1. What are the major growth drivers for the Human Coagulation Factor VII Market by Product market?

Factors such as are projected to boost the Human Coagulation Factor VII Market by Product market expansion.

+1 2315155523

Market Lens IQ is a global market intelligence and strategic consulting firm delivering advanced syndicated research reports, customized industry analysis, competitive intelligence, and data-driven advisory solutions to organizations across international markets. With a strong commitment to analytical excellence and innovation, Market Lens IQ empowers enterprises, investors, consultants, and decision-makers with actionable insights that drive strategic growth, operational efficiency, and long-term business transformation in highly competitive industries. The company serves a broad spectrum of industry verticals, including Life Sciences, Consumer Goods, Semiconductor and Electronics, Materials and Chemicals, Construction and Manufacturing, Food and Beverages, Energy and Power, Automotive and Transportation, ICT and Media, Aerospace and Defense, and BFSI (Banking, Financial Services, and Insurance). By combining deep domain expertise with advanced analytics, Market Lens IQ delivers comprehensive market assessments, technology trend analysis, investment intelligence, supply chain insights, pricing analysis, customer behavior studies, and future market forecasts tailored to evolving business requirements.

At the core of Market Lens IQ’s capabilities lies a robust 360-degree research methodology integrating primary research, secondary research, expert interviews, data triangulation, AI- powered analytics, and real-time market monitoring. Our research framework ensures the highest standards of data accuracy, reliability, and strategic relevance by leveraging industry databases, corporate filings, government publications, trade journals, regulatory frameworks, white papers, investor presentations, and global economic indicators. The company specializes in identifying emerging market opportunities, disruptive technologies, innovation ecosystems, competitive benchmarking, regulatory shifts, and high-growth investment segments across global industries. Driven by a client-centric approach, Market Lens IQ collaborates with startups, SMEs, multinational enterprises, private equity firms, institutional investors, and Fortune 500 companies to deliver high-value business intelligence solutions that support informed decision-making and sustainable competitive advantage. Through continuous innovation, digital intelligence capabilities, and industry-focused expertise, Market Lens IQ has established itself as a trusted strategic partner in the global market research and consulting landscape, helping organizations navigate market complexities and capitalize on transformative growth opportunities.

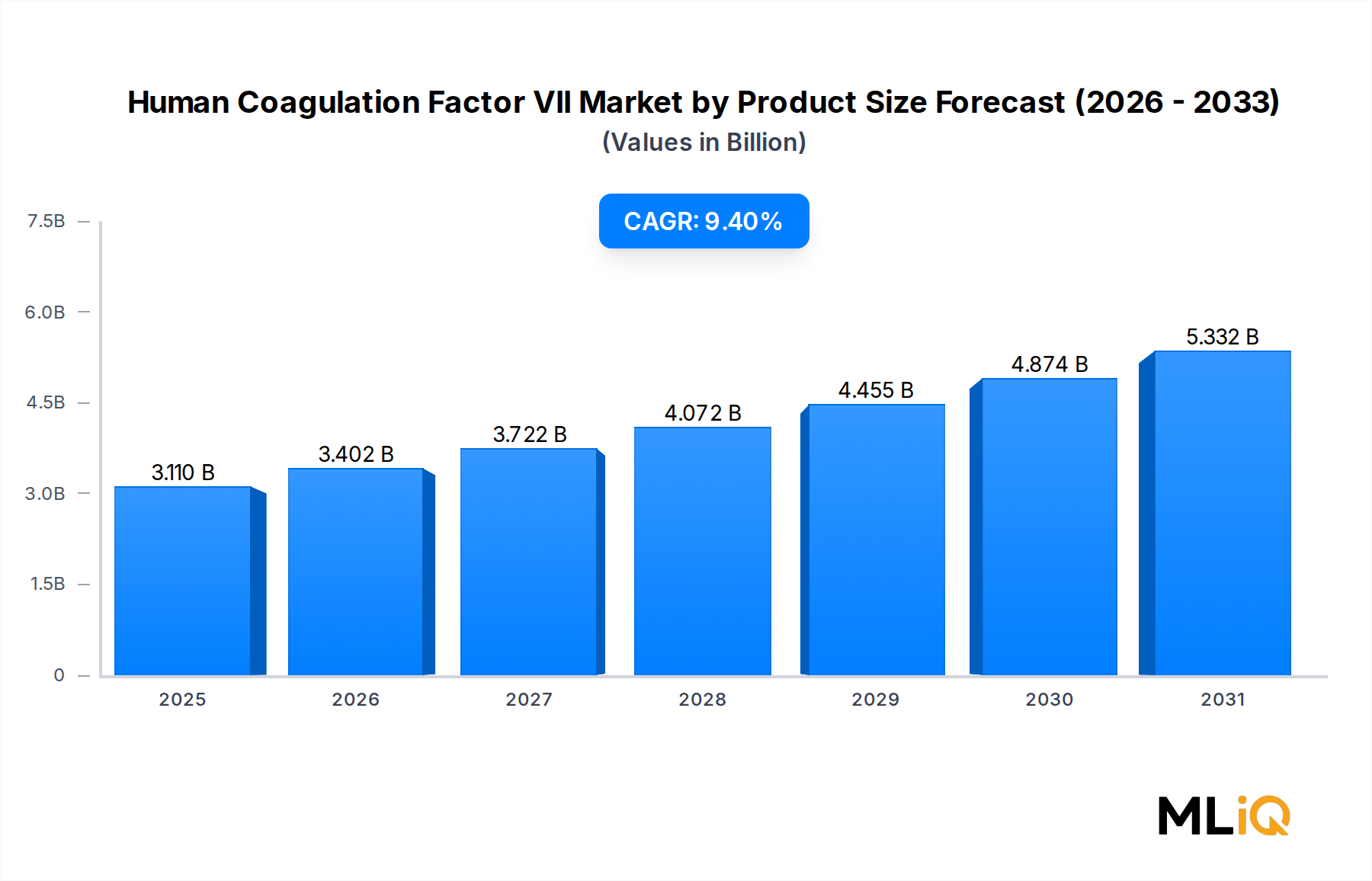

The global Human Coagulation Factor VII Market by Product was valued at $3.11 billion in the base year and is projected to expand at a compound annual growth rate of 9.4% through the forecast period of 2025 to 2033, reflecting robust and sustained demand across hemophilia management, surgical applications, and broader hemorrhagic disorder treatment protocols. This trajectory positions the market as one of the more dynamically evolving segments within the broader life sciences sector, underpinned by a convergence of clinical, demographic, and biotechnological forces.

At its core, demand for Factor VII — a serine protease integral to the extrinsic coagulation cascade — is being driven by the rising global burden of hemophilia A and B, congenital Factor VII deficiency, and the expanding use of bypassing agents in patients who develop inhibitors to standard replacement therapies. The World Federation of Hemophilia has consistently documented increases in diagnosed patient populations globally, a trend that directly amplifies therapeutic consumption.

The bifurcation of the product landscape into recombinant and plasma-derived modalities is a defining structural feature. Recombinant Factor VIIa products, most prominently NovoSeven from Novo Nordisk, have established clinical dominance in high-income markets where safety profiles and pathogen-free manufacturing are prioritized. Meanwhile, plasma-derived Factor VII retains a meaningful share in cost-sensitive and developing-market contexts, where established fractionation infrastructure and lower price points sustain adoption.

From a macroeconomic standpoint, several tailwinds reinforce the 9.4% CAGR projection. These include increased healthcare expenditure in Asia Pacific markets such as China and India, the maturation of national bleeding disorder registries, favorable regulatory pathways for biosimilar recombinant therapies, and the gradual expansion of universal healthcare coverage in emerging economies. The pipeline of next-generation extended half-life recombinant Factor VII analogs also introduces a future demand inflection point, as these therapies promise reduced dosing frequency and improved patient adherence.

On the supply side, the market is served by a concentrated group of multinational pharmaceutical and plasma-product companies, each operating under stringent Good Manufacturing Practice frameworks. Vertical integration and strategic plasma sourcing alliances are becoming competitively necessary as raw material availability tightens. Hospital networks and ambulatory surgical centers represent the two primary end-user channels, with hospitals commanding the majority share due to the acute-care nature of Factor VII indication management.

The forward-looking outlook through 2033 is decidedly constructive. With gene therapy for hemophilia advancing through late-stage trials, there exists a long-term substitution risk for recombinant Factor VII; however, near- and mid-term dynamics strongly favor continued volume and value growth in conventional factor replacement and bypassing agent categories. The combination of unmet diagnostic capacity in lower-income regions and pipeline-driven premium pricing in high-income regions ensures a durable and diversified growth foundation.

Within the Human Coagulation Factor VII Market by Product, the Recombinant Factor VII sub-segment consistently commands the largest revenue share and is the primary growth engine across the forecast horizon. This dominance is attributable to multiple reinforcing clinical, regulatory, and commercial factors that collectively insulate the recombinant segment from competitive erosion.

Recombinant Factor VIIa was first approved in the 1990s for the management of bleeding episodes in hemophilia A and B patients with inhibitors — a critically underserved population for whom standard Factor VIII or IX replacement is ineffective. The mechanism of action, involving direct activation of Factor X on the surface of activated platelets independent of Factors VIII and IX, renders it uniquely valuable as a bypassing agent. Subsequent label expansions to cover congenital Factor VII deficiency, Glanzmann's thrombasthenia, and perioperative bleeding management in various surgical contexts have progressively widened the addressable patient base.

Novo Nordisk's NovoSeven (eptacog alfa) remains the global market leader within this sub-segment, benefiting from decades of clinical evidence, established reimbursement frameworks in North America and Europe, and a deeply entrenched prescriber base. The company has invested substantially in clinical extension studies and post-marketing safety surveillance, reinforcing its regulatory standing across multiple jurisdictions. Competing recombinant offerings from other manufacturers remain limited in number due to the complex manufacturing requirements for recombinant serine proteases, the significant capital investment required for mammalian cell culture infrastructure, and the difficulty of establishing clinical non-inferiority against a well-validated reference product.

The preference for recombinant Factor VII over plasma-derived alternatives in developed markets is partly safety-driven: recombinant products eliminate the theoretical risk of pathogen transmission inherent in plasma-derived manufacturing, a concern that gained renewed regulatory attention following the hemophilia community's historical exposure to HIV and hepatitis C through contaminated plasma products in the 1980s. Regulatory agencies in the United States, European Union, and Japan have generally favored recombinant therapies in their reimbursement and guidance frameworks.

In terms of revenue concentration, North America and Europe together account for the majority of recombinant Factor VII revenues, driven by high per-patient treatment costs, comprehensive insurance coverage for rare bleeding disorders, and active hemophilia treatment center networks. The average annual cost of treatment for an inhibitor patient utilizing recombinant Factor VIIa can reach several hundred thousand USD, reflecting both the high dosing frequency and unit price of the product.

However, the recombinant sub-segment's dominance is not static. Biosimilar and follow-on recombinant Factor VIIa candidates are advancing through regulatory pipelines in multiple geographies, and several companies in Asia — particularly in China and India — are developing domestically manufactured recombinant alternatives to reduce import dependency and lower treatment costs. This biosimilar pressure is expected to introduce moderate pricing headwinds post-2027, though volume gains from expanded access are likely to offset per-unit revenue compression at the aggregate market level.

Extended half-life recombinant Factor VIIa variants, such as eptacog beta and albumin-fused constructs, represent the next phase of product evolution. These differentiated formulations offer less frequent dosing intervals and potentially improved trough factor activity, which may justify premium pricing and displace first-generation recombinant products over time. Companies including CSL Behring and Pfizer Inc. are positioned to participate in this next-generation recombinant landscape through their respective pipeline assets and manufacturing capabilities.

The recombinant segment's share is therefore consolidating at premium tiers while simultaneously broadening its volume base in emerging markets, creating a two-speed dynamic that will shape competitive strategy through the end of the forecast period.

The Human Coagulation Factor VII Market by Product is shaped by a constellation of demand accelerators and structural constraints, each operating at different timescales and geographies.

Driver 1: Rising Hemophilia Diagnosis Rates. The World Federation of Hemophilia's Annual Global Survey documented over 300,000 identified individuals with inherited bleeding disorders globally as of recent reporting cycles, yet estimates suggest that diagnosed populations represent a fraction of the actual disease burden, particularly in sub-Saharan Africa and South Asia. As national newborn screening programs expand and hematology infrastructure matures in emerging economies, new patient identification rates are expected to increase materially, directly expanding the Factor VII addressable market.

Driver 2: Surgical Volume Recovery and Expansion. The post-pandemic normalization of elective and semi-elective surgical procedures has restored demand for hemostatic agents in operative settings. Factor VII is deployed perioperatively in patients with coagulopathies undergoing cardiac surgery, liver transplantation, and trauma interventions. Global surgical volume growth, estimated at low- to mid-single-digit percentages annually, sustains this application channel.

Driver 3: Inhibitor Patient Population Growth. As patients with severe hemophilia receive more intensive and earlier factor replacement therapy, a subset develops inhibitory antibodies that necessitate bypassing agents including Factor VIIa. Growing treatment intensity in both developed and developing markets is paradoxically expanding the inhibitor-complicated patient population, which drives premium Factor VIIa demand.

Constraint 1: High Treatment Costs and Reimbursement Barriers. The annual cost burden of recombinant Factor VIIa therapy for inhibitor patients creates significant access friction in lower-middle-income countries. Payer resistance and formulary restrictions in several European markets have constrained volume uptake even where clinical need exists.

Constraint 2: Gene Therapy Pipeline Risk. Approvals of gene therapies for hemophilia A and B, such as valoctocogene roxaparvovec and etranacogene dezaparvovec, introduce a substitution risk for the longer-term factor replacement market. While Factor VII-specific gene therapy remains earlier in development, the broader narrative creates investor and procurement uncertainty.

Constraint 3: Plasma Supply Volatility. For the plasma-derived segment, collection center disruptions — as observed during 2020 and 2021 — create supply chain fragility that limits product availability and constrains manufacturing throughput for plasma-derived Factor VII producers.

The competitive landscape of the Human Coagulation Factor VII Market by Product is characterized by a high degree of concentration among established pharmaceutical and plasma-product multinationals, with emerging biosimilar entrants beginning to challenge the status quo in select geographies.

Sanofi: A major player in rare blood disorder therapeutics, Sanofi has built a comprehensive hemophilia portfolio that positions it as a strategic participant in the broader coagulation factor space, with particular strength in long-acting and subcutaneous formulations.

CSL Behring: One of the world's leading plasma-derived protein manufacturers, CSL Behring maintains extensive plasma fractionation capacity globally and is a key supplier of plasma-derived coagulation factors, including Factor VII, across hospital and specialty pharmacy channels.

ProSpec: Operates primarily in the research-grade and laboratory supply segment of coagulation proteins, providing high-purity Factor VII for diagnostic reagent and research applications rather than clinical replacement therapy.

Novo Nordisk: The originator and global leader in recombinant Factor VIIa (NovoSeven), Novo Nordisk commands the largest revenue share in the recombinant segment and continues to invest in next-generation eptacog constructs to defend market position against biosimilar entrants.

Grifols USA LLC: A global plasma-derived products specialist, Grifols maintains a vertically integrated plasma supply chain — from collection centers to fractionation — that provides cost and availability advantages in plasma-derived Factor VII manufacturing.

Bayer AG: Historically active in the hemophilia treatment space through its Factor VIII and IX products, Bayer AG's presence in the coagulation factor ecosystem provides strategic context for potential Factor VII portfolio development and partnership activity.

Octapharma AG: A privately held plasma products company with significant European manufacturing depth, Octapharma AG produces a range of plasma-derived coagulation factors and competes effectively in European and select emerging market geographies.

Pfizer Inc.: Through its rare disease and biologics franchises, Pfizer Inc. maintains capabilities relevant to recombinant protein manufacturing and has participated in the hemophilia treatment market through both proprietary products and strategic licensing arrangements.

Tany Technogene Ltd.: A specialized biotechnology firm active in coagulation factor research and development, Tany Technogene Ltd. represents the segment of smaller innovators contributing to pipeline diversification in the Factor VII space.

Baxter International Inc.: With a long history in intravenous therapies and specialty biopharmaceuticals, Baxter International Inc. has established distribution and hospital supply relationships that support market penetration for coagulation factor products.

January 2024: Novo Nordisk announced updated long-term safety and efficacy data for eptacog beta in patients with hemophilia A and B with inhibitors, reinforcing its regulatory submissions in key Asia Pacific markets including Japan and South Korea.

March 2024: CSL Behring disclosed an expansion of its plasma fractionation facility in Marburg, Germany, increasing manufacturing capacity for plasma-derived coagulation factors including Factor VII, with the expansion expected to be fully operational by 2026.

June 2024: Grifols USA LLC received FDA acknowledgment of its supplemental Biologics License Application for enhanced pathogen reduction steps in its plasma-derived coagulation factor manufacturing processes, reinforcing product safety profiles.

August 2024: A Phase II clinical trial for an albumin-fused recombinant Factor VIIa construct, sponsored by a European biotech consortium, reported positive interim data demonstrating extended half-life performance with an acceptable safety profile in congenital Factor VII deficiency patients.

October 2024: Octapharma AG secured reimbursement approval for its plasma-derived Factor VII product in three additional Middle Eastern markets through a GCC-level regulatory submission, expanding geographic revenue diversification.

February 2025: The European Medicines Agency published updated guidelines on the clinical development requirements for biosimilar recombinant Factor VIIa products, providing regulatory clarity that is expected to accelerate biosimilar entry timelines within the EU by 2027 to 2028.

April 2025: Baxter International Inc. entered a co-promotion agreement with a regional distributor network across Southeast Asia to expand hospital-level access to its specialty coagulation products portfolio, targeting the ASEAN market.

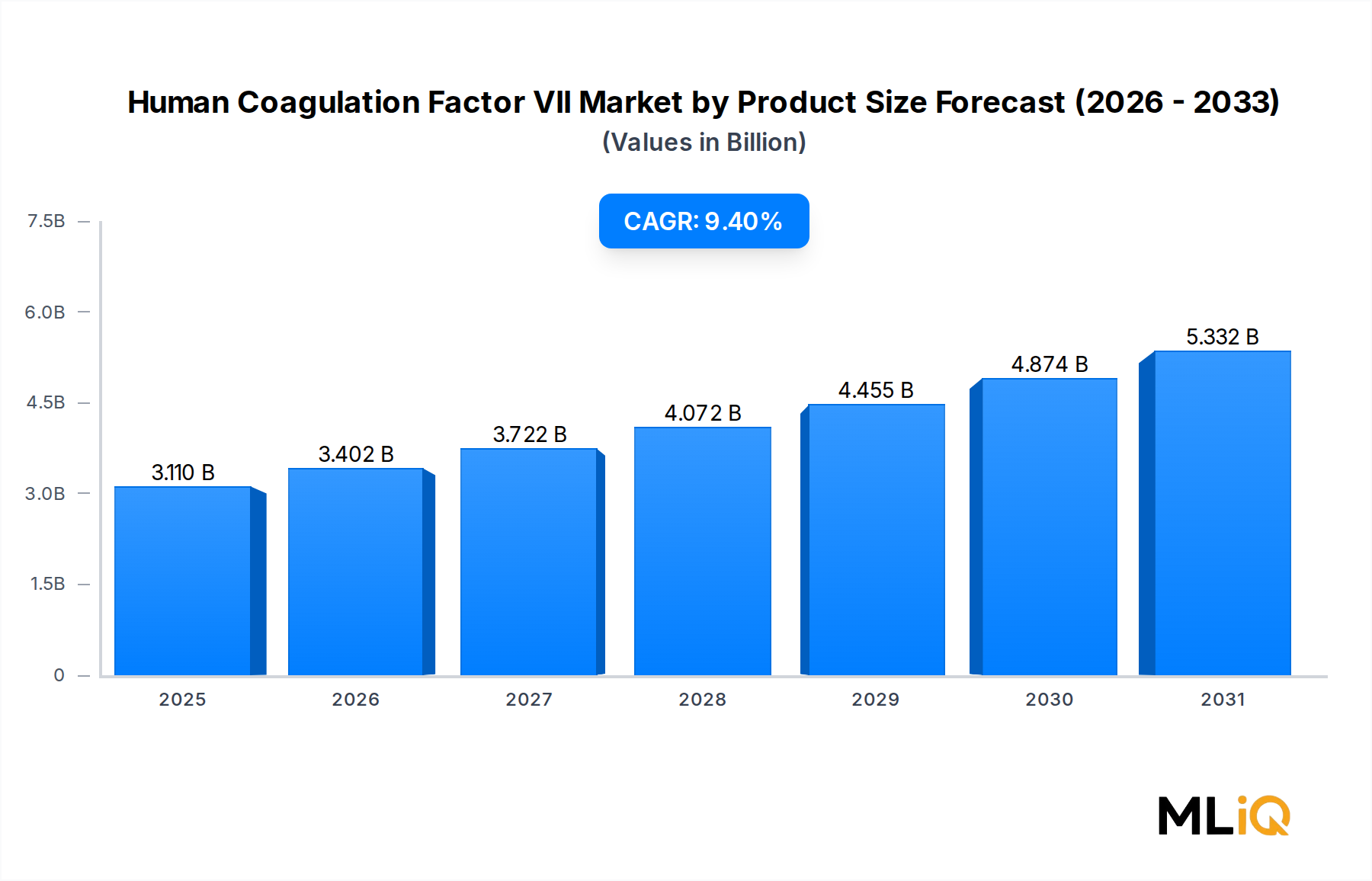

The geographic distribution of revenues within the Human Coagulation Factor VII Market by Product reflects disparate levels of healthcare infrastructure, reimbursement sophistication, diagnosed patient density, and regulatory development across global regions.

North America represents the most mature and highest-revenue region, accounting for an estimated 38% to 42% of global market value. The United States is the dominant contributor, supported by comprehensive hemophilia treatment center networks, favorable reimbursement through commercial insurance and Medicaid, and a high prevalence of diagnosed inhibitor patients. Canada and Mexico contribute additional but comparatively modest volumes. The North American regional CAGR is estimated at approximately 7.5% to 8.0%, reflecting market maturity and pricing pressure from managed care negotiations, partially offset by label expansions and premium pricing of next-generation recombinant products.

Europe constitutes the second-largest regional market, with Germany, the United Kingdom, France, Italy, and Spain as the principal revenue contributors. The region benefits from long-established hemophilia treatment center infrastructure and national patient registries. European revenues are subject to ongoing health technology assessment-driven price negotiations, which moderate growth relative to the global average. The Nordics demonstrate above-average treatment intensity per capita, while Eastern European markets show accelerating growth as reimbursement frameworks mature. European CAGR is estimated at 8.0% to 8.5%.

Asia Pacific is the fastest-growing region in the Human Coagulation Factor VII Market by Product, with a projected CAGR of 11.5% to 12.5% through 2033. China and India represent the largest volume opportunities, driven by massive underdiagnosed hemophilia populations, expanding national health insurance coverage, and government-supported rare disease treatment programs. Japan and South Korea maintain mature market characteristics with premium product access. The ASEAN bloc is emerging as a secondary growth cluster, with Indonesia, Thailand, and Vietnam showing rising diagnostic and treatment investment.

Middle East and Africa exhibit a bifurcated picture. The GCC nations — particularly Saudi Arabia, the UAE, and Kuwait — maintain well-funded healthcare systems that support premium Factor VII product access at rates comparable to European benchmarks. Sub-Saharan Africa remains largely underserved, with access concentrated in South Africa and select urban centers. Regional CAGR for Middle East and Africa is estimated at 9.0% to 10.0%.

South America, anchored by Brazil and Argentina, is advancing through a period of healthcare system formalization. Brazil's public health system (SUS) has historically supported hemophilia treatment access through centralized purchasing, creating a volume-stable but price-controlled market dynamic. South American C

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 9.4% from 2020-2034 |

| Segmentation |

|

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Comprehensive validation mechanisms ensuring market intelligence accuracy, reliability, and adherence to international standards.

500+ data sources cross-validated

200+ industry specialists validation

NAICS, SIC, ISIC, TRBC standards

Continuous market tracking updates

Factors such as are projected to boost the Human Coagulation Factor VII Market by Product market expansion.

Key companies in the market include Sanofi, CSL Behring, ProSpec, Novo Nordisk, Grifols USA LLC, Bayer AG, Octapharma AG, Pfizer Inc., Tany Technogene Ltd., Baxter International Inc..

The market segments include Product, Application, End User.

The market size is estimated to be USD 3.11 billion as of 2022.

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3200, USD 4425, and USD 7412 respectively.

The market size is provided in terms of value, measured in billion and volume, measured in .

Yes, the market keyword associated with the report is "Human Coagulation Factor VII Market by Product," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Human Coagulation Factor VII Market by Product, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.