1. What are the major growth drivers for the Pharmaceutical Glycerin Based Products Market market?

Factors such as are projected to boost the Pharmaceutical Glycerin Based Products Market market expansion.

Market Lens IQ is a global market intelligence and strategic consulting firm delivering advanced syndicated research reports, customized industry analysis, competitive intelligence, and data-driven advisory solutions to organizations across international markets. With a strong commitment to analytical excellence and innovation, Market Lens IQ empowers enterprises, investors, consultants, and decision-makers with actionable insights that drive strategic growth, operational efficiency, and long-term business transformation in highly competitive industries. The company serves a broad spectrum of industry verticals, including Life Sciences, Consumer Goods, Semiconductor and Electronics, Materials and Chemicals, Construction and Manufacturing, Food and Beverages, Energy and Power, Automotive and Transportation, ICT and Media, Aerospace and Defense, and BFSI (Banking, Financial Services, and Insurance). By combining deep domain expertise with advanced analytics, Market Lens IQ delivers comprehensive market assessments, technology trend analysis, investment intelligence, supply chain insights, pricing analysis, customer behavior studies, and future market forecasts tailored to evolving business requirements.

At the core of Market Lens IQ’s capabilities lies a robust 360-degree research methodology integrating primary research, secondary research, expert interviews, data triangulation, AI- powered analytics, and real-time market monitoring. Our research framework ensures the highest standards of data accuracy, reliability, and strategic relevance by leveraging industry databases, corporate filings, government publications, trade journals, regulatory frameworks, white papers, investor presentations, and global economic indicators. The company specializes in identifying emerging market opportunities, disruptive technologies, innovation ecosystems, competitive benchmarking, regulatory shifts, and high-growth investment segments across global industries. Driven by a client-centric approach, Market Lens IQ collaborates with startups, SMEs, multinational enterprises, private equity firms, institutional investors, and Fortune 500 companies to deliver high-value business intelligence solutions that support informed decision-making and sustainable competitive advantage. Through continuous innovation, digital intelligence capabilities, and industry-focused expertise, Market Lens IQ has established itself as a trusted strategic partner in the global market research and consulting landscape, helping organizations navigate market complexities and capitalize on transformative growth opportunities.

+1 2315155523

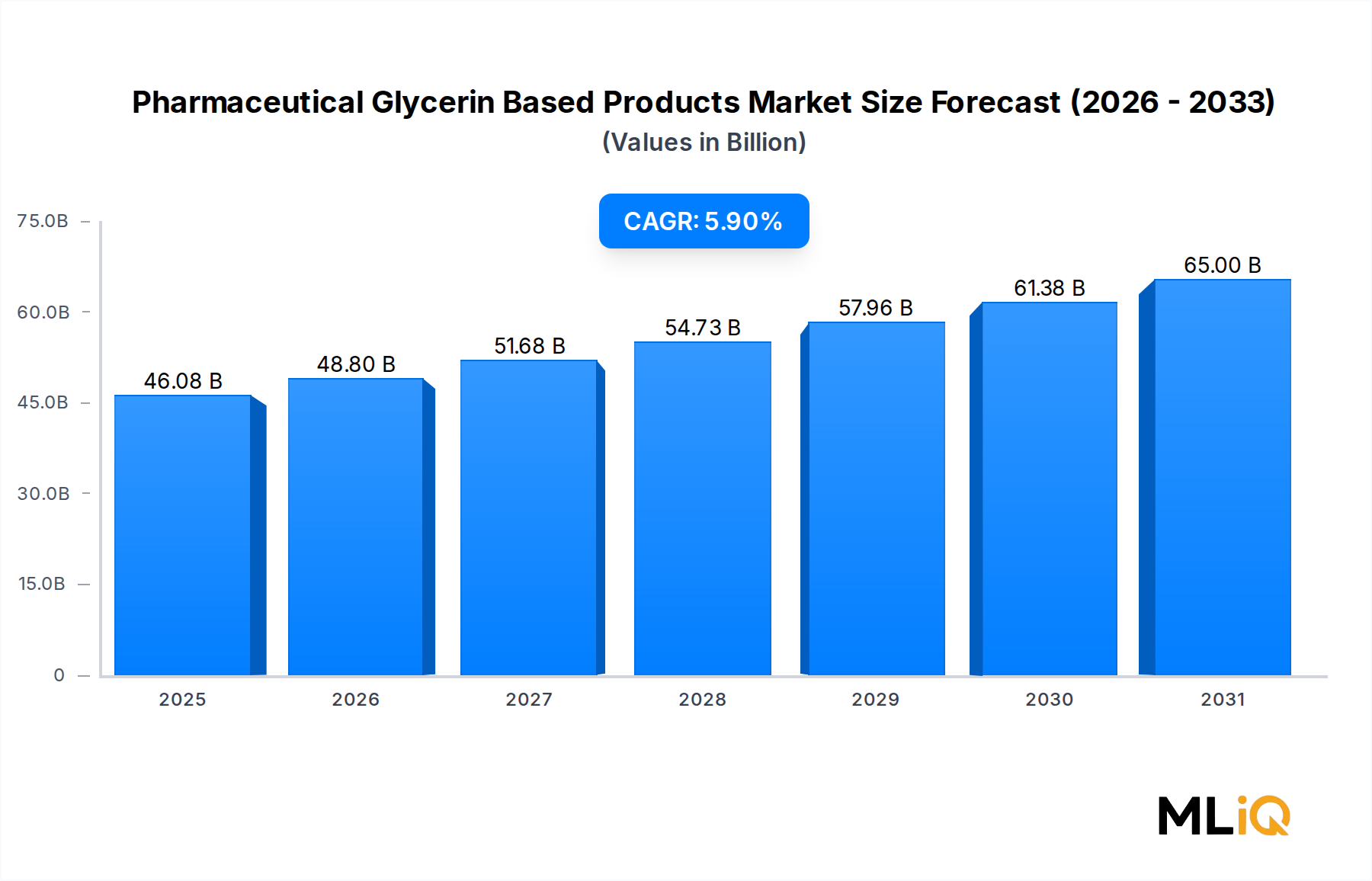

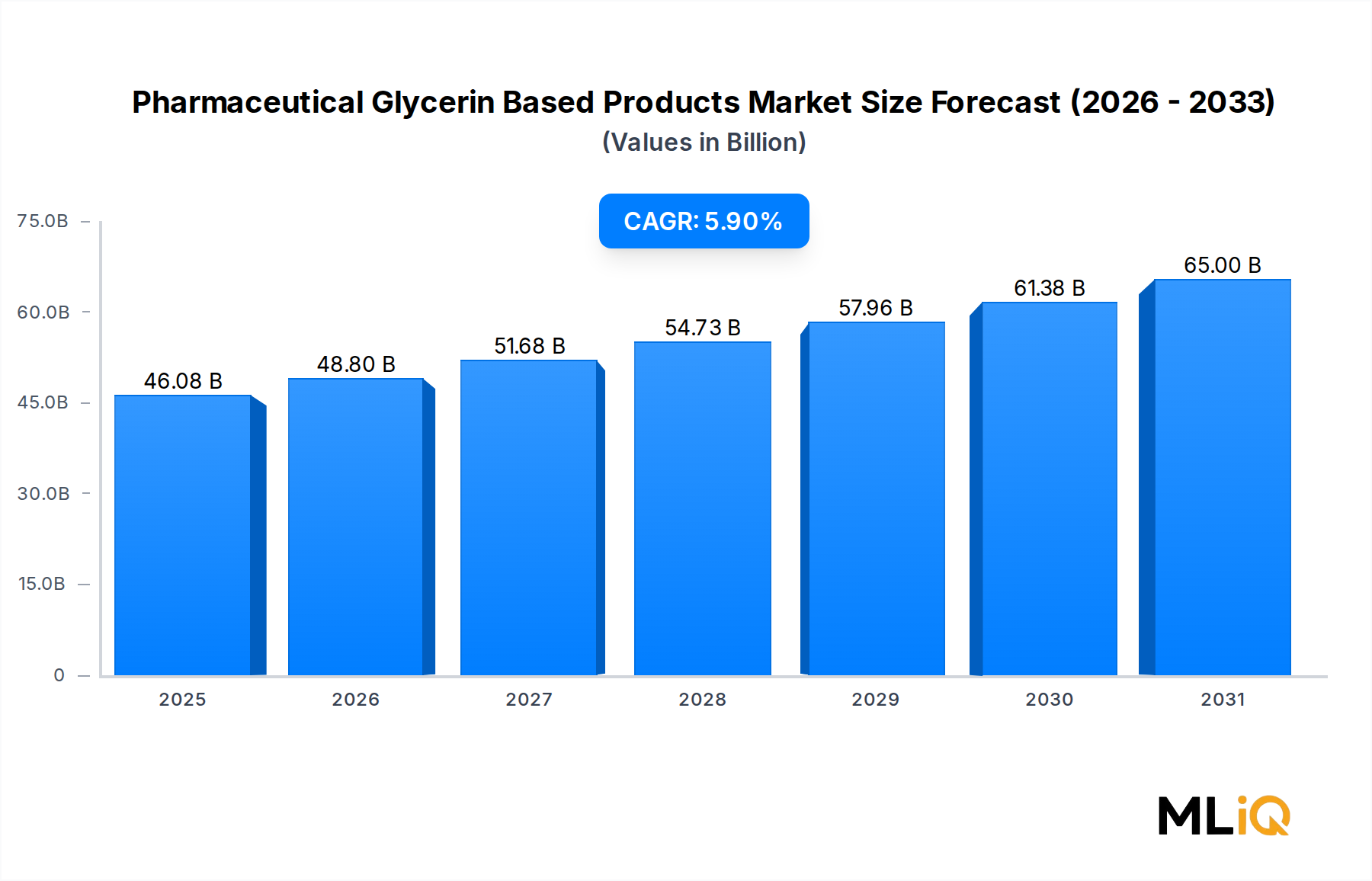

The global Pharmaceutical Glycerin Based Products Market was valued at $46.08 billion in the base assessment period and is projected to expand at a compound annual growth rate (CAGR) of 5.9% through 2033, reflecting robust demand across a broad spectrum of therapeutic and formulation-related applications. This steady trajectory positions the market to cross significantly elevated valuation thresholds by the end of the forecast horizon, driven by structural demand shifts in pharmaceutical manufacturing, growing patient populations with chronic conditions, and heightened regulatory emphasis on excipient safety and biocompatibility.

Pharmaceutical-grade glycerin remains one of the most versatile active and inactive pharmaceutical ingredients across product categories including dermatological preparations, ophthalmic solutions, cough remedies, glycerine rectal formulations, and cardiovascular-related products such as angina treatments. The compound's hygroscopic, solubilizing, and humectant properties continue to underpin its indispensability in both over-the-counter and prescription drug segments.

Key demand drivers include the accelerating global burden of skin-related disorders and dry-eye syndromes, growing geriatric populations requiring topical and suppository-based drug delivery, and the expanding penetration of pharmaceutical products in emerging economies across Asia Pacific and Latin America. The rise of biosimilars and specialty pharmaceutical formulations has further expanded glycerin's addressable application base.

Macro-level tailwinds reinforcing market growth include increased healthcare expenditure globally, post-pandemic supply chain restructuring that prioritizes domestic pharmaceutical ingredient sourcing, and an upsurge in consumer spending on OTC dermatological and respiratory health products. Additionally, the increasing integration of glycerin as a co-solvent and plasticizer in advanced drug delivery platforms is opening new revenue streams for market participants.

On the supply side, the oleochemical and biodiesel industries continue to serve as primary glycerin feedstock sources, ensuring relative feedstock availability even as pharmaceutical-grade refining capacity expands. However, crude glycerin price volatility and evolving pharmacopeial purity standards present near-term margin pressures for formulators and contract manufacturers alike.

From a forward-looking perspective, the 2025–2033 window is expected to witness intensified M&A activity among excipient specialists, increased investment in ultra-high-purity glycerin refining infrastructure, and the adoption of green chemistry principles in glycerin synthesis. These dynamics collectively reinforce a constructive long-term outlook for stakeholders across the value chain, from raw material producers to finished dosage form manufacturers.

Among all drug type segments within the Pharmaceutical Glycerin Based Products Market — including ophthalmic, cough remedies, glycerine rectal, and angina formulations — the dermatological segment commands the largest revenue share. This dominance is attributable to the convergence of high product volume, broad OTC accessibility, diversified formulation formats, and the growing global prevalence of skin conditions such as eczema, psoriasis, xerosis, and contact dermatitis.

Glycerin's role as both an active moisturizing agent and a functional excipient in dermatological formulations is central to this segment's leadership. In topical creams, lotions, gels, ointments, and serums, pharmaceutical-grade glycerin serves simultaneously as a humectant that draws moisture to the skin surface, a solubilizer for active pharmaceutical ingredients, and a viscosity modifier that improves product spreadability and patient compliance. This multifunctional profile is difficult to replicate with alternative excipients at comparable cost-performance ratios.

The dermatological segment benefits from structural demographic tailwinds. Globally, more than 600 million individuals are estimated to suffer from chronic dermatological conditions requiring continuous or recurrent topical pharmacotherapy. Aging skin exhibits reduced natural moisturization factor (NMF) activity, making glycerin-containing emollients and barrier-repair formulations medically necessary for a growing elderly cohort. In parallel, rising urbanization, pollution exposure, and altered microbiome dynamics in younger populations are expanding the patient addressable market for dermatological glycerin-based products.

From a competitive standpoint, leading pharmaceutical companies active in the dermatological glycerin-based segment include Johnson and Johnson, which maintains a diversified topical product portfolio spanning consumer health and prescription dermatology; AbbVie Inc, with its immunology-linked dermatological pipeline that increasingly incorporates glycerin-based vehicles; Bausch Health Companies Inc., a dedicated dermatology-focused entity with significant exposure to branded topical formulations; and Croda International plc, which plays a pivotal role as a high-performance ingredient supplier enabling premium dermatological formulations for third-party drug manufacturers.

Market share within the dermatological sub-segment is gradually consolidating toward larger players with integrated supply chains and robust regulatory affairs capabilities, as pharmacopeial compliance requirements for glycerin purity (meeting United States Pharmacopeia and European Pharmacopoeia standards) create meaningful barriers to entry for smaller formulators. The segment is also witnessing premiumization, with dermocosmetic and prescription-strength glycerin formulations commanding higher average selling prices than standard OTC moisturizers.

Geographically, North America and Europe collectively represent the dominant revenue pool for dermatological glycerin-based products, reflecting higher per-capita healthcare spending, well-established reimbursement frameworks for prescription dermatologicals, and elevated consumer awareness of skin health. However, Asia Pacific is the fastest-growing sub-region within this segment, driven by expanding middle-class populations in China and India, rising dermatological diagnosis rates, and increasing pharmaceutical retail infrastructure.

The dermatological segment's share is expected to remain above 35% of total market revenue through 2033, with its absolute growth in dollar terms outpacing all other drug type sub-segments owing to the sheer volume of OTC product launches, the expansion of private-label dermatological lines by major pharmacy chains, and continued R&D investment in novel glycerin-based transdermal systems.

The Pharmaceutical Glycerin Based Products Market is propelled by a set of quantifiable drivers while simultaneously navigating material constraints that influence capacity planning, pricing strategies, and regulatory timelines.

Driver 1 — Rising Chronic Disease Burden: The global prevalence of chronic conditions requiring continuous pharmacotherapy is a primary growth catalyst. Cardiovascular disease, which underpins demand for angina-related glycerin formulations such as glyceryl trinitrate-based products, affects an estimated 520 million individuals globally. Dermatological disorders affect roughly 1.9 billion people at any given time. These population-level statistics translate directly into sustained volume demand for glycerin-based finished dosage forms across multiple therapeutic categories.

Driver 2 — Expanding Pharmaceutical Manufacturing in Emerging Markets: Asia Pacific pharmaceutical production output grew at approximately 8–9% annually over the prior five-year period, with China and India serving as primary glycerin-based product manufacturing hubs. This regional industrialization drives both domestic consumption and export-oriented production, supporting global market volume growth.

Driver 3 — OTC Market Expansion: Globally, OTC pharmaceutical sales surpassed $170 billion in recent years, with cough remedies and dermatological preparations among the highest-volume categories. Glycerin-based OTC products benefit disproportionately from this expansion, as regulatory barriers for reformulation and market entry are lower than for prescription drugs.

Constraint 1 — Raw Material Price Volatility: Crude glycerin, a byproduct of biodiesel and oleochemical production, is subject to significant price swings tied to energy markets and vegetable oil commodity cycles. Price spikes of 15–25% within single calendar years have historically compressed margins for pharmaceutical-grade glycerin refiners and downstream formulators.

Constraint 2 — Stringent Pharmacopeial Standards: Compliance with USP, EP, and JP purity specifications for pharmaceutical-grade glycerin requires capital-intensive refining and quality assurance infrastructure, limiting supplier diversity and increasing production costs for smaller market participants.

The competitive landscape of the Pharmaceutical Glycerin Based Products Market is characterized by a mix of vertically integrated pharmaceutical conglomerates, specialty excipient manufacturers, and oleochemical-to-pharmaceutical value chain players. Key competitors are profiled below:

dupoint: A leading materials science corporation with significant exposure to specialty chemical inputs used in pharmaceutical formulation; its glycerin-related product streams feed into high-purity excipient applications across multiple dosage form categories.

AbbVie Inc: A global biopharmaceutical leader with a strong dermatology and immunology portfolio; AbbVie leverages glycerin-based delivery vehicles in its topical and ophthalmic formulation pipelines, capitalizing on its robust R&D and regulatory infrastructure.

Johnson and Johnson: A diversified healthcare giant with consumer, pharmaceutical, and medical device divisions; its consumer health segment is a major producer of glycerin-containing dermatological and personal care products sold across global retail and pharmacy channels.

Takeda Pharmaceutical Company Ltd: A Japan-headquartered global pharmaceutical company with therapeutic focus areas including gastroenterology and rare diseases; Takeda utilizes glycerin-based excipients in oral and topical drug formulations across its broad product portfolio.

Abbott Laboratories: A diversified healthcare and diagnostics company that incorporates pharmaceutical-grade glycerin in select nutritional and pharmaceutical product lines, leveraging its global manufacturing and distribution network.

The Dow Chemical Company: A major chemical manufacturer supplying high-purity glycerin and glycerin derivatives to pharmaceutical customers; Dow's integrated oleochemical operations provide cost-competitive feedstock for pharmaceutical-grade glycerin production.

Bausch Health Companies Inc.: A specialty pharmaceutical company with concentrated exposure to dermatology, ophthalmology, and gastroenterology; Bausch is among the most direct competitors in glycerin-based ophthalmic and dermatological finished dosage forms.

Emery Oleochemicals: A global producer of natural-based chemicals including pharmaceutical-grade glycerin; Emery supplies refined glycerin to drug manufacturers and excipient compounders across North America, Europe, and Asia Pacific.

Capsugel: A leader in drug delivery systems and encapsulation technologies; Capsugel uses glycerin as a key plasticizer in softgel capsule manufacturing, making it a significant industrial consumer of pharmaceutical-grade glycerin.

Croda International plc: A specialty chemicals company providing high-performance excipients and active ingredients to pharmaceutical formulators; Croda's glycerin-derived product lines support advanced topical, ophthalmic, and parenteral drug delivery systems.

January 2024: AbbVie Inc announced the expansion of its dermatological formulation pipeline with new glycerin-based biologic vehicle platforms intended for enhanced skin penetration in immunodermatology indications, targeting regulatory submission by late 2025.

March 2024: Croda International plc launched a new series of ultra-high-purity glycerin excipients certified to meet both USP and EP monograph specifications, targeting ophthalmic and parenteral drug manufacturers seeking reduced endotoxin burden.

June 2024: Emery Oleochemicals completed a capacity expansion at its Malaysian glycerin refining facility, adding 15,000 metric tons per year of pharmaceutical-grade glycerin output to address growing Asia Pacific demand.

August 2024: Capsugel (a Lonza company) filed a patent application related to novel glycerin-plasticized softgel formulations exhibiting improved dissolution profiles for poorly water-soluble active pharmaceutical ingredients.

October 2024: The European Medicines Agency (EMA) released updated guidance on glycerin excipient testing requirements for injectable and ophthalmic pharmaceutical products, with mandatory compliance timelines beginning Q1 2026.

December 2024: Johnson and Johnson's consumer health division received regulatory approval in India for an expanded glycerin-based dermatological moisturizer line, marking entry into the medical-grade OTC moisturizer segment in a key emerging market.

February 2025: The Dow Chemical Company announced a strategic supply agreement with a major European pharmaceutical contract manufacturer to provide pharmaceutical-grade glycerin under long-term fixed-price contracts, mitigating volatility risk for both parties.

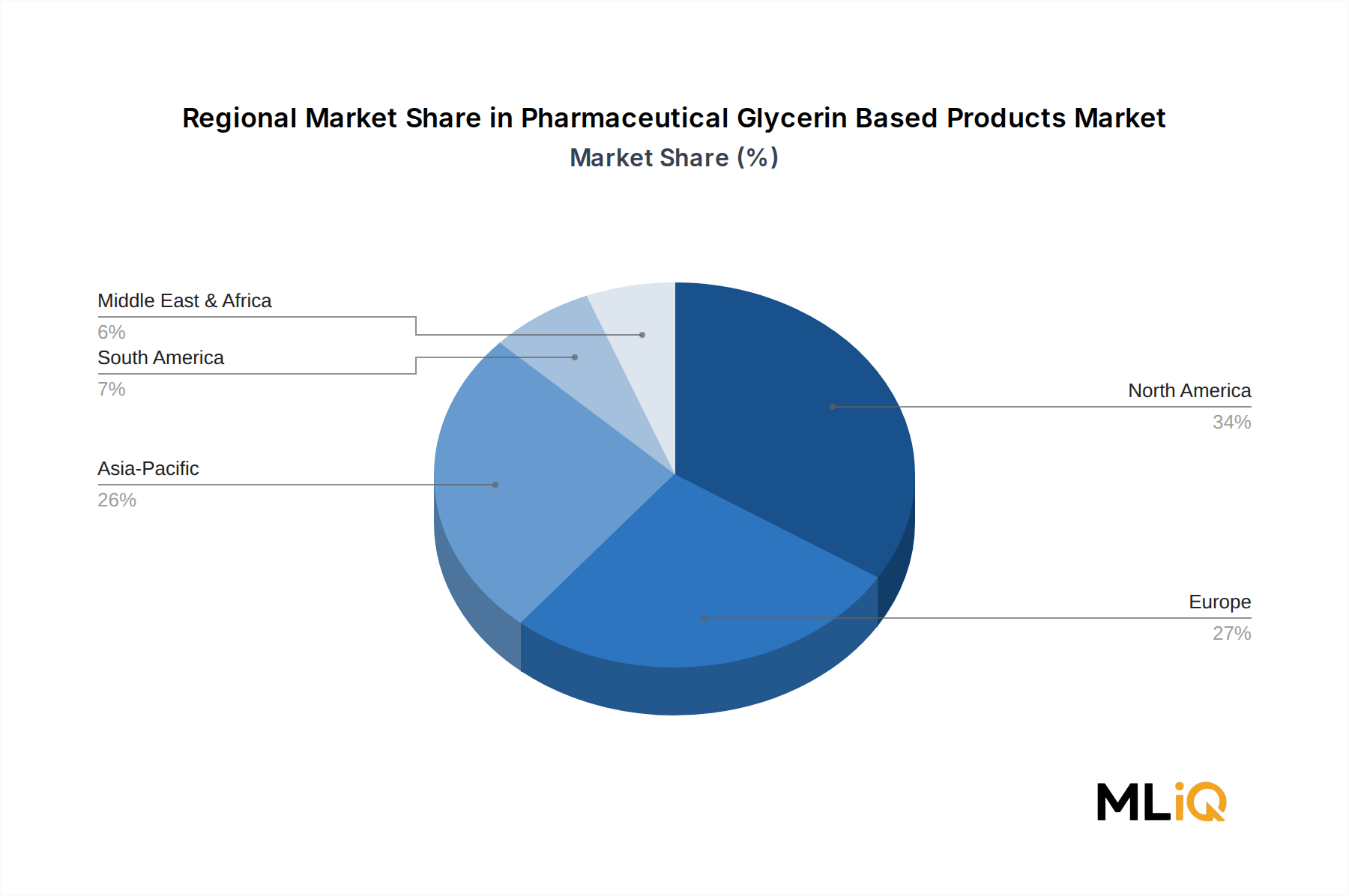

Regional dynamics within the Pharmaceutical Glycerin Based Products Market reflect divergent growth trajectories shaped by healthcare infrastructure maturity, regulatory environments, and demographic profiles.

North America represents the most mature and highest-revenue region, accounting for an estimated 32–34% of total global market value. The United States anchors this position through its large branded pharmaceutical sector, extensive OTC distribution networks, and high per-capita consumption of dermatological and ophthalmic glycerin-based products. Canada and Mexico contribute incrementally, with Mexico emerging as a nearshoring hub for pharmaceutical manufacturing. The North American market is growing at approximately 4.5–5.0% CAGR, below the global average, reflecting market saturation in core product categories.

Europe constitutes the second-largest regional market, holding approximately 26–28% of global revenue. Germany, France, the United Kingdom, and Italy are the primary national markets, supported by strong generics industries, well-developed pharmacovigilance frameworks, and robust hospital procurement systems. European demand is driven by aging demographics and high chronic disease prevalence. The regional CAGR is estimated at 4.8–5.2%, with Nordics and Benelux showing stronger growth tied to premium pharmaceutical formulation activity.

Asia Pacific is the fastest-growing region, projected to expand at a CAGR of 7.5–8.5% through 2033. China and India dominate regional volume on the back of large domestic pharmaceutical manufacturing bases, expanding healthcare access programs, and rising middle-class health expenditure. South Korea, Japan, and ASEAN markets contribute through specialty pharmaceutical and cosmeceutical demand. The region's share of global market value is expected to increase from approximately 24% to over 30% by the end of the forecast period.

The Middle East & Africa region, while currently representing approximately 6–7% of global market value, is gaining momentum driven by Gulf Cooperation Council healthcare infrastructure investments and South Africa's growing pharmaceutical retail sector. Turkey and Israel serve as regional pharmaceutical manufacturing and export centers. Regional CAGR is estimated at 6.0–6.5%.

South America accounts for roughly 5–6% of global revenue, with Brazil and Argentina as dominant markets. Healthcare reform initiatives and domestic pharmaceutical production incentives in Brazil are the primary regional growth catalysts, supporting a CAGR of approximately 5.5–6.0% for the region.

Technological innovation within the Pharmaceutical Glycerin Based Products Market is reshaping formulation science, manufacturing efficiency, and product performance across all major drug type segments.

The first major disruptive technology trajectory is the development of nanostructured glycerin-based drug delivery systems. Nanoemulsions, nanosuspensions, and glycerin-based lipid nanoparticles are enabling enhanced bioavailability for poorly soluble active pharmaceutical ingredients, particularly in dermatological and ophthalmic applications. Adoption of nanodelivery platforms is accelerating, with R&D investment in lipid nanoparticle technology surpassing $2 billion globally in recent years following the validation of the modality through mRNA vaccine applications. For glycerin-based product manufacturers, nanoformulation capability is rapidly transitioning from a differentiator to a competitive necessity in specialty dermatological and ophthalmic segments.

The second disruptive technology is continuous manufacturing (CM) as applied to glycerin-based solid and semi-solid dosage forms. Traditional batch manufacturing of glycerin-containing creams, ointments, and suppositories is being displaced by continuous processing lines that offer tighter process control, reduced batch-to-batch variability, and lower overall cost of goods. Regulatory agencies including the FDA have actively encouraged CM adoption, and capital investment in CM infrastructure among top-tier pharmaceutical manufacturers exceeded $500 million annually in the 2022–2024 period. Incumbent batch-manufacturing operations face margin pressure as CM-equipped competitors achieve superior yield and quality metrics. \

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.9% from 2020-2034 |

| Segmentation |

|

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Comprehensive validation mechanisms ensuring market intelligence accuracy, reliability, and adherence to international standards.

500+ data sources cross-validated

200+ industry specialists validation

NAICS, SIC, ISIC, TRBC standards

Continuous market tracking updates

Factors such as are projected to boost the Pharmaceutical Glycerin Based Products Market market expansion.

Key companies in the market include dupoint, AbbVie Inc, Johnson and Johnson, Takeda Pharmaceutical Company Ltd, Abbott Laboratories, The Dow Chemical Company, Bausch Health Companies Inc., Takeda Pharmaceutical Company, Emery Oleochemicals, Capsugel, Croda International plc.

The market segments include Drug Type.

The market size is estimated to be USD 46.08 billion as of 2022.

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3456, USD 5769, and USD 10995 respectively.

The market size is provided in terms of value, measured in billion and volume, measured in .

Yes, the market keyword associated with the report is "Pharmaceutical Glycerin Based Products Market," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Pharmaceutical Glycerin Based Products Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.