1. What are the major growth drivers for the Breast Pumps Market market?

Factors such as are projected to boost the Breast Pumps Market market expansion.

Breast Pumps Market

Breast Pumps Market

Market Lens IQ is a global market intelligence and strategic consulting firm delivering advanced syndicated research reports, customized industry analysis, competitive intelligence, and data-driven advisory solutions to organizations across international markets. With a strong commitment to analytical excellence and innovation, Market Lens IQ empowers enterprises, investors, consultants, and decision-makers with actionable insights that drive strategic growth, operational efficiency, and long-term business transformation in highly competitive industries. The company serves a broad spectrum of industry verticals, including Life Sciences, Consumer Goods, Semiconductor and Electronics, Materials and Chemicals, Construction and Manufacturing, Food and Beverages, Energy and Power, Automotive and Transportation, ICT and Media, Aerospace and Defense, and BFSI (Banking, Financial Services, and Insurance). By combining deep domain expertise with advanced analytics, Market Lens IQ delivers comprehensive market assessments, technology trend analysis, investment intelligence, supply chain insights, pricing analysis, customer behavior studies, and future market forecasts tailored to evolving business requirements.

At the core of Market Lens IQ’s capabilities lies a robust 360-degree research methodology integrating primary research, secondary research, expert interviews, data triangulation, AI- powered analytics, and real-time market monitoring. Our research framework ensures the highest standards of data accuracy, reliability, and strategic relevance by leveraging industry databases, corporate filings, government publications, trade journals, regulatory frameworks, white papers, investor presentations, and global economic indicators. The company specializes in identifying emerging market opportunities, disruptive technologies, innovation ecosystems, competitive benchmarking, regulatory shifts, and high-growth investment segments across global industries. Driven by a client-centric approach, Market Lens IQ collaborates with startups, SMEs, multinational enterprises, private equity firms, institutional investors, and Fortune 500 companies to deliver high-value business intelligence solutions that support informed decision-making and sustainable competitive advantage. Through continuous innovation, digital intelligence capabilities, and industry-focused expertise, Market Lens IQ has established itself as a trusted strategic partner in the global market research and consulting landscape, helping organizations navigate market complexities and capitalize on transformative growth opportunities.

+1 2315155523

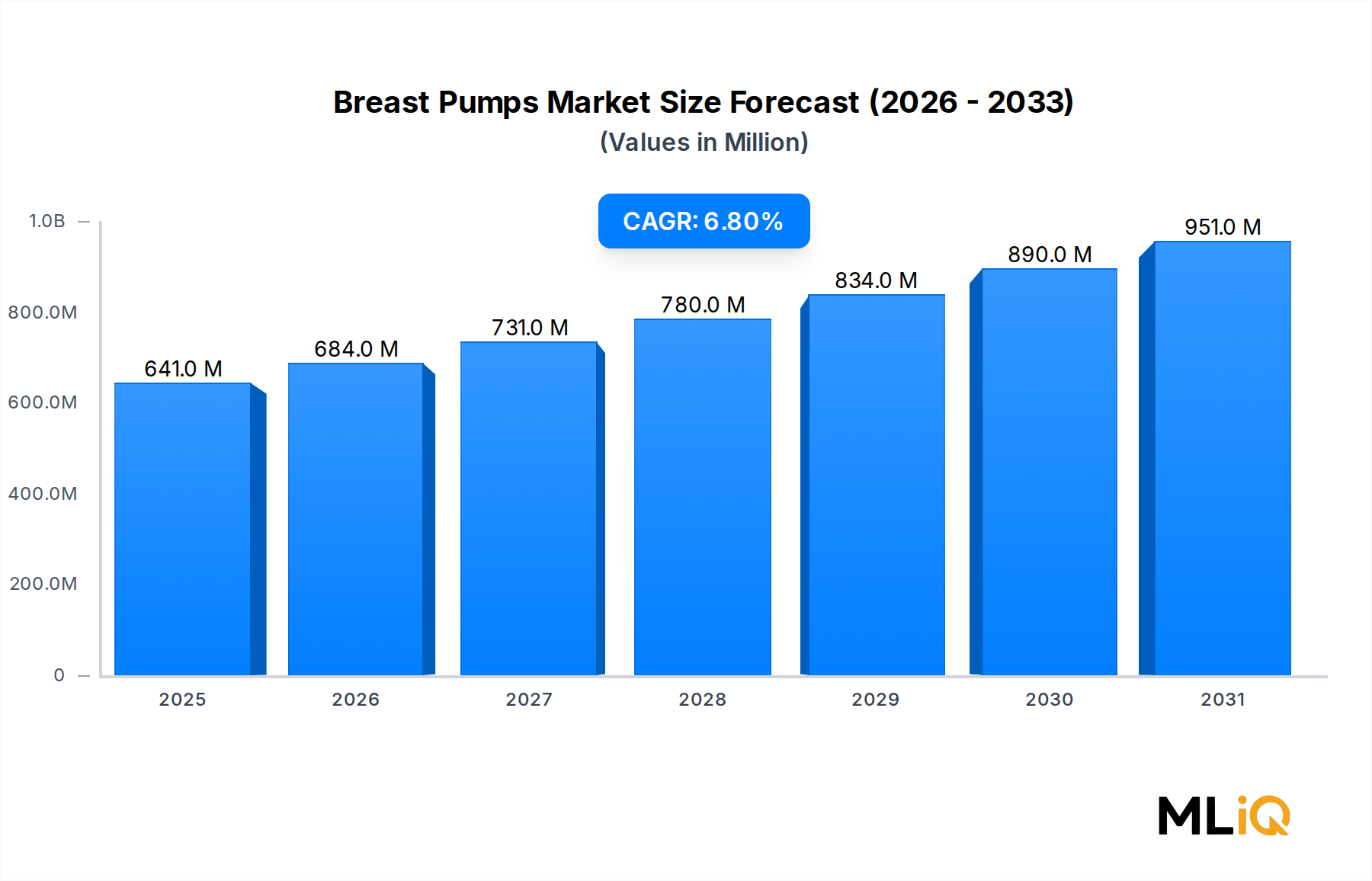

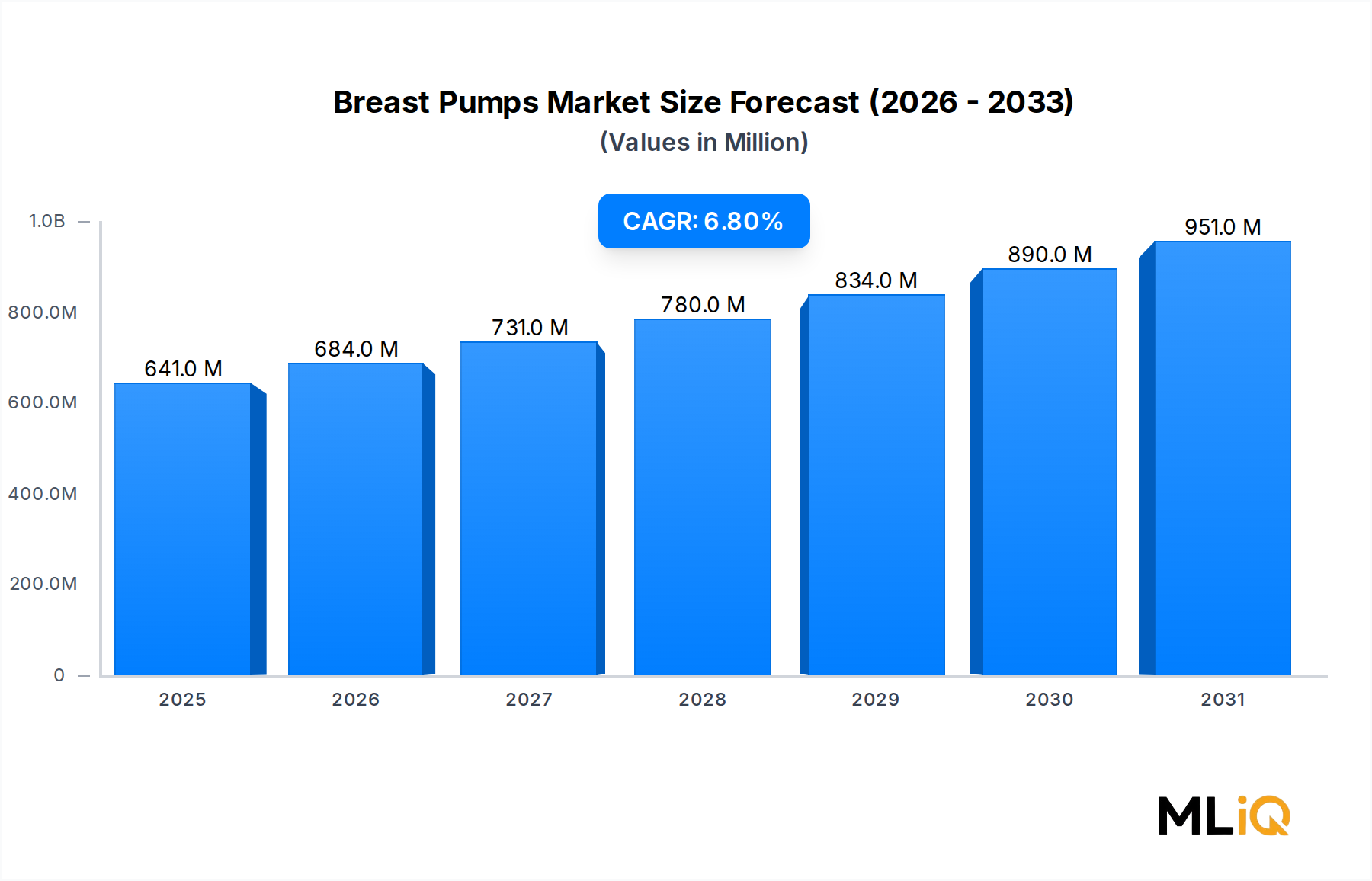

The global breast pumps market is currently valued at $640.70 million and is projected to expand at a compound annual growth rate (CAGR) of 6.8% through the forecast horizon, reflecting robust and sustained demand across developed and emerging economies alike. This growth trajectory positions the market as one of the more resilient sub-segments within maternal and infant healthcare, buoyed by a confluence of demographic, legislative, and technological forces.

At the macro level, rising female labor force participation rates — particularly in North America, Europe, and parts of Asia Pacific — are compelling more new mothers to seek clinically reliable and convenient breastfeeding solutions. According to the International Labour Organization, female employment rates in OECD countries have risen steadily over the past decade, directly correlating with higher adoption of personal-use breast pumps. Concurrently, growing awareness of the nutritional and immunological benefits of breast milk, endorsed by organizations such as the World Health Organization (WHO) and UNICEF, is reinforcing breastfeeding intent even among mothers who return to work shortly after childbirth.

Legislative tailwinds are equally significant. In the United States, the Affordable Care Act mandates insurance coverage for breast pumps, which has dramatically reduced out-of-pocket expenditure barriers and driven unit volumes upward. Similar reimbursement frameworks are gaining traction in European markets, including Germany, France, and the United Kingdom, expanding the addressable market substantially.

On the innovation front, the integration of Bluetooth connectivity, app-based milk volume tracking, and rechargeable battery systems into wearable pump designs is reshaping consumer expectations. The pivot toward hands-free, discreet devices — a category now anchored by companies such as Willow Innovations — is creating premium-tier growth vectors that command meaningfully higher average selling prices and margin profiles.

From a segmentation standpoint, electric breast pumps continue to dominate the revenue mix, outpacing manual alternatives on the strength of convenience, clinical efficacy, and insurance coverage eligibility. Hospital-grade pumps remain a critical volume anchor in institutional settings, particularly neonatal intensive care units (NICUs).

Looking forward, the market is expected to benefit from expanding healthcare infrastructure in Asia Pacific, increasing public health investments in breastfeeding promotion in Sub-Saharan Africa and Latin America, and continuous product miniaturization driven by advances in motor engineering and silicone component technology. These intersecting drivers underpin a forward-looking outlook characterized by steady volume growth, premiumization at the consumer tier, and competitive intensity among global and regional incumbents.

Within the breast pumps market, electric breast pumps represent the single largest revenue-generating segment, accounting for a majority share that continues to consolidate as product innovation accelerates and reimbursement frameworks broaden. The dominance of this segment is rooted in multiple structural advantages that manual alternatives fundamentally cannot replicate at scale.

First and foremost, clinical efficacy differentiates electric pumps decisively. Hospital-grade and consumer-grade electric units are engineered to mimic the natural suckling rhythm of infants through programmable cycle and vacuum settings, which research consistently demonstrates yields higher milk expression volumes per session compared with manual operation. For mothers of premature infants or those experiencing low milk supply, this clinical superiority is not merely a convenience feature — it is a medical necessity, making electric options the default recommendation from lactation consultants and neonatologists globally.

Second, the insurance coverage dynamic in the United States — the single largest national market — structurally advantages electric breast pumps. The Affordable Care Act's preventive services mandate, operationalized through HRSA guidelines, covers the provision of a breast pump, and most insurers fulfill this obligation with electric double pumps. This policy framework has effectively commoditized access to electric units at the consumer level, eliminating price as the primary barrier and shifting competitive dynamics toward brand trust, product features, and post-purchase support.

Third, technological evolution within the electric segment is creating a visible stratification between standard double electric pumps and next-generation wearable, app-connected devices. Companies like Willow Innovations have pioneered in-bra wearable pumps that operate without external tubing or collection bottles, enabling fully hands-free operation. This category commands retail price points between $400 and $600 per unit — a premium of approximately 150% to 200% over traditional double electric models — and is attracting a disproportionate share of venture capital and consumer marketing investment.

Key players dominating the electric pump sub-segment include Medela AG, which maintains the broadest installed base globally on the strength of its clinical heritage and hospital supply relationships; Koninklijke Philips N.V., which competes through its Avent brand with a design-forward, consumer-centric portfolio; and Willow Innovations, which has carved out a high-growth niche in the wearable tier. Ameda and Hygeia Health focus on hospital-grade electric systems, supplying NICUs and maternity wards where pump rental and multi-user configurations are standard.

The Electric Breast Pumps Market is also benefiting from the maturation of lithium-ion battery technology, which has enabled smaller, lighter motor assemblies without sacrificing suction strength. This engineering progress has been pivotal in enabling the wearable segment's growth and will likely continue driving product roadmaps over the next five years.

Market share within the electric segment is consolidating around a small group of global incumbents, but competitive pressure from well-funded direct-to-consumer brands is intensifying, particularly in the United States and United Kingdom. Private label offerings from large retail pharmacy chains are also beginning to capture price-sensitive consumers in the standard electric tier, compressing margins for mid-market brands.

Overall, the electric segment's dominance is not at risk in the near term, but its internal composition is shifting meaningfully — from a commoditized double-pump category toward a bifurcated landscape comprising value-tier standard pumps and premium-tier wearable devices, each governed by distinct competitive dynamics, margin profiles, and consumer acquisition strategies.

The breast pumps market is propelled by a defined set of quantifiable drivers while simultaneously facing structural constraints that moderate the pace of expansion.

Rising breastfeeding rates globally represent the foundational demand driver. The WHO reports that exclusive breastfeeding rates have improved across low- and middle-income countries, with global initiation rates exceeding 40% in several key markets. National breastfeeding promotion campaigns in India, Brazil, and China — economies collectively representing more than 3.5 billion people — are translating into tangible volume growth for both personal-use and hospital-grade pump categories.

Workplace reintegration timelines are a second critical driver. Data from the U.S. Bureau of Labor Statistics indicates that more than 60% of mothers with infants under one year of age participate in the labor force, with the majority returning to work within 12 weeks of delivery. This dynamic creates a structural and recurring demand pool for personal-use pumps, as continued breastfeeding after return to work requires mechanical expression.

Insurance mandates and reimbursement coverage represent the most direct policy lever. In the United States alone, the ACA mandate has driven pump unit coverage to millions of beneficiaries annually, and similar coverage expansion in Germany (through statutory health insurers), France, and the United Kingdom is progressively lowering purchase barriers across the EU.

On the constraint side, high device costs remain a meaningful access barrier in price-sensitive markets. Standard electric double pumps retail between $150 and $350 in developed markets, and wearable devices exceed $400, levels that are prohibitive without insurance coverage or subsidies. In Southeast Asia and Sub-Saharan Africa, where reimbursement infrastructure is nascent, adoption remains constrained to upper-income urban demographics.

Hygiene and infection control concerns related to open-system pump designs — which risk milk contamination through the pump mechanism — are also constraining hospital adoption of lower-cost models and reinforcing a preference for closed-system, single-user designs. Regulatory scrutiny from the FDA and CE marking requirements in Europe adds compliance overhead that limits new market entrants and can delay product launches by 12 to 24 months.

The competitive landscape of the breast pumps market is characterized by a mixture of established medtech incumbents, consumer health brands, and innovation-driven challengers. The following profiles capture the strategic positioning of the primary participants:

Koninklijke Philips N.V.: A global medtech leader competing in the breast pump category through its Philips Avent brand, with a portfolio spanning electric double pumps and manual options. The company leverages its consumer health distribution infrastructure and retail brand equity to maintain top-three global market share.

Medela AG: The dominant clinical brand globally, with deep relationships across hospital systems, NICUs, and lactation consultant networks. Medela's hospital-grade rental program provides a recurring revenue stream and functions as a brand awareness vehicle for its consumer-tier products.

Ardo Medical AG.: A Swiss-headquartered specialist focused on clinical-grade breast pump systems, with particular strength in European hospital and home-care channels. Ardo competes on product quality and reimbursement positioning within statutory health insurance frameworks.

Hygeia Health: A U.S.-based manufacturer specializing in eco-friendly, hospital-grade electric breast pumps. Hygeia distinguishes itself through its open-return policy and sustainability positioning, targeting environmentally conscious consumers and insurance-sponsored programs.

Willow Innovations, Inc.: The pioneer of the all-in-one wearable breast pump category, Willow has attracted significant venture funding and built a loyal premium consumer base. Its app-connected platform enables milk volume tracking and personalized pumping programs.

Albert Manufacturing USA: A U.S.-based contract manufacturer and brand supplier with a focus on cost-competitive electric and manual pump solutions for retail and insurance fulfillment channels.

Linco Baby Merchandise Works Co. Ltd.: A Taiwan-based OEM and ODM manufacturer supplying breast pump components and finished products to both private-label retailers and branded companies across Asia and globally.

Ameda: A legacy brand with a long history in hospital-grade pump systems, Ameda maintains institutional relationships in U.S. hospital networks and competes through its Purely Yours consumer-tier line.

Babybelle Asia Ltd.: A regional player focused on the Asia Pacific market, offering competitively priced electric and manual breast pump solutions targeting first-time mothers in emerging market geographies.

Pigeon Corporation: A Japan-headquartered baby care conglomerate with strong brand penetration across Asia Pacific. Pigeon's breast pump portfolio is integrated within a broader maternal and infant product ecosystem, supporting cross-sell and brand loyalty dynamics.

January 2024: Willow Innovations launched its third-generation wearable breast pump, the Willow Go, featuring an enhanced motor design and expanded compatibility with its iOS and Android tracking application, targeting the mainstream premium consumer tier.

March 2024: Medela AG announced an expanded hospital supply agreement with a major U.S. health system network covering more than 45 hospital facilities, reinforcing its institutional market leadership in North America.

June 2023: Koninklijke Philips N.V. received CE mark certification for its updated Avent double electric pump model under the revised EU Medical Device Regulation (MDR) framework, enabling continued market access across European Union member states.

September 2023: Hygeia Health entered a strategic distribution partnership with a national U.S. insurance fulfillment provider, extending its reach to an additional estimated 2 million covered lives under ACA-compliant benefit programs.

November 2023: Ardo Medical AG expanded its production capacity at its Swiss manufacturing facility, investing approximately €12 million to support growing demand from European statutory health insurers and direct-to-consumer channels.

February 2023: Pigeon Corporation announced the launch of a new electric breast pump line in India, targeting the rapidly expanding urban maternal care segment amid rising female workforce participation rates.

April 2024: The U.S. FDA issued updated guidance on breast pump classification and 510(k) submission requirements, increasing compliance clarity for manufacturers but also raising the technical documentation threshold for new market entrants.

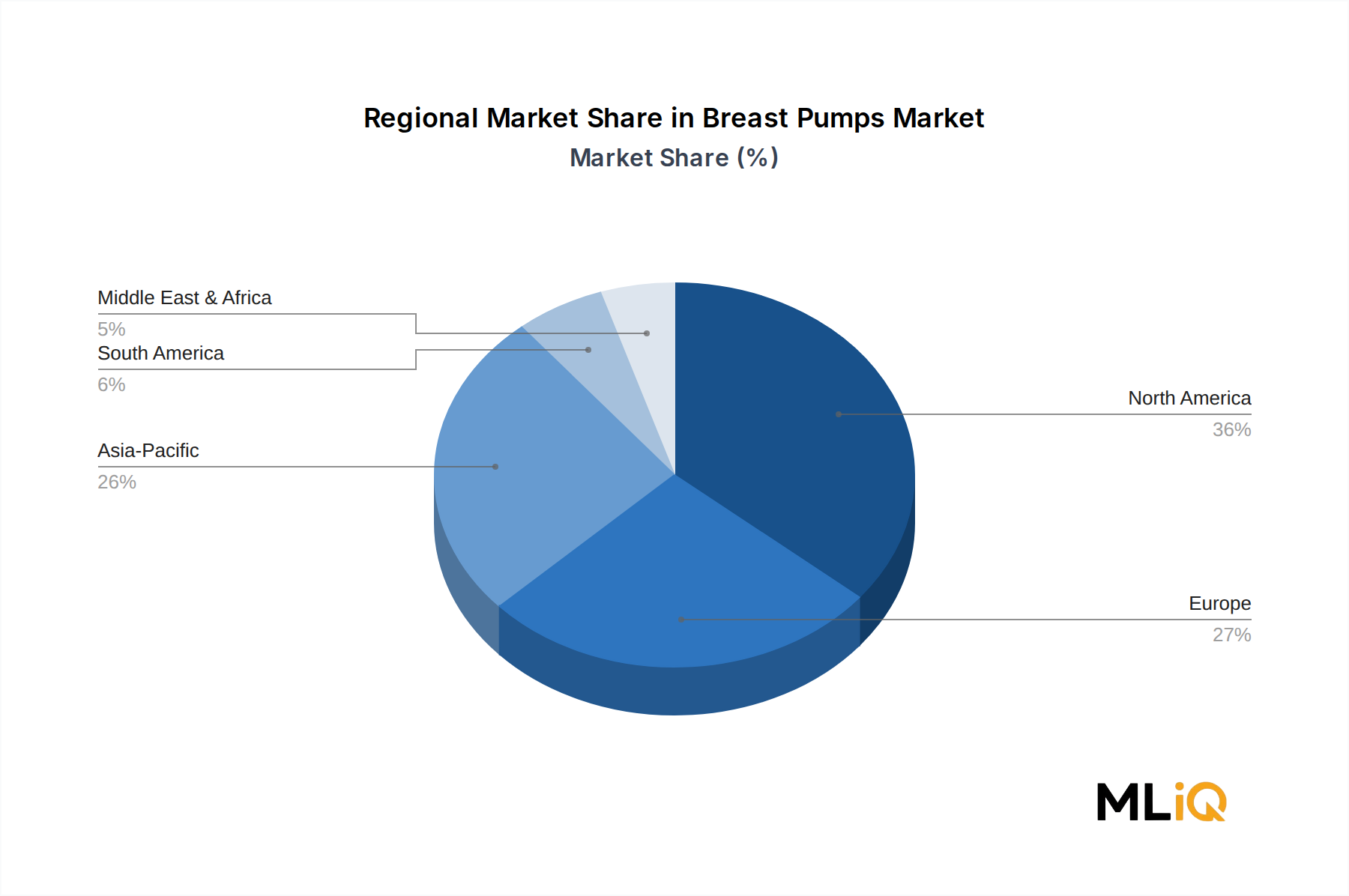

The breast pumps market exhibits pronounced regional differentiation in terms of revenue concentration, growth velocity, and underlying demand drivers.

North America is the most mature and highest-revenue region, accounting for an estimated 38% to 42% of global market value. The United States is the primary contributor, underpinned by the ACA insurance mandate, high breastfeeding awareness, and a dense retail and online distribution infrastructure. The regional CAGR is estimated at approximately 5.2%, reflecting a market that is growing steadily but maturing in terms of product penetration. Canada and Mexico contribute incrementally, with Mexico showing above-average growth potential as healthcare access expands.

Europe represents the second-largest regional market, with Germany, France, and the United Kingdom serving as the anchor economies. Statutory health insurance reimbursement in Germany and France provides a structurally supportive demand environment, while the United Kingdom's NHS breastfeeding promotion programs sustain clinical pump utilization. The European regional CAGR is estimated at 5.8%, with the Nordics and Benelux showing premium product adoption above the European average.

Asia Pacific is the fastest-growing region, with a projected regional CAGR of approximately 8.5% to 9.2%, driven by China, India, Japan, and ASEAN markets. Rising disposable incomes, increasing female labor force participation, and government-backed breastfeeding promotion in China and India are the primary catalysts. Japan and South Korea exhibit high premium product adoption, with consumers demonstrating willingness to pay for advanced wearable and smart-connected pump models.

The Middle East and Africa region is an emerging growth market, with GCC countries showing the most immediate commercial potential due to high per-capita healthcare expenditure and a growing expatriate population familiar with breast pump usage. Sub-Saharan Africa remains nascent, constrained by limited retail infrastructure and low insurance penetration, but represents a long-term volume opportunity as healthcare access expands.

South America, led by Brazil and Argentina, is growing at a moderate pace, with Brazil's public health system increasingly incorporating breastfeeding support tools into maternal care protocols. Regional CAGR is estimated at approximately 6.0%, with growth contingent on macroeconomic stability and continued public health investment.

The breast pumps market has attracted a meaningful volume of strategic capital over the past two to three years, with investment activity concentrated in two principal areas: wearable and smart-connected pump technology, and supply chain vertical integration in Asia Pacific.

Willow Innovations has been the most visible recipient of venture funding in the consumer wearable pump segment, having raised over $100 million in cumulative venture and growth equity financing. This capital has been deployed across product development, regulatory compliance, and direct-to-consumer marketing, establishing the wearable category as a credible premium tier within the broader market. The success of this model has attracted several early-stage competitors and attracted attention from strategic acquirers within the medtech and consumer health sectors.

Medela AG has pursued a strategy of selective bolt-on acquisitions to strengthen its clinical service capabilities and digital health integration. The company's investments in app-based lactation support platforms reflect a broader industry trend toward ecosystem-based retention models, where hardware is paired with subscription software services to extend customer lifetime value.

In Asia Pacific, private equity and corporate venture arms of large baby care conglomerates — including Pigeon Corporation and regional players — have increased their investment in domestic manufacturing capabilities, motivated by supply chain resilience concerns following post-pandemic logistics disruptions. These investments are also designed to capture the growing volume of cost-sensitive consumers in India, Indonesia, and Vietnam who represent the next wave of market entrants.

Strategic partnerships between pump manufacturers and insurance fulfillment companies in the United States have also emerged as a form of commercial capital allocation, with manufacturers investing in co-marketing and logistics integration to secure preferred supplier status within ACA-mandated benefit ecosystems. This dynamic effectively creates semi-exclusive distribution arrangements that function as durable competitive moats.

The Hospital Grade Breast Pumps Market sub-segment has seen institutional investment from hospital group purchasing organizations (GPOs) seeking

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6.8% from 2020-2034 |

| Segmentation |

|

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Comprehensive validation mechanisms ensuring market intelligence accuracy, reliability, and adherence to international standards.

500+ data sources cross-validated

200+ industry specialists validation

NAICS, SIC, ISIC, TRBC standards

Continuous market tracking updates

Factors such as are projected to boost the Breast Pumps Market market expansion.

Key companies in the market include Koninklijke Philips N.V., Medela AG, Ardo Medical AG., Hygeia Health, Willow Innovations, Inc., Albert Manufacturing USA, Linco Baby Merchandise Works Co. Ltd., Ameda, Babybelle Asia Ltd., Pigeon Corporation.

The market segments include Product Type, Technology, Application.

The market size is estimated to be USD 640.70 million as of 2022.

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3456, USD 4740, and USD 10995 respectively.

The market size is provided in terms of value, measured in million and volume, measured in .

Yes, the market keyword associated with the report is "Breast Pumps Market," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Breast Pumps Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.