1. What are the major growth drivers for the Wooden Floor Market market?

Factors such as are projected to boost the Wooden Floor Market market expansion.

+1 2315155523

Wooden Floor Market

Wooden Floor Market

Market Lens IQ is a global market intelligence and strategic consulting firm delivering advanced syndicated research reports, customized industry analysis, competitive intelligence, and data-driven advisory solutions to organizations across international markets. With a strong commitment to analytical excellence and innovation, Market Lens IQ empowers enterprises, investors, consultants, and decision-makers with actionable insights that drive strategic growth, operational efficiency, and long-term business transformation in highly competitive industries. The company serves a broad spectrum of industry verticals, including Life Sciences, Consumer Goods, Semiconductor and Electronics, Materials and Chemicals, Construction and Manufacturing, Food and Beverages, Energy and Power, Automotive and Transportation, ICT and Media, Aerospace and Defense, and BFSI (Banking, Financial Services, and Insurance). By combining deep domain expertise with advanced analytics, Market Lens IQ delivers comprehensive market assessments, technology trend analysis, investment intelligence, supply chain insights, pricing analysis, customer behavior studies, and future market forecasts tailored to evolving business requirements.

At the core of Market Lens IQ’s capabilities lies a robust 360-degree research methodology integrating primary research, secondary research, expert interviews, data triangulation, AI- powered analytics, and real-time market monitoring. Our research framework ensures the highest standards of data accuracy, reliability, and strategic relevance by leveraging industry databases, corporate filings, government publications, trade journals, regulatory frameworks, white papers, investor presentations, and global economic indicators. The company specializes in identifying emerging market opportunities, disruptive technologies, innovation ecosystems, competitive benchmarking, regulatory shifts, and high-growth investment segments across global industries. Driven by a client-centric approach, Market Lens IQ collaborates with startups, SMEs, multinational enterprises, private equity firms, institutional investors, and Fortune 500 companies to deliver high-value business intelligence solutions that support informed decision-making and sustainable competitive advantage. Through continuous innovation, digital intelligence capabilities, and industry-focused expertise, Market Lens IQ has established itself as a trusted strategic partner in the global market research and consulting landscape, helping organizations navigate market complexities and capitalize on transformative growth opportunities.

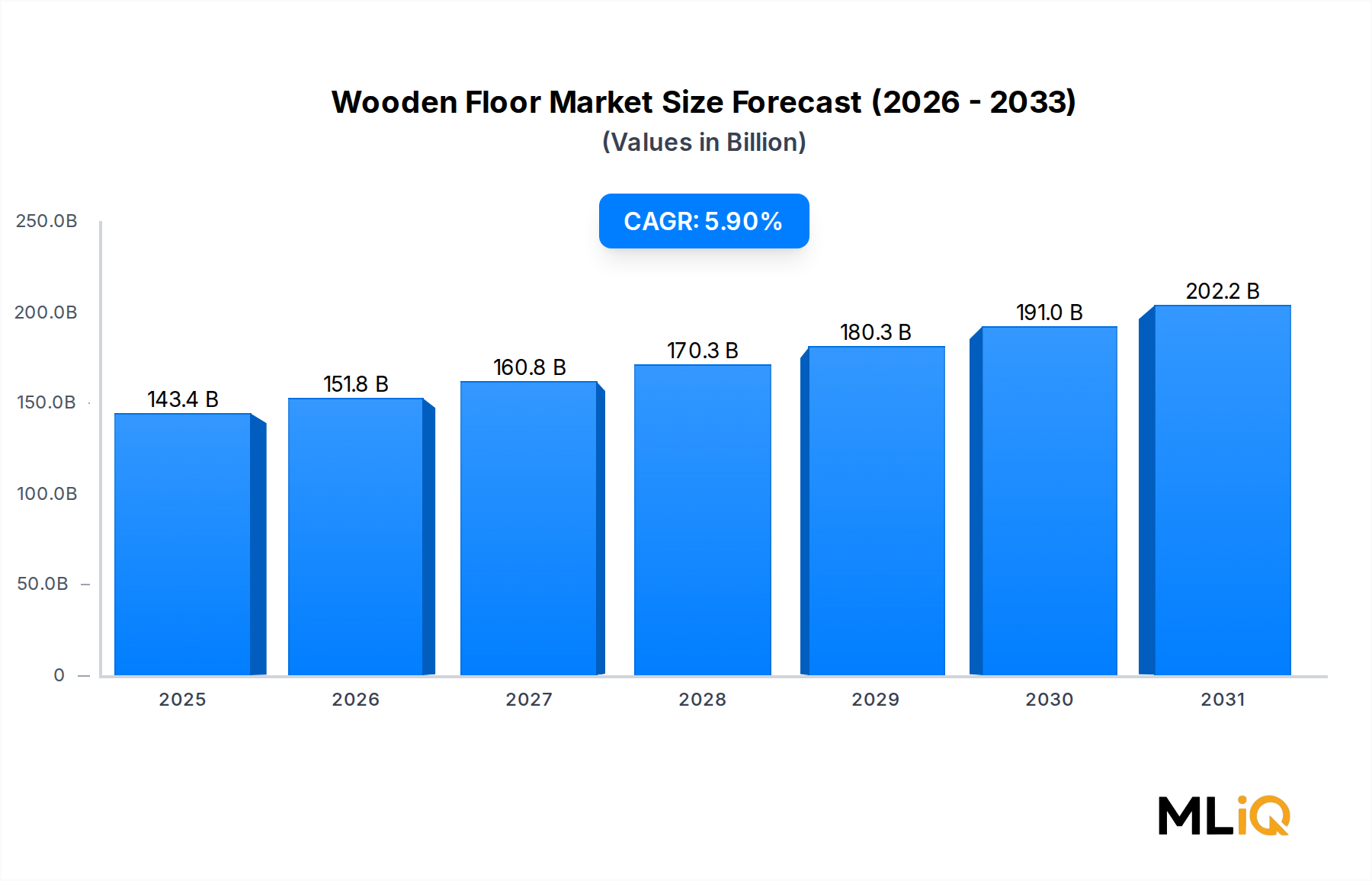

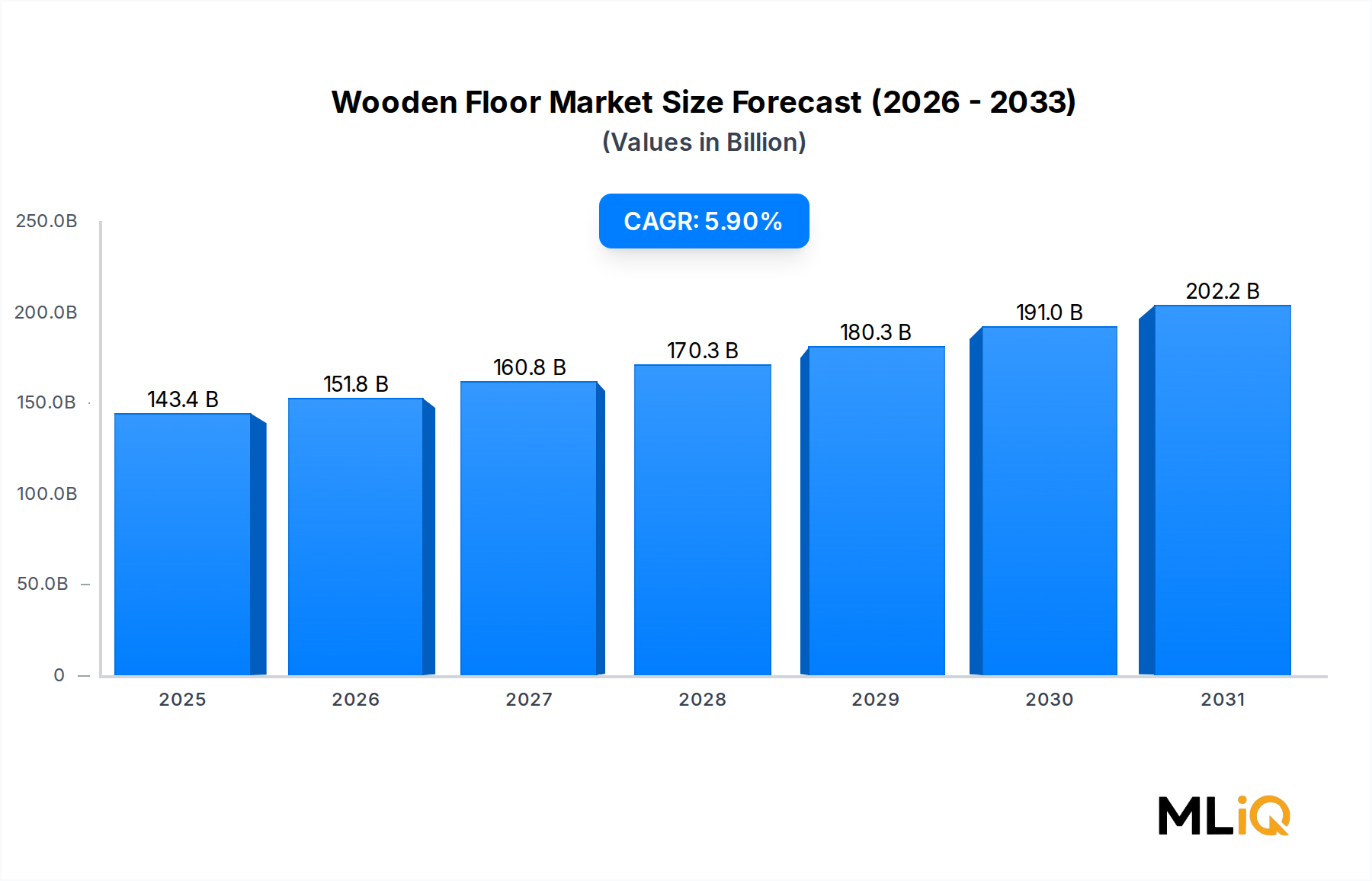

The global Wooden Floor Market is positioned for robust and sustained expansion over the forecast horizon, underpinned by accelerating urbanization, rising disposable incomes, and a global pivot toward premium interior aesthetics. As of the base year, the market is valued at approximately $143,376.66 million, with projections indicating continued momentum at a compound annual growth rate (CAGR) of 5.9% through the forecast period. This trajectory reflects deepening demand across both residential and non-residential construction segments worldwide.

Several macro-level forces are converging to propel the Wooden Floor Market forward. First, global housing starts have rebounded significantly in developed markets following post-pandemic supply chain normalization, while emerging economies across Asia Pacific and the Middle East are experiencing first-time homeownership booms that directly stimulate flooring demand. Second, the commercial real estate sector — particularly office renovation, hospitality refurbishment, and retail fit-out — is driving high-volume procurement of engineered and solid wood flooring solutions.

A pronounced preference for eco-conscious and biophilic design is reshaping product development pipelines across the industry. Consumers and specifiers increasingly demand flooring solutions that carry Forest Stewardship Council (FSC) or Programme for the Endorsement of Forest Certification (PEFC) certifications, compelling manufacturers to align sourcing strategies with sustainable forestry standards. This shift intersects favorably with the Timber and Lumber Market, where responsibly harvested timber commands growing price premiums and supports brand differentiation.

Technological innovation in surface finishing, dimensional stability engineering, and click-lock installation systems has materially reduced installation costs and expanded the accessible customer base. Engineered wood, in particular, has democratized wooden flooring by offering a cost-effective alternative to solid hardwood without compromising on visual appeal or durability, positioning this sub-segment as the fastest-growing product category within the broader market.

Geographically, the market exhibits a healthy diversification of demand. While Europe and North America represent mature, renovation-led markets with strong replacement cycles, Asia Pacific is emerging as the primary engine of new-build demand, accounting for an increasingly significant share of global revenue. The Middle East and Africa, though smaller in absolute terms, are experiencing above-average growth rates fueled by infrastructure development and rising affluence.

Looking ahead, the Wooden Floor Market is expected to benefit from converging trends in green construction standards, smart home integration, and the premiumization of living spaces globally. Market participants that invest in digitally enabled customer experiences, sustainable supply chains, and product innovation — including moisture-resistant and underfloor heating-compatible formats — will be best positioned to capture disproportionate share in this expanding landscape.

Within the Wooden Floor Market, the product segmentation is anchored by two primary categories: engineered wood and solid wood flooring. Of these, engineered wood flooring has emerged as the dominant sub-segment by revenue share, accounting for the majority of global sales volume and value. This dominance is neither coincidental nor temporary — it reflects a structural alignment between product characteristics, consumer expectations, and broader construction trends.

Engineered wood flooring is constructed from a thin veneer of real hardwood bonded over multiple layers of high-density fiberboard (HDF), plywood, or softwood core material. This multi-layer construction endows the product with significantly superior dimensional stability compared to solid wood, enabling it to perform in environments with fluctuating humidity and temperature — conditions that would cause solid wood to warp, cup, or gap. As a result, engineered wood flooring is suitable for installation over radiant heating systems, in basements, and in tropical or humid climates where solid wood traditionally underperforms.

The Engineered Wood Flooring Market has benefited substantially from the premiumization trend in home renovation and commercial interior design. Specifiers and end-users increasingly perceive engineered wood as a technically superior, value-engineered alternative that delivers the warmth and authenticity of natural timber at a more accessible price point. This perception is reinforced by continuous innovation in veneer thickness — premium products now offer veneer layers of 4mm to 6mm, allowing for one or more resanding cycles and extending product lifespan considerably.

Key manufacturers competing in this dominant segment include TARKETT S.A., which has invested heavily in multi-layer engineered plank formats targeting the European renovation market; KÄHRS HOLDING AB (PUBL), recognized globally for its three-layer engineered boards and commitment to sustainable forestry sourcing; and MOHAWK INDUSTRIES, INC., which leverages its vertically integrated manufacturing platform to deliver cost-competitive engineered wood products across North American retail and professional channels.

Solid wood flooring, while holding a smaller market share compared to engineered variants, retains strong demand in luxury residential and heritage restoration segments. Products in the Hardwood Flooring Market — encompassing species such as white oak, maple, walnut, and hickory — command premium price points and are favored in high-end new construction projects where long-term floor refinishing value is a design consideration. Solid wood's inability to be installed in moisture-prone environments or over radiant heating systems has structurally capped its addressable market relative to engineered wood.

The competitive dynamics within the dominant engineered wood segment are intensifying. Chinese manufacturers have scaled production of entry-level engineered planks significantly, exerting downward pricing pressure on European and North American incumbents. In response, established players are differentiating through product innovation — including wider plank formats (up to 300mm), hand-scraped and wire-brushed surface textures, UV-cured oil finishes, and acoustic underlayment integration — features that are difficult to replicate at low cost and that resonate with premium segment buyers.

The share of engineered wood within the overall Wooden Floor Market is expected to continue growing as awareness of its technical advantages spreads in emerging markets, where solid wood has historically dominated due to cultural preference and raw material availability. Education-driven sales strategies by major distributors, combined with increasing architect specification of engineered products in commercial projects, are accelerating this structural share shift across all major geographies.

The Wooden Floor Market is propelled by a set of quantifiable, intersecting drivers while simultaneously navigating identifiable structural constraints that modulate growth velocity.

Primary Driver — Residential Construction Rebound: Global residential construction expenditure has rebounded sharply since 2022, with the United Nations estimating that 2.5 billion people will need new housing by 2050, primarily in urban centers across Asia and Africa. This demographic imperative directly translates into sustained flooring demand, with wooden floors specified in a meaningful share of new residential builds due to their aesthetic premium and perceived lifestyle value. The Residential Flooring Market is a critical demand aggregator for wooden floor manufacturers, and its expansion feeds directly into volume uptake.

Secondary Driver — Commercial Renovation Cycles: The post-pandemic reconfiguration of commercial and hospitality real estate has triggered significant renovation activity. Hotels, restaurants, and corporate offices are investing in premium flooring to attract occupants and guests, with wood and wood-effect surfaces consistently ranked among the top specification choices. The Commercial Flooring Market has reported mid-single-digit growth rates, with wooden and wood-inspired surfaces gaining share versus carpet in office and hospitality applications.

Tertiary Driver — Sustainability and Green Building Certifications: LEED and BREEAM certification programs increasingly incentivize the use of natural, renewable materials including FSC-certified wood flooring. Buildings targeting green ratings are more likely to specify wooden floors, creating a differentiated demand channel that supports premium pricing and margin expansion for compliant manufacturers.

Primary Constraint — Competition from Luxury Vinyl Tile: The Luxury Vinyl Tile Market represents the single most significant competitive threat to wooden flooring. Luxury vinyl tile (LVT) and luxury vinyl plank (LVP) products offer waterproof performance, lower installed cost, and high-fidelity wood visual reproduction. Market data indicates that LVT has captured meaningful share from wooden flooring in the mid-market residential and healthcare segments over the past five years, constraining the addressable market for genuine wood products.

Secondary Constraint — Raw Material Cost Volatility: Timber prices experienced extreme volatility between 2020 and 2023, with North American lumber futures reaching record highs of approximately $1,700 per thousand board feet in May 2021 before normalizing. This price volatility disrupts product pricing strategies and compresses manufacturer margins, particularly for producers that lack backward integration into forestry operations.

The competitive landscape of the Wooden Floor Market is characterized by a mix of global flooring conglomerates, specialized wood floor manufacturers, and vertically integrated timber producers. Key participants include:

TARKETT S.A.: A Paris-based global flooring leader with a diversified portfolio spanning hardwood, engineered wood, and sports flooring. The company has committed to a circular economy roadmap, targeting 100% recyclable product lines by 2030, which strengthens its positioning in sustainability-focused specification channels.

KÄHRS HOLDING AB (PUBL): A Swedish manufacturer widely regarded as a pioneer of engineered wood flooring technology, holding significant intellectual property in multi-layer construction methods. Kährs distributes across more than 70 countries and maintains a strong premium brand identity anchored in Scandinavian design heritage and FSC-certified sourcing.

NATURE HOME HOLDING COMPANY LIMITED: A China-based flooring company with a vertically integrated business model spanning timber sourcing, manufacturing, and retail distribution. The company has aggressively expanded its engineered wood product range to capture both domestic and export market opportunities.

BRUMARK: Specializes in custom flooring solutions for the entertainment, events, and commercial sectors, offering engineered wood and specialty floor systems. The company's project-specific capabilities position it as a preferred partner for high-profile commercial fit-outs.

MANNINGTON MILLS, INC.: A family-owned U.S. flooring manufacturer with a strong presence in both residential and commercial channels, offering solid hardwood and engineered wood alongside resilient flooring categories. Innovation in surface technology and in-house design capabilities differentiate its product offering.

MOHAWK INDUSTRIES, INC.: The world's largest flooring company by revenue, with a global manufacturing footprint and distribution network. Mohawk's scale provides significant competitive advantages in cost efficiency, product breadth, and retailer shelf space allocation.

BORAL LIMITED: An Australian building materials company with timber flooring operations, serving the Asia Pacific region. Boral leverages its construction materials distribution channels to cross-sell flooring products to homebuilders and contractors.

BERKSHIRE HATHAWAY INC. (SHAW INDUSTRIES GROUP, INC.): Shaw Industries is one of the largest floor covering manufacturers in the world, with engineered hardwood and solid wood product lines distributed through retail and builder channels across North America.

BEAULIEU INTERNATIONAL GROUP N.V.: A Belgian flooring and textiles conglomerate with a growing hard surface flooring portfolio, including engineered wood and laminate products distributed across European and export markets.

ARMSTRONG FLOORING, INC.: A specialist in hardwood and resilient flooring with deep roots in the North American market, known for its wide-plank engineered hardwood collections and professional installation support programs.

January 2023: TARKETT S.A. announced the expansion of its ReStart take-back program to additional European markets, enabling consumers to return end-of-life wooden flooring for recycling, advancing circular economy commitments within the sector.

March 2023: KÄHRS HOLDING AB (PUBL) launched a new collection of wide-plank engineered oak floors incorporating thermally modified surface treatments, targeting premium residential and boutique hospitality segments with enhanced durability and a weathered aesthetic.

June 2023: MOHAWK INDUSTRIES, INC. disclosed capital investment of approximately $50 million in its U.S. engineered hardwood manufacturing facilities to increase production capacity and support domestic supply chain resilience amid ongoing import tariff pressures.

September 2023: The European Commission finalized updated formaldehyde emission limits under the Construction Products Regulation, setting stricter thresholds for wood-based flooring products sold in EU member states, with compliance required by mid-2025.

November 2023: NATURE HOME HOLDING COMPANY LIMITED announced a strategic distribution partnership with a pan-Asian retail chain to expand its branded wooden floor products into Southeast Asian growth markets, targeting first-time homeowners in Vietnam, Thailand, and Indonesia.

February 2024: ARMSTRONG FLOORING, INC. completed a portfolio restructuring following its 2022 bankruptcy filing, re-emerging with a focused hardwood flooring product line and a revised go-to-market strategy emphasizing direct-to-builder channel sales.

April 2024: Global FSC-certified forest area surpassed 230 million hectares, providing expanded certified timber supply for wooden floor manufacturers seeking to meet growing consumer and regulatory demand for responsibly sourced materials.

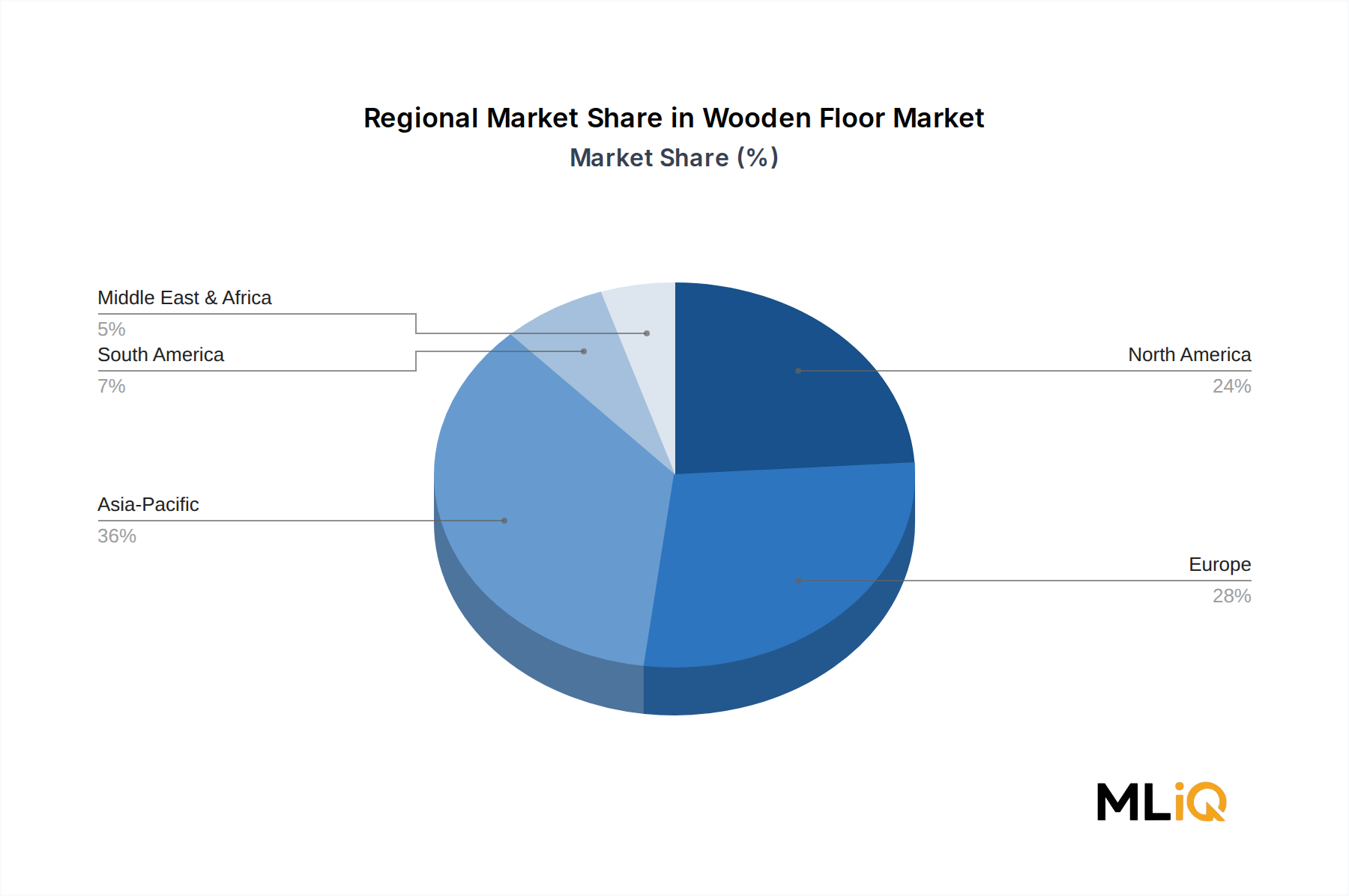

The Wooden Floor Market exhibits meaningful regional variation in growth rates, demand drivers, and competitive dynamics, reflecting differences in construction activity levels, consumer preferences, and economic development trajectories.

Europe represents the most mature regional market, accounting for a substantial share of global revenue — estimated at approximately 30–35% of the total market value. European demand is predominantly renovation-driven, with replacement cycles for aging flooring stock in Germany, France, the United Kingdom, and the Nordic countries generating consistent annual volume. Stringent building regulations, high environmental standards, and a deep cultural affinity for natural wood materials sustain premium pricing. The regional CAGR is estimated at approximately 4.2%, reflecting steady but moderated growth consistent with a mature market. Germany is the largest single-country market within Europe, driven by high homeownership rates and strong renovation spending.

North America is the second-largest regional market, with the United States accounting for the dominant share of regional revenue. The North American market benefits from a large installed base of existing homes undergoing renovation, robust new residential construction in the Sun Belt states, and growing builder adoption of engineered hardwood as a standard specification. The regional CAGR is estimated at 4.8%. Canada and Mexico contribute incremental volume, with Mexico emerging as a faster-growing market on the back of nearshoring-driven construction activity.

Asia Pacific is the fastest-growing regional market, with a projected CAGR of approximately 7.5%, driven primarily by China, India, South Korea, and ASEAN nations. China remains the single largest country-level market globally by volume, with both domestic consumption and export manufacturing playing critical roles. India is the most rapidly expanding sub-market within the region, fueled by urbanization, a growing middle class, and government-backed affordable housing schemes. The building Materials Market dynamics in Asia Pacific directly influence wooden floor demand, as residential construction output in the region continues to outpace the global average.

The Middle East and Africa region is smaller in absolute terms but demonstrates above-average growth momentum, with a regional CAGR estimated at 6.3%. GCC countries — particularly Saudi Arabia and the UAE — are significant demand centers due to large-scale hospitality and luxury residential projects. South Africa leads the African sub-region in terms of market development.

South America, led by Brazil and Argentina, contributes a moderate share of global revenue. Brazil's domestic timber resources provide natural advantages for local wooden floor manufacturers, though economic volatility and currency risk temper investment and consumer spending cycles.

The Wooden Floor Market operates within an increasingly complex and stringent regulatory environment that spans environmental standards, chemical emission limits, and trade policy frameworks across key geographies.

In the European Union, the Construction Products Regulation (CPR) sets foundational performance requirements for flooring products, including reaction to fire, slip resistance, and formaldehyde emission classifications. As noted above, updated emission thresholds finalized in late 2023 will require all wood-based flooring products to comply with Class E1 or better formaldehyde emission standards by mid-2025, pushing manufacturers to reformulate adhesives and finishes across their product lines. The EU Timber Regulation (EUTR), and its successor the EU Deforestation Regulation (EUDR) effective December 2024, require companies to conduct due diligence to ensure that wood products placed on the EU market have not contributed to deforestation. Compliance with the EUDR imposes significant documentation and traceability

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Comprehensive validation mechanisms ensuring market intelligence accuracy, reliability, and adherence to international standards.

500+ data sources cross-validated

200+ industry specialists validation

NAICS, SIC, ISIC, TRBC standards

Continuous market tracking updates

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.9% from 2020-2034 |

| Segmentation |

|

Factors such as are projected to boost the Wooden Floor Market market expansion.

Key companies in the market include TARKETT S.A., KÄHRS HOLDING AB (PUBL), NATURE HOME HOLDING COMPANY LIMITED, BRUMARK, MANNINGTON MILLS, INC., MOHAWK INDUSTRIES, INC., BORAL LIMITED, BERKSHIRE HATHAWAY INC. (SHAW INDUSTRIES GROUP, INC.), BEAULIEU INTERNATIONAL GROUP N.V., ARMSTRONG FLOORING, INC..

The market segments include Product, Application.

The market size is estimated to be USD 143376.66 million as of 2022.

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3456, USD 5769, and USD 10995 respectively.

The market size is provided in terms of value, measured in million and volume, measured in .

Yes, the market keyword associated with the report is "Wooden Floor Market," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Wooden Floor Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.