1. What are the major growth drivers for the Orthodontic Equipment and Consumables Market market?

Factors such as are projected to boost the Orthodontic Equipment and Consumables Market market expansion.

Orthodontic Equipment and Consumables Market

Orthodontic Equipment and Consumables Market

Market Lens IQ is a global market intelligence and strategic consulting firm delivering advanced syndicated research reports, customized industry analysis, competitive intelligence, and data-driven advisory solutions to organizations across international markets. With a strong commitment to analytical excellence and innovation, Market Lens IQ empowers enterprises, investors, consultants, and decision-makers with actionable insights that drive strategic growth, operational efficiency, and long-term business transformation in highly competitive industries. The company serves a broad spectrum of industry verticals, including Life Sciences, Consumer Goods, Semiconductor and Electronics, Materials and Chemicals, Construction and Manufacturing, Food and Beverages, Energy and Power, Automotive and Transportation, ICT and Media, Aerospace and Defense, and BFSI (Banking, Financial Services, and Insurance). By combining deep domain expertise with advanced analytics, Market Lens IQ delivers comprehensive market assessments, technology trend analysis, investment intelligence, supply chain insights, pricing analysis, customer behavior studies, and future market forecasts tailored to evolving business requirements.

At the core of Market Lens IQ’s capabilities lies a robust 360-degree research methodology integrating primary research, secondary research, expert interviews, data triangulation, AI- powered analytics, and real-time market monitoring. Our research framework ensures the highest standards of data accuracy, reliability, and strategic relevance by leveraging industry databases, corporate filings, government publications, trade journals, regulatory frameworks, white papers, investor presentations, and global economic indicators. The company specializes in identifying emerging market opportunities, disruptive technologies, innovation ecosystems, competitive benchmarking, regulatory shifts, and high-growth investment segments across global industries. Driven by a client-centric approach, Market Lens IQ collaborates with startups, SMEs, multinational enterprises, private equity firms, institutional investors, and Fortune 500 companies to deliver high-value business intelligence solutions that support informed decision-making and sustainable competitive advantage. Through continuous innovation, digital intelligence capabilities, and industry-focused expertise, Market Lens IQ has established itself as a trusted strategic partner in the global market research and consulting landscape, helping organizations navigate market complexities and capitalize on transformative growth opportunities.

+1 2315155523

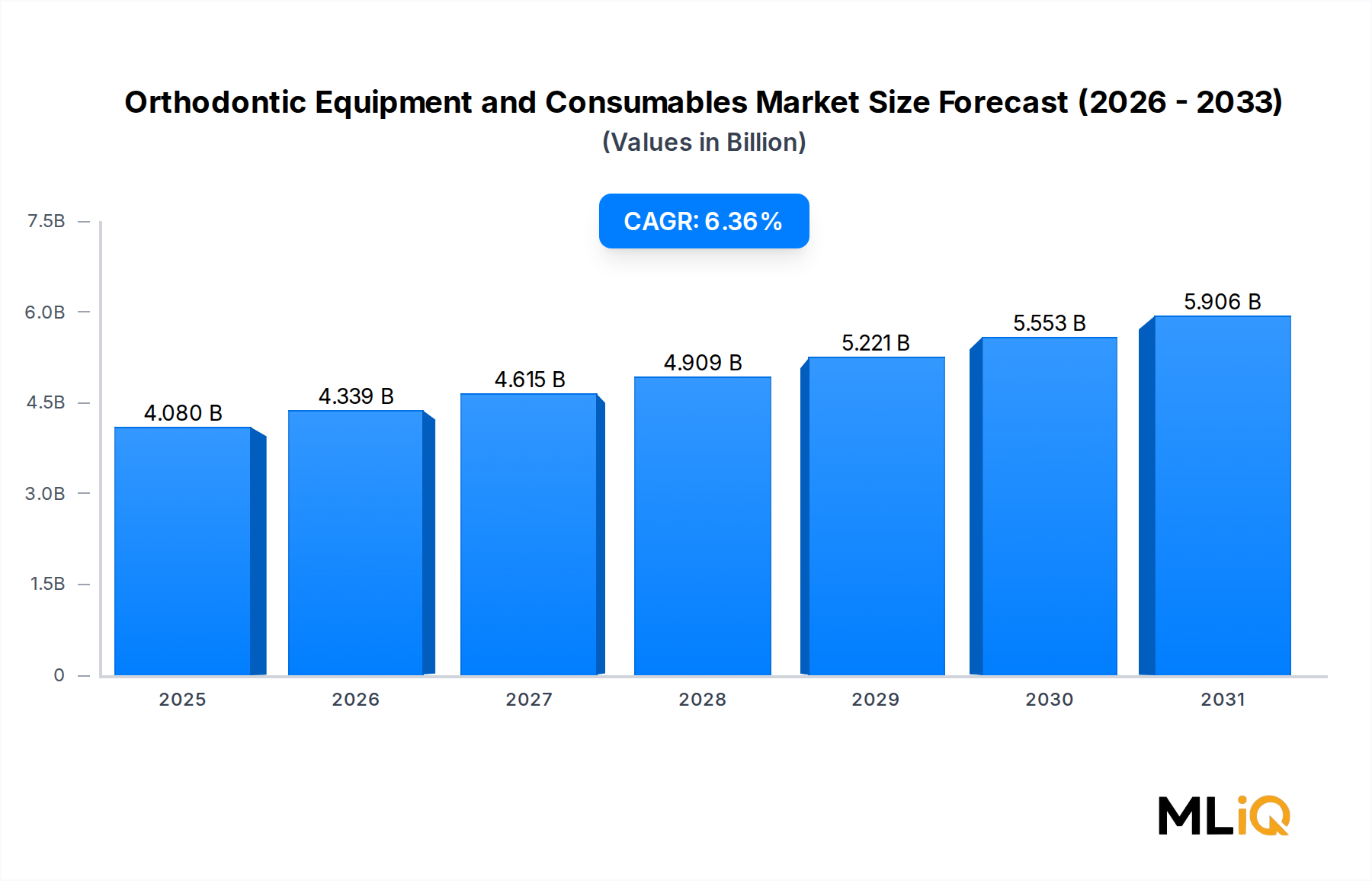

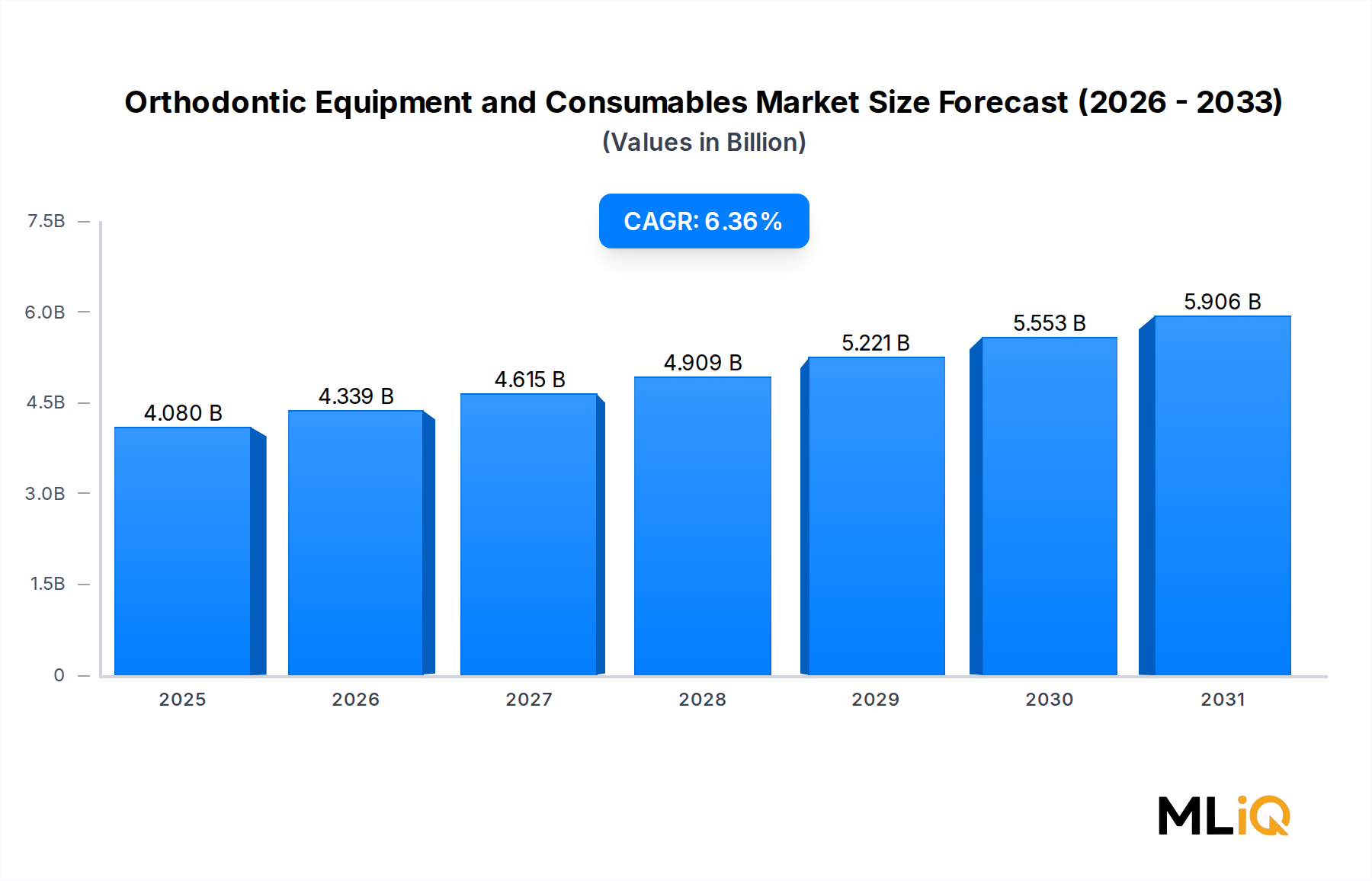

The global Orthodontic Equipment and Consumables Market is valued at $4.08 billion in 2025 and is projected to expand at a compound annual growth rate (CAGR) of 6.36% through 2033, reflecting robust structural demand across both developed and emerging economies. This growth trajectory positions the market to reach approximately $6.7 billion by 2033, driven by a convergence of demographic, technological, and behavioral factors reshaping orthodontic care delivery worldwide.

Rising awareness of dental aesthetics among adults and adolescents remains the most prominent demand catalyst. Historically considered a pediatric specialty, orthodontic treatment has progressively penetrated the adult demographic, with adults now accounting for over one-third of new orthodontic patients in key markets such as the United States and Germany. This demographic broadening significantly expands the total addressable market for both equipment and consumables segments.

Technological innovation is a second critical macro tailwind. The adoption of digital orthodontic workflows — encompassing intraoral scanners, CAD/CAM systems, and 3D printing — is compressing treatment timelines, reducing chairside labor, and enabling more precise appliance fabrication. Clinicians and dental service organizations are investing in digital infrastructure at an accelerating pace, underpinning capital equipment expenditure across the forecast period.

On the consumables side, bracket systems, archwires, ligatures, and anchorage appliances continue to generate high-frequency, recurring revenue. The shift from traditional metal brackets toward ceramic and self-ligating variants reflects increasing patient preference for aesthetically discreet options, a trend reinforcing average selling price (ASP) improvement across consumables portfolios.

Macroeconomic tailwinds including rising disposable incomes in Asia Pacific and Latin America, expanding dental insurance coverage frameworks, and government-led oral health initiatives in markets like India, China, and Brazil are collectively broadening access to orthodontic services. Concurrently, the proliferation of dental service organizations (DSOs) in North America and Europe is standardizing procurement, favoring scale suppliers with comprehensive product portfolios.

Supply-side maturity in North America and Western Europe contrasts with nascent but rapidly growing markets in Southeast Asia and the Middle East, creating a bifurcated growth dynamic. Investors and market participants should anticipate continued M&A activity as incumbents seek to consolidate technology platforms and geographic footprints.

Forward-looking sentiment is constructive. The intersection of clinical digitization, aesthetic demand, and emerging-market penetration provides a durable multi-year growth foundation. Companies that successfully integrate hardware, software, and consumables ecosystems — creating switching-cost moats — are best positioned to capture disproportionate value over the forecast horizon.

Within the Orthodontic Equipment and Consumables Market, the orthodontic consumables segment commands the largest revenue share, consistently representing more than 55% of total market value. This dominance is structurally entrenched due to the high-frequency, recurring nature of consumable procurement relative to the episodic capital expenditure associated with equipment purchases.

Orthodontic consumables encompass four primary product families: orthodontic brackets, orthodontic archwires, orthodontic ligatures, and orthodontic anchorage appliances. Among these, orthodontic brackets constitute the single highest-revenue sub-segment. Brackets are the primary bonded interface between the archwire force system and the tooth surface, and their per-patient consumption is non-negotiable in fixed appliance therapy. The transition from traditional stainless-steel brackets to ceramic, sapphire, and self-ligating variants has elevated average unit pricing, supporting revenue expansion even in markets with stable patient volume growth.

Orthodontic archwires represent the second-largest consumables sub-category. Archwires fabricated from nickel-titanium (NiTi) superelastic alloys and beta-titanium are preferred in contemporary clinical protocols for their biomechanical efficiency and shape-memory properties, commanding significant price premiums over conventional stainless-steel archwires. The Orthodontic Archwires Market is benefiting from continued material science innovation, with heat-activated NiTi and copper NiTi variants gaining clinical traction.

Orthodontic ligatures, while lower in unit value, are consumed in the highest absolute quantities per patient treatment cycle. Their role in securing the archwire to the bracket bracket slot makes them a constant replenishment item, generating predictable annuity-style revenue for distributors and manufacturers alike.

Orthodontic anchorage appliances, including temporary anchorage devices (TADs), palate expanders, and headgear systems, occupy a specialized niche. TAD adoption has grown materially over the past decade as clinicians seek to achieve three-dimensional tooth movement control without relying on patient compliance with removable anchorage systems. This sub-segment is growing at an above-market rate as training penetration for TAD placement increases among general orthodontists globally.

Key players within the consumables segment include Dentsply International Inc, 3M Unitek (a division of 3M Company), Ormco Corporation (a Danaher Corporation subsidiary), and Henry Schein, Inc., among others. Dentsply International Inc maintains a particularly strong position through its vertically integrated bracket and archwire portfolio, supported by a global distribution infrastructure.

The consumables segment's share is not merely holding steady — it is consolidating, driven by three reinforcing dynamics. First, the growing installed base of orthodontic practices (both standalone and DSO-affiliated) generates expanding consumable pull-through demand. Second, the introduction of aesthetically superior products at premium price points elevates revenue per patient course of treatment. Third, private label and value-segment entry by Asian manufacturers has not materially eroded mid-to-premium tier pricing, as clinician preference for validated, regulatory-cleared consumables from established brands remains strong in North America and Europe.

For market participants, the consumables segment offers superior gross margin profiles relative to capital equipment, given lower manufacturing complexity per unit (relative to imaging systems or dental chairs), streamlined regulatory pathways for incremental product variants, and high purchase frequency. This makes it the preferred focal point for strategic investment and portfolio expansion among incumbents and new entrants alike.

The Orthodontic Equipment and Consumables Market is shaped by a well-defined set of quantifiable drivers and structural constraints that collectively determine its growth ceiling and floor.

Driver 1: Rising Adult Orthodontic Demand. The adult orthodontic patient cohort (ages 18 and above) has grown from approximately 20% of total orthodontic patients in 2010 to over 35% in 2024 across developed markets. This demographic shift significantly expands recurring treatment cycles and drives higher ASP-per-patient metrics, as adult patients disproportionately select premium aesthetic appliances, including ceramic brackets and clear aligners.

Driver 2: Digitization of Clinical Workflows. Penetration of intraoral scanners — a critical enabler of digital orthodontics — exceeded 40% among orthodontic specialists in the United States by 2024, up from less than 15% in 2018. This rapid adoption drives capital investment in CAD/CAM dental systems, 3D printers, and planning software, materially expanding the equipment segment's total serviceable market. The CAD/CAM Dental Systems Market is a directly adjacent growth vector for orthodontic equipment suppliers.

Driver 3: Emerging Market Expansion. Asia Pacific's orthodontic treatment penetration rate remains below 5% in countries such as India and Indonesia, compared to 25–30% in the United States, signifying a structurally underpenetrated opportunity. Rising middle-class income, urbanization, and the expansion of private dental clinic chains are rapidly closing this gap.

Driver 4: Insurance Coverage Expansion. In the United States, orthodontic coverage under employer-sponsored dental plans covers approximately 60% of children and a growing share of adults, reducing out-of-pocket barriers and supporting stable volume growth.

Constraint 1: High Capital Equipment Costs. Advanced orthodontic equipment, including CBCT imaging systems and CAD/CAM units, represents six-figure procurement decisions for independent practitioners, constraining adoption velocity among smaller clinics, particularly in price-sensitive emerging markets.

Constraint 2: Skilled Labor Shortage. The global shortage of trained orthodontic specialists limits patient throughput capacity, particularly in underserved rural markets, creating a supply-side ceiling on demand conversion.

Constraint 3: Reimbursement Variability. Inconsistent reimbursement frameworks across European national health systems and in Middle Eastern markets create revenue unpredictability for equipment suppliers reliant on institutional procurement channels.

The competitive landscape of the Orthodontic Equipment and Consumables Market is characterized by a mix of large diversified healthcare conglomerates, specialized dental equipment manufacturers, and regional players. The following profiles the key participants:

Danaher Corporation: A diversified science and technology company whose dental platform, operating through Ormco and KaVo Kerr, delivers a comprehensive orthodontic consumables and equipment portfolio spanning brackets, archwires, and imaging systems. Danaher's lean operating model and continuous M&A discipline have made it one of the most formidable competitors in the space.

Dentsply International Inc: One of the world's largest manufacturers of professional dental products, with a deep orthodontic consumables portfolio that includes brackets, bonding agents, and archwires marketed under brands including GAC. The company is actively pursuing digital integration to complement its traditional consumables strength.

Henry Schein, Inc.: A leading dental product distributor with a global commercial infrastructure serving orthodontic practices across North America, Europe, and Asia Pacific. Its distribution-centric model gives it unparalleled channel reach and purchasing scale.

Patterson Companies: A major dental supply chain company providing orthodontic consumables and equipment to a broad practitioner base in North America. Patterson's value-added services, including practice management software and equipment financing, differentiate its customer engagement model.

Sirona Dental Systems Inc.: A pioneer in digital dental systems, including CEREC CAD/CAM platforms and imaging solutions used in digital orthodontic workflows. Its technology integration with Dentsply following the merger strengthened its position at the intersection of equipment and digital services.

3 Shape A/S: A specialist in intraoral scanning and 3D digital dental solutions, with its TRIOS scanner platform widely adopted in orthodontic practices globally. The company's open-system philosophy and software ecosystem drive strong network effects.

GC Corporation: A Japan-based global dental materials company with a growing orthodontic consumables and bonding material portfolio, holding particularly strong positions across Asia Pacific and Europe.

Ultradent Products, Inc.: Known for specialty dental and orthodontic consumables including bonding agents, cements, and ancillary treatment products, with a loyal clinician following built on clinical validation and training programs.

Midmark Corporation: A provider of dental equipment including dental chairs, delivery systems, and operatory solutions. Its ergonomic and workflow-focused product philosophy resonates with modern practice design standards.

Zimmer Dental Inc.: Focused on dental implant and anchorage systems with applications in complex orthodontic-surgical cases, serving a specialized niche within the broader orthodontic market.

Septodont: A dental pharmaceutical and consumables company with relevant offerings in anesthetics and bonding materials used in orthodontic procedures.

January 2024: Danaher Corporation completed the separation of its Envista Holdings dental business, restructuring its orthodontic portfolio strategy and sharpening commercial focus on high-growth consumable and digital orthodontic segments.

March 2024: 3 Shape A/S launched a next-generation intraoral scanning platform with enhanced AI-powered orthodontic treatment planning integration, extending its competitive lead in the digital orthodontics workflow segment.

May 2024: Henry Schein, Inc. announced an expanded distribution agreement with a leading clear aligner manufacturer, broadening its consumables portfolio and reinforcing its position as a preferred full-service orthodontic supply partner for DSOs.

August 2023: Dentsply International Inc introduced an updated generation of self-ligating brackets incorporating low-friction surface coatings, targeting clinicians seeking enhanced archwire engagement performance and reduced treatment duration.

October 2023: GC Corporation received CE Mark approval for a new range of orthodontic bonding composites formulated for compatibility with ceramic and zirconia bracket systems, expanding addressable clinical applications in European markets.

February 2025: Patterson Companies announced an enhanced digital orthodontic equipment financing program targeting independent orthodontic practices, aimed at accelerating CAD/CAM system adoption among non-DSO affiliated clinicians.

November 2023: Midmark Corporation unveiled a redesigned orthodontic chair line with integrated digital connectivity features, supporting chairside tablet integration and real-time patient record synchronization.

The Orthodontic Equipment and Consumables Market exhibits distinct regional growth profiles, reflecting variations in healthcare infrastructure, income levels, insurance penetration, and digital adoption.

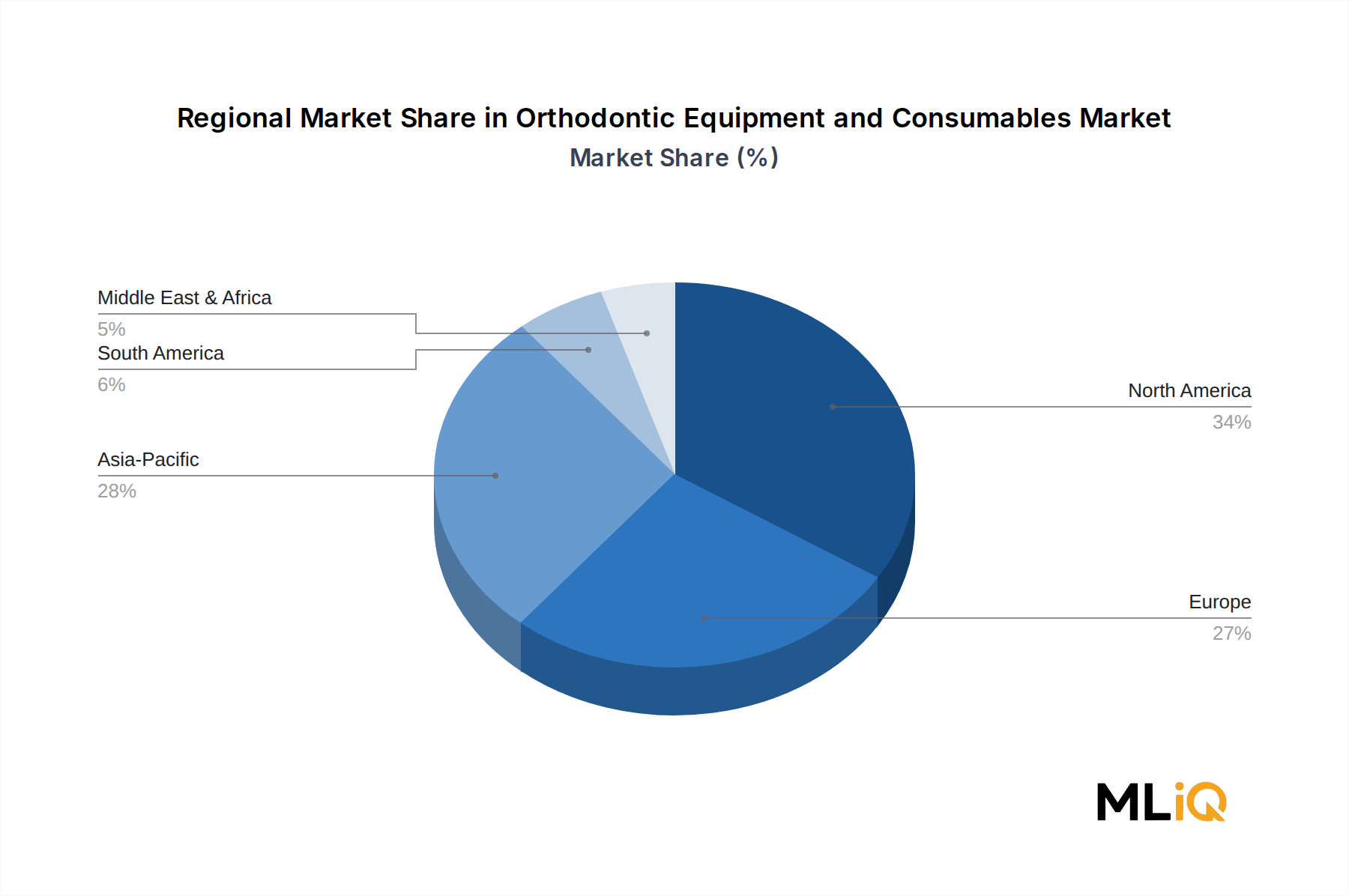

North America remains the most mature and highest-revenue region, accounting for approximately 38% of global market value in 2025. The United States dominates regional demand, underpinned by high per-capita dental spending (exceeding $400 per person annually), robust orthodontic insurance coverage, and the highest concentration of DSOs globally. The regional CAGR is estimated at 5.1% through 2033, reflecting a mature but innovation-driven growth dynamic. Canada and Mexico contribute incrementally, with Mexico emerging as a near-shore manufacturing hub for select consumable categories.

Europe represents approximately 28% of global market share, with Germany, the United Kingdom, France, and Italy collectively accounting for the majority of regional revenue. The region benefits from strong dental specialist density and advanced digital orthodontic adoption, particularly in Germany and the Nordics. However, heterogeneous reimbursement policies across EU member states temper growth velocity. The European regional CAGR is estimated at 4.8% through 2033.

Asia Pacific is the fastest-growing regional market, with a projected CAGR of 8.9% through 2033. China and India are the primary growth engines, driven by expanding middle-class populations, rapid urbanization, and government oral health initiatives. Japan and South Korea maintain high per-capita orthodontic expenditure and significant demand for premium digital systems. The ASEAN subregion — including Indonesia, Thailand, and Vietnam — is an emerging frontier market with structurally low treatment penetration rates and accelerating private sector dental investment.

Latin America accounts for approximately 7% of global revenue, with Brazil and Argentina as the dominant markets. Brazil's large population base and growing cosmetic dentistry culture position it as a high-potential market for aesthetic orthodontic consumables. The regional CAGR is estimated at 6.7% through 2033, with infrastructure and income constraints moderating the ceiling.

The Middle East and Africa region represents the smallest current revenue share at approximately 5%, but includes high-growth pockets, particularly within GCC countries (Saudi Arabia, UAE), where premium dental care expenditure is elevated by high disposable incomes and medical tourism activity. South Africa serves as a gateway market for sub-Saharan expansion. The regional CAGR is estimated at 7.2% through 2033.

The supply chain underpinning the Orthodontic Equipment and Consumables Market is moderately complex, characterized by multi-tier dependencies on specialty metals, engineering polymers, and electronic components sourced from globally distributed suppliers.

Nickel-titanium (NiTi) alloy is the most strategically critical raw material for archwire manufacturing. NiTi's superelastic and shape-memory properties make it clinically irreplaceable in contemporary archwire design. Nickel prices experienced significant volatility between 2021 and 2023, with spot prices peaking above $29,000 per metric ton in March 2022

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6.36% from 2020-2034 |

| Segmentation |

|

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Comprehensive validation mechanisms ensuring market intelligence accuracy, reliability, and adherence to international standards.

500+ data sources cross-validated

200+ industry specialists validation

NAICS, SIC, ISIC, TRBC standards

Continuous market tracking updates

Factors such as are projected to boost the Orthodontic Equipment and Consumables Market market expansion.

Key companies in the market include Sirona Dental Systems Inc., Ultradent Products, Inc., GC Corporation, Henry Schein, Inc., Patterson Companies, Zimmer Dental Inc., 3 Shape A/S, Septodont, Midmark Corporation, Danaher Corporation, Dentsply International Inc, Inc.

The market segments include Orthodontic equipment, Orthodontic consumables.

The market size is estimated to be USD 4.08 billion as of 2022.

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3690, USD 5820, and USD 9870 respectively.

The market size is provided in terms of value, measured in billion and volume, measured in .

Yes, the market keyword associated with the report is "Orthodontic Equipment and Consumables Market," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Orthodontic Equipment and Consumables Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.