1. What are the major growth drivers for the Cold Plasma Implant Treatment Devices Market market?

Factors such as are projected to boost the Cold Plasma Implant Treatment Devices Market market expansion.

Market Lens IQ is a global market intelligence and strategic consulting firm delivering advanced syndicated research reports, customized industry analysis, competitive intelligence, and data-driven advisory solutions to organizations across international markets. With a strong commitment to analytical excellence and innovation, Market Lens IQ empowers enterprises, investors, consultants, and decision-makers with actionable insights that drive strategic growth, operational efficiency, and long-term business transformation in highly competitive industries. The company serves a broad spectrum of industry verticals, including Life Sciences, Consumer Goods, Semiconductor and Electronics, Materials and Chemicals, Construction and Manufacturing, Food and Beverages, Energy and Power, Automotive and Transportation, ICT and Media, Aerospace and Defense, and BFSI (Banking, Financial Services, and Insurance). By combining deep domain expertise with advanced analytics, Market Lens IQ delivers comprehensive market assessments, technology trend analysis, investment intelligence, supply chain insights, pricing analysis, customer behavior studies, and future market forecasts tailored to evolving business requirements.

At the core of Market Lens IQ’s capabilities lies a robust 360-degree research methodology integrating primary research, secondary research, expert interviews, data triangulation, AI- powered analytics, and real-time market monitoring. Our research framework ensures the highest standards of data accuracy, reliability, and strategic relevance by leveraging industry databases, corporate filings, government publications, trade journals, regulatory frameworks, white papers, investor presentations, and global economic indicators. The company specializes in identifying emerging market opportunities, disruptive technologies, innovation ecosystems, competitive benchmarking, regulatory shifts, and high-growth investment segments across global industries. Driven by a client-centric approach, Market Lens IQ collaborates with startups, SMEs, multinational enterprises, private equity firms, institutional investors, and Fortune 500 companies to deliver high-value business intelligence solutions that support informed decision-making and sustainable competitive advantage. Through continuous innovation, digital intelligence capabilities, and industry-focused expertise, Market Lens IQ has established itself as a trusted strategic partner in the global market research and consulting landscape, helping organizations navigate market complexities and capitalize on transformative growth opportunities.

+1 2315155523

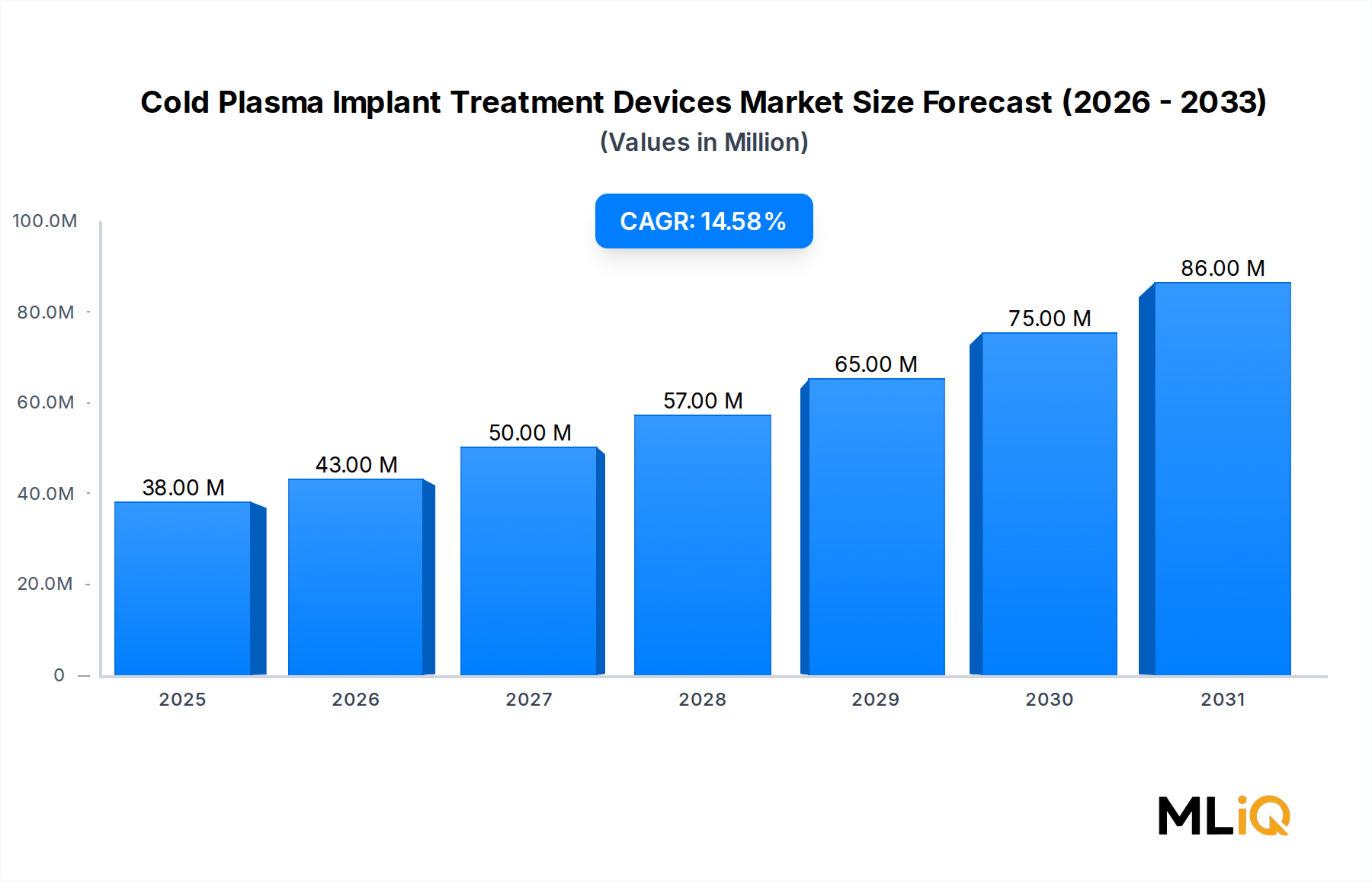

The Cold Plasma Implant Treatment Devices Market is positioned as one of the most technically sophisticated and rapidly expanding niches within medical device surface engineering. Valued at $37.82 million in the base year, the market is projected to expand at a compound annual growth rate (CAGR) of 14.70% through the forecast period of 2025–2033, reflecting strong underlying demand for advanced implant surface modification technologies. This growth trajectory places the market among the fastest-scaling segments in the broader Life Sciences instrumentation landscape.

At its core, cold plasma treatment — often referred to as non-thermal or atmospheric pressure plasma — enables the precise modification of implant surfaces at the molecular level without inducing thermal damage to sensitive biomaterials. This capability is particularly critical for orthopedic and dental implants, where surface hydrophilicity, osseointegration potential, and microbial resistance are decisive clinical performance factors. Increasing rates of implant surgeries globally, driven by aging demographics and rising incidence of musculoskeletal disorders, are generating consistent demand for devices capable of optimizing implant-tissue interaction.

Several macro tailwinds are reinforcing this growth trajectory. First, regulatory agencies in the United States and European Union are tightening sterilization and biocompatibility standards for implantable materials, compelling manufacturers to adopt plasma-based surface activation as a validated pre-treatment step. Second, the convergence of handheld device miniaturization and advanced plasma generation electronics is making cold plasma treatment accessible in clinical settings beyond centralized manufacturing facilities. Third, rising R&D expenditure among large medical device original equipment manufacturers (OEMs) is fueling adoption of commercial plasma systems as part of next-generation implant production workflows.

The competitive landscape remains fragmented but is showing early signs of consolidation as technology providers form strategic alliances with implant manufacturers. Key players including RELYON PLASMA GMBH, TERRAPLASMA GMBH, and NORDSON CORPORATION are investing in application-specific device configurations. Geographically, North America currently commands the largest revenue share, while the Asia Pacific region is anticipated to register the highest CAGR over the forecast horizon, underpinned by expanding healthcare infrastructure and growing medical tourism in China, India, and South Korea.

Looking ahead, the integration of cold plasma units into automated implant manufacturing lines and the development of point-of-care handheld devices for intraoperative implant surface activation represent the two most consequential near-term growth vectors. The Cold Plasma Implant Treatment Devices Market is, in summary, transitioning from a niche research application into a mainstream clinical and manufacturing necessity.

The application segment encompassing orthopedic implants and dental implants constitutes the single largest and most revenue-generative sub-market within the Cold Plasma Implant Treatment Devices Market. This dominance is rooted in the fundamental biological requirements of osseointegration — the direct structural and functional connection between living bone and the surface of a load-bearing implant — which cold plasma treatment has been empirically demonstrated to enhance across titanium, zirconia, PEEK, and cobalt-chromium substrates.

For dental implants specifically, cold plasma surface activation addresses one of the most persistent clinical challenges: marginal bone loss and early implant failure attributable to inadequate initial osseointegration. Studies published in peer-reviewed prosthodontic journals have consistently demonstrated that plasma-treated titanium implants exhibit contact angles below 10 degrees, compared to untreated surfaces averaging 60–80 degrees, a several-fold improvement in wettability that accelerates fibronectin adsorption and subsequent osteoblast attachment. This biophysical advantage translates into measurable clinical outcomes, which drives procurement decisions among dental device manufacturers and hospital-based implantology centers.

The orthopedic segment is equally compelling. Total hip and knee replacement procedures are projected to grow substantially through 2033 as the global population over 65 years of age expands. In the United States alone, total joint replacement surgeries number in the hundreds of thousands annually, and implant revision rates — frequently attributed to suboptimal osseointegration or peri-implant infection — create persistent demand for surface treatment technologies that can meaningfully reduce failure incidence. Cold plasma treatment, by creating reactive oxygen and nitrogen species (RONS) on implant surfaces, also delivers antimicrobial surface conditioning that reduces biofilm formation risk, a dual benefit that orthopedic surgeons and hospital procurement committees increasingly factor into supplier selection criteria.

Key players operating prominently within this application segment include RELYON PLASMA GMBH, which has developed modular plasma systems compatible with standard implant manufacturing conveyor lines; PLASMA MEDICAL SYSTEMS, which focuses on clinical-grade point-of-care handheld devices; and ADTEC PLASMA TECHNOLOGY, which supplies high-frequency plasma generators used in both dental and orthopedic implant production environments. NOVAPLASMA and TERRAPLASMA GMBH are also active in this space, with the latter emphasizing preclinical research tools tailored to academic and hospital-based R&D teams.

In terms of market share dynamics, the orthopedic and dental implant segment is not merely holding its lead — it is consolidating it. As clinical evidence accumulates and reimbursement frameworks in key markets begin to acknowledge plasma surface treatment as a value-adding step in implant preparation, procurement volumes are increasing. Medical device companies, which account for a substantial share of commercial system purchases, are integrating cold plasma units into ISO Class 7 and Class 8 cleanroom manufacturing environments, embedding the technology into quality management systems (QMS) that cannot easily be displaced by competing surface modification approaches such as acid etching or sandblasting alone.

The segment's dominance is further reinforced by the regulatory landscape: the U.S. FDA's 510(k) and PMA pathways increasingly scrutinize biocompatibility data submissions, making plasma-mediated surface documentation a competitive differentiator in premarket submissions. This regulatory dynamic effectively functions as a structural demand driver that insulates the orthopedic and dental implant application segment from cyclical demand fluctuations.

Several quantifiable drivers and measurable constraints define the competitive and growth dynamics of the Cold Plasma Implant Treatment Devices Market over the 2025–2033 forecast period.

Driver 1 — Rising Implant Procedure Volumes: Global dental implant placements exceeded 5 million annually in recent data periods, with projections suggesting double-digit percentage growth through the end of the decade. Orthopedic implant procedures follow a similar trajectory, driven by musculoskeletal disease prevalence. Each implant represents a potential point of cold plasma treatment adoption, establishing a large and growing addressable base.

Driver 2 — Stringent Biocompatibility Standards: The ISO 10993 series and EU Medical Device Regulation (MDR 2017/745), now fully in force, impose detailed biocompatibility and surface characterization requirements. Manufacturers seeking CE Mark compliance must document surface chemistry changes with greater rigor, increasing the value proposition of plasma treatment as a repeatable, validatable process step.

Driver 3 — Technological Miniaturization: Advances in power electronics and dielectric barrier discharge engineering have reduced the footprint and cost of cold plasma generators by an estimated 30–40% over the past five years, enabling deployment in clinical settings that previously lacked the infrastructure to accommodate large commercial systems. This has opened the handheld device sub-segment as a meaningful growth vector.

Driver 4 — Infection Control Imperatives: Hospital-acquired infections related to implant procedures carry estimated per-case costs exceeding $50,000 in advanced healthcare systems. Cold plasma's demonstrated antimicrobial efficacy against MRSA, E. coli, and Candida biofilms provides a compelling economic argument for adoption in high-acuity hospital settings.

Constraint 1 — High Capital Expenditure: Commercial cold plasma systems suitable for GMP-compliant implant manufacturing environments carry price points that can challenge the capital budgets of smaller medical device manufacturers and independent dental laboratories, limiting penetration in price-sensitive markets.

Constraint 2 — Limited Clinical Standardization: The absence of universally accepted treatment protocols — including optimal plasma exposure duration, gas composition, and power density for specific implant materials — creates hesitancy among conservative hospital procurement committees and regulatory bodies, slowing adoption in certain geographies.

The competitive landscape of the Cold Plasma Implant Treatment Devices Market features a mix of specialized plasma technology developers, academic spin-offs, and diversified industrial equipment suppliers. The following profiles characterize the strategic positioning of key market participants:

RELYON PLASMA GMBH: A Germany-based pioneer in atmospheric pressure plasma technology, RELYON PLASMA GMBH offers a broad portfolio of plasma jets and plasma systems optimized for medical device surface activation, with strong integration capabilities for automated manufacturing lines.

NOVAPLASMA: Focused on compact plasma treatment solutions for biomedical applications, NOVAPLASMA has established itself as an innovator in low-temperature plasma systems targeting both dental implant manufacturers and research institutions seeking benchtop-scale devices.

EUROPLASMA NV: A Belgian company with deep expertise in plasma coating and surface treatment across multiple industries, EUROPLASMA NV leverages its cross-sector technology base to deliver specialized biomedical plasma treatment systems compliant with ISO and EU MDR requirements.

TANTEC A/S: A Danish surface treatment specialist, TANTEC A/S provides plasma activation equipment widely used in the medical device sector, with particular strength in Scandinavian and Northern European hospital and manufacturing markets.

PLASMAWISE: Positioned as a solutions-oriented provider, PLASMAWISE develops customized plasma treatment protocols and equipment configurations tailored to the specific substrate and geometry requirements of orthopedic and dental implant producers.

AG AFS ENTWICKLUNGS+VERTRIEBS GMBH: A German development and distribution company active in plasma technology applications for surface engineering, AG AFS ENTWICKLUNGS+VERTRIEBS GMBH serves both manufacturing and clinical market channels with specialized plasma exposure systems.

TERRAPLASMA GMBH: Emerging from academic plasma physics research in Germany, TERRAPLASMA GMBH focuses on plasma medicine applications and has developed devices specifically designed for intraoperative and clinical plasma treatment scenarios, including implant surface activation at point of care.

PLASMA MEDICAL SYSTEMS: Specializing in medical-grade plasma devices, PLASMA MEDICAL SYSTEMS is recognized for its handheld and portable device configurations that enable cold plasma treatment in sterile surgical environments, addressing the growing demand for intraoperative implant conditioning.

NORDSON CORPORATION: A large, diversified precision dispensing and surface treatment technology corporation, NORDSON CORPORATION brings significant manufacturing scale, global distribution infrastructure, and R&D investment capacity to the cold plasma device segment.

ADTEC PLASMA TECHNOLOGY: A Japan-based supplier of plasma generators and power systems, ADTEC PLASMA TECHNOLOGY serves the medical device manufacturing sector with high-frequency plasma sources integrated into implant surface preparation workflows.

Q1 2024: RELYON PLASMA GMBH announced an expanded partnership with a leading European orthopedic implant manufacturer to co-develop an inline plasma activation module for titanium hip stem production lines, targeting full GMP qualification by mid-2025.

Q2 2024: TERRAPLASMA GMBH published peer-reviewed clinical data demonstrating a statistically significant improvement in early osseointegration rates for plasma-treated zirconia dental implants versus untreated controls in a multicenter European trial, bolstering the evidence base for clinical adoption.

Q3 2024: NORDSON CORPORATION disclosed capital investment in upgrading its plasma surface treatment equipment product lines, specifically to address ISO 10993 compliance documentation workflows demanded by FDA and EU MDR regulatory submissions.

Q4 2023: EUROPLASMA NV received CE Mark certification for a new series of biomedical plasma treatment chambers designed for small-batch implant processing, enabling entry into hospital-based central sterile supply department workflows across the EU.

Q1 2025: PLASMA MEDICAL SYSTEMS launched a next-generation handheld cold plasma device featuring a rechargeable battery module and disposable plasma jet cartridges, targeting oral and maxillofacial surgery suites for intraoperative dental implant surface activation.

Q2 2025: ADTEC PLASMA TECHNOLOGY entered into a distribution agreement with a South Korean medical device distributor to expand commercial presence across ASEAN implant manufacturing clusters, reflecting accelerating Asia Pacific market penetration.

Q3 2023: The International Organization for Standardization (ISO) initiated a working group to develop a draft standard specifically addressing plasma surface treatment validation for implantable medical devices, a regulatory development that, once finalized, is expected to accelerate institutional procurement decisions globally.

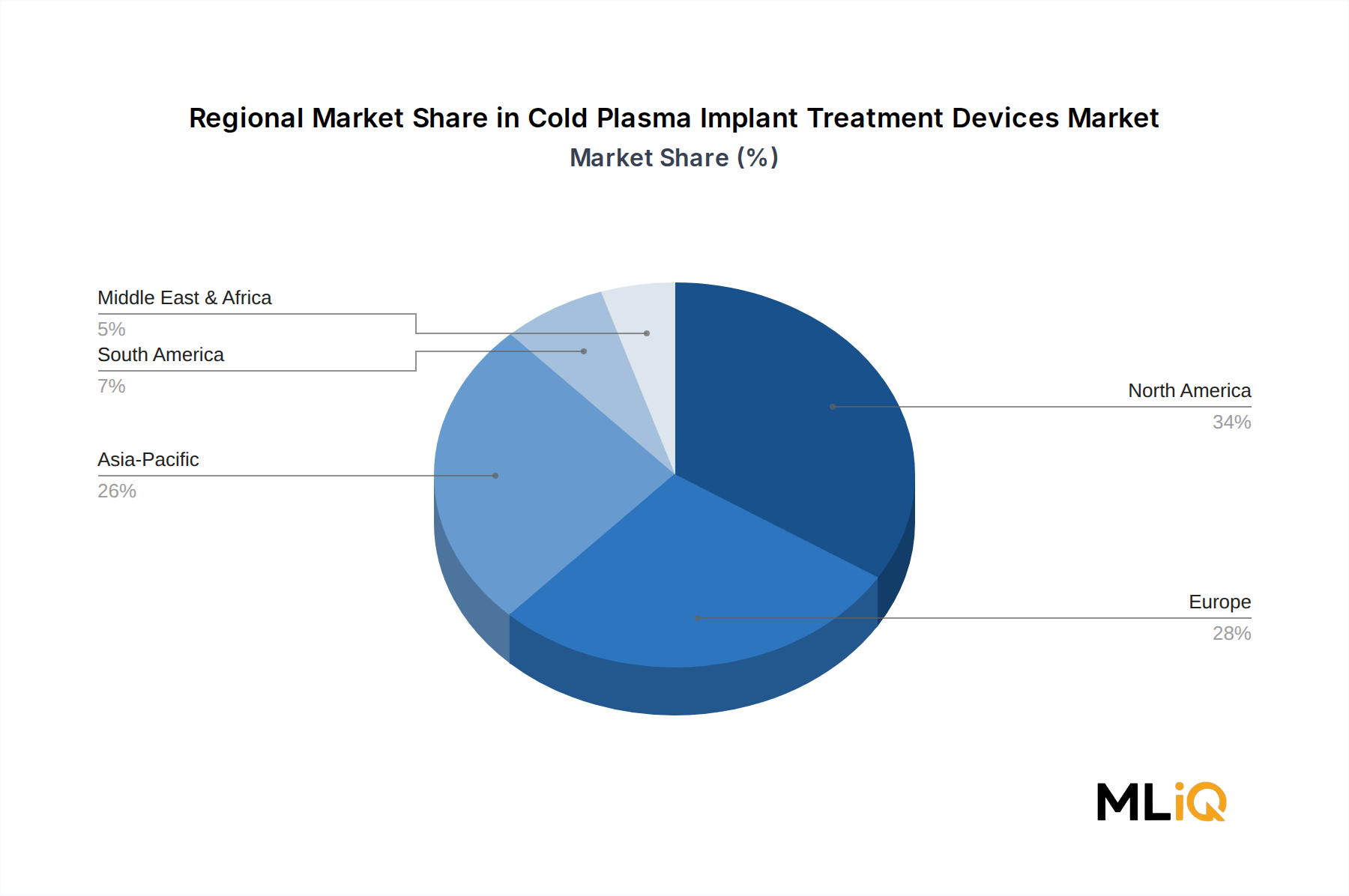

The Cold Plasma Implant Treatment Devices Market exhibits distinct regional growth profiles shaped by healthcare infrastructure maturity, regulatory environments, and implant procedure volumes.

North America: North America holds the largest revenue share, estimated at approximately 35–38% of global market value, driven by the United States' high volume of elective orthopedic and dental procedures, robust reimbursement frameworks, and the presence of major medical device OEMs that are early adopters of advanced surface treatment technologies. FDA regulatory rigor around biocompatibility documentation is a structural driver of plasma device procurement. The regional CAGR is estimated at 12.5–13.5%, reflecting a mature but still-expanding base.

Europe: Europe is the second-largest regional market, accounting for approximately 28–32% of global revenue. Germany, France, and the United Kingdom are the primary revenue contributors, with Germany holding a disproportionate share owing to the concentration of plasma technology developers including RELYON PLASMA GMBH and TERRAPLASMA GMBH. The full enforcement of EU MDR has accelerated adoption of validated surface treatment processes, making cold plasma treatment a compliance-driven procurement priority. European CAGR is estimated at 13.0–14.0%.

Asia Pacific: Asia Pacific is the fastest-growing region, with a projected CAGR of 17.0–18.5% over the forecast period. China, Japan, South Korea, and India are the primary growth markets. China's domestic medical device manufacturing sector is expanding rapidly, with government policy incentives supporting technology localization, including plasma surface treatment equipment. Japan's advanced manufacturing culture and South Korea's medical tourism sector are additional demand catalysts. ADTEC PLASMA TECHNOLOGY's presence in Japan and recent ASEAN distribution agreements reflect industry recognition of this regional growth premium.

Latin America: Brazil and Argentina represent the principal markets in Latin America, a region that currently accounts for approximately 6–8% of global revenue. CAGR is estimated at 11.0–12.5%, with growth primarily driven by expanding private dental clinic networks and increasing elective orthopedic procedure volumes supported by rising middle-class healthcare expenditure.

Middle East & Africa: This region contributes approximately 5–7% of global market value, with the GCC countries — particularly Saudi Arabia and the UAE — leading adoption. Healthcare infrastructure investment under Vision 2030 initiatives and the establishment of regional medical device manufacturing zones are creating nascent demand. CAGR is estimated at 13.5–15.0%, making this a region to monitor for accelerated growth.

The regulatory environment governing the Cold Plasma Implant Treatment Devices Market is multi-layered, spanning device classification, biocompatibility testing standards, manufacturing process validation, and plasma-specific safety protocols.

In the United States, the FDA classifies cold plasma treatment devices used in implant manufacturing under various 510(k) and De Novo pathways depending on intended use and risk classification. Devices used for surface modification of implantable components must comply with 21 CFR Part 820 Quality System Regulation (now transitioning to alignment with ISO 13485), and surface treatment processes must be fully documented in Device Master Records as critical manufacturing steps. The FDA's increased scrutiny of biocom

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 14.70% from 2020-2034 |

| Segmentation |

|

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Comprehensive validation mechanisms ensuring market intelligence accuracy, reliability, and adherence to international standards.

500+ data sources cross-validated

200+ industry specialists validation

NAICS, SIC, ISIC, TRBC standards

Continuous market tracking updates

Factors such as are projected to boost the Cold Plasma Implant Treatment Devices Market market expansion.

Key companies in the market include RELYON PLASMA GMBH, NOVAPLASMA, EUROPLASMA NV, TANTEC A/S, PLASMAWISE, AG AFS ENTWICKLUNGS+VERTRIEBS GMBH, TERRAPLASMA GMBH, PLASMA MEDICAL SYSTEMS, NORDSON CORPORATION, ADTEC PLASMA TECHNOLOGY.

The market segments include Application, Type, End user.

The market size is estimated to be USD 37.82 million as of 2022.

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3712, USD 5769, and USD 10663 respectively.

The market size is provided in terms of value, measured in million and volume, measured in .

Yes, the market keyword associated with the report is "Cold Plasma Implant Treatment Devices Market," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Cold Plasma Implant Treatment Devices Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.