1. What are the major growth drivers for the Gastrointestinal Therapeutics Market market?

Factors such as are projected to boost the Gastrointestinal Therapeutics Market market expansion.

+1 2315155523

Market Lens IQ is a global market intelligence and strategic consulting firm delivering advanced syndicated research reports, customized industry analysis, competitive intelligence, and data-driven advisory solutions to organizations across international markets. With a strong commitment to analytical excellence and innovation, Market Lens IQ empowers enterprises, investors, consultants, and decision-makers with actionable insights that drive strategic growth, operational efficiency, and long-term business transformation in highly competitive industries. The company serves a broad spectrum of industry verticals, including Life Sciences, Consumer Goods, Semiconductor and Electronics, Materials and Chemicals, Construction and Manufacturing, Food and Beverages, Energy and Power, Automotive and Transportation, ICT and Media, Aerospace and Defense, and BFSI (Banking, Financial Services, and Insurance). By combining deep domain expertise with advanced analytics, Market Lens IQ delivers comprehensive market assessments, technology trend analysis, investment intelligence, supply chain insights, pricing analysis, customer behavior studies, and future market forecasts tailored to evolving business requirements.

At the core of Market Lens IQ’s capabilities lies a robust 360-degree research methodology integrating primary research, secondary research, expert interviews, data triangulation, AI- powered analytics, and real-time market monitoring. Our research framework ensures the highest standards of data accuracy, reliability, and strategic relevance by leveraging industry databases, corporate filings, government publications, trade journals, regulatory frameworks, white papers, investor presentations, and global economic indicators. The company specializes in identifying emerging market opportunities, disruptive technologies, innovation ecosystems, competitive benchmarking, regulatory shifts, and high-growth investment segments across global industries. Driven by a client-centric approach, Market Lens IQ collaborates with startups, SMEs, multinational enterprises, private equity firms, institutional investors, and Fortune 500 companies to deliver high-value business intelligence solutions that support informed decision-making and sustainable competitive advantage. Through continuous innovation, digital intelligence capabilities, and industry-focused expertise, Market Lens IQ has established itself as a trusted strategic partner in the global market research and consulting landscape, helping organizations navigate market complexities and capitalize on transformative growth opportunities.

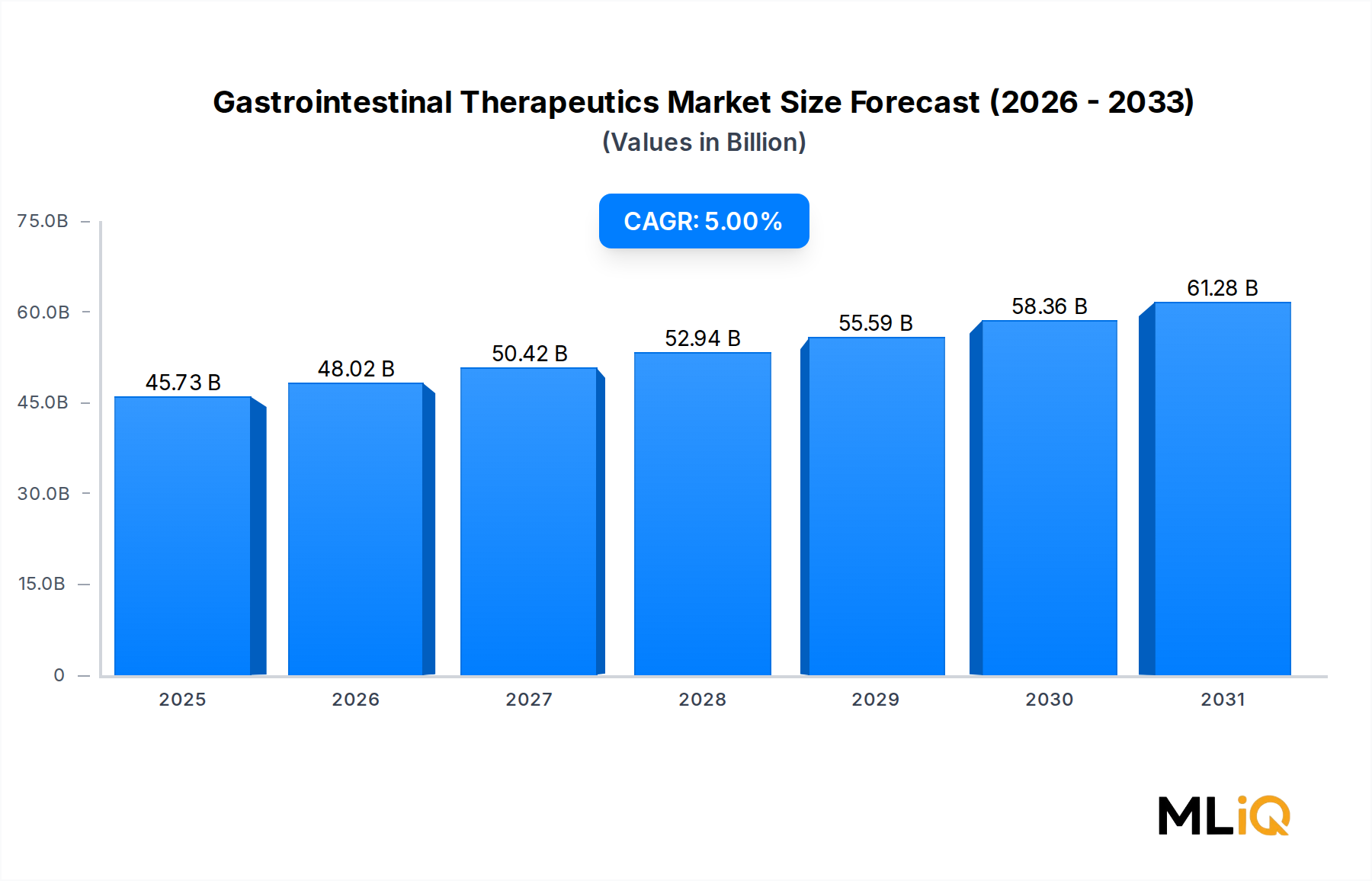

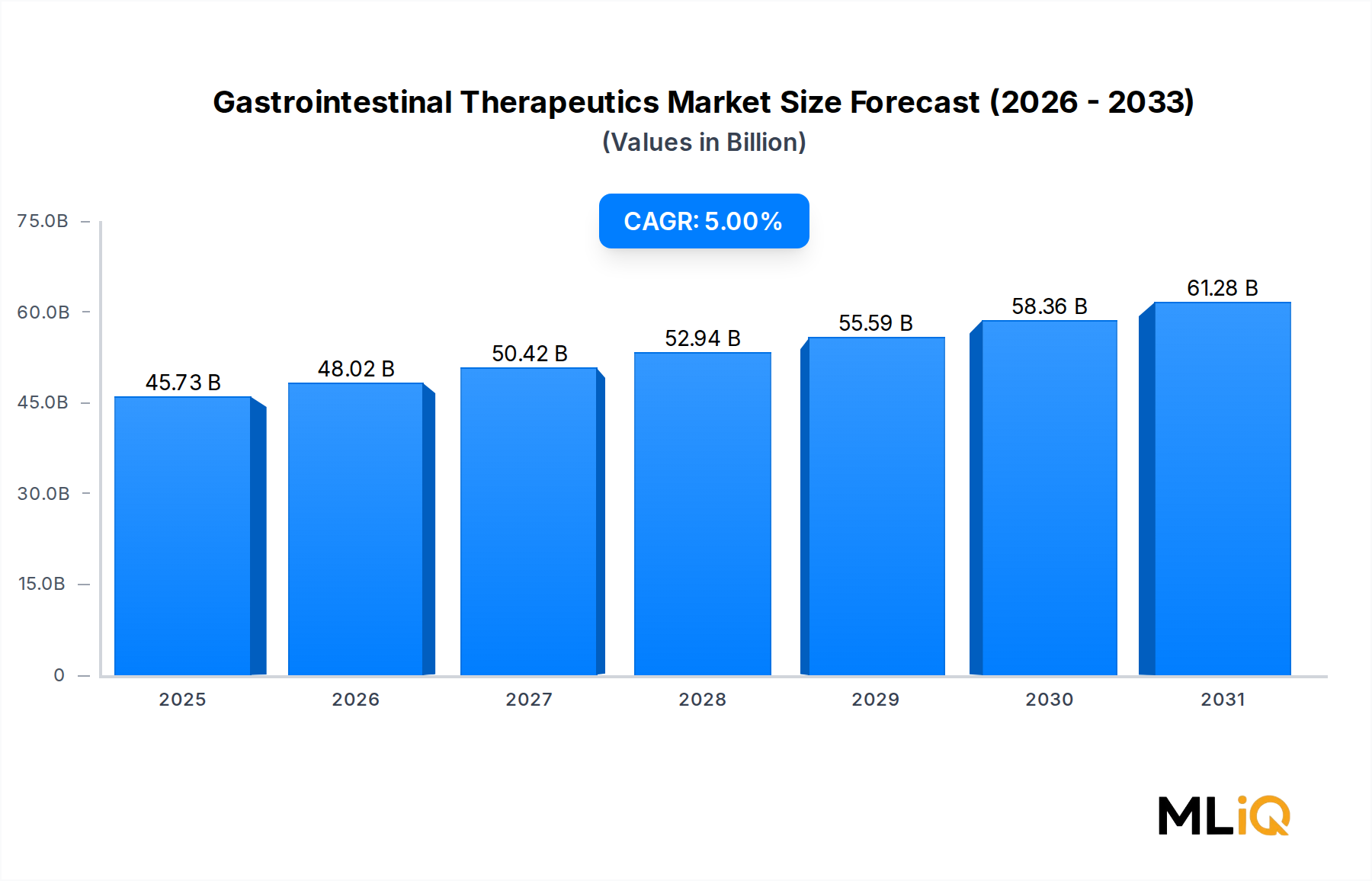

The global Gastrointestinal Therapeutics Market is currently valued at $45.73 billion and is projected to expand at a compound annual growth rate (CAGR) of 5% over the forecast period. This steady and resilient growth trajectory reflects the confluence of rising gastrointestinal (GI) disease prevalence, expanding pharmaceutical pipelines, and increasingly sophisticated patient management protocols worldwide.

Gastrointestinal disorders collectively represent one of the most burdensome disease categories globally, affecting hundreds of millions of people annually. Conditions including inflammatory bowel disease (IBD), gastroesophageal reflux disease (GERD), peptic ulcer disease, and irritable bowel syndrome (IBS) are increasingly prevalent, driven by sedentary lifestyles, dietary shifts toward processed foods, rising stress levels, and an aging global population. Urbanization in emerging markets has amplified exposure to these risk factors, widening the addressable patient pool beyond traditional high-income markets.

On the demand side, macro tailwinds include greater disease awareness among patients and healthcare providers, improved diagnostic infrastructure—particularly in Asia Pacific and Latin America—and widening insurance and reimbursement coverage for advanced therapies such as biologics. The shift from generalized treatment protocols to precision medicine approaches is accelerating prescribing of targeted agents, elevating both average treatment costs and market revenues.

Supply-side dynamics are equally favorable. A robust late-stage clinical pipeline across drug classes, including next-generation biologic agents, novel small molecules, and microbiome-targeted therapies, is expected to refresh the product landscape materially over the coming years. Biosimilar entry for established biologic brands is simultaneously creating volume growth in cost-sensitive markets while intensifying pricing competition in mature segments.

The Specialty Pharmaceuticals Market broadly intersects with GI therapeutics, as a significant proportion of GI drugs—particularly biologics and immunomodulators—fall under specialty pharmacy management. This linkage is deepening as payers increasingly require step-therapy protocols and prior authorization for high-cost agents.

North America currently commands the largest revenue share, supported by advanced healthcare infrastructure and high per-capita treatment expenditure. Asia Pacific is the fastest-growing region, propelled by population growth, improving healthcare access, and increasing GI disease burden. Europe maintains a mature but innovation-driven market landscape, with regulatory harmonization under the European Medicines Agency facilitating efficient product launches.

Looking forward, the market's growth will be sustained by biologics pipeline maturation, digital health integration for disease monitoring, and the emergence of gut microbiome therapeutics as a transformative new drug category. The overall outlook through the end of the forecast period remains constructive, underpinned by structural demand growth and ongoing pharmaceutical innovation.

Among all drug classes within the Gastrointestinal Therapeutics Market, biologics represent the dominant and fastest-growing segment by revenue share. This leadership position is rooted in the clinical superiority of biologic agents over conventional small molecules for severe and moderate-to-severe GI conditions, particularly inflammatory bowel disease and its two primary subtypes: Crohn's disease and ulcerative colitis.

Biologics encompass a broad class of complex, large-molecule drugs derived from living cells. In the GI context, the most commercially significant categories include anti-tumor necrosis factor (anti-TNF) agents, anti-integrin therapies, and interleukin inhibitors. Anti-TNF agents such as adalimumab and infliximab pioneered the modern biologic era in GI medicine, achieving blockbuster status and collectively generating tens of billions in cumulative global sales. More recently, selective anti-integrin therapies like vedolizumab and IL-12/23 inhibitors such as ustekinumab have expanded the biologic armamentarium, offering differentiated efficacy and safety profiles.

The dominance of biologics is reinforced by several structural factors. First, the unmet clinical need in IBD remains high—a substantial proportion of patients fail or become intolerant to conventional immunosuppressants, creating a persistent addressable population for advanced therapies. Second, biologics command substantially higher average selling prices compared to small molecules, inflating their revenue contribution even at lower prescription volumes. Third, long-duration treatment regimens—often lasting years or indefinitely—generate recurring revenue streams for manufacturers.

Key players within the biologics segment include AbbVie Inc., which markets the world's leading IBD biologic; Takeda Pharmaceutical Company Limited, whose gut-selective anti-integrin franchise has achieved significant global penetration; and Pfizer Inc., which has expanded its GI biologic portfolio through both internal development and strategic acquisitions. Bristol-Myers Squibb Company has also entered the space with IL pathway-targeted agents.

Biosimilar competition is beginning to erode the revenue base of first-generation anti-TNF biologics, particularly in Europe and increasingly in the United States. However, this erosion is being partially offset by volume expansion in lower-income markets where biosimilars are making biologic therapy accessible for the first time. Meanwhile, originator manufacturers are defending market position through next-generation molecule development, subcutaneous formulation launches, and patient support program enhancements.

The Biologics Drug Market overall is experiencing structural expansion, with GI indications constituting one of its most active therapeutic areas alongside oncology and immunology. Regulatory agencies globally have streamlined biologic approval pathways, and the number of GI-focused biologics in Phase II and Phase III trials has never been higher. Pipeline candidates targeting novel pathways—including JAK inhibitors, S1P receptor modulators, and IL-23-specific antibodies—are poised to enter the market and further reinforce the segment's revenue dominance.

Share consolidation within the biologic segment is expected to continue, with established players leveraging manufacturing scale, real-world evidence generation, and global commercialization networks to maintain competitive advantage against both new biologic entrants and biosimilar challengers.

The Gastrointestinal Therapeutics Market is shaped by a well-defined set of quantifiable drivers and measurable constraints that collectively determine the market's growth velocity.

Driver 1 — Rising GI Disease Prevalence: IBD affects an estimated 6.8 million people globally, with incidence rates rising sharply in newly industrialized nations across Asia and the Middle East. GERD affects approximately 20% of adults in Western populations, while IBS prevalence is estimated at 10–15% globally. These figures collectively translate into a structural, non-cyclical demand base that insulates the market from macroeconomic downturns.

Driver 2 — Aging Demographics: Adults over age 65 exhibit significantly higher rates of GI disease, polypharmacy-related gastric complications, and functional bowel disorders. With the global population aged 65+ projected to double by 2050, the age-related demand multiplier for GI therapeutics is substantial and growing.

Driver 3 — Innovation Pipeline and New Approvals: The U.S. Food and Drug Administration (FDA) and European Medicines Agency (EMA) collectively approved over a dozen new GI-focused molecules between 2020 and 2025, including several first-in-class agents. Each new approval expands the addressable patient pool and creates incremental revenue opportunities beyond existing treatment paradigms.

Driver 4 — Expanding Reimbursement in Emerging Markets: Government healthcare expenditure per capita has risen significantly in China, Brazil, India, and Southeast Asia, improving reimbursement access for branded and specialty GI therapies.

Constraint 1 — Pricing Pressure and Biosimilar Erosion: The U.S. Inflation Reduction Act and European reference pricing mechanisms are exerting downward pressure on biologic list prices. Biosimilar versions of top-selling GI biologics have captured meaningful market share in the EU, compressing originator revenues.

Constraint 2 — Stringent Regulatory Requirements: Accelerating requirements for real-world evidence, post-marketing surveillance studies, and long-term safety data add development time and cost, delaying product launches and squeezing net margins for smaller developers.

Constraint 3 — Patient Adherence Challenges: Chronic GI conditions require sustained therapy, yet adherence rates for oral and injectable GI medications remain suboptimal—estimated at below 60% for maintenance IBD therapies—limiting real-world efficacy and reducing drug utilization rates relative to diagnosed patient populations.

Bausch Health Companies Inc.: A vertically integrated GI specialist with an extensive branded and generic GI portfolio spanning acid-related disorders and bowel disease; the company continues to invest in both branded GI assets and off-patent line extensions to sustain revenue across treatment segments.

Bayer AG: Maintains a significant OTC and prescription GI presence, particularly in antacid formulations and self-care gastrointestinal products; Bayer leverages its global consumer health infrastructure to distribute GI therapies across both developed and emerging markets.

AbbVie Inc.: Holds the market-leading position in biologic IBD therapy through its flagship anti-TNF franchise; AbbVie is actively diversifying its GI pipeline with next-generation IL-23 and JAK-inhibitor compounds to offset biosimilar-related revenue pressure on its core asset.

AstraZeneca plc: Maintains a focused GI presence in proton pump inhibitor and acid-related disorder management; the company has historically been a major player in GERD pharmacotherapy and continues to defend its market share through branded formulation differentiation.

Cosmo Pharmaceuticals: Specializes in targeted colonic delivery technologies and has developed a proprietary portfolio of GI agents including formulations for IBD and bowel preparation; Cosmo's technological differentiation in colonic drug delivery provides a durable competitive moat in specialty GI segments.

Organon Group of Companies: Focuses on established branded medicines and biosimilars with GI applications, leveraging a broad global commercial footprint in women's health and established medicine portfolios that include GI therapeutics across emerging markets.

Teva Pharmaceutical Industries Limited: A leading global generics manufacturer with extensive presence across GI drug classes including aminosalicylates, proton pump inhibitors, and laxatives; Teva is also advancing a biosimilar pipeline targeting high-value biologic GI therapies.

Pfizer Inc.: Pursues a dual strategy in GI markets through both innovative biologic agents and established small-molecule franchises; Pfizer's global manufacturing and regulatory capabilities position it to compete effectively across both branded and biosimilar segments.

Takeda Pharmaceutical Company Limited: A dedicated GI-focused pharmaceutical company with one of the deepest GI pipelines among large-cap biopharma peers; Takeda's gut-selective biologic franchise and ongoing investment in novel GI mechanisms reinforce its strategic leadership in the therapeutic area.

Bristol-Myers Squibb Company: Has expanded its immunology pipeline into GI indications with selective cytokine inhibitors; Bristol-Myers Squibb is leveraging its established immunology infrastructure and commercial relationships to gain share in inflammatory GI conditions.

January 2024: AbbVie received FDA approval for a next-generation IL-23 inhibitor for moderate-to-severe Crohn's disease, expanding its biologic GI franchise beyond the anti-TNF class and reinforcing its position as the segment leader.

March 2024: Takeda Pharmaceutical Company Limited announced positive Phase III results for a subcutaneous formulation of its anti-integrin therapy, enabling more convenient home administration and potentially expanding the eligible patient population for biologic IBD therapy.

May 2024: Teva Pharmaceutical Industries Limited launched a biosimilar version of a top-selling anti-TNF biologic in key European markets, accelerating biosimilar penetration in the EU and intensifying pricing competition for originator manufacturers.

August 2024: Cosmo Pharmaceuticals announced a licensing agreement with a major Asian pharmaceutical company to commercialize its proprietary colonic drug delivery platform across China and Southeast Asia, marking a significant emerging-market expansion milestone.

October 2024: The U.S. FDA issued updated guidance on real-world evidence requirements for GI biologics post-approval surveillance, increasing the regulatory compliance burden for manufacturers but also providing a framework to support label expansions.

December 2024: Bristol-Myers Squibb Company reported Phase II proof-of-concept data for a novel TYK2 inhibitor in ulcerative colitis, signaling a potential new competitive entrant in the advanced therapy segment for IBD.

February 2025: Pfizer Inc. completed enrollment in a pivotal Phase III trial evaluating an oral JAK inhibitor for moderate-to-severe IBD, with topline data anticipated in the second half of 2025.

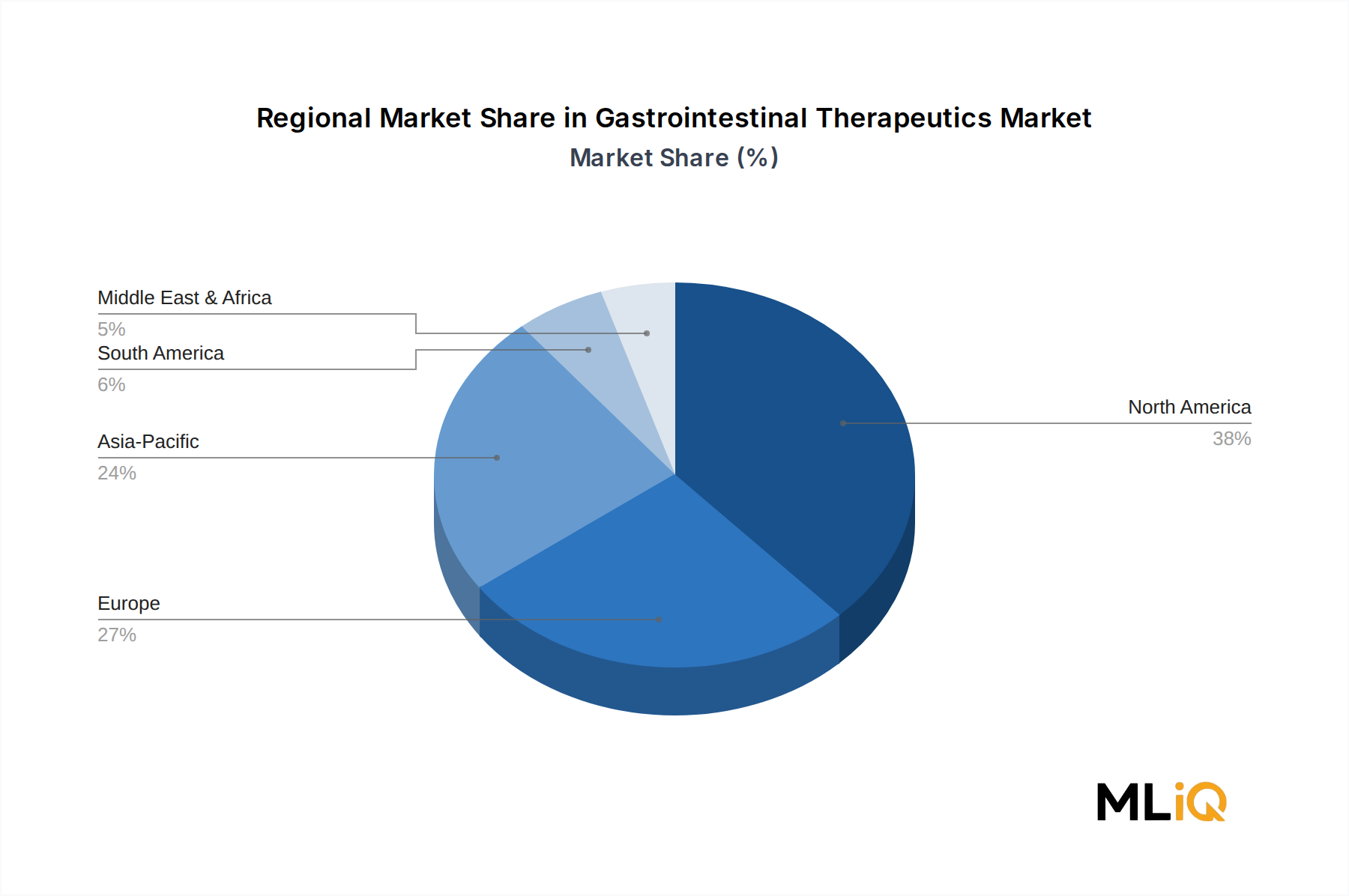

The Gastrointestinal Therapeutics Market exhibits meaningfully differentiated growth dynamics across its five major geographic regions, reflecting divergent healthcare infrastructure maturity, disease prevalence patterns, and reimbursement environments.

North America commands the largest regional revenue share, estimated at approximately 38–40% of global market value, anchored by the United States. The U.S. market benefits from the highest per-capita pharmaceutical spending globally, broad reimbursement coverage for specialty GI biologics, and a dense network of academic medical centers specializing in GI disease. Canada and Mexico contribute incrementally, with Mexico representing a volume-growth market for generic GI therapies. North America's CAGR is estimated at approximately 4.5%, reflecting market maturity offset by ongoing biologic innovation.

Europe represents the second-largest regional market, with Germany, France, the United Kingdom, and Italy as primary revenue contributors. Europe is characterized by universal healthcare systems with robust GI disease management protocols, though reference pricing and mandatory biosimilar substitution policies constrain branded biologic pricing. The region's CAGR is estimated at 3.8–4.2%, with growth driven by pipeline launches and rising IBD incidence in Eastern European markets. The Nordics and Benelux subregions demonstrate elevated adoption of biologic therapies relative to regional peers.

Asia Pacific is the fastest-growing region, with an estimated CAGR of 7.0–7.5%, driven by China, India, Japan, South Korea, and ASEAN markets. Rapid urbanization, dietary westernization, and improving diagnostic capabilities are inflating GI disease incidence across the region. China's National Reimbursement Drug List expansions have materially improved biologic GI therapy access, while Japan's established healthcare infrastructure supports innovation-driven adoption. India represents a high-volume generics market with growing branded specialty GI penetration.

South America, led by Brazil and Argentina, is experiencing CAGR growth of approximately 5.5–6.0%, supported by expanding middle-class healthcare access and increasing GI disease awareness. Brazil's public health system is progressively incorporating biologic IBD therapies into its standard of care protocols, driving volume growth.

Middle East and Africa represents the smallest but potentially high-growth region, with GCC countries—particularly Saudi Arabia and the UAE—driving above-average GI therapy spending due to elevated GERD and obesity prevalence, high per-capita healthcare expenditure, and a preference for branded pharmaceuticals. Africa's contribution remains limited by infrastructure constraints but is expected to grow as the Digestive Health Supplements Market and OTC GI categories expand alongside improving retail pharmacy infrastructure.

The Gastrointestinal Therapeutics Market serves a heterogeneous end-user base, with distinct purchasing behavior across hospital pharmacies, drug stores and retail pharmacies, and online providers.

Hospital pharmacies represent the primary distribution channel for high-cost specialty GI therapies, including biologics and intravenous infusion agents. Procurement decisions in this channel are institutionally driven, with hospital formulary committees, pharmacy and therapeutics (P&T) committees, and group purchasing organizations (GPOs) playing central roles. Price sensitivity in the hospital channel is acute for generic and commodity GI products but less determinative for branded biologics, where clinical differentiation and payer formulary positioning are more influential.\

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5% from 2020-2034 |

| Segmentation |

|

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Comprehensive validation mechanisms ensuring market intelligence accuracy, reliability, and adherence to international standards.

500+ data sources cross-validated

200+ industry specialists validation

NAICS, SIC, ISIC, TRBC standards

Continuous market tracking updates

Factors such as are projected to boost the Gastrointestinal Therapeutics Market market expansion.

Key companies in the market include Bausch Health Companies Inc., Bayer AG, AbbVie Inc., AstraZeneca plc, Cosmo Pharmaceuticals, Organon Group of Companies, Teva Pharmaceutical Industries Limited, Pfizer Inc., Takeda Pharmaceutical Company Limited, Bristol-Myers Squibb Company.

The market segments include Drug Class, Application, Distribution Channel.

The market size is estimated to be USD 45.73 billion as of 2022.

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3570, USD 5730, and USD 9600 respectively.

The market size is provided in terms of value, measured in billion and volume, measured in .

Yes, the market keyword associated with the report is "Gastrointestinal Therapeutics Market," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Gastrointestinal Therapeutics Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.