1. What are the major growth drivers for the Indian Dental Consumables Market market?

Factors such as are projected to boost the Indian Dental Consumables Market market expansion.

+1 2315155523

Market Lens IQ is a global market intelligence and strategic consulting firm delivering advanced syndicated research reports, customized industry analysis, competitive intelligence, and data-driven advisory solutions to organizations across international markets. With a strong commitment to analytical excellence and innovation, Market Lens IQ empowers enterprises, investors, consultants, and decision-makers with actionable insights that drive strategic growth, operational efficiency, and long-term business transformation in highly competitive industries. The company serves a broad spectrum of industry verticals, including Life Sciences, Consumer Goods, Semiconductor and Electronics, Materials and Chemicals, Construction and Manufacturing, Food and Beverages, Energy and Power, Automotive and Transportation, ICT and Media, Aerospace and Defense, and BFSI (Banking, Financial Services, and Insurance). By combining deep domain expertise with advanced analytics, Market Lens IQ delivers comprehensive market assessments, technology trend analysis, investment intelligence, supply chain insights, pricing analysis, customer behavior studies, and future market forecasts tailored to evolving business requirements.

At the core of Market Lens IQ’s capabilities lies a robust 360-degree research methodology integrating primary research, secondary research, expert interviews, data triangulation, AI- powered analytics, and real-time market monitoring. Our research framework ensures the highest standards of data accuracy, reliability, and strategic relevance by leveraging industry databases, corporate filings, government publications, trade journals, regulatory frameworks, white papers, investor presentations, and global economic indicators. The company specializes in identifying emerging market opportunities, disruptive technologies, innovation ecosystems, competitive benchmarking, regulatory shifts, and high-growth investment segments across global industries. Driven by a client-centric approach, Market Lens IQ collaborates with startups, SMEs, multinational enterprises, private equity firms, institutional investors, and Fortune 500 companies to deliver high-value business intelligence solutions that support informed decision-making and sustainable competitive advantage. Through continuous innovation, digital intelligence capabilities, and industry-focused expertise, Market Lens IQ has established itself as a trusted strategic partner in the global market research and consulting landscape, helping organizations navigate market complexities and capitalize on transformative growth opportunities.

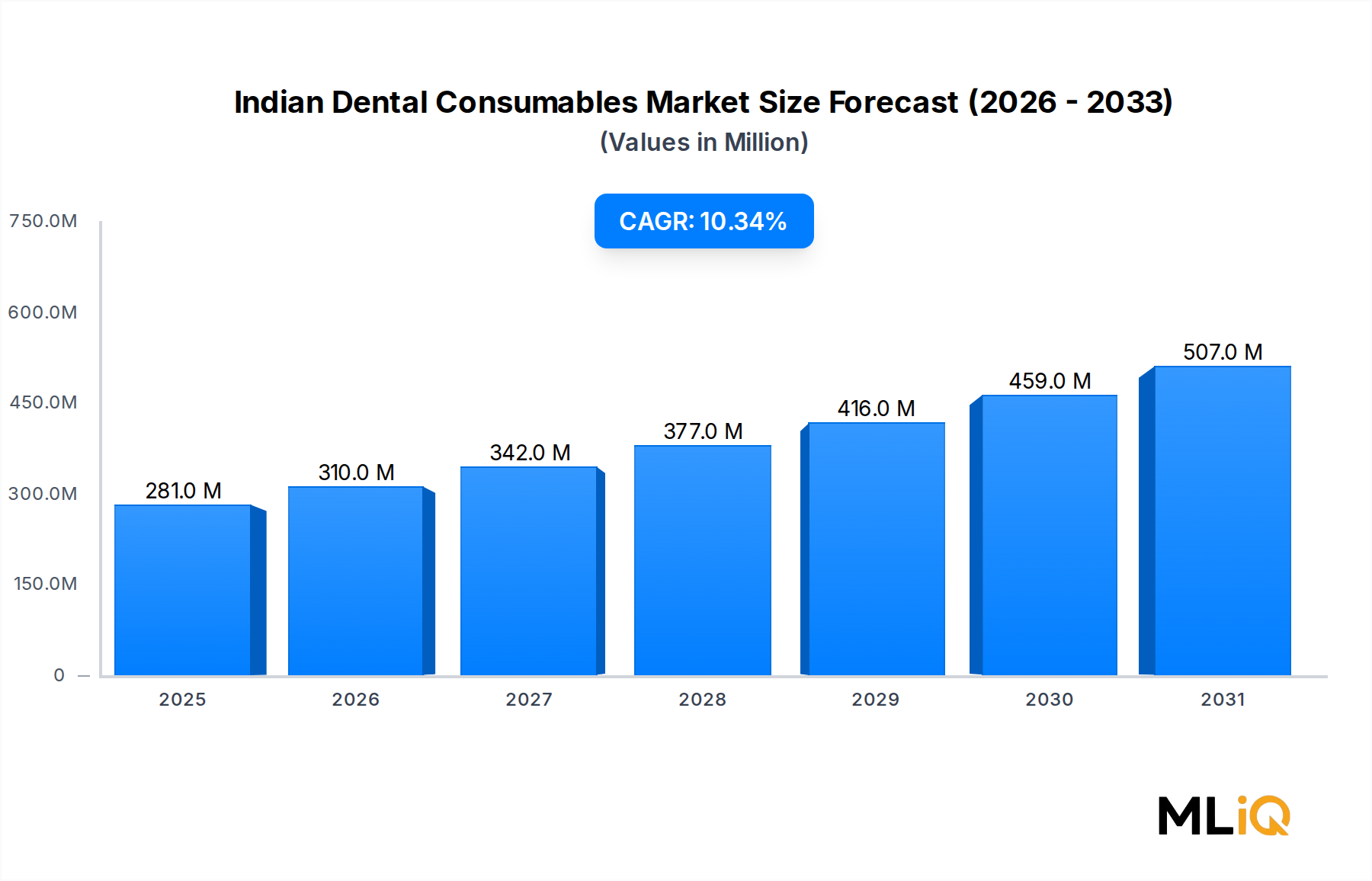

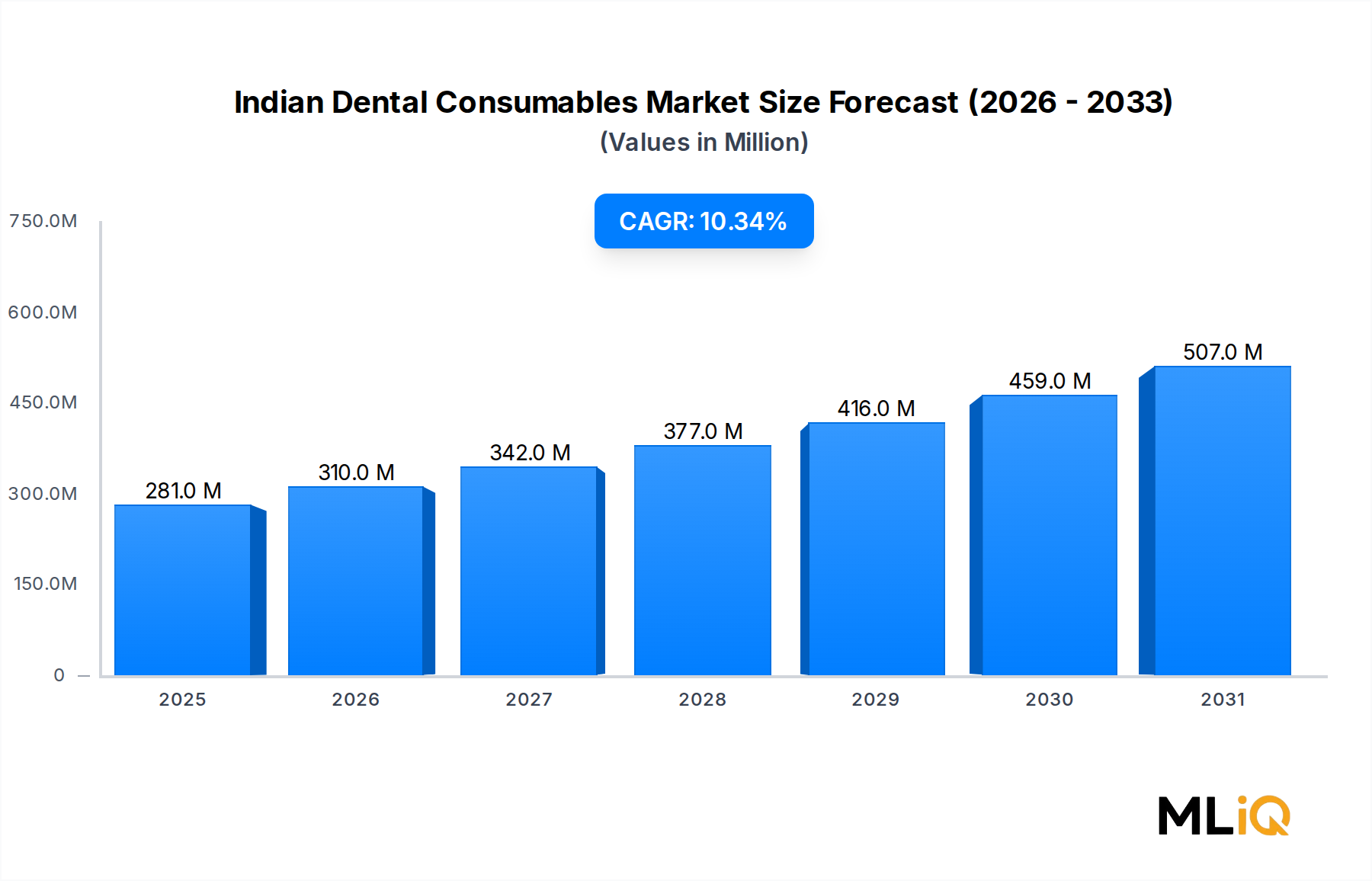

The Indian Dental Consumables Market is valued at $281.28 million as of the base assessment period and is projected to expand at a compound annual growth rate of 10.3% through 2033, reflecting one of the most dynamic growth trajectories across the broader Asia Pacific life sciences sector. This growth is anchored in a convergence of structural healthcare reforms, rising disposable incomes, expanding dental tourism infrastructure, and a rapidly professionalizing dental services industry across both urban and semi-urban geographies.

Demand is being propelled by a swelling patient base that increasingly prioritizes aesthetic and preventive dentistry. The Indian Council of Medical Research estimates that more than 50% of India's population suffers from some form of dental disease, yet dental visit rates remain comparatively low, signaling a significant latent demand pool that is now being unlocked through government-backed oral health programs and private insurance penetration. Under the Ayushman Bharat initiative, partial dental coverage expansions have begun to channel formal patient volume into organized dental practice networks.

From a macro perspective, India's healthcare expenditure as a percentage of GDP has risen from roughly 1.3% to 2.1% over the past decade, creating favorable downstream conditions for consumable procurement. The proliferation of dental chains — a format that now accounts for an estimated 22% of organized dental care delivery — is shifting procurement toward high-volume, standardized consumable contracts, benefiting large-format suppliers and global brands with distribution depth.

Key demand drivers include the increasing adoption of digital dentistry workflows, the accelerating uptake of single-visit restorative procedures, and growing awareness of minimally invasive endodontic techniques. Simultaneously, the market is witnessing structural shifts in consumable mix — moving from purely metallic restorations toward polymer-based and ceramic composites, driven by patient preference for aesthetics and practitioner preference for biocompatible outcomes.

The competitive landscape remains moderately fragmented, with global multinationals competing alongside agile domestic players who leverage cost efficiency and localized supply chains. The forecast period through 2033 is expected to see consolidation, as organized dental service providers increasingly standardize procurement and favor suppliers with integrated product portfolios spanning restoration, endodontics, impression materials, and disposables. Capital inflows from private equity into the Indian dental services sector further catalyze consumable volume growth, making this one of the most investable sub-segments within the broader South Asian life sciences ecosystem.

Within the Indian Dental Consumables Market, the dental restoration sub-segment — encompassing metals, polymers, ceramics, and biomaterials — commands the largest revenue share and is expected to maintain its leading position through 2033. This dominance is attributable to the high procedural frequency of restorative dentistry, the breadth of material categories involved, and the increasing complexity of restoration protocols that require multiple co-used consumable types per procedure.

Metallic restorations, historically the workhorse of Indian dental practice due to their durability and cost-effectiveness, continue to hold volume significance in Tier 2 and Tier 3 markets. Dental amalgam and base metal alloys remain in clinical use despite global regulatory scrutiny, largely because their cost-per-unit remains accessible for lower-income patient segments. However, the share of metallic materials is under secular pressure as composite resins, ceramic inlays, and glass ionomer cements gain adoption.

Polymer-based composites have emerged as the fastest-growing sub-category within restoration, growing at an estimated 12–14% annually within the segment. The shift is driven by patient demand for tooth-colored restorations, improved material formulations that match dentin hardness more accurately, and practitioner familiarity gained through enhanced dental school curricula. Leading suppliers have responded with localized product lines engineered for the high humidity conditions prevalent in Indian clinical environments, which can affect bonding agent performance and composite polymerization.

Ceramics represent the premium end of the restoration market and are gaining traction in urban dental practices, specialist clinics, and dental chains that cater to middle- and upper-income demographics. CAD/CAM-compatible ceramic blocks, zirconia discs, and lithium disilicate systems are increasingly being procured by clinics investing in in-house milling capabilities — a trend aligned with the expansion of the Dental Imaging Market and digital workflow adoption. The unit economics of ceramic-based restorations offer practitioners substantially higher margins compared to composite procedures, incentivizing upselling behavior.

Biomaterials constitute a high-value, innovation-intensive corner of the restorative segment. Products such as bioactive glasses, hydroxyapatite-based composites, and calcium silicate cements are gaining clinical acceptance, particularly in minimally invasive protocols and pediatric dentistry. This sub-category intersects with broader developments in the Dental Biomaterials Market, where research investment from academic institutions and multinational R&D centers is accelerating the commercialization pipeline.

Key players capturing share within the restoration segment include Dentsply Sirona Inc., 3M Company, and Prime Dental Products Pvt Ltd, each with distinct positioning — global formulation depth, innovation leadership, and domestic cost competitiveness respectively. Institut Straumann AG has also extended its restoration portfolio through acquisitions, seeking to capture value across the full restorative workflow. The segment's share is not merely consolidating but actively expanding in absolute terms as procedural complexity and material diversity increase, generating higher consumable spend per treatment episode across the market.

The Indian Dental Consumables Market is shaped by a set of quantifiable drivers and structural constraints that collectively determine its 10.3% CAGR trajectory through 2033.

On the demand side, India's dental practitioner base has grown to over 290,000 registered dentists, a figure expanding at roughly 6% annually as dental college output increases. Each incremental practitioner represents a recurring consumable procurement node, directly translating institutional enrollment into market volume. Urban dental chains, which have grown from fewer than 500 outlets in 2015 to over 3,200 by 2024, standardize and amplify per-outlet consumable spend.

The rise of cosmetic and elective dentistry is a quantitatively significant driver. Whitening procedures, composite veneers, and clear aligner therapies have grown to represent an estimated 18% of total dental procedure revenue in metro markets, each requiring dedicated consumable categories. This has driven premiumization within the market, increasing average revenue per procedure.

Government procurement programs represent another structured driver. The National Oral Health Programme allocates funding for dental consumables in public health settings, creating a non-discretionary procurement channel that underpins baseline volume even during economic slowdowns.

Constraints include price sensitivity at the practitioner level, particularly among solo practitioners who represent over 65% of the installed dental practice base. These practitioners prioritize lowest landed cost over clinical innovation, limiting premium product penetration. Import duty structures on certain consumable raw materials and finished goods add 10–25% to effective landed cost for international products, constraining the growth of premium segments and incentivizing import substitution.

Supply chain fragmentation in cold-chain-sensitive categories — such as certain bonding agents and biologic-based materials — creates quality inconsistency in non-metro distribution, indirectly acting as a market constraint by reducing clinical confidence in some product categories. Regulatory harmonization with global standards under the Medical Devices Rules framework is ongoing but creates transitional compliance costs for mid-sized domestic manufacturers.

The competitive landscape of the Indian Dental Consumables Market is defined by a blend of multinational corporations with broad portfolios and domestic manufacturers with cost and distribution advantages.

INDIDENT MEDICAL DEVICES: A domestic manufacturer focused on endodontic and restorative consumables, leveraging cost-competitive production for Tier 2 and Tier 3 market penetration with an expanding distribution network across 18 Indian states.

ZIMMER BIOMET HOLDINGS, INC.: A global leader in dental implants and regenerative materials, Zimmer Biomet maintains a significant presence in India's premium restorative and implant consumable segments through its established distributor relationships and clinical education programs.

PRIME DENTAL PRODUCTS PVT LTD: One of India's most recognized domestic dental consumable brands, Prime Dental competes across restoration, endodontics, and impression materials with ISO-certified manufacturing and strong penetration into standalone clinic networks.

DANAHER CORPORATION: Operating through its Envista Holdings dental segment, Danaher brings global R&D capabilities and a diversified consumable portfolio including imaging and restorative products, with growing traction in organized dental chain accounts in India.

MANI, INC.: A Japan-headquartered precision instruments manufacturer with strong presence in the Indian endodontic files and burs category, known for consistent quality and competitive pricing that appeals to both institutional and individual practitioner buyers.

ADIN DENTAL IMPLANT SYSTEMS LTD.: An Israel-based implant and biomaterial specialist expanding in the Indian market through direct distribution partnerships, targeting the growing mid-premium implantology segment.

INSTITUT STRAUMANN AG: A global benchmark in implant and restorative dentistry, Straumann has invested in India-specific market development, including academic partnerships and clinical training centers that drive adoption of its premium consumable portfolio.

ANAND MEPRODUCTS PVT. LTD.: A specialized Indian manufacturer in the dental impression materials and disposables categories, competing primarily on pricing and domestic supply chain reliability for independent dental clinics.

3M COMPANY: A diversified materials science leader, 3M holds strong positions in dental adhesives, composites, and orthodontic consumables in India, supported by its global formulation infrastructure and local regulatory compliance investment.

OSSTEM IMPLANT CO., LTD.: A South Korea-based implant consumable leader with aggressive pricing and expanding Indian distribution, targeting the rapidly growing mid-market implantology segment.

DENTSPLY SIRONA INC.: A comprehensive dental solutions provider with the broadest consumable portfolio in the market, spanning endodontics, restorative, impression, and preventive categories, maintaining category leadership through continuous product launches and dental chain supply agreements.

January 2024: Institut Straumann AG announced a partnership with a leading Indian dental education consortium to establish three clinical training centers in Mumbai, Delhi, and Bengaluru, aimed at accelerating adoption of its premium biomaterial and restorative consumable lines.

March 2024: The Central Drugs Standard Control Organisation finalized updated classification norms for Class B dental consumables under India's Medical Devices Rules, introducing mandatory performance testing for composite resins and impression materials, affecting the compliance timelines of over 40 domestic manufacturers.

May 2024: 3M Company launched a localized composite resin formulation specifically engineered for high-humidity tropical clinical environments, targeting the approximately 70% of Indian dental practices located in high-humidity geographic zones.

August 2024: Dentsply Sirona Inc. expanded its Indian distribution infrastructure by signing a national distribution agreement with a major pharmaceutical logistics provider, aiming to extend premium endodontic consumable reach to 200+ additional Tier 2 cities.

October 2024: Osstem Implant Co., Ltd. reduced its Indian market pricing on core implant abutment consumables by an estimated 15% following the commissioning of a regional warehousing hub in Pune, intensifying competitive pressure in the mid-premium implant consumable segment.

February 2025: Prime Dental Products Pvt Ltd received ISO 13485:2016 certification renewal for its expanded manufacturing facility in Gujarat, adding capacity for dental sealants and bonding agents to meet rising domestic demand.

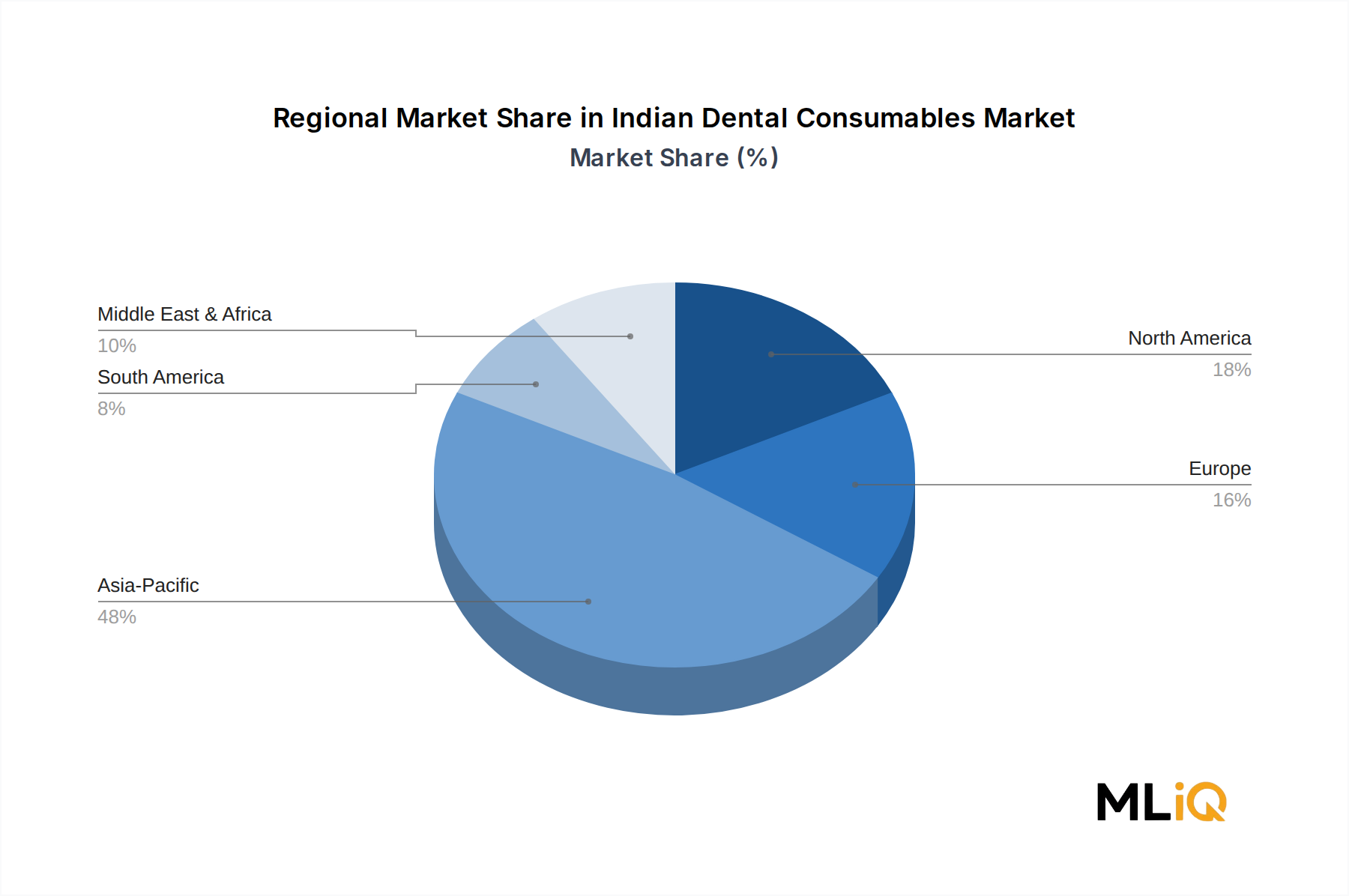

The Indian Dental Consumables Market, while geographically centered in India, is analyzed by its multinational suppliers and investors in the context of the broader Asia Pacific and global regional competitive framework.

Asia Pacific represents the most dynamic regional growth engine for dental consumable supply chains feeding into India, recording an estimated regional CAGR of 11.2% through 2033. India itself, as a sub-region within Asia Pacific, is outpacing peers including Indonesia and Vietnam in absolute consumable demand growth, driven by its large dentist base and organized dental chain expansion. China, as the dominant Asia Pacific market, serves as both a competitive manufacturing benchmark and a sourcing hub for raw ceramic and polymer inputs used in Indian dental manufacturing.

North America, representing the most mature regional market globally, contributes to the Indian Dental Consumables Market primarily as a technology and formulation origin point. Leading American multinationals hold an estimated 28–32% combined import value share in premium Indian dental consumable categories. North America's growth in dental consumables is projected at approximately 5.8% CAGR, reflecting market saturation relative to the India opportunity.

Europe, particularly Germany and Switzerland — home to Dentsply Sirona and Institut Straumann respectively — functions as the primary innovation and regulatory benchmark for the Indian premium segment. European-origin products command pricing premiums of 20–35% over domestically manufactured equivalents, limiting volume share but sustaining high value share in the implant and ceramic restoration categories. European regional CAGR for dental consumables is estimated at 4.9%.

Middle East & Africa (MEA) represents an adjacent growth corridor for Indian dental consumable exporters, with GCC dental markets increasingly sourcing from Indian manufacturers given their cost competitiveness and improving quality certifications. Indian exports to MEA in dental consumables have grown at approximately 14% annually over 2021–2024, indicating a meaningful reverse-flow trade dynamic.

South America, while not a primary market for Indian dental consumable trade, represents a comparative benchmark where mid-tier domestic manufacturing models similar to India's are developing, providing strategic intelligence on localization strategies that global players may replicate in the Indian context.

The customer base of the Indian Dental Consumables Market is stratified across four primary segments: independent solo practitioners, multi-chair clinic groups, organized dental chains, and public sector dental institutions.

Independent solo practitioners constitute the numerically dominant segment, representing over 65% of the total practitioner base. This cohort is highly price-sensitive, with purchase decisions driven primarily by landed cost-per-unit, product familiarity, and proximity of the local distributor. Brand loyalty is moderate but can be disrupted by price differentials exceeding 10–12%, making this segment a competitive battleground for domestic manufacturers. Procurement is typically transactional, occurring through local dental supply dealers on a monthly or as-needed basis, with limited advance planning.

Multi-chair clinic groups occupy an intermediate segment, blending price sensitivity with a growing orientation toward clinical performance and patient outcome metrics. These buyers are more receptive to product trials, clinical evidence presentations, and dental representative engagement. Their purchasing volumes justify direct engagement from regional distributor sales forces, and they show increasing interest in consumable categories aligned with the Oral Care Market's premiumization trend.

Organized dental chains represent the highest-value procurement segment per outlet, driven by standardized protocols, bulk purchasing agreements, and a preference for suppliers offering integrated product portfolios, training support, and consignment or credit terms. This segment has shifted toward vendor consolidation, with leading chains working with fewer than five primary consumable suppliers nationally. Digital procurement portals and e-tendering mechanisms are emerging within this segment, compressing traditional distributor margins.

Public sector dental institutions procure through government tender mechanisms, prioritizing lowest bid compliance within specification parameters. This segment values durability, regulatory certification, and domestic manufacturing credentials. While margin-compressed, it provides volume stability and reference site value for domestic manufacturers.

A notable behavioral shift observed in recent cycles is the increasing influence of dental school training on brand preference among newly qualified practitioners, prompting suppliers to invest in academic seeding programs as a long-term demand cultivation strategy.

The supply chain architecture of the Indian Dental Consumables Market is characterized by a dual dependency on imported specialty raw materials and a domestically concentrated manufacturing and distribution layer.

Key upstream inputs include dental-grade zirconia, used in ceramic restorations and sourced predominantly from China and Australia, where price volatility has ranged between **8

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 10.3% from 2020-2034 |

| Segmentation |

|

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Comprehensive validation mechanisms ensuring market intelligence accuracy, reliability, and adherence to international standards.

500+ data sources cross-validated

200+ industry specialists validation

NAICS, SIC, ISIC, TRBC standards

Continuous market tracking updates

Factors such as are projected to boost the Indian Dental Consumables Market market expansion.

Key companies in the market include INDIDENT MEDICAL DEVICES, ZIMMER BIOMET HOLDINGS, INC., PRIME DENTAL PRODUCTS PVT LTD, DANAHER CORPORATION, MANI, INC., ADIN DENTAL IMPLANT SYSTEMS LTD., INSTITUT STRAUMANN AG, ANAND MEPRODUCTS PVT., LTD., 3M COMPANY, OSSTEM IMPLANT CO., LTD., DENTSPLY SIRONA INC..

The market segments include Product, Endodontics, Other Dental Consumables.

The market size is estimated to be USD 281.28 million as of 2022.

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3200, USD 2012, and USD 4370 respectively.

The market size is provided in terms of value, measured in million and volume, measured in .

Yes, the market keyword associated with the report is "Indian Dental Consumables Market," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Indian Dental Consumables Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.