1. What are the major growth drivers for the Scar Treatment Market market?

Factors such as are projected to boost the Scar Treatment Market market expansion.

Market Lens IQ is a global market intelligence and strategic consulting firm delivering advanced syndicated research reports, customized industry analysis, competitive intelligence, and data-driven advisory solutions to organizations across international markets. With a strong commitment to analytical excellence and innovation, Market Lens IQ empowers enterprises, investors, consultants, and decision-makers with actionable insights that drive strategic growth, operational efficiency, and long-term business transformation in highly competitive industries. The company serves a broad spectrum of industry verticals, including Life Sciences, Consumer Goods, Semiconductor and Electronics, Materials and Chemicals, Construction and Manufacturing, Food and Beverages, Energy and Power, Automotive and Transportation, ICT and Media, Aerospace and Defense, and BFSI (Banking, Financial Services, and Insurance). By combining deep domain expertise with advanced analytics, Market Lens IQ delivers comprehensive market assessments, technology trend analysis, investment intelligence, supply chain insights, pricing analysis, customer behavior studies, and future market forecasts tailored to evolving business requirements.

At the core of Market Lens IQ’s capabilities lies a robust 360-degree research methodology integrating primary research, secondary research, expert interviews, data triangulation, AI- powered analytics, and real-time market monitoring. Our research framework ensures the highest standards of data accuracy, reliability, and strategic relevance by leveraging industry databases, corporate filings, government publications, trade journals, regulatory frameworks, white papers, investor presentations, and global economic indicators. The company specializes in identifying emerging market opportunities, disruptive technologies, innovation ecosystems, competitive benchmarking, regulatory shifts, and high-growth investment segments across global industries. Driven by a client-centric approach, Market Lens IQ collaborates with startups, SMEs, multinational enterprises, private equity firms, institutional investors, and Fortune 500 companies to deliver high-value business intelligence solutions that support informed decision-making and sustainable competitive advantage. Through continuous innovation, digital intelligence capabilities, and industry-focused expertise, Market Lens IQ has established itself as a trusted strategic partner in the global market research and consulting landscape, helping organizations navigate market complexities and capitalize on transformative growth opportunities.

+1 2315155523

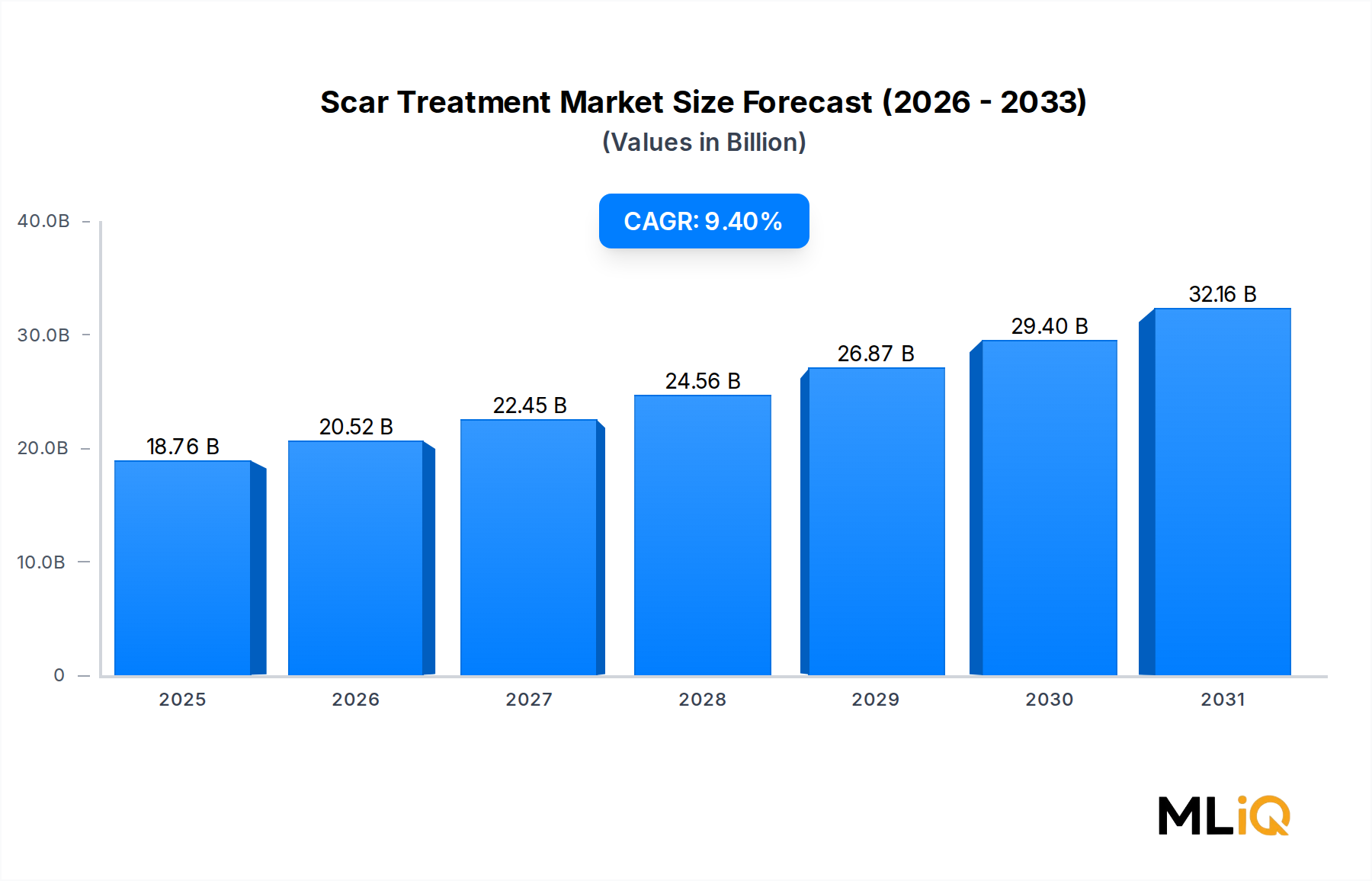

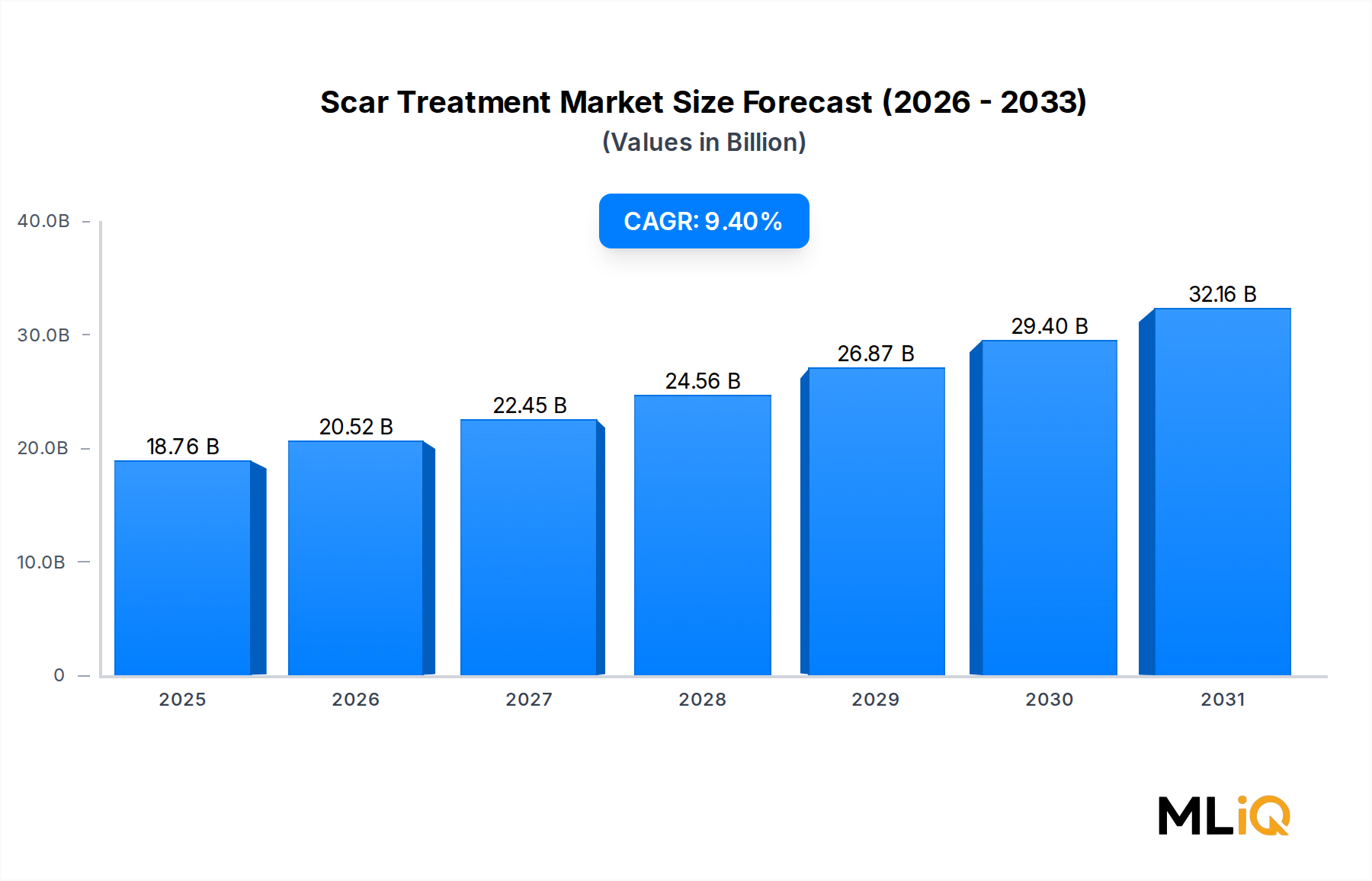

The global scar treatment industry is entering a period of accelerated expansion, driven by rising incidence of surgical procedures, burns, trauma, and a surging consumer appetite for aesthetic improvement. The market was valued at $18.76 billion and is projected to grow at a compound annual growth rate (CAGR) of 9.4% over the forecast horizon, reflecting robust demand across both clinical and home-care settings. These figures position scar therapeutics as one of the most dynamic verticals within the broader life sciences landscape.

Several macro tailwinds are powering this trajectory. Global surgical volumes continue to climb — the World Health Organization estimates over 313 million major surgical procedures are performed annually, each carrying inherent scarring risk. Simultaneously, a cultural shift toward aesthetic self-care has normalized elective scar remediation, dramatically expanding the addressable consumer base beyond traditional clinical indications. The proliferation of minimally invasive cosmetic procedures — growing at double-digit rates in markets such as South Korea, Brazil, and the United States — further amplifies post-procedural scar management demand.

Key demand drivers include technological advances in laser-based platforms, the democratization of topical silicone formulations, and expanding reimbursement frameworks in North America and Western Europe for medically necessary scar revision. The rising prevalence of keloid and hypertrophic scarring among darker skin phenotypes, particularly across Sub-Saharan Africa and South Asia, is opening new geographic frontiers for specialized treatment protocols.

From a product standpoint, the market is bifurcated between topical agents — gels, sheets, and creams — and energy-based devices including fractional CO2 lasers and pulsed dye laser systems. The topical segment commands the largest revenue share due to accessibility and over-the-counter availability, while laser-based treatment is the fastest-growing sub-segment, propelled by falling device costs and increasing aesthetic clinic penetration in emerging economies.

End-user dynamics are equally instructive. Hospitals remain the primary revenue hub for complex, post-surgical scar management, while clinics are rapidly gaining share through elective aesthetic procedures. The home-care segment — fueled by direct-to-consumer e-commerce platforms and telehealth consultations — represents the most disruptive growth vector over the medium term.

Looking ahead, pipeline innovation in biologics, autologous cell therapies, and combination treatment regimens (pairing pharmacological and energy-based modalities) is expected to redefine clinical outcomes and create premium pricing tiers. Strategic partnerships between device manufacturers and pharmaceutical companies are already reshaping the competitive landscape, setting the stage for a market that could substantially exceed its current valuation by the end of the decade.

Among all product categories within the scar treatment industry, topical formulations consistently capture the largest share of global revenues. This dominance is attributable to a confluence of factors: widespread over-the-counter availability, physician recommendation rates, cost-effectiveness relative to procedural alternatives, and the ease of self-administration across diverse patient populations. Topical agents encompass silicone gels, silicone sheets, corticosteroid creams, onion extract gels, retinoid formulations, and combination products — each targeting distinct scar morphologies and patient demographics.

Silicone-based topical products represent the clinical gold standard, endorsed by the International Advisory Panel on Scar Management and supported by decades of randomized controlled trial data demonstrating efficacy in reducing scar height, erythema, and pruritus. The mechanism — sustained hydration and occlusion of the stratum corneum — is both clinically validated and patient-tolerated, contributing to superior adherence rates versus procedural interventions requiring clinic visits.

The emergence of advanced gel formulations incorporating active pharmaceutical ingredients such as heparin, allantoin, and vitamin E has further differentiated the topical segment. These combination products command price premiums of 20–35% over single-ingredient silicone gels, supporting improved margin structures for innovator brands. Importantly, formulation innovation has enabled manufacturers to target specific scar subtypes: atrophic scars from acne are increasingly treated with retinoid-infused topicals, while hypertrophic and keloid lesions respond better to corticosteroid-impregnated silicone systems.

From a competitive standpoint, key players driving topical segment revenues include Mölnlycke Health Care AB, whose Mepiform and Mepitac silicone product lines are widely distributed across hospital and retail channels, and hra pharma, which markets the Kelo-cote brand — one of the most clinically referenced silicone gel products globally. Smith and Nephew plc. leverages its Cica-Care silicone gel sheeting across both institutional and consumer markets, benefiting from a strong distributor network in North America and Europe.

The market is also witnessing aggressive entry by private-label and generic manufacturers, particularly from India and China, where regulatory frameworks permit faster market authorization for topical scar products. This competitive pressure is compressing average selling prices in value segments while simultaneously expanding market volume — a dynamic that sustains top-line growth even as per-unit economics soften for incumbent brands.

Retail pharmacy chains and e-commerce platforms have become critical distribution channels for topical scar products. Online sales of over-the-counter scar gels grew at an estimated 18–22% annually in the post-pandemic period, as consumers increasingly self-diagnose and self-treat minor scarring without clinical consultation. This trend is particularly pronounced in the Asia Pacific region, where mobile-first commerce and social media-driven beauty awareness converge to accelerate consumer adoption.

Home-care adoption is further reinforced by dermatologists prescribing topical regimens as adjunct therapy following laser or surgical procedures, creating a recurring-use demand pattern that drives customer lifetime value for branded product companies. The segment's dominance is, therefore, both structural and self-reinforcing, underpinned by clinical validation, distribution breadth, price accessibility, and innovation momentum that collectively position topical treatments as the enduring revenue anchor of the scar treatment industry.

The scar treatment industry is governed by a set of powerful demand accelerators and equally material structural constraints that any rigorous market analysis must quantify.

On the driver side, the global burden of burn injuries alone creates a substantial treatment funnel. The World Health Organization estimates approximately 180,000 deaths annually from burns, with non-fatal burn injuries numbering in the tens of millions — each case generating downstream demand for scar management products. Burn survivors, particularly those with contracture scarring, require multi-year, multi-modality treatment plans, representing high-lifetime-value patients for healthcare providers and manufacturers alike.

The global cosmetic surgery market — a direct feeder segment — surpassed $50 billion in value in recent years and continues to grow at approximately 7–8% annually. Post-surgical scarring is virtually universal, and a growing proportion of patients proactively seek scar treatment, expanding the addressable population beyond reactive clinical need. The normalization of aesthetic procedures among millennials and Gen Z demographics is a particularly durable structural tailwind.

Technology-driven drivers are also significant. The unit cost of fractional laser platforms has declined by an estimated 30–40% over the past decade, democratizing access for tier-2 aesthetic clinics and enabling broader patient reach. This aligns with the rapid expansion of aesthetic clinic networks in India, China, Brazil, and Turkey.

On the constraint side, reimbursement limitations remain a critical barrier. In most markets, scar treatments classified as aesthetic rather than medically necessary are excluded from public and private insurance coverage, forcing out-of-pocket expenditure that suppresses adoption in price-sensitive demographics. In the United States, the lack of FDA-approved indications for several widely used topical formulations limits prescriber confidence and restricts direct-to-physician marketing.

Product safety concerns — including steroid atrophy from corticosteroid injections and the risk of post-inflammatory hyperpigmentation following aggressive laser resurfacing — continue to create patient hesitancy, particularly among underrepresented skin types. Adverse event rates in darker Fitzpatrick skin types remain a clinical challenge that constrains laser adoption in Africa, South Asia, and the Middle East.

The competitive landscape of the scar treatment industry is moderately consolidated at the premium tier but highly fragmented among generic and regional players. Below is a structured profile of leading participants:

Bausch Health Companies Inc.: A diversified specialty pharmaceutical company with significant dermatology assets, Bausch Health leverages its established prescriber relationships and retail pharmacy distribution network to maintain strong positioning in topical scar management categories across North America.

Avita Medical Limited: Specializing in autologous cell harvesting and regenerative skin solutions, Avita Medical's RECELL system represents a frontier approach to severe burn and traumatic wound scarring, with expanding FDA-cleared indications that differentiate it from conventional scar treatment modalities.

Cynosure, Inc.: A leading aesthetic device manufacturer, Cynosure markets a portfolio of laser and light-based platforms including fractional CO2 and pulsed dye laser systems that are widely deployed in clinical settings for atrophic, hypertrophic, and post-surgical scar revision.

sisram inc: Operating as the medical aesthetics arm of Fosun Pharma, sisram inc (Alma Lasers) develops and distributes advanced energy-based platforms for scar treatment across Asia Pacific and emerging markets, with growing penetration in European aesthetic clinics.

Mölnlycke Health Care AB: A global leader in advanced wound care and surgical products, Mölnlycke Health Care AB commands strong institutional market share through its silicone-based scar management product lines distributed across hospital systems in over 90 countries.

Sientra, Inc.: Primarily known for its breast implant portfolio, Sientra, Inc. participates in the broader aesthetic reconstruction market, addressing post-mastectomy and post-surgical scarring through partnerships with reconstructive surgery centers.

Smith and Nephew plc.: A diversified medical technology company, Smith and Nephew plc. maintains a dedicated wound management division that markets silicone gel sheeting and advanced dressings for post-operative and burn scar management across global healthcare systems.

Polytech Health & Aesthetics GmbH: A German-based specialty manufacturer focused on silicone implants and aesthetic solutions, Polytech Health & Aesthetics GmbH serves the European reconstructive surgery market with products that intersect with post-surgical scar management protocols.

hra pharma: A European consumer healthcare specialist, hra pharma is the brand owner of the Kelo-cote silicone gel franchise, one of the most extensively studied and clinically referenced topical scar management products available globally in both OTC and prescription channels.

January 2024: Avita Medical Limited received expanded FDA clearance for the RECELL GO system in acute burn wound management, broadening the clinical indication scope and reinforcing the company's leadership in regenerative scar prevention strategies.

March 2024: Cynosure, Inc. announced the commercial launch of its next-generation fractional laser platform in the European Union market, targeting aesthetic clinics with enhanced pulse modulation technology designed to reduce adverse events in darker skin phototypes — a historically underserved patient population.

May 2024: Mölnlycke Health Care AB entered into a distribution agreement with a leading Asia Pacific healthcare logistics company to expand availability of its silicone scar management portfolio across Southeast Asian hospital networks, targeting markets including Indonesia, Vietnam, and Thailand.

August 2024: Smith and Nephew plc. published Phase III clinical trial results demonstrating statistically significant improvement in Vancouver Scar Scale scores for patients using its next-generation silicone gel sheeting versus standard-of-care controls — data intended to support reimbursement submissions in key European markets.

October 2024: sisram inc announced a strategic partnership with a South Korean aesthetic clinic chain to co-market energy-based scar treatment protocols integrating Alma Lasers platforms with proprietary topical adjunct therapies.

February 2025: hra pharma expanded its Kelo-cote product line with the launch of a sunscreen-integrated scar gel formulation in the United Kingdom and Germany, addressing patient demand for combined UV protection and scar management in a single-step application.

The global scar treatment industry exhibits pronounced regional heterogeneity in both market maturity and growth velocity, shaped by healthcare infrastructure, demographic profiles, and cultural attitudes toward aesthetic intervention.

North America is the most mature regional market, accounting for an estimated 38–42% of global revenue. The United States anchors this dominance through high surgical volumes — approximately 50 million outpatient surgical procedures annually — a well-developed aesthetic clinic ecosystem, and above-average consumer spending on dermatological care. Canada and Mexico contribute incremental volumes, with Mexico emerging as a medical tourism hub for cost-sensitive scar revision procedures. The regional CAGR is estimated at 7.8%, reflecting market saturation in premium product categories partially offset by innovation-driven premiumization.

Europe represents the second-largest regional revenue pool, capturing approximately 28–30% of global market value. Germany, the United Kingdom, and France are the primary revenue contributors, supported by robust public healthcare systems that reimburse post-surgical and burn scar treatments under medically necessary criteria. The Nordics and Benelux sub-regions exhibit above-average adoption of advanced laser-based scar platforms. European regional CAGR is projected at approximately 8.2%, driven by expanding aesthetic medicine reimbursement and medical device innovation originating from German and French manufacturers.

Asia Pacific is the fastest-growing regional market, with a projected CAGR of 12.1–13.5%, powered by rapid urbanization, rising disposable incomes, and an intensely competitive aesthetic medicine sector particularly in China, South Korea, India, and Japan. South Korea's position as a global aesthetic medicine leader drives disproportionate per-capita spending on scar remediation, while China's enormous patient population and accelerating domestic medical device manufacturing capacity create dual demand and supply dynamics favorable to market expansion.

Latin America, led by Brazil and Argentina, exhibits a CAGR of approximately 10.3%, underpinned by Brazil's status as the world's second-largest cosmetic surgery market by procedure volume. The Middle East and Africa region, while currently representing a smaller absolute revenue share, is growing rapidly — particularly in GCC states and Turkey — fueled by medical tourism, high aesthetic procedure adoption rates, and increasing investment in private dermatology clinic infrastructure.

The upstream supply architecture of the scar treatment industry is anchored by a relatively concentrated set of specialty raw materials, each carrying distinct sourcing risk profiles that manufacturers must actively manage.

Medical-grade silicone is the most strategically critical input, underpinning the dominant topical segment as well as gel sheets and implant-adjacent scar management products. Global supply of medical-grade polydimethylsiloxane (PDMS) is concentrated among a handful of multinational chemical producers including Dow Corning (now integrated into Dow Inc.), Momentive Performance Materials, and Wacker Chemie AG. Supply tightness in medical-grade silicone feedstocks emerged prominently during 2021–2022 as pandemic-era industrial disruptions intersected with surging demand from multiple end markets including semiconductors, healthcare, and consumer electronics. Scar treatment manufacturers reported lead time extensions of 8–14 weeks during this period, prompting strategic safety stock accumulation and dual-sourcing initiatives.

Hyaluronic acid, used in injectable scar treatment formulations and combination topical products, represents another key upstream dependency. Production is concentrated in China, with Bloomage Biotechnology and Fufeng Group controlling substantial global output. Price volatility in pharmaceutical-grade hyaluronic acid has historically tracked fermentation feedstock costs (primarily glucose and corn starch), creating exposure to agricultural commodity cycles. The Hyaluronic Acid Market dynamics directly influence formulation costs for injectable and biopolymer-enhanced scar treatment products.

Active pharmaceutical ingredients (APIs) for corticosteroid-based scar treatments — primarily triamcinolone acetonide — are largely manufactured in India and China. Geopolitical supply chain diversification pressures post-pandemic have prompted European and North

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 9.4% from 2020-2034 |

| Segmentation |

|

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Comprehensive validation mechanisms ensuring market intelligence accuracy, reliability, and adherence to international standards.

500+ data sources cross-validated

200+ industry specialists validation

NAICS, SIC, ISIC, TRBC standards

Continuous market tracking updates

Factors such as are projected to boost the Scar Treatment Market market expansion.

Key companies in the market include Bausch Health Companies Inc., Avita Medical Limited, Cynosure, Inc., sisram inc, Mölnlycke Health Care AB, Sientra, Inc., Smith and Nephew plc., Polytech Health & Aesthetics GmbH, hra pharma.

The market segments include Scar Type, Product, End User.

The market size is estimated to be USD 18.76 billion as of 2022.

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3456, USD 5769, and USD 10995 respectively.

The market size is provided in terms of value, measured in billion and volume, measured in .

Yes, the market keyword associated with the report is "Scar Treatment Market," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Scar Treatment Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.