1. What are the major growth drivers for the Pelvic Inflammatory Disease Treatment Market market?

Factors such as are projected to boost the Pelvic Inflammatory Disease Treatment Market market expansion.

Pelvic Inflammatory Disease Treatment Market

Pelvic Inflammatory Disease Treatment Market

Market Lens IQ is a global market intelligence and strategic consulting firm delivering advanced syndicated research reports, customized industry analysis, competitive intelligence, and data-driven advisory solutions to organizations across international markets. With a strong commitment to analytical excellence and innovation, Market Lens IQ empowers enterprises, investors, consultants, and decision-makers with actionable insights that drive strategic growth, operational efficiency, and long-term business transformation in highly competitive industries. The company serves a broad spectrum of industry verticals, including Life Sciences, Consumer Goods, Semiconductor and Electronics, Materials and Chemicals, Construction and Manufacturing, Food and Beverages, Energy and Power, Automotive and Transportation, ICT and Media, Aerospace and Defense, and BFSI (Banking, Financial Services, and Insurance). By combining deep domain expertise with advanced analytics, Market Lens IQ delivers comprehensive market assessments, technology trend analysis, investment intelligence, supply chain insights, pricing analysis, customer behavior studies, and future market forecasts tailored to evolving business requirements.

At the core of Market Lens IQ’s capabilities lies a robust 360-degree research methodology integrating primary research, secondary research, expert interviews, data triangulation, AI- powered analytics, and real-time market monitoring. Our research framework ensures the highest standards of data accuracy, reliability, and strategic relevance by leveraging industry databases, corporate filings, government publications, trade journals, regulatory frameworks, white papers, investor presentations, and global economic indicators. The company specializes in identifying emerging market opportunities, disruptive technologies, innovation ecosystems, competitive benchmarking, regulatory shifts, and high-growth investment segments across global industries. Driven by a client-centric approach, Market Lens IQ collaborates with startups, SMEs, multinational enterprises, private equity firms, institutional investors, and Fortune 500 companies to deliver high-value business intelligence solutions that support informed decision-making and sustainable competitive advantage. Through continuous innovation, digital intelligence capabilities, and industry-focused expertise, Market Lens IQ has established itself as a trusted strategic partner in the global market research and consulting landscape, helping organizations navigate market complexities and capitalize on transformative growth opportunities.

+1 2315155523

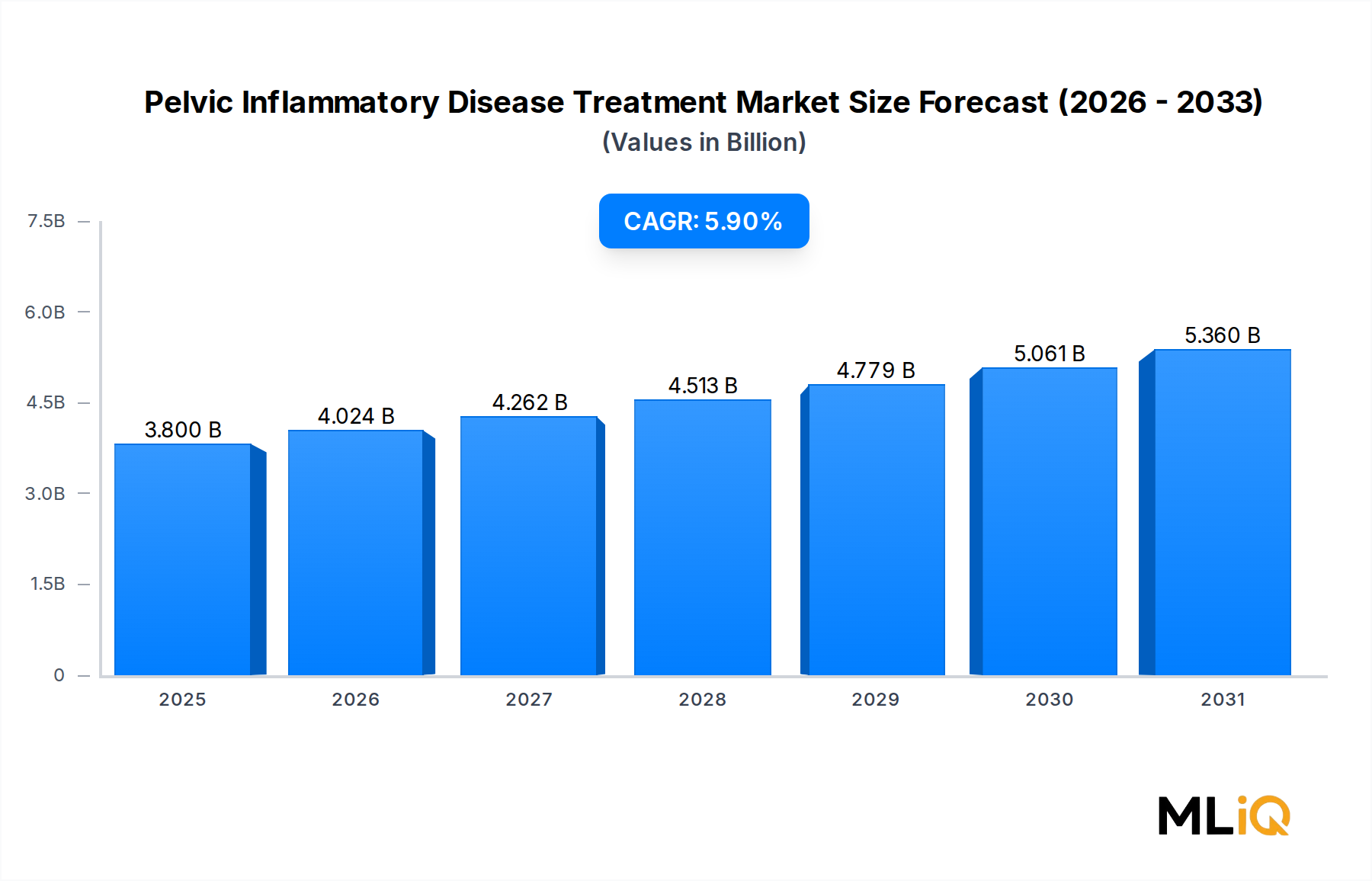

The global Pelvic Inflammatory Disease Treatment Market is valued at $3.8 billion in 2025 and is projected to expand at a compound annual growth rate (CAGR) of 5.9% through 2033, reaching an estimated $6.0 billion by the end of the forecast period. This sustained trajectory is underpinned by a convergence of epidemiological, therapeutic, and healthcare infrastructure factors that are collectively reshaping the treatment paradigm for pelvic inflammatory disease (PID).

PID, a polymicrobial infection of the upper female reproductive tract, remains one of the most consequential gynecological conditions globally, with sequelae including chronic pelvic pain, ectopic pregnancy, and infertility. The rising global incidence of sexually transmitted infections (STIs), particularly chlamydia and gonorrhea, which serve as primary etiological agents, continues to expand the addressable patient population. According to the World Health Organization, more than 374 million new STI cases are recorded annually across four major pathogens, sustaining a robust upstream demand signal for PID therapeutics.

Macro tailwinds reinforcing market growth include expanding access to healthcare in emerging economies, heightened public health awareness campaigns targeting reproductive health, increasing government-funded STI screening programs, and ongoing investments in antibiotic pipeline development. The proliferation of outpatient specialty centers and evolving clinical guidelines that support oral over parenteral therapy for mild-to-moderate PID cases are also reshaping prescribing patterns and distribution dynamics.

The market benefits from a well-established drug landscape dominated by combination antibiotic regimens including macrolides, tetracyclines, beta-lactams, and nitroimidazoles. Generic penetration remains high, creating a dual-track market where innovators focus on novel delivery mechanisms and resistance-overcoming formulations, while generic manufacturers compete aggressively on price and volume.

Regionally, North America and Europe account for the majority of current revenue share, supported by robust diagnostic infrastructure, high awareness, and favorable reimbursement frameworks. However, Asia Pacific is emerging as the fastest-growing regional market, driven by rising STI incidence, urbanization, and expanding healthcare access in China, India, and ASEAN nations.

Looking ahead to 2033, the market outlook remains constructive. Key opportunities include the development of novel antibiotic classes targeting resistant organisms, digital health integration for improved patient adherence, and expanded public-private partnerships in low-to-middle-income countries. The Pelvic Inflammatory Disease Treatment Market is poised for durable, mid-single-digit growth as clinical, demographic, and policy tailwinds remain broadly favorable.

Among all segmentation dimensions analyzed, the drug class segment constitutes the primary revenue-generating axis of the Pelvic Inflammatory Disease Treatment Market. Within drug classes, the macrolides sub-segment holds the dominant position by revenue share, a trend expected to persist and modestly consolidate through 2033.

Macrolides, particularly azithromycin, are embedded within first-line treatment guidelines issued by the U.S. Centers for Disease Control and Prevention (CDC), the European Centre for Disease Prevention and Control (ECDC), and the World Health Organization. The CDC's 2021 STI Treatment Guidelines explicitly recommend a regimen combining ceftriaxone with doxycycline (a tetracycline) and metronidazole (a nitroimidazole) for inpatient cases, while azithromycin-based regimens remain widely used in outpatient settings. This guideline-entrenched status provides macrolides with a structural demand floor that competitors cannot easily erode.

The macrolides segment's dominance is reinforced by several pharmacological and commercial attributes. Azithromycin's extended tissue half-life, favorable safety profile, once-daily dosing convenience, and broad antimicrobial spectrum make it particularly well-suited for PID management across acute and subacute presentations. These characteristics translate directly into strong prescriber preference and patient adherence rates, which are critical metrics in STI-associated infection management.

From a competitive standpoint, the macrolides sub-segment is served by a mix of originator pharmaceutical companies and a highly active generic manufacturing ecosystem. Pfizer Inc. retains significant brand recognition through its original azithromycin franchise (Zithromax), while generic manufacturers including Teva Pharmaceutical Industries Ltd and Mylan N.V. (now part of Viatris) have captured substantial volume share through aggressive pricing strategies. This bifurcated competitive structure means that while branded revenue per unit is under pressure, total macrolide volume dispensed continues to grow, sustaining overall segment revenue.

The Antibiotic Drugs Market, of which macrolides form a critical pillar, is itself experiencing structural shifts due to antimicrobial resistance (AMR) concerns. Increasing Neisseria gonorrhoeae resistance to azithromycin has been documented in multiple surveillance studies, prompting regulatory agencies and clinical bodies to revisit monotherapy recommendations. This AMR dynamic is a dual-edged factor: it creates short-term prescription substitution pressures but simultaneously drives R&D investment into next-generation macrolide derivatives and combination strategies, supporting longer-term segment innovation.

The tetracyclines sub-segment, primarily represented by doxycycline, occupies a strong secondary position. Doxycycline's continued inclusion in CDC and ECDC combination regimens for PID ensures persistent demand. The beta-lactam sub-segment, anchored by ceftriaxone for parenteral treatment of severe PID cases, is particularly important in the hospital and specialty center end-user segments. Nitroimidazoles (metronidazole, tinidazole) complete the standard-of-care combination and maintain stable demand driven by guideline adherence.

By route of administration, the oral segment leads the market in volume terms, reflecting a global clinical trend toward outpatient management of mild-to-moderate PID. The parenteral segment, while smaller in volume, commands higher per-unit pricing and is concentrated in hospital settings, contributing disproportionately to revenue relative to its volume share. The Parenteral Drug Delivery Market is a relevant adjacent space, as innovations in injectable drug formulation and delivery devices influence how parenteral PID therapies are administered and monitored.

Overall, the dominance of the macrolides drug class segment is structural rather than cyclical. Its position is protected by clinical guideline endorsement, broad generic availability ensuring affordability, and the continued centrality of azithromycin in outpatient PID treatment protocols worldwide. The segment's share is expected to remain stable or consolidate slightly as AMR-driven regimen evolution proceeds.

The Pelvic Inflammatory Disease Treatment Market is propelled by a set of quantifiable drivers while simultaneously facing defined structural constraints that market participants must navigate.

Driver 1: Rising STI Incidence as a Primary Demand Catalyst The WHO estimates that 376 million STI infections occur annually, with chlamydia accounting for 127 million cases and gonorrhea for 87 million. Since chlamydia and gonorrhea together account for approximately 50% of PID etiology, this upstream epidemiological burden directly translates into a sustained and growing treatment-seeking population. The CDC reports that roughly 1 million women in the United States experience a new PID episode each year, underscoring the scale of domestic demand alone.

Driver 2: Expanding Healthcare Infrastructure in Emerging Markets Asia Pacific healthcare expenditure has grown at a pace exceeding 7% annually over the past five years across key markets including India and ASEAN nations. Increased hospital bed capacity, rising insurance penetration, and government-funded reproductive health programs in these geographies are expanding the diagnosed and treated PID patient pool, directly inflating market volume and revenue.

Driver 3: Generic Drug Accessibility Improving Treatment Rates Generic versions of key PID therapeutics account for over 80% of global prescription volumes for this indication. The maturity of the Generic Pharmaceuticals Market has substantially lowered the cost barrier for PID treatment in low-to-middle-income countries, converting previously untreated or undertreated cases into active therapy episodes.

Constraint 1: Antimicrobial Resistance Reducing First-Line Efficacy Documented azithromycin resistance in Neisseria gonorrhoeae exceeds 5% in several European surveillance cohorts and has crossed 10% in certain urban U.S. populations. This erosion of first-line efficacy is forcing clinicians toward more complex, often parenteral combination regimens that reduce outpatient treatment feasibility and increase per-episode cost.

Constraint 2: Underdiagnosis and Diagnostic Gaps An estimated 85% of PID cases globally are asymptomatic or minimally symptomatic at presentation, resulting in chronic underdiagnosis. Limited access to the Women's Health Diagnostics Market infrastructure in lower-income geographies suppresses the addressable treated market, representing a structural ceiling on volume growth in these regions.

The competitive landscape of the Pelvic Inflammatory Disease Treatment Market is characterized by a mix of large diversified pharmaceutical conglomerates, specialty pharma players, and an active generic manufacturing tier. The following profiles outline the strategic positioning of leading participants:

Bristol Myers Squibb Company: A major diversified biopharmaceutical firm with a broad anti-infective and specialty care portfolio; its distribution network and established relationships with hospital pharmacy systems position it competitively in the PID treatment space.

Johnson and Johnson Services Inc: Through its Janssen Pharmaceuticals subsidiary, Johnson and Johnson maintains a presence in infectious disease therapeutics with a focus on combination therapy innovation and global market access programs targeting gynecological infections.

Teva Pharmaceutical Industries Ltd: One of the world's largest generic drug manufacturers, Teva is a dominant supplier of generic azithromycin, doxycycline, and metronidazole, the core agents in PID treatment protocols, leveraging economies of scale and global distribution infrastructure.

F. Hoffmann-La Roche Ltd: Roche's diagnostics division plays an increasingly important role in PID management through molecular diagnostic tools that enable rapid pathogen identification, supporting targeted antibiotic prescribing and reducing empirical therapy reliance.

Pfizer Inc.: As the originator of the azithromycin franchise (Zithromax), Pfizer retains brand equity in the PID treatment space while also competing in the broader Infectious Disease Therapeutics Market through its anti-infective pipeline.

AstraZeneca: AstraZeneca's portfolio contributions to PID treatment are primarily through its broad-spectrum antibiotic assets and its focus on addressing AMR through novel antibiotic development collaborations and public-private partnerships.

Mylan N.V.: As part of Viatris following its merger, Mylan's generic manufacturing capabilities ensure extensive global availability of key PID therapeutics at competitive price points, particularly in emerging markets.

Sanofi: Sanofi contributes to the PID treatment landscape through its established anti-infective product lines and its public health partnerships targeting STI and reproductive health outcomes in sub-Saharan Africa and Southeast Asia.

Merck & Co., Inc.: Merck's anti-infective portfolio and vaccine pipeline (including HPV vaccination programs that reduce downstream gynecological disease burden) position it as a strategically relevant player across the PID disease continuum.

Janssen Pharmaceuticals, Inc.: Operating as a subsidiary of Johnson and Johnson, Janssen focuses on specialty pharmaceuticals and infectious disease, contributing formulation innovation and clinical development resources relevant to PID therapy optimization.

Mayne Pharma Group Limited: A specialty pharmaceutical company with a focus on women's health and dermatology; Mayne Pharma has invested specifically in doxycycline-based formulations relevant to PID treatment, giving it a targeted niche positioning in this market.

January 2024: The CDC released updated interim guidance on gonorrhea treatment protocols, expanding recommendations for dual-therapy regimens in PID management to address rising ceftriaxone resistance signals observed in Pacific Island surveillance data, directly impacting prescribing practices in North America and Oceania.

March 2024: Teva Pharmaceutical Industries Ltd announced expanded manufacturing capacity for doxycycline hyclate tablets at its European production facilities, targeting supply chain resilience following documented shortages of tetracycline-class antibiotics in 2023 that disrupted PID treatment programs in multiple EU member states.

June 2024: The European Medicines Agency (EMA) issued a pharmacovigilance signal assessment related to fluoroquinolone use in gynecological infections, reinforcing restrictions that have redirected clinicians toward macrolide and tetracycline combinations for outpatient PID management.

September 2024: Mayne Pharma Group Limited received FDA approval for a modified-release doxycycline formulation demonstrating improved gastrointestinal tolerability, a clinically significant advancement given that GI adverse effects are a primary driver of non-adherence in oral PID therapy regimens.

November 2024: A landmark multicenter clinical trial published in The Lancet Infectious Diseases confirmed non-inferiority of a 7-day oral azithromycin-plus-metronidazole regimen versus standard 14-day doxycycline-based therapy for mild-to-moderate PID, potentially supporting future guideline revisions that could expand outpatient treatment eligibility.

February 2025: The WHO released its updated Essential Medicines List, retaining all core PID therapeutic agents while adding new annotation guidance on minimum treatment duration and AMR stewardship considerations for antibiotic use in reproductive tract infections.

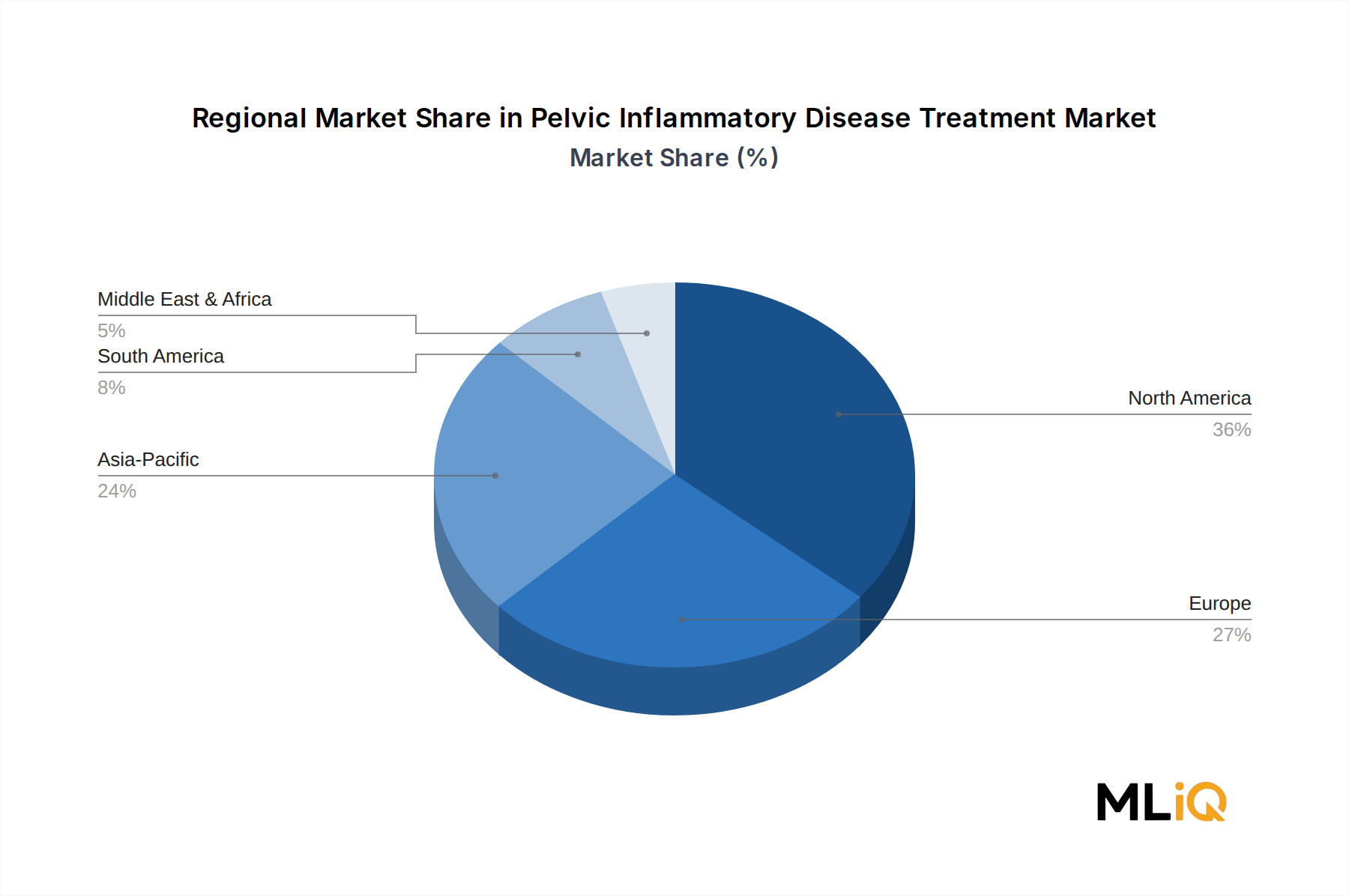

The Pelvic Inflammatory Disease Treatment Market exhibits pronounced regional heterogeneity in terms of revenue contribution, growth velocity, and demand drivers.

North America: North America accounts for approximately 35–38% of global market revenue in 2025, making it the largest individual regional market. The United States drives this dominance, supported by a high diagnostic rate, comprehensive STI surveillance infrastructure, and robust reimbursement frameworks for reproductive health treatments. The U.S. market benefits from strong prescription volumes across both brand and generic segments. The regional CAGR is estimated at 4.8% through 2033, reflecting a relatively mature market profile with incremental growth driven by rising STI incidence and expanded Medicaid coverage for reproductive health services.

Europe: Europe represents the second-largest regional market, contributing roughly 28–30% of global revenue. Germany, the United Kingdom, and France are the primary national markets. Centralized healthcare systems and strong clinical guideline infrastructure ensure consistent treatment rates. The regional CAGR is projected at approximately 4.5%, with growth modestly constrained by stringent AMR stewardship policies that are shifting treatment compositions and reducing some high-volume antibiotic prescriptions.

Asia Pacific: Asia Pacific is the fastest-growing regional market, with a projected CAGR of 8.2% through 2033. China, India, and ASEAN nations are the primary growth engines. Rapid urbanization, increasing STI prevalence, expanding health insurance coverage, and government investments in reproductive health programs are the principal demand catalysts. The Hospital Pharmacy Market in this region is expanding rapidly, improving drug accessibility in previously underserved urban and peri-urban populations. The Gynecological Disorders Treatment Market is a closely adjacent growth sector reinforcing investment in this region.

Latin America: Brazil and Argentina anchor Latin American demand, which contributes approximately 10–12% of global revenue. Regional CAGR is estimated at 6.3%, above the global average, supported by rising public health investment and expanding generic drug availability through government procurement programs. Structural challenges including healthcare access inequality and high rates of undiagnosed PID temper the full realization of growth potential.

Middle East & Africa: This region represents the smallest current revenue share at approximately 8–10% but carries significant long-term growth potential. South Africa, Turkey, and GCC nations are the most developed sub-markets. The Sexually Transmitted Infections Treatment Market in sub-Saharan Africa is particularly underdeveloped relative to disease

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.9% from 2020-2034 |

| Segmentation |

|

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Comprehensive validation mechanisms ensuring market intelligence accuracy, reliability, and adherence to international standards.

500+ data sources cross-validated

200+ industry specialists validation

NAICS, SIC, ISIC, TRBC standards

Continuous market tracking updates

Factors such as are projected to boost the Pelvic Inflammatory Disease Treatment Market market expansion.

Key companies in the market include Bristol Myers Squibb Company, Johnson and Johnson Services Inc, Teva Pharmaceutical Industries Ltd, F. Hoffmann-La Roche Ltd, Pfizer Inc., AstraZeneca, Mylan N.V., Sanofi, Merck & Co., Inc, Janssen Pharmaceuticals, Inc., Mayne Pharma Group Limited.

The market segments include Drug Class, Route of Administration, End User, Distribution Channel.

The market size is estimated to be USD 3.8 billion as of 2022.

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3690, USD 5820, and USD 9870 respectively.

The market size is provided in terms of value, measured in billion and volume, measured in .

Yes, the market keyword associated with the report is "Pelvic Inflammatory Disease Treatment Market," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Pelvic Inflammatory Disease Treatment Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.