1. What are the major growth drivers for the Needle-Free Injection Systems Market market?

Factors such as are projected to boost the Needle-Free Injection Systems Market market expansion.

Market Lens IQ is a global market intelligence and strategic consulting firm delivering advanced syndicated research reports, customized industry analysis, competitive intelligence, and data-driven advisory solutions to organizations across international markets. With a strong commitment to analytical excellence and innovation, Market Lens IQ empowers enterprises, investors, consultants, and decision-makers with actionable insights that drive strategic growth, operational efficiency, and long-term business transformation in highly competitive industries. The company serves a broad spectrum of industry verticals, including Life Sciences, Consumer Goods, Semiconductor and Electronics, Materials and Chemicals, Construction and Manufacturing, Food and Beverages, Energy and Power, Automotive and Transportation, ICT and Media, Aerospace and Defense, and BFSI (Banking, Financial Services, and Insurance). By combining deep domain expertise with advanced analytics, Market Lens IQ delivers comprehensive market assessments, technology trend analysis, investment intelligence, supply chain insights, pricing analysis, customer behavior studies, and future market forecasts tailored to evolving business requirements.

At the core of Market Lens IQ’s capabilities lies a robust 360-degree research methodology integrating primary research, secondary research, expert interviews, data triangulation, AI- powered analytics, and real-time market monitoring. Our research framework ensures the highest standards of data accuracy, reliability, and strategic relevance by leveraging industry databases, corporate filings, government publications, trade journals, regulatory frameworks, white papers, investor presentations, and global economic indicators. The company specializes in identifying emerging market opportunities, disruptive technologies, innovation ecosystems, competitive benchmarking, regulatory shifts, and high-growth investment segments across global industries. Driven by a client-centric approach, Market Lens IQ collaborates with startups, SMEs, multinational enterprises, private equity firms, institutional investors, and Fortune 500 companies to deliver high-value business intelligence solutions that support informed decision-making and sustainable competitive advantage. Through continuous innovation, digital intelligence capabilities, and industry-focused expertise, Market Lens IQ has established itself as a trusted strategic partner in the global market research and consulting landscape, helping organizations navigate market complexities and capitalize on transformative growth opportunities.

Needle-Free Injection Systems Market

Needle-Free Injection Systems Market+1 2315155523

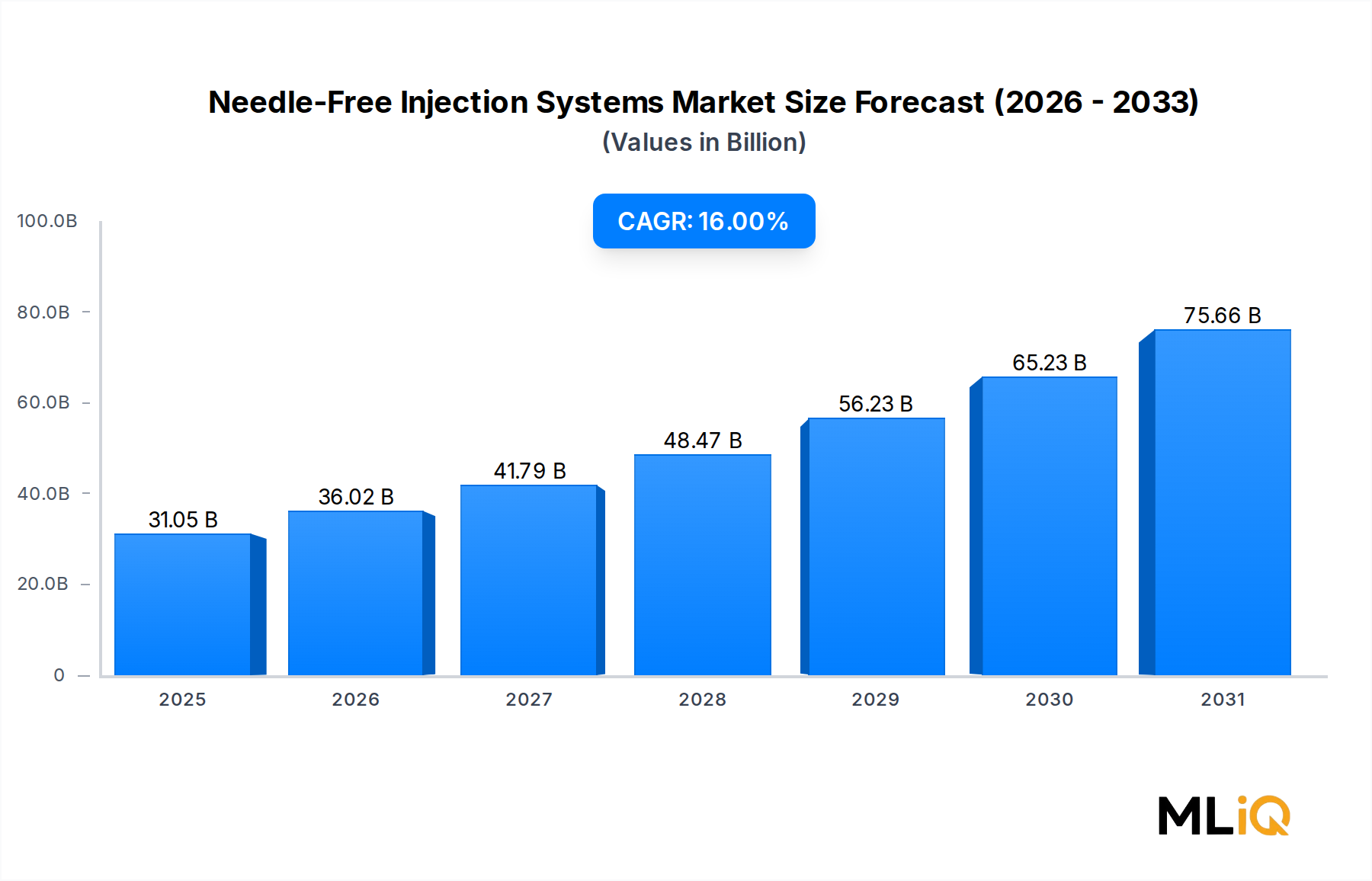

The global Needle-Free Injection Systems Market is poised for exceptional expansion, registering a compound annual growth rate (CAGR) of 16.0% over the forecast period. The market was valued at approximately $31,054.98 million and is expected to sustain robust momentum driven by accelerating adoption across vaccine delivery, insulin administration, and pain management applications. This trajectory positions needle-free technology as one of the most dynamically evolving segments within the broader Life Sciences sector.

Several macro-level forces underpin this growth. The global burden of needle-stick injuries — estimated at over 1 million incidents annually in healthcare settings worldwide — has intensified the urgency for safer drug delivery alternatives. Regulatory bodies including the U.S. FDA and the European Medicines Agency have progressively supported needle-free alternatives as part of broader occupational health mandates. In parallel, the global vaccination drive accelerated during and post the COVID-19 pandemic has unlocked large-scale demand for high-throughput, pain-free immunization technologies, particularly in low- and middle-income countries where cold-chain constraints and trained personnel shortages make conventional injections logistically complex.

On the demand side, the proliferation of biologics and biosimilars — which require precise subcutaneous or intramuscular delivery — is pushing pharmaceutical manufacturers to seek delivery platforms that preserve drug efficacy while improving patient adherence. Needle-free systems have demonstrated clinical equivalence with conventional hypodermic injections for multiple therapeutic classes, including vaccines, hormones, and analgesics, lending them increasing clinical credibility.

The home care segment is emerging as a critical growth frontier. As chronic disease management increasingly migrates from hospital settings to patient self-administration environments, needle-free devices offer an ergonomic and psychologically less aversive alternative. Patients managing diabetes, multiple sclerosis, and rheumatoid arthritis represent a significant and captive addressable base for next-generation needle-free platforms.

The competitive landscape is maturing, with established players investing heavily in platform diversification and geographic expansion. Emerging markets in Asia Pacific and Latin America represent the fastest-growing demand pools, supported by expanding healthcare infrastructure and government immunization programs. Meanwhile, North America continues to command the largest absolute revenue share, buoyed by premium pricing, high insurance coverage, and early technology adoption.

Looking ahead, convergence between digital health ecosystems and needle-free delivery — including connected injectors with dose-tracking capabilities — is expected to further elevate market value and differentiate product offerings in an increasingly competitive landscape.

Among all application segments, vaccine delivery represents the single largest revenue contributor within the Needle-Free Injection Systems Market, and its dominance is both structurally entrenched and accelerating. The segment's primacy stems from a confluence of public health imperatives, favorable regulatory pathways, and scalable deployment models — particularly in mass immunization campaigns where operational efficiency is paramount.

The economics of vaccine delivery are compelling for needle-free technology. In high-volume immunization environments — such as national vaccination drives or military inoculation programs — needle-free jet injectors can administer up to 1,000 doses per device per day, dramatically reducing per-dose delivery costs compared to conventional syringe-based methods. This throughput advantage has made needle-free systems the technology of choice for agencies such as the World Health Organization (WHO) and UNICEF for campaigns targeting measles, polio, influenza, and hepatitis B across endemic regions.

The COVID-19 pandemic served as a powerful validation event. The unprecedented logistical demands of vaccinating billions of individuals in compressed timeframes exposed the operational limitations of conventional needle-and-syringe delivery, catalyzing investment in needle-free alternatives. Several national governments and global health organizations fast-tracked procurement of needle-free jet injectors, creating a durable installed base that will support recurring demand for consumables and replacement devices.

From a product architecture perspective, vaccine delivery applications predominantly utilize liquid-based needle-free systems — specifically spring-based and gas-propelled injectors — capable of delivering precise antigen volumes transdermally or intramuscularly without skin puncture. These systems achieve bioavailability profiles comparable to intramuscular injections, a critical requirement given the immunogenicity sensitivity of many vaccine formulations.

Key players active in this segment include PharmaJet, which has established strategic partnerships with global health agencies for its Stratis needle-free injector, an FDA-cleared device validated for flu, polio, and other vaccines. CROSSJECT NEEDLE FREE INJECTION SYSTEMS has similarly advanced auto-injector platforms targeting emergency vaccine administration scenarios. Medical International Technology, Inc. has a long-standing presence in multi-dose vaccine delivery for public health programs.

The segment's revenue share is not only substantial but expanding. Emerging economies in Sub-Saharan Africa, South Asia, and Southeast Asia are scaling national immunization programs with international donor support, and needle-free injection systems are increasingly specified in procurement tenders due to their safety profile and reduced biohazardous waste generation — a priority in healthcare systems with limited sharps disposal infrastructure.

A notable trend is the integration of prefilled cartridge technologies with needle-free platforms for vaccine delivery, reducing preparation time and human error in field settings. This aligns the segment with dynamics observed in the Prefilled Syringes Market, where prefilled formats are gaining share due to convenience and dose accuracy. The vaccine delivery sub-segment is also benefiting from advancements in thermostable vaccine formulations that extend shelf life, further reinforcing the operational case for needle-free delivery in resource-constrained environments.

Looking forward, the segment is expected to maintain its revenue leadership as booster dose campaigns, pandemic preparedness stockpiling, and novel vaccine platforms — including mRNA-based therapies — create sustained procurement demand.

The Needle-Free Injection Systems Market is shaped by a set of well-defined structural drivers and a parallel set of adoption constraints that modulate its growth trajectory.

Driver 1: Needle-Stick Injury Burden. The WHO estimates that approximately 16 billion injections are administered globally each year, with healthcare workers sustaining over 1 million needle-stick injuries annually. These injuries carry significant risk of transmitting bloodborne pathogens including HIV, Hepatitis B, and Hepatitis C. Occupational safety mandates in the U.S. (OSHA Bloodborne Pathogens Standard) and the EU (Directive 2010/32/EU on prevention of sharps injuries) are compelling healthcare providers to transition toward safer delivery alternatives, including needle-free systems.

Driver 2: Rising Prevalence of Chronic Diseases. The International Diabetes Federation reports over 537 million adults living with diabetes globally as of recent estimates, a figure projected to exceed 780 million by 2045. The insulin delivery segment — a primary application within the Needle-Free Injection Systems Market — directly benefits from this epidemiological expansion. Self-injection fatigue and needle phobia, affecting an estimated 10% of the global population, further elevate demand for needle-free alternatives.

Driver 3: Biologics and Biosimilars Pipeline Expansion. As of 2024, the global biologics pipeline comprised over 7,000 molecules in various clinical stages, many requiring subcutaneous delivery. Needle-free platforms offer formulation-compatible delivery for protein-based therapeutics, expanding addressable market scope. This intersects with growth dynamics in the Biologics Drug Delivery Market, where delivery innovation is a key competitive differentiator.

Constraint 1: High Device Cost. Needle-free injector systems carry significantly higher upfront costs relative to conventional syringes — often 5x to 15x the per-unit price — limiting adoption in price-sensitive markets and budget-constrained healthcare systems without subsidy mechanisms.

Constraint 2: Limited Formulary Compatibility. Not all drug formulations are compatible with needle-free delivery; high-viscosity biologics and certain lyophilized compounds require reformulation, adding development cost and timeline risk for pharmaceutical sponsors.

Constraint 3: Regulatory Complexity. Device-drug combination classifications under FDA 21 CFR Part 3 and EMA guidance introduce multi-agency review pathways that extend time-to-market and increase compliance expenditure.

The competitive landscape of the Needle-Free Injection Systems Market is characterized by a mix of dedicated medical device innovators, pharmaceutical delivery specialists, and diversified life sciences companies. Below is a strategic profile of key players:

CROSSJECT NEEDLE FREE INJECTION SYSTEMS: A France-based innovator focused on auto-injector platforms for emergency medicine applications, including convulsive disorders and anaphylaxis. The company's ZENEO platform represents a differentiated needle-free auto-injector with growing clinical validation and regulatory filings across European markets.

PHARMAJET: A U.S.-based company and one of the most commercially prominent needle-free injection system developers for vaccine delivery. PharmaJet's Stratis device is FDA-cleared and WHO-prequalified, enabling deployment through global immunization programs in over 40 countries.

MEDICAL INTERNATIONAL TECHNOLOGY, INC.: A Canadian pioneer in multi-use needle-free injection technology with decades of presence in public health immunization programs. The company supplies devices for both human and veterinary vaccine delivery, giving it a diversified end-market exposure.

ANTARES PHARMA, INC.: A specialty pharmaceutical and delivery technology company with a robust portfolio of needle-free and auto-injector systems. Antares has strategic partnerships with major pharmaceutical firms for device-drug combination products, particularly in the hormone therapy and testosterone replacement space.

VALERITAS HOLDINGS, INC.: Known for its V-Go wearable insulin delivery device, Valeritas brought a unique patch-pump approach to the insulin delivery sub-segment. The company addressed the needs of type 2 diabetes patients seeking simplified, needle-minimized basal-bolus insulin administration.

NATIONAL MEDICAL PRODUCTS, INC.: An established supplier of needle-free injection systems with a focus on clinical and institutional settings. The company maintains a broad product catalog spanning disposable and reusable injector platforms.

THE EUROPEAN PHARMA GROUP: A diversified pharmaceutical services and device distribution entity with operations spanning multiple EU member states. The group has positioned needle-free delivery systems within its specialty drug delivery portfolio targeting hospital and ambulatory care segments.

INJEX PHARMA AG: A German company specializing in needle-free injection systems for insulin delivery and other subcutaneous applications. INJEX's systems are designed for patient self-administration, aligning with the growing home care and chronic disease self-management trends.

Q1 2024: PharmaJet announced expanded procurement agreements with GAVI, the Vaccine Alliance, for deployment of its Stratis needle-free injector in Sub-Saharan African immunization programs, covering measles-rubella and inactivated polio vaccine campaigns.

Q2 2024: CROSSJECT received a positive opinion from European regulatory authorities for its ZENEO midazolam auto-injector, marking a significant milestone in the emergency medicine application of needle-free delivery technology.

Q3 2023: Antares Pharma completed a strategic acquisition that expanded its auto-injector manufacturing capacity, with the stated goal of supporting growing demand from biopharmaceutical partners across oncology and immunology indications.

Q4 2023: The WHO updated its guidance on vaccine delivery best practices, formally recognizing needle-free jet injectors as equivalent delivery systems for selected antigen types — a regulatory endorsement expected to accelerate public-sector procurement globally.

Q1 2023: INJEX Pharma AG launched a next-generation insulin needle-free injector platform in European markets, featuring a redesigned ergonomic housing and improved dose precision mechanism targeting type 1 and type 2 diabetes patient cohorts.

Q2 2023: National Medical Products, Inc. entered into a distribution partnership with a major U.S. group purchasing organization (GPO) to expand hospital formulary access for its disposable needle-free injector product line.

Q3 2022: A peer-reviewed clinical study published in a leading vaccinology journal confirmed bioequivalence between needle-free intradermal delivery and conventional intramuscular injection for influenza vaccines, strengthening the clinical evidence base for market adoption.

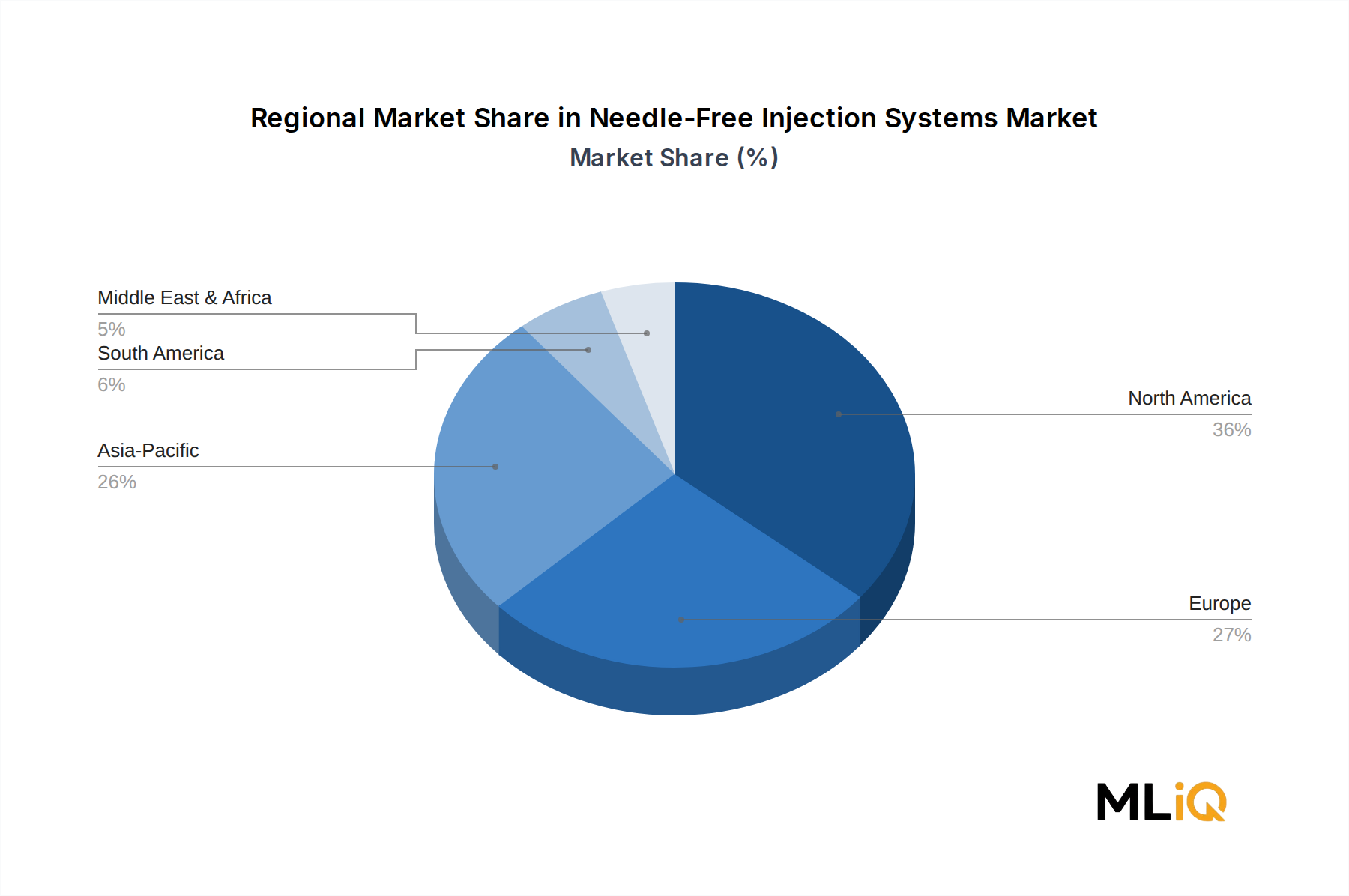

The Needle-Free Injection Systems Market exhibits significant regional heterogeneity in terms of growth velocity, revenue concentration, and demand drivers.

North America commands the largest revenue share of the global Needle-Free Injection Systems Market, accounting for an estimated 38%–42% of total market value. The United States is the primary contributor, supported by high per-capita healthcare expenditure, a mature regulatory framework, and strong adoption of premium drug delivery technologies. The U.S. market benefits from robust private insurance reimbursement coverage and a large installed base of biologic drug users requiring subcutaneous delivery. The regional CAGR is estimated at 13.5%–14.5%, reflecting a more mature but steadily expanding market.

Europe represents the second-largest regional market, with Germany, France, and the United Kingdom as lead contributors. The EU's Directive 2010/32/EU mandating prevention of sharps injuries in healthcare settings has been a structural legislative driver for needle-free adoption across hospital and clinical settings. Europe is also a significant hub for device manufacturing and R&D investment. The regional CAGR is estimated at 12.5%–13.5%.

Asia Pacific is the fastest-growing regional segment, with a projected CAGR of 18.5%–20.0%. China and India collectively represent the dominant demand centers, driven by expanding national immunization programs, a massive diabetic patient population, and government healthcare infrastructure investment. India's Universal Immunization Programme and China's National Health Commission mandates for vaccine delivery modernization are creating significant procurement opportunities for needle-free system providers. ASEAN markets, including Indonesia and Vietnam, are emerging as secondary growth nodes.

The Middle East and Africa region is gaining traction, particularly in GCC countries where healthcare modernization initiatives are funding adoption of advanced delivery technologies, and in Sub-Saharan Africa where global health donor programs are financing needle-free vaccine delivery infrastructure. Regional CAGR is estimated at 15.0%–17.0%.

South America, led by Brazil and Argentina, represents a moderate-growth market with a CAGR of approximately 13.0%–14.0%, where growth is contingent on healthcare budget cycles and international health program disbursements.

The supply chain architecture of the Needle-Free Injection Systems Market spans precision-engineered components, high-grade polymers, elastomeric seals, and electronic sub-assemblies for connected device variants — creating a multi-tiered upstream dependency structure.

Medical-grade polymers — specifically polycarbonate, polypropylene, and high-density polyethylene — constitute the primary structural materials for device housings and cartridge bodies. These materials are sourced from a concentrated group of specialty chemical producers, and their pricing is directly correlated with crude oil price movements. The 2021–2023 commodity cycle saw petrochemical feedstock prices spike by 30%–45%, compressing device manufacturers' input cost margins and prompting supply chain diversification efforts.

Elastomeric components, including silicone rubber seals and plunger stoppers, are critical for ensuring airtight drug containment in prefilled configurations. The silicone supply chain experienced notable tightness during 2021–2022, driven by semiconductor industry competition for the same raw material inputs, resulting in extended lead times for medical device-grade silicone.

Stainless steel — used in spring mechanisms for spring-based injector systems and precision orifice nozzles — has experienced moderate price volatility, with steel indices fluctuating 15%–25% over the 2020–2024 period due to geopolitical disruptions and energy cost escalation in European steel production.

The Needle-Free Injection Systems Market also depends on the Medical Plastics Market for injection-molded sub-components and sterile packaging materials. Disruptions in this upstream segment — such as resin shortages and logistics bottlenecks during the pandemic — cascaded into device production delays. Manufacturers are increasingly responding through dual-sourcing strategies, regional supplier qualification

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 16.0% from 2020-2034 |

| Segmentation |

|

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Comprehensive validation mechanisms ensuring market intelligence accuracy, reliability, and adherence to international standards.

500+ data sources cross-validated

200+ industry specialists validation

NAICS, SIC, ISIC, TRBC standards

Continuous market tracking updates

Factors such as are projected to boost the Needle-Free Injection Systems Market market expansion.

Key companies in the market include CROSSJECT NEEDLE FREE INJECTION SYSTEMS, PHARMAJET, MEDICAL INTERNATIONAL TECHNOLOGY, INC., ANTARES PHARMA, INC., VALERITAS HOLDINGS, INC., NATIONAL MEDICAL PRODUCTS, INC., THE EUROPEAN PHARMA GROUP, INJEX PHARMA AG.

The market segments include Product, Source of Power, Type, Usability, Site of Delivery, Application, End User.

The market size is estimated to be USD 31054.98 million as of 2022.

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3456, USD 5769, and USD 10995 respectively.

The market size is provided in terms of value, measured in million and volume, measured in .

Yes, the market keyword associated with the report is "Needle-Free Injection Systems Market," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Needle-Free Injection Systems Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.