1. What are the major growth drivers for the Pocket Otoscope Market market?

Factors such as are projected to boost the Pocket Otoscope Market market expansion.

Pocket Otoscope Market

Pocket Otoscope Market

Market Lens IQ is a global market intelligence and strategic consulting firm delivering advanced syndicated research reports, customized industry analysis, competitive intelligence, and data-driven advisory solutions to organizations across international markets. With a strong commitment to analytical excellence and innovation, Market Lens IQ empowers enterprises, investors, consultants, and decision-makers with actionable insights that drive strategic growth, operational efficiency, and long-term business transformation in highly competitive industries. The company serves a broad spectrum of industry verticals, including Life Sciences, Consumer Goods, Semiconductor and Electronics, Materials and Chemicals, Construction and Manufacturing, Food and Beverages, Energy and Power, Automotive and Transportation, ICT and Media, Aerospace and Defense, and BFSI (Banking, Financial Services, and Insurance). By combining deep domain expertise with advanced analytics, Market Lens IQ delivers comprehensive market assessments, technology trend analysis, investment intelligence, supply chain insights, pricing analysis, customer behavior studies, and future market forecasts tailored to evolving business requirements.

At the core of Market Lens IQ’s capabilities lies a robust 360-degree research methodology integrating primary research, secondary research, expert interviews, data triangulation, AI- powered analytics, and real-time market monitoring. Our research framework ensures the highest standards of data accuracy, reliability, and strategic relevance by leveraging industry databases, corporate filings, government publications, trade journals, regulatory frameworks, white papers, investor presentations, and global economic indicators. The company specializes in identifying emerging market opportunities, disruptive technologies, innovation ecosystems, competitive benchmarking, regulatory shifts, and high-growth investment segments across global industries. Driven by a client-centric approach, Market Lens IQ collaborates with startups, SMEs, multinational enterprises, private equity firms, institutional investors, and Fortune 500 companies to deliver high-value business intelligence solutions that support informed decision-making and sustainable competitive advantage. Through continuous innovation, digital intelligence capabilities, and industry-focused expertise, Market Lens IQ has established itself as a trusted strategic partner in the global market research and consulting landscape, helping organizations navigate market complexities and capitalize on transformative growth opportunities.

+1 2315155523

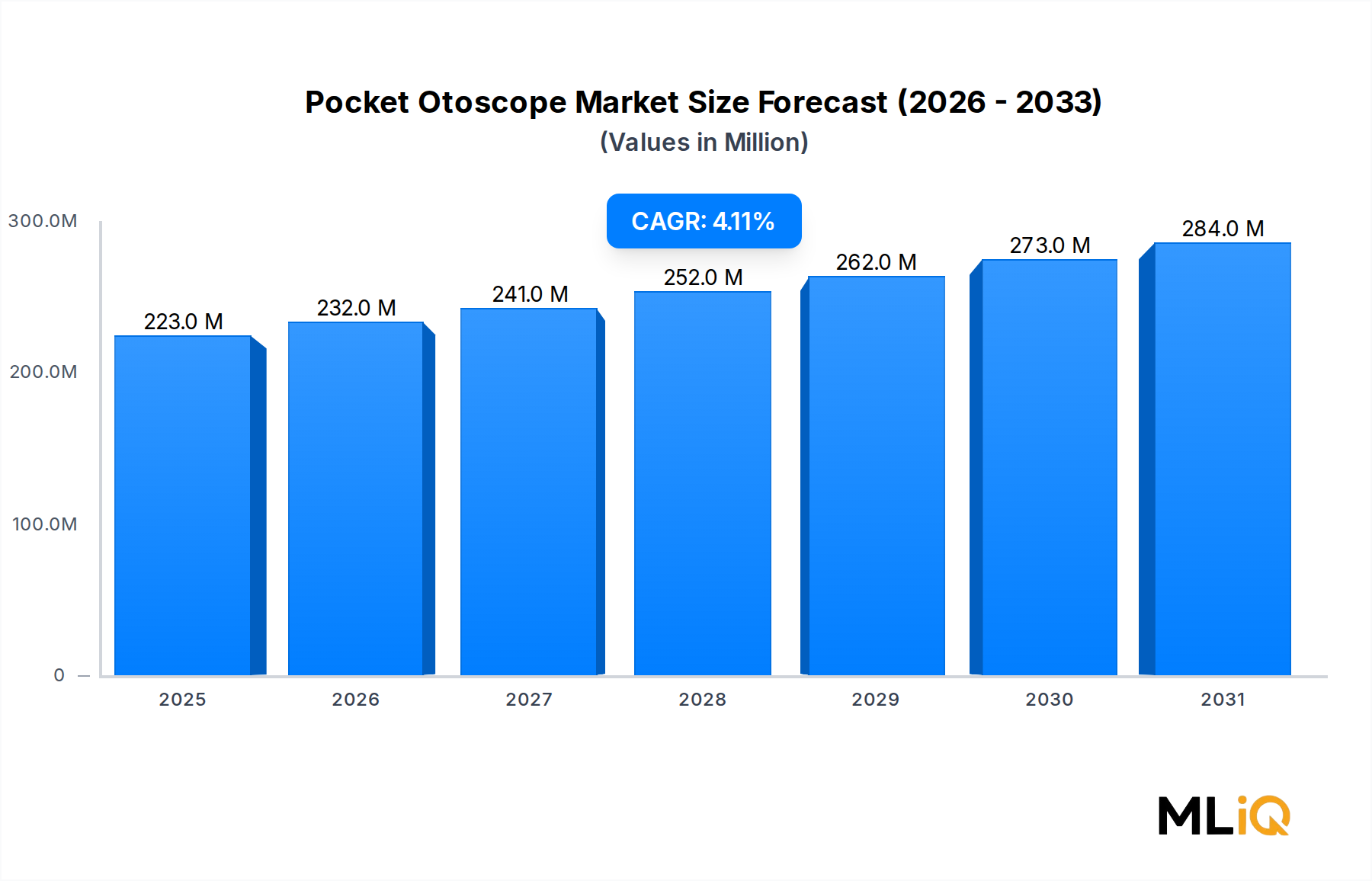

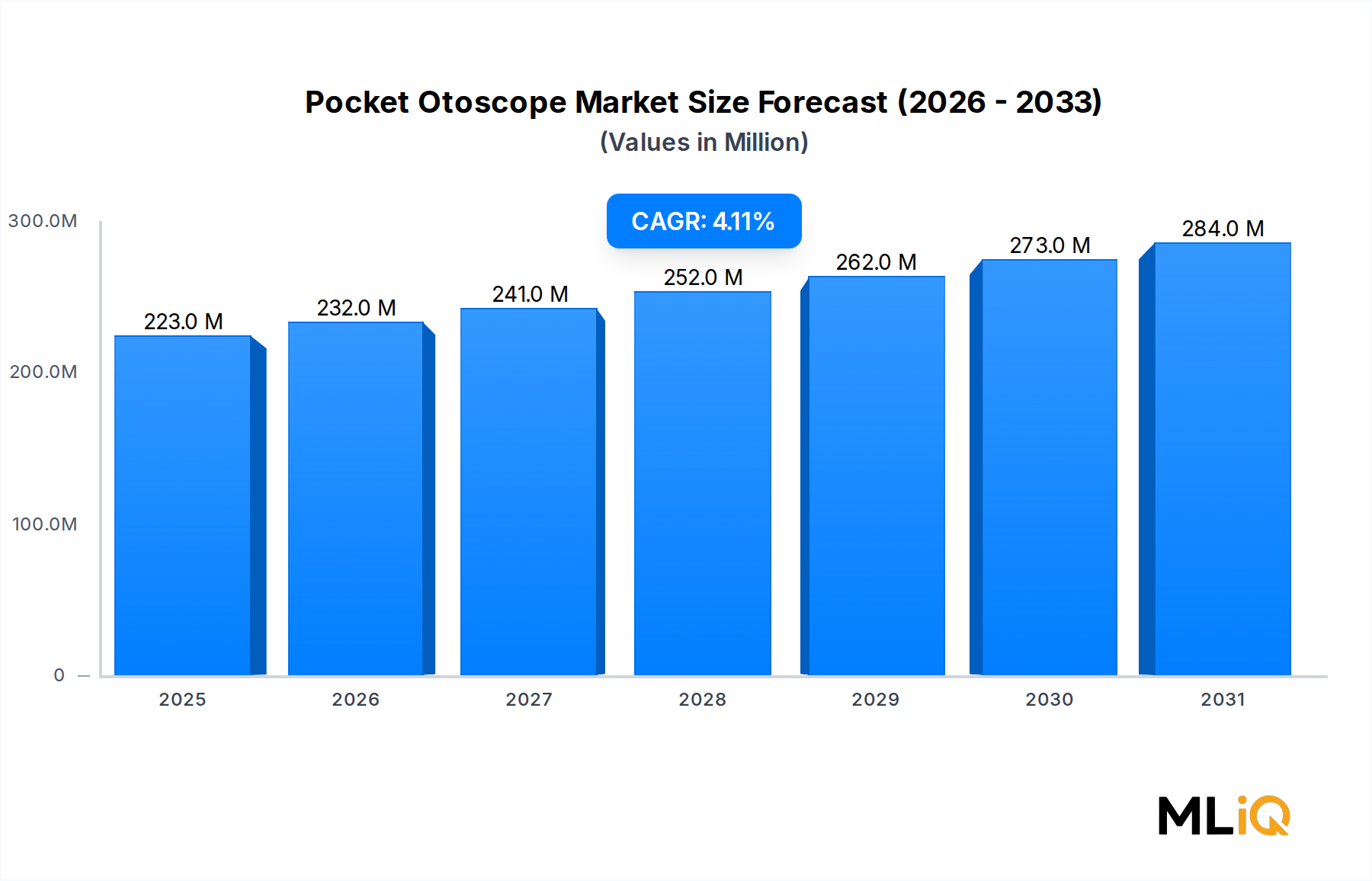

The global Pocket Otoscope Market was valued at $222.5 million in 2024 and is projected to expand at a compound annual growth rate (CAGR) of 4.18% through the forecast period of 2025 to 2033. This steady growth trajectory reflects the sustained clinical importance of compact, portable otoscopic examination tools across primary care, emergency medicine, and specialist audiology practices worldwide.

Pocket otoscopes occupy a critical niche within the broader Diagnostic Instruments Market, offering clinicians a lightweight, cost-effective alternative to full-sized wall-mounted units. Their relevance has been amplified by a global push toward decentralized healthcare delivery, where point-of-care assessments must be conducted outside traditional hospital settings — in mobile clinics, rural health outposts, military field units, and residential care environments.

Key demand drivers include rising incidence rates of ear infections (otitis media), which remain among the most frequently diagnosed conditions in pediatric medicine globally. The World Health Organization estimates that chronic suppurative otitis media affects approximately 65 to 330 million individuals worldwide, driving sustained procurement demand for affordable, portable examination tools. Additionally, expanding healthcare infrastructure in Asia Pacific and Sub-Saharan Africa is opening new institutional procurement channels.

Macro tailwinds further supporting the market include growing medical tourism, heightened telemedicine integration (digital otoscopes complementing pocket formats), increased government investment in preventive healthcare diagnostics, and the proliferation of training programs for community health workers in low- and middle-income countries. These workers increasingly require compact, durable, and inexpensive diagnostic tools, precisely the profile of pocket otoscopes.

On the innovation front, the integration of LED optics has materially improved illumination quality without increasing device bulk, while ergonomic handle redesigns are reducing clinician fatigue during high-volume examinations. The shift from halogen to LED-based systems has also lowered total cost of ownership, extending device lifespan and reducing consumable expenditure.

Looking forward, the market outlook through 2033 is constructive. Institutional procurement cycles in hospitals and research centers remain stable, while emerging market expansion and product premiumization in developed regions will collectively sustain the 4.18% CAGR. The competitive landscape is moderately fragmented, with a mix of established diagnostics brands and regional manufacturers competing on price, optical quality, and handle ergonomics. Strategic product launches, distributor partnerships, and OEM arrangements are expected to define competitive positioning over the forecast horizon.

Among all product segments in the Pocket Otoscope Market — which include Stainless Steel Handle, Plastic Handle, Chrome Finished Handle, and Others — the Stainless Steel Handle sub-segment commands the largest revenue share. This dominance is attributable to a convergence of clinical preference, institutional procurement standards, durability requirements, and reimbursement considerations across hospital and research center end-users.

Stainless steel handle otoscopes are the preferred choice in hospital environments because they withstand rigorous autoclave sterilization cycles and repeated chemical disinfection without structural degradation. Infection control protocols in tertiary care hospitals — particularly post-pandemic — demand instruments that can be fully sterilized between patient contacts, a standard that plastic-handle variants struggle to consistently meet. This functional superiority directly underpins the segment's revenue leadership.

From a materials engineering perspective, medical-grade stainless steel (typically 316L or 304 alloy) offers a superior strength-to-weight ratio compared to polycarbonate or ABS plastics, while also providing corrosion resistance critical in humid clinical environments. The tactile authority and perceived quality associated with stainless steel also influences physician purchasing decisions, particularly among specialist otolaryngologists and general practitioners who view their diagnostic instruments as professional identity markers.

Key players concentrating their product lines in the stainless steel handle segment include Welch Allyn, which has long positioned premium stainless steel diagnostic sets as flagship offerings within hospital procurement programs, and American Diagnostic Corporation, which markets stainless steel pocket otoscopes at accessible price points targeting both institutional and individual clinician buyers. Instruments GB and Medica International have similarly built stainless steel handle product lines targeting UK and European hospital procurement tenders respectively.

The segment's market share is consolidating rather than eroding, driven by several reinforcing dynamics. First, group purchasing organizations (GPOs) in North America and national health service procurement bodies in Europe consistently specify stainless steel instruments in their standardized diagnostic equipment catalogs. Second, the lifecycle economics favor stainless steel: while upfront unit costs are higher than plastic alternatives, lower replacement frequency and compatibility with existing sterilization infrastructure reduce total cost per examination over multi-year procurement horizons.

Volume dynamics within the stainless steel handle segment are also being shaped by the Handheld Medical Devices Market, where modular diagnostic handle platforms — allowing interchangeable heads for otoscopic, ophthalmoscopic, and laryngoscopic use — are gaining traction. Stainless steel handles dominate this modular category because their dimensional tolerances and thread engineering are more compatible with precision interchangeable head systems than molded plastic alternatives.

Nevertheless, the segment faces incremental pressure from advanced polymer composites that mimic metallic aesthetics while offering reduced weight. Chrome Finished Handle variants — which apply chrome plating over brass or zinc alloy substrates — are gaining minor share in mid-tier markets where cost sensitivity limits stainless steel adoption but institutional appearance standards preclude full plastic adoption. This dynamic is most visible in Latin America and Southeast Asia, where mid-tier private hospital chains are growing procurement volumes.

Overall, the stainless steel handle sub-segment is expected to maintain its leading revenue position through 2033, with its share potentially tightening as LED and digital integration — features more easily incorporated into stainless steel chassis — become standard differentiators in premium institutional procurement decisions.

The Pocket Otoscope Market is shaped by a set of quantifiable drivers and structural constraints that collectively define its 4.18% CAGR trajectory through 2033.

Driver 1 — Pediatric ENT Disease Burden: Otitis media is the second most commonly diagnosed illness in children under five globally, accounting for approximately 50% of all antibiotic prescriptions in pediatric primary care in the United States alone. This persistent clinical burden creates consistent, non-cyclical demand for pocket otoscopes across both hospital outpatient departments and primary care clinics.

Driver 2 — Healthcare Infrastructure Expansion in Emerging Markets: Asia Pacific and Africa are experiencing accelerated investment in primary healthcare infrastructure. India's Ayushman Bharat program, targeting coverage for over 500 million low-income beneficiaries, has stimulated procurement of basic diagnostic instruments including pocket otoscopes across newly commissioned health and wellness centers. Similar dynamics are observable in Southeast Asia under ASEAN health equity frameworks.

Driver 3 — Telemedicine and Remote Diagnostics Integration: The telemedicine market surged following 2020, with virtual ENT consultations requiring remote-compatible diagnostic documentation. Pocket otoscopes equipped with smartphone camera adapters or built-in digital sensors now bridge the gap between physical examination and teleconsultation, broadening the addressable use case and supporting unit volume growth in the Point-of-Care Diagnostics Market.

Driver 4 — Cost-Effectiveness vs. Full-Scale Alternatives: Pocket otoscopes typically retail between $15 and $200, versus $300 to $2,000+ for wall-mounted or digital diagnostic units. This price accessibility supports procurement by smaller clinics, community health workers, and individual practitioners in both developed and developing markets.

Constraint 1 — Substitution Pressure from Digital Otoscopes: Advanced digital otoscopes with integrated imaging, cloud connectivity, and AI-assisted tympanic membrane analysis are capturing premium institutional budgets. As the Medical Imaging Devices Market matures, some hospital procurement decisions are bypassing traditional pocket formats in favor of connected, documentable digital systems.

Constraint 2 — Limited Reimbursement Differentiation: Pocket otoscopes are generally not separately reimbursed by payers; their cost is embedded in procedural reimbursements. This limits clinician willingness to upgrade devices beyond functional minimums, compressing average selling prices and margin potential for manufacturers.

The competitive landscape of the Pocket Otoscope Market is moderately fragmented, with a mix of global diagnostics conglomerates, regional medical device manufacturers, and specialty distributors competing across price tiers and geographic markets. Key players identified within the market include:

Welch Allyn: A flagship brand in clinical diagnostics and a subsidiary of Hillrom (now Baxter International), Welch Allyn dominates the premium institutional segment with its MacroView and PanOptic pocket otoscope lines, leveraging its global hospital distribution network and GPO agreements to maintain leading revenue share.

American Diagnostic Corporation: Known for affordable, clinician-grade diagnostic instruments, American Diagnostic Corporation targets both institutional and individual practitioner segments with a broad SKU range of stainless steel and fiber optic pocket otoscopes, competing primarily on value-for-performance positioning.

Instruments GB: A UK-based manufacturer specializing in medical diagnostic instruments, Instruments GB serves NHS procurement frameworks and European hospital tenders with competitively priced stainless steel and chrome finished handle otoscope lines.

Medica International: Operating as both a manufacturer and distributor, Medica International focuses on supplying diagnostic instruments to emerging market healthcare systems, leveraging cost-optimized production and regional distribution partnerships.

Dr Mom Otoscopes: Positioned uniquely in the consumer and direct-to-patient segment, Dr Mom Otoscopes markets compact otoscopes to parents and caregivers for home-based ear examination, capturing a distinct market tier outside traditional institutional procurement.

Sunshine Instruments: A regional player with manufacturing capabilities in Asia, Sunshine Instruments competes primarily on price in high-volume institutional procurement tenders across Asia Pacific and the Middle East, offering OEM manufacturing services to Western brands.

Universe Surgical Equipment co: Serving hospital and clinic procurement channels in North America and the Middle East, Universe Surgical Equipment co distributes a range of pocket diagnostic instruments including otoscopes within broader surgical and diagnostic equipment catalogs.

ZZZRT Trades LLC: Operating as a distributor and reseller, ZZZRT Trades LLC aggregates diagnostic instrument supply for small clinic networks and online marketplace channels, competing on availability and pricing flexibility.

Dixie EMS: Primarily focused on emergency medical services equipment supply, Dixie EMS distributes pocket otoscopes as part of comprehensive first-responder diagnostic kits, targeting EMS agencies and military medical units.

RA Block Diagnostics: A specialty diagnostics supplier with a focus on physician office and ambulatory care markets, RA Block Diagnostics provides pocket otoscopes alongside broader diagnostic instrument portfolios.

January 2023: Welch Allyn launched an updated fiber optic pocket otoscope series featuring enhanced LED illumination and redesigned ergonomic stainless steel handles, targeting hospital outpatient and urgent care procurement cycles in North America and Western Europe.

March 2023: American Diagnostic Corporation expanded its direct-to-clinician e-commerce distribution channel, partnering with major healthcare GPO platforms to offer bundled diagnostic instrument sets including pocket otoscopes at contracted pricing for member institutions.

July 2023: A leading Asia Pacific medical device distributor signed an OEM supply agreement with Sunshine Instruments to private-label a new line of LED pocket otoscopes for distribution across Indian public health procurement programs under the Ayushman Bharat initiative.

November 2023: Dr Mom Otoscopes secured increased shelf presence across major U.S. pharmacy retail chains and online health product marketplaces, reflecting growing consumer interest in home-based pediatric diagnostic tools following post-pandemic health awareness trends.

February 2024: Instruments GB received CE mark recertification under the updated EU Medical Device Regulation (MDR 2017/745) for its full range of stainless steel pocket otoscope products, ensuring continued access to European hospital procurement tenders.

September 2024: A regional Middle Eastern distributor partnered with Medica International to supply pocket otoscopes to newly established primary health care centers across Gulf Cooperation Council (GCC) nations, as part of national healthcare capacity expansion programs.

December 2024: Universe Surgical Equipment co announced inclusion of digital-compatible pocket otoscope adapters in its standard catalog, reflecting growing demand from telehealth-integrated clinic networks seeking backward-compatible diagnostic documentation solutions.

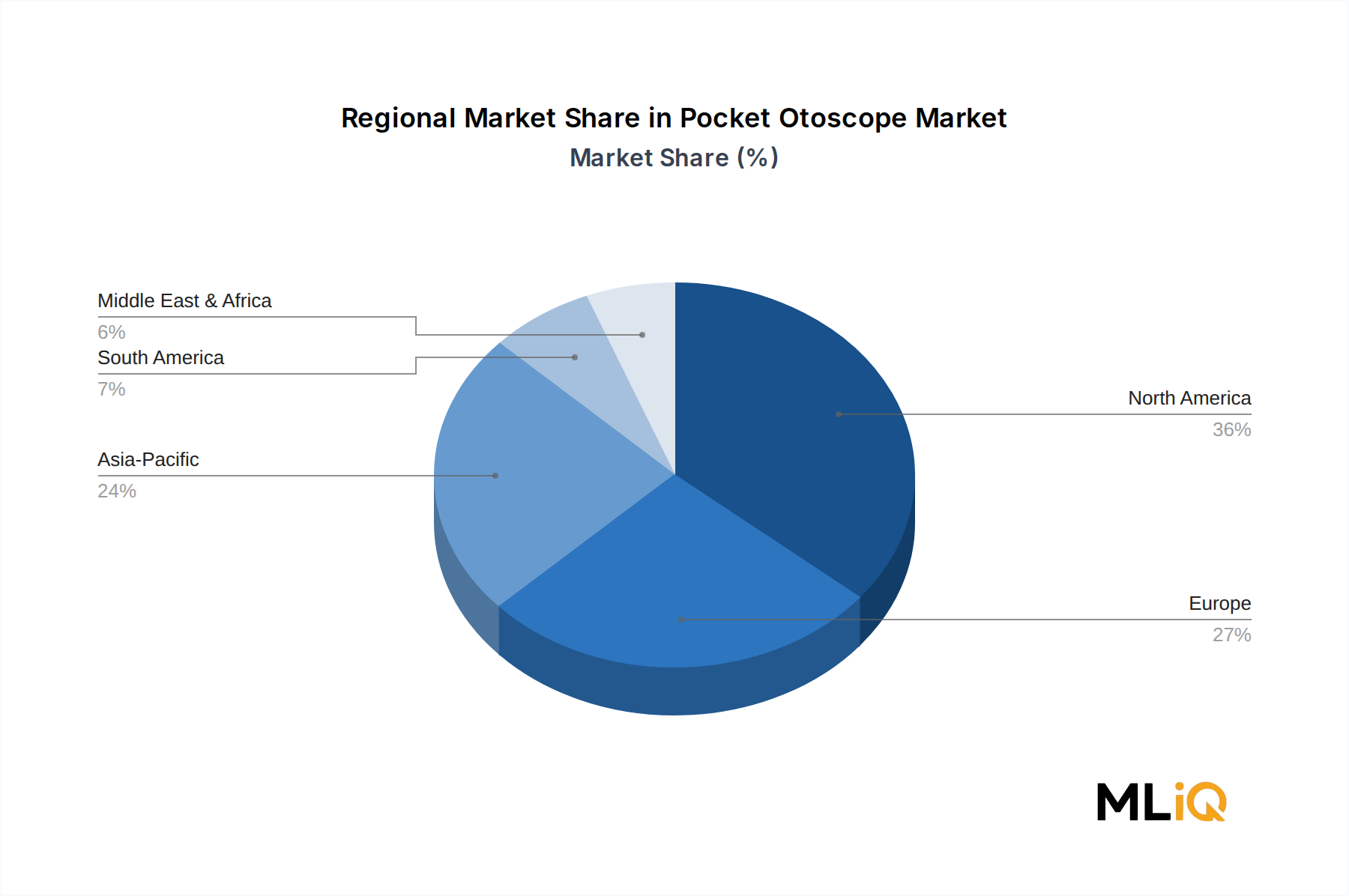

The Pocket Otoscope Market exhibits distinct regional dynamics, with North America maintaining mature market leadership while Asia Pacific emerges as the fastest-growing region.

North America accounts for the largest regional revenue share, estimated at approximately 35–38% of global market value in 2024. The United States drives this dominance through deep hospital penetration, well-established GPO procurement frameworks, and high per-capita healthcare spending. Canada and Mexico contribute incrementally, with Canada's publicly funded healthcare system providing stable institutional demand and Mexico benefiting from growing private clinic networks. The regional CAGR is estimated at approximately 3.2–3.5%, reflecting market maturity and moderate upgrade cycle activity rather than volume-driven growth.

Europe represents the second-largest regional market, with the United Kingdom, Germany, France, Italy, and Spain collectively accounting for an estimated 28–30% of global revenue. European procurement is heavily influenced by national health service tender processes and the evolving EU MDR compliance landscape, which is consolidating the supplier base toward larger, compliant manufacturers. The Benelux and Nordic sub-regions exhibit above-average per-device spending, favoring premium stainless steel and fiber optic configurations. Europe's regional CAGR is estimated at 3.5–3.8%, slightly above North America due to emerging market expansion within Eastern Europe.

Asia Pacific is the fastest-growing regional market, projected at a CAGR of 5.5–6.0% through 2033. China, India, Japan, South Korea, and ASEAN nations collectively represent the region's growth engine. India's government-funded primary healthcare expansion, China's community health center modernization programs, and Southeast Asia's rising middle-class-driven private healthcare consumption are primary demand catalysts. The Otolaryngology Devices Market in Asia Pacific is particularly dynamic, with increasing specialist clinic establishment in tier-two and tier-three cities creating new procurement volumes. Oceania, while smaller in absolute terms, exhibits premium demand characteristics aligned with developed market profiles.

The Middle East and Africa region is growing at an estimated CAGR of 4.8–5.2%, driven by GCC healthcare infrastructure investment, particularly in Saudi Arabia and the UAE, alongside expanding primary care networks in North Africa and Sub-Saharan Africa. South Africa serves as a regional distribution hub for pocket otoscope supply into the broader African continent.

South America, led by Brazil and Argentina, maintains a moderate CAGR of approximately 3.8–4.0%, with public health system procurement providing baseline demand and private clinic sector growth generating incremental premium product demand. Economic volatility in Argentina and currency risk remain structural constraints for the region.

Technological evolution within the Pocket Otoscope Market is being shaped by three principal innovation vectors: LED and fiber optic illumination advancement, smartphone integration and digital otoscopy, and artificial intelligence-assisted diagnostic interpretation.

LED illumination has fundamentally displaced traditional halogen bulb systems across all price tiers of the pocket otoscope segment. Modern medical-grade LEDs deliver color-rendering indices (CRI) above 90, closely approximating natural daylight conditions and enabling more accurate tympanic membrane assessment. LED systems also consume significantly less power, extend battery life, reduce heat generation within the speculum tip, and eliminate bulb replacement costs — collectively improving the total cost of ownership profile. Adoption of LED technology is now effectively complete at the premium institutional tier and is rapidly penetrating mid-tier and emerging market product categories. Manufacturers who have not yet transitioned to LED illumination face accelerating obsolescence pressure.

Smartphone-compatible digital otoscope adapters represent the most disruptive near-term technology trajectory. These accessories — ranging from simple optical clip attachments to sophisticated

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.18% from 2020-2034 |

| Segmentation |

|

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Comprehensive validation mechanisms ensuring market intelligence accuracy, reliability, and adherence to international standards.

500+ data sources cross-validated

200+ industry specialists validation

NAICS, SIC, ISIC, TRBC standards

Continuous market tracking updates

Factors such as are projected to boost the Pocket Otoscope Market market expansion.

Key companies in the market include Instruments GB, Medica International, Welch Allyn, Dr Mom Otoscopes, ZZZRT Trades LLC, Dixie EMS, Universe Surgical Equipment co, Sunshine Instruments, American Diagnostic Corporation, RA Block Diagnostics.

The market segments include Product, End-User.

The market size is estimated to be USD 222.5 million as of 2022.

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3690, USD 5820, and USD 9870 respectively.

The market size is provided in terms of value, measured in million and volume, measured in .

Yes, the market keyword associated with the report is "Pocket Otoscope Market," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Pocket Otoscope Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.