to emerging markets and biosimilar-driven access expansion.

The competitive landscape of the Autoimmune and Inflammatory Immunomodulators Market is characterized by the coexistence of large multinational pharmaceutical corporations, specialized biotechnology firms, and emerging generics and biosimilar manufacturers. The following profiles capture the strategic positioning of key participants:

Abbott Laboratories: A diversified healthcare conglomerate with a historically significant immunology franchise through its former pharmaceutical division, now AbbVie; Abbott retains diagnostics capabilities that support immunomodulator patient monitoring ecosystems.

Concord Biotech: An India-based specialty pharmaceutical company focused on fermentation-derived biologics and immunosuppressants, leveraging cost-efficient manufacturing to serve both domestic and export markets in immunology.

SUN Pharma: One of India's largest pharmaceutical manufacturers, SUN Pharma has expanded its specialty portfolio to include biologics and branded generics targeting autoimmune conditions, with a growing presence in North American and European specialty markets.

GlaxoSmithKline Plc.: A global pharmaceutical leader with active immunology programs, including belimumab (Benlysta) for systemic lupus erythematosus, representing one of the few approved therapies specifically targeting lupus pathophysiology.

AstraZeneca: A top-tier innovator in complement biology and inflammatory disease, AstraZeneca's acquisition of Alexion brought transformative biologic assets including ravulizumab and eculizumab, and its respiratory immunology pipeline features dupilumab-adjacent candidates.

Novartis Global: A dominant force in IL-17 and IL-23 inhibition with secukinumab (Cosentyx) and iscalimab in development; Novartis also leads in gene therapy research that may intersect with autoimmune disease correction in the longer term.

Pfizer Inc.: A broad-based pharmaceutical powerhouse with JAK inhibitor tofacitinib (Xeljanz) approved across multiple autoimmune indications and an active biologics pipeline targeting IL-23, OX40L, and TL1A pathways.

Avaxia Biologics: A clinical-stage biotechnology company specializing in orally delivered antibody therapies targeting gastrointestinal inflammatory conditions, offering a differentiated delivery approach relative to injectable biologics.

Merck & Co. Inc.: A global innovator with immunology programs extending beyond its flagship oncology PD-1 franchise to include autoimmune applications; Merck's pipeline includes investigational therapies for inflammatory skin and bowel conditions.

Aurobindo Pharma Ltd.: A major Indian generics and biosimilars manufacturer with an expanding biologics portfolio aimed at making immunomodulator therapies accessible in price-sensitive markets across Asia, Africa, and Latin America.

January 2024: The U.S. FDA granted approval for a next-generation subcutaneous IL-23 inhibitor targeting moderate-to-severe plaque psoriasis, expanding the addressable patient population for biologic immunomodulators in dermatology.

March 2024: The European Medicines Agency (EMA) completed a positive opinion for a biosimilar version of a major TNF-alpha inhibitor, marking the entry of lower-cost competition in the EU's rheumatoid arthritis biologics segment.

May 2024: Novartis Global announced positive Phase III data for a novel IL-17 receptor inhibitor in axial spondyloarthritis, reinforcing its pipeline depth in the musculoskeletal immunology space.

July 2024: AstraZeneca disclosed an expanded co-development agreement with a clinical-stage biotechnology firm targeting type I interferon pathways in systemic lupus erythematosus and dermatomyositis.

September 2024: Pfizer Inc. reported Phase II efficacy results for its TL1A monoclonal antibody candidate in Crohn's disease, supporting the growing importance of gut-specific immunomodulation as a distinct therapeutic frontier.

November 2024: The Indian pharmaceutical regulatory authority (CDSCO) granted approval for Aurobindo Pharma Ltd.'s biosimilar adalimumab, enabling domestic access at approximately 60% lower cost than originator pricing.

February 2025: Merck & Co. Inc. entered into a licensing agreement valued at $1.4 billion to acquire rights to a pre-clinical autoimmune bispecific antibody platform targeting simultaneous IL-6 and IL-17 neutralization.

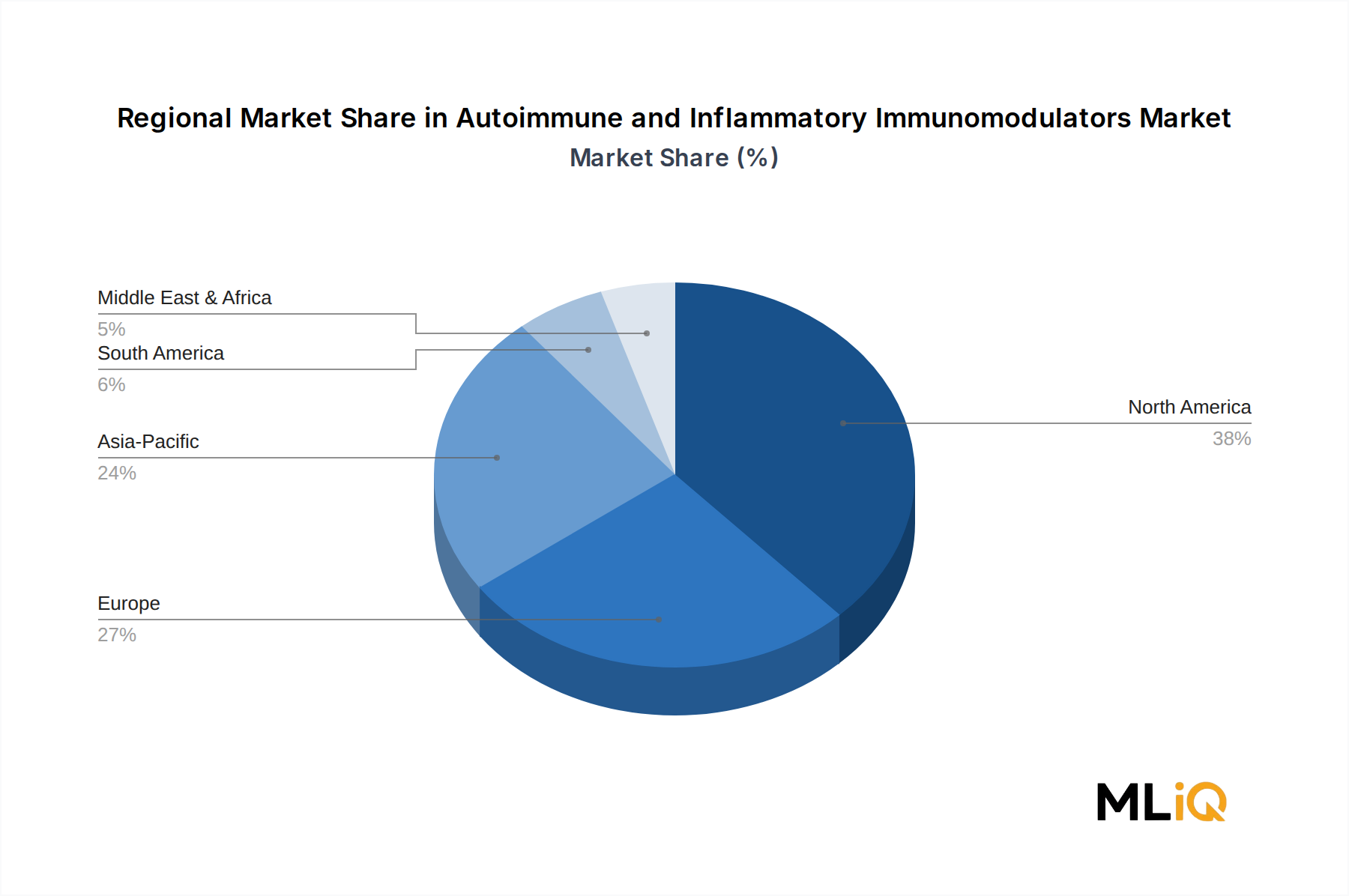

Geographic analysis of the Autoimmune and Inflammatory Immunomodulators Market reveals pronounced regional variation in market maturity, growth velocity, and dominant demand drivers.

North America remains the largest regional market, accounting for approximately 42–45% of global revenue in 2023, equivalent to roughly $92–98 billion. The United States is the primary contributor, supported by the world's highest per-capita pharmaceutical expenditure (exceeding $1,400 annually), a favorable biologics reimbursement environment, and a dense network of academic medical centers generating clinical adoption. Canada and Mexico contribute incrementally, with Canada's provincial formulary systems enabling increasing biosimilar substitution. The regional CAGR for North America is estimated at 5.8% through 2033, reflecting moderate growth constrained by pricing reform and market saturation in first-line biologic categories.

Europe represents the second-largest region, capturing approximately 28–31% of global revenue. Germany, France, the UK, Italy, and Spain collectively drive the majority of European demand. The region's growth is moderated by stringent health technology assessment (HTA) frameworks — particularly Germany's AMNOG system and NICE in the UK — which compress manufacturer pricing power. However, biosimilar adoption in Europe is among the highest globally, driving volume growth even as unit prices decline. European regional CAGR is estimated at 5.2%, with the Nordics and Benelux emerging as innovation hotspots.

Asia Pacific is the fastest-growing region, with an estimated regional CAGR of 9.1% through 2033. China and India are the primary growth engines, driven by rising diagnostic penetration, expanding middle-class healthcare access, and substantial government investment in domestic biopharmaceutical manufacturing. Japan and South Korea represent more mature Asia Pacific markets with strong regulatory infrastructure supporting biologic approvals. The ASEAN cluster is an emerging frontier, with Malaysia, Thailand, and Vietnam increasing specialty pharmaceutical adoption.

The Middle East and Africa region, while representing a smaller absolute revenue base, is growing at approximately 7.4% CAGR, driven by Gulf Cooperation Council (GCC) healthcare expansion programs and increasing diagnosis rates for conditions like ankylosing spondylitis and inflammatory bowel disease. South Africa and Turkey serve as regional pharmaceutical hubs.

South America is growing at an estimated 6.9% CAGR, with Brazil and Argentina as the dominant markets. Access to biologics remains constrained by pricing and reimbursement challenges, though government procurement programs in Brazil are expanding institutional market access for select immunomodulators.

The Autoimmune and Inflammatory Immunomodulators Market is undergoing a technology-

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6.7% from 2020-2034 |

| Segmentation |

|

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Comprehensive validation mechanisms ensuring market intelligence accuracy, reliability, and adherence to international standards.

500+ data sources cross-validated

200+ industry specialists validation

NAICS, SIC, ISIC, TRBC standards

Continuous market tracking updates

Factors such as are projected to boost the Autoimmune and Inflammatory Immunomodulators Market market expansion.

Key companies in the market include Abbott Laboratories, Concord Biotech, SUN Pharma, GlaxoSmithKline Plc., AstraZeneca, Novartis Global, Pfizer Inc., Avaxia Biologics, Merck & Co. Inc., Aurobindo Pharma Ltd..

The market segments include Type, Application.

The market size is estimated to be USD 217.7 billion as of 2022.

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3690, USD 5820, and USD 9870 respectively.

The market size is provided in terms of value, measured in billion and volume, measured in .

Yes, the market keyword associated with the report is "Autoimmune and Inflammatory Immunomodulators Market," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Autoimmune and Inflammatory Immunomodulators Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.