1. What are the major growth drivers for the Cardiac Ablation Devices Market market?

Factors such as are projected to boost the Cardiac Ablation Devices Market market expansion.

+1 2315155523

Cardiac Ablation Devices Market

Cardiac Ablation Devices Market

Market Lens IQ is a global market intelligence and strategic consulting firm delivering advanced syndicated research reports, customized industry analysis, competitive intelligence, and data-driven advisory solutions to organizations across international markets. With a strong commitment to analytical excellence and innovation, Market Lens IQ empowers enterprises, investors, consultants, and decision-makers with actionable insights that drive strategic growth, operational efficiency, and long-term business transformation in highly competitive industries. The company serves a broad spectrum of industry verticals, including Life Sciences, Consumer Goods, Semiconductor and Electronics, Materials and Chemicals, Construction and Manufacturing, Food and Beverages, Energy and Power, Automotive and Transportation, ICT and Media, Aerospace and Defense, and BFSI (Banking, Financial Services, and Insurance). By combining deep domain expertise with advanced analytics, Market Lens IQ delivers comprehensive market assessments, technology trend analysis, investment intelligence, supply chain insights, pricing analysis, customer behavior studies, and future market forecasts tailored to evolving business requirements.

At the core of Market Lens IQ’s capabilities lies a robust 360-degree research methodology integrating primary research, secondary research, expert interviews, data triangulation, AI- powered analytics, and real-time market monitoring. Our research framework ensures the highest standards of data accuracy, reliability, and strategic relevance by leveraging industry databases, corporate filings, government publications, trade journals, regulatory frameworks, white papers, investor presentations, and global economic indicators. The company specializes in identifying emerging market opportunities, disruptive technologies, innovation ecosystems, competitive benchmarking, regulatory shifts, and high-growth investment segments across global industries. Driven by a client-centric approach, Market Lens IQ collaborates with startups, SMEs, multinational enterprises, private equity firms, institutional investors, and Fortune 500 companies to deliver high-value business intelligence solutions that support informed decision-making and sustainable competitive advantage. Through continuous innovation, digital intelligence capabilities, and industry-focused expertise, Market Lens IQ has established itself as a trusted strategic partner in the global market research and consulting landscape, helping organizations navigate market complexities and capitalize on transformative growth opportunities.

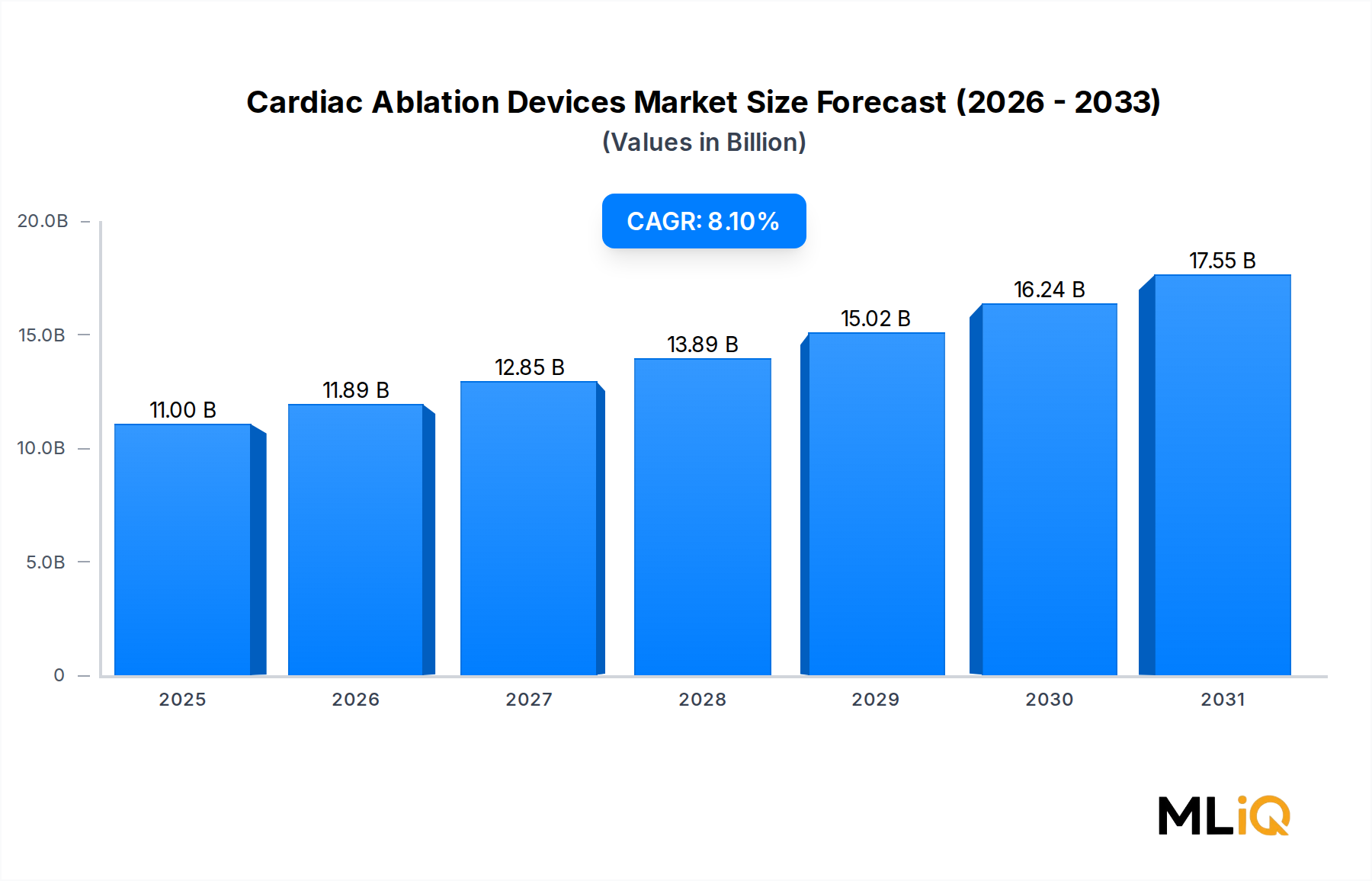

The global cardiac ablation devices market was valued at $11 billion in 2024 and is projected to expand at a compound annual growth rate (CAGR) of 8.1% through the forecast period, reflecting robust demand across hospital catheterization laboratories, ambulatory surgical centers, and electrophysiology specialty clinics worldwide. This trajectory places the market on course to nearly double its current valuation within the next decade, driven by a confluence of epidemiological, technological, and healthcare-investment tailwinds.

At the macro level, the global burden of cardiac arrhythmias continues to intensify. Atrial fibrillation (AF) alone affects an estimated 59 million individuals worldwide, a figure expected to rise sharply with aging populations in North America, Europe, and Asia Pacific. This epidemiological pressure is the single most consequential demand driver for ablation procedures and the hardware ecosystems that support them. As pharmacological rate-control therapies demonstrate limitations in rhythm normalization, interventional electrophysiology has emerged as the preferred long-term solution, elevating procedure volumes and device adoption rates simultaneously.

From a technology standpoint, the market is experiencing a pivotal transition from conventional point-by-point radiofrequency ablation toward high-power short-duration (HPSD) protocols, pulsed-field ablation (PFA), and contact-force sensing catheters. These innovations reduce procedural time, improve lesion quality, and lower complication rates — all of which influence both clinical preference and hospital capital allocation. The convergence of 3D electroanatomical mapping with real-time intracardiac echocardiography is further elevating procedural precision.

Reimbursement expansion in key markets — including updated CMS payment schedules in the United States and evolving NICE guidance in the United Kingdom — has reduced the financial barriers that historically constrained AF ablation adoption. Meanwhile, rising healthcare infrastructure investments in China, India, South Korea, and the ASEAN bloc are opening high-volume emerging-market channels.

Competitively, the market remains moderately consolidated, with a small cohort of multinational medtech corporations controlling the majority of revenue share, while a growing tier of specialty innovators challenges incumbents in niche catheter and energy-delivery subsegments. The interplay between large-platform companies and agile device startups is accelerating innovation cycles, particularly in the pulsed-field and cryoballoon segments.

Looking forward, the Cardiac Ablation Devices Market is expected to benefit from rising procedural volumes, expanding indication approvals, and the integration of artificial intelligence into mapping and navigation workflows. The market's 8.1% CAGR signals strong, sustained investor and clinical confidence through the forecast horizon.

Radiofrequency (RF) ablation represents the largest and most established product and technology segment within the Cardiac Ablation Devices Market, commanding the plurality of global revenue share. This dominance is attributable to decades of clinical validation, broad procedural familiarity among electrophysiologists, an extensive installed base of compatible mapping and navigation infrastructure, and a well-developed regulatory approval pathway across all major geographies.

RF ablation functions by delivering alternating electrical current at frequencies typically between 350 kHz and 500 kHz through a catheter electrode tip, generating resistive heating that creates discrete, targeted myocardial lesions. The technology's versatility spans the full spectrum of cardiac arrhythmias addressed in clinical practice — from paroxysmal and persistent atrial fibrillation to supraventricular tachycardias, ventricular tachycardias, and accessory pathway-mediated arrhythmias — giving it unparalleled procedural breadth compared to single-indication alternatives such as cryoablation.

Within the RF segment, the evolution toward contact-force sensing catheters has been particularly transformative. Devices equipped with force-sensing technology allow real-time measurement of catheter-tissue contact, enabling operators to deliver reproducible, transmural lesions while minimizing the risk of steam pops or perforation. Clinical data consistently demonstrates superior pulmonary vein isolation durability with force-guided RF ablation, which has reinforced physician preference and driven premium pricing power for leading manufacturers.

High-power short-duration (HPSD) ablation protocols represent the most dynamic innovation frontier within the RF subsegment. By delivering higher wattage (50–90W) over shorter application times (5–15 seconds), HPSD approaches reduce the risk of esophageal thermal injury while achieving deeper, more uniform lesions. Early multicenter registry data suggests HPSD protocols can reduce total procedural time by 20–35% compared to conventional RF delivery, a meaningful operational benefit for high-volume electrophysiology programs facing scheduling pressures.

Key players anchoring the RF segment include Boston Scientific Corporation, which markets the DIRECTSENSE technology platform; Abbott Laboratories, whose TactiCath contact-force catheter family holds a significant market position; Johnson & Johnson (Biosense Webster, Inc.), which commands substantial share through the THERMOCOOL SMARTTOUCH portfolio; and Stryker Corporation, which participates through its surgical ablation division targeting open and minimally invasive cardiac surgery applications.

Despite the emergence of pulsed-field ablation as a rapidly growing challenger technology, RF ablation's share is not expected to erode materially in the near term. PFA systems currently carry narrower indication approvals and higher unit costs, constraining their adoption to high-volume academic and tertiary centers. The broader community hospital electrophysiology market — which accounts for a substantial share of global procedure volume — will continue to rely on RF platforms for the foreseeable future.

The RF segment's revenue share is consolidating rather than expanding, as the overall market grows and newer modalities capture incremental share at the margin. However, because the total addressable procedure volume is itself growing at a high-single-digit rate, absolute RF revenue continues to rise. The segment's maturity also confers pricing discipline challenges, as competitive dynamics among established players have compressed average selling prices on standard RF catheters, while premium contact-force and irrigated-tip variants sustain higher margins. This bifurcation is driving portfolio premiumization strategies across all major RF catheter manufacturers.

The Cardiac Ablation Devices Market is shaped by a set of quantifiable drivers and structural constraints that collectively determine the pace and geography of adoption.

Driver 1: Rising Atrial Fibrillation Prevalence. Atrial fibrillation affects approximately 59 million people globally as of recent epidemiological surveys, with incidence projected to increase by 40–50% by 2050 in developed markets due to aging demographics. This translates directly into growing procedural pipelines for electrophysiology laboratories, as AF represents the single largest application for ablation devices by procedure volume.

Driver 2: Shift Toward Rhythm Control. The landmark EAST-AFNET 4 trial demonstrated that early rhythm control — including ablation — reduces cardiovascular outcomes by 21% compared to rate control alone. This landmark evidence has accelerated guideline updates by the ESC and AHA, expanding the eligible patient population for ablation and creating a structural increase in referral rates from cardiology to electrophysiology programs.

Driver 3: Pulsed-Field Ablation Adoption. PFA systems, which received CE Mark and initial FDA approvals between 2021 and 2024, are driving capital equipment investment cycles at major electrophysiology centers. Early adopter hospitals are committing to PFA generator platforms, stimulating a parallel consumable catheter revenue stream that is expected to contribute meaningfully to market growth through 2030.

Constraint 1: Procedural Complexity and Training Barriers. Cardiac ablation procedures require specialized training periods of 12–24 months for operators to achieve independent competency, limiting the expansion of procedural capacity in markets with constrained electrophysiology workforce pipelines, particularly in South Asia, Latin America, and sub-Saharan Africa.

Constraint 2: Device and Procedure Costs. The total cost of an AF ablation procedure, including disposable catheters, mapping consumables, and facility fees, can range from $8,000 to $25,000 in high-income markets, creating access barriers in price-sensitive healthcare systems and constraining volume growth in middle-income geographies despite significant unmet clinical need.

Constraint 3: Complication Risk. Serious procedural complications — including cardiac tamponade (occurring in approximately 1–2% of cases), pulmonary vein stenosis, and atrioesophageal fistula — continue to influence physician risk-benefit calculations, particularly in less experienced centers, moderating procedure ramp-up rates.

The competitive landscape of the Cardiac Ablation Devices Market is characterized by a high degree of technological differentiation, significant R&D investment, and a mix of diversified medtech conglomerates and focused electrophysiology specialists.

Johnson & Johnson (Biosense Webster, Inc.): The electrophysiology division of Johnson & Johnson holds a leading global position through its CARTO 3D mapping system and THERMOCOOL catheter family, with ongoing investment in pulsed-field ablation via its VARIPULSE platform approved in key markets.

Abbott Laboratories: Abbott competes through its TactiCath contact-force sensing catheter portfolio and EnSite X electroanatomical mapping system, maintaining strong market presence in North America and Europe while expanding its Asia Pacific commercial footprint.

Boston Scientific Corporation: Boston Scientific deploys a broad electrophysiology portfolio spanning RF catheters, cryoablation systems, and intracardiac echocardiography, with its FARAPULSE pulsed-field ablation system representing a high-growth priority following FDA clearance.

Medtronic (referenced in context): The company's Arctic Front Advance cryoballoon system holds a dominant position in the cryoablation subsegment, particularly for pulmonary vein isolation in paroxysmal AF, competing directly against RF-based point-by-point approaches on simplicity and procedural standardization grounds.

Stryker Corporation: Stryker participates in the cardiac ablation segment primarily through its surgical ablation product lines, targeting cardiothoracic surgeons performing concomitant surgical AF ablation during open-heart procedures.

CardioFocus Inc.: CardioFocus markets the HeartLight Endoscopic Ablation System, which combines laser energy delivery with direct visualization of the pulmonary vein, differentiating on real-time tissue contact confirmation and titrated energy delivery.

Advanced Cardiac Therapeutics: A specialist innovation company focused on contact-force and impedance-based feedback technologies for RF catheter ablation, partnering with broader platform players to integrate sensing capabilities into next-generation catheter designs.

Olympus Corporation: Olympus contributes to the ablation ecosystem through its endoscopic visualization and flexible scope technologies, supporting hybrid electrophysiology-surgical procedures and intracardiac imaging workflows.

CONMED Corporation: CONMED targets the surgical electrophysiology segment with its radio-frequency surgical ablation products used in Maze and mini-Maze procedures, competing on price and procedural integration with cardiac surgery teams.

MicroPort Inc.: MicroPort serves as a significant competitor in the Asia Pacific market, leveraging local manufacturing cost advantages and established hospital relationships in China to penetrate the rapidly growing RF catheter and mapping system segments.

January 2024: Boston Scientific received FDA 510(k) clearance for its FARAPULSE pulsed-field ablation system for paroxysmal atrial fibrillation, marking a pivotal commercial milestone that accelerated PFA adoption in U.S. electrophysiology centers and validated the energy modality's regulatory pathway.

March 2024: Abbott Laboratories announced the commercial launch of its next-generation EnSite X EP mapping system with AI-assisted arrhythmia annotation features, targeting procedural efficiency improvements of up to 30% in complex electrophysiology cases.

June 2024: Johnson & Johnson (Biosense Webster, Inc.) received CE Mark renewal for its VARIPULSE pulsed-field ablation catheter in the European Union, reinforcing its competitive positioning against FARAPULSE in the premium PFA segment.

August 2024: The European Heart Rhythm Association published updated consensus guidance recommending pulsed-field ablation as an acceptable first-line approach for paroxysmal AF ablation in experienced centers, formalizing clinical endorsement that is expected to accelerate European PFA uptake through 2026.

October 2024: MicroPort Inc. completed a Series C funding round to accelerate R&D and commercialization of its next-generation irrigated RF ablation catheter platform targeting the China domestic market, reflecting intensifying local-market competition against multinational incumbents.

February 2025: CardioFocus Inc. reported 12-month efficacy data from its HEARTLIGHT X3 post-market registry, demonstrating 78% freedom from AF recurrence at one year, supporting label expansion discussions with the FDA for persistent AF indications.

The regulatory environment governing the Cardiac Ablation Devices Market is complex and jurisdiction-specific, with key frameworks in the United States, European Union, China, and Japan exerting the most significant commercial influence.

In the United States, cardiac ablation devices are regulated as Class II or Class III medical devices by the Food and Drug Administration (FDA), depending on their energy modality and intended use. Catheters for AF ablation typically require Premarket Approval (PMA), the most rigorous FDA review pathway, involving randomized controlled trial data. The recent FDA clearances of PFA systems through both PMA and De Novo pathways have demonstrated regulatory openness to novel energy modalities with strong safety profiles, encouraging further innovation-stage submissions.

In the European Union, the transition from the legacy Medical Device Directive (MDD) to the Medical Device Regulation (MDR, EU 2017/745) has introduced more stringent clinical evidence requirements, notified body capacity constraints, and extended certification timelines. Several smaller ablation device manufacturers have reported delays of 12–24 months in obtaining CE Mark under MDR, temporarily constraining product launches in the EU27 market. However, the MDR's harmonized standards are expected to improve long-term market confidence and reduce post-market surveillance inconsistencies.

In China, the National Medical Products Administration (NMPA) has accelerated review pathways for innovative medical devices under the Breakthrough Device Program, offering priority review to technologies addressing unmet clinical needs. This has benefited domestic players such as MicroPort while also enabling faster approvals for multinational product launches that previously faced multi-year queues.

In Japan, the Pharmaceuticals and Medical Devices Agency (PMDA) applies a stringent review framework with mandatory Japanese clinical data requirements for Class III devices, creating a market entry barrier but also ensuring premium pricing power for approved products. Reimbursement decisions by the Central Social Insurance Medical Council (Chuikyo) directly govern procedure economics and influence hospital adoption rates.

Globally, the World Health Organization's noncommunicable disease (NCD) action plans and regional cardiovascular health strategies are increasing government procurement focus on interventional cardiac technologies, creating new public-sector demand channels particularly in middle-income countries.

The end-user base for the Cardiac Ablation Devices Market is stratified across several distinct institutional and clinical segments, each characterized by different purchasing criteria, budget cycles, and procurement architectures.

Hospital electrophysiology laboratories represent the dominant end-user category, accounting for the majority of global device revenue. Within this segment, academic medical centers and tertiary referral hospitals are the earliest adopters of premium technologies such as pulsed-field ablation systems and advanced 3D mapping platforms, driven by research mandates, physician opinion leadership, and access to capital equipment budgets supplemented by clinical trial funding. Purchasing decisions at this level involve multidisciplinary value analysis committees (VACs) that assess clinical outcomes data, total cost of ownership, vendor service contracts, and equipment

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 8.1% from 2020-2034 |

| Segmentation |

|

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Comprehensive validation mechanisms ensuring market intelligence accuracy, reliability, and adherence to international standards.

500+ data sources cross-validated

200+ industry specialists validation

NAICS, SIC, ISIC, TRBC standards

Continuous market tracking updates

Factors such as are projected to boost the Cardiac Ablation Devices Market market expansion.

Key companies in the market include CONMED Corporation., Advanced Cardiac Therapeutics, Alcon Laboratories Inc., Boston Scientific Corporation, CardioFocus Inc., Johnson & Johnson (Biosense Webster, Inc.), Stryker Corporation, Olympus Corporation, Abbott Laboratories, MicroPort Inc..

The market segments include Product, Technology, Function, Application.

The market size is estimated to be USD 11 billion as of 2022.

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3690, USD 5820, and USD 9870 respectively.

The market size is provided in terms of value, measured in billion and volume, measured in .

Yes, the market keyword associated with the report is "Cardiac Ablation Devices Market," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Cardiac Ablation Devices Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.