1. What are the major growth drivers for the Axial Piston Hydraulic Motors and Pumps Market market?

Factors such as are projected to boost the Axial Piston Hydraulic Motors and Pumps Market market expansion.

+1 2315155523

Axial Piston Hydraulic Motors and Pumps Market

Axial Piston Hydraulic Motors and Pumps Market

Market Lens IQ is a global market intelligence and strategic consulting firm delivering advanced syndicated research reports, customized industry analysis, competitive intelligence, and data-driven advisory solutions to organizations across international markets. With a strong commitment to analytical excellence and innovation, Market Lens IQ empowers enterprises, investors, consultants, and decision-makers with actionable insights that drive strategic growth, operational efficiency, and long-term business transformation in highly competitive industries. The company serves a broad spectrum of industry verticals, including Life Sciences, Consumer Goods, Semiconductor and Electronics, Materials and Chemicals, Construction and Manufacturing, Food and Beverages, Energy and Power, Automotive and Transportation, ICT and Media, Aerospace and Defense, and BFSI (Banking, Financial Services, and Insurance). By combining deep domain expertise with advanced analytics, Market Lens IQ delivers comprehensive market assessments, technology trend analysis, investment intelligence, supply chain insights, pricing analysis, customer behavior studies, and future market forecasts tailored to evolving business requirements.

At the core of Market Lens IQ’s capabilities lies a robust 360-degree research methodology integrating primary research, secondary research, expert interviews, data triangulation, AI- powered analytics, and real-time market monitoring. Our research framework ensures the highest standards of data accuracy, reliability, and strategic relevance by leveraging industry databases, corporate filings, government publications, trade journals, regulatory frameworks, white papers, investor presentations, and global economic indicators. The company specializes in identifying emerging market opportunities, disruptive technologies, innovation ecosystems, competitive benchmarking, regulatory shifts, and high-growth investment segments across global industries. Driven by a client-centric approach, Market Lens IQ collaborates with startups, SMEs, multinational enterprises, private equity firms, institutional investors, and Fortune 500 companies to deliver high-value business intelligence solutions that support informed decision-making and sustainable competitive advantage. Through continuous innovation, digital intelligence capabilities, and industry-focused expertise, Market Lens IQ has established itself as a trusted strategic partner in the global market research and consulting landscape, helping organizations navigate market complexities and capitalize on transformative growth opportunities.

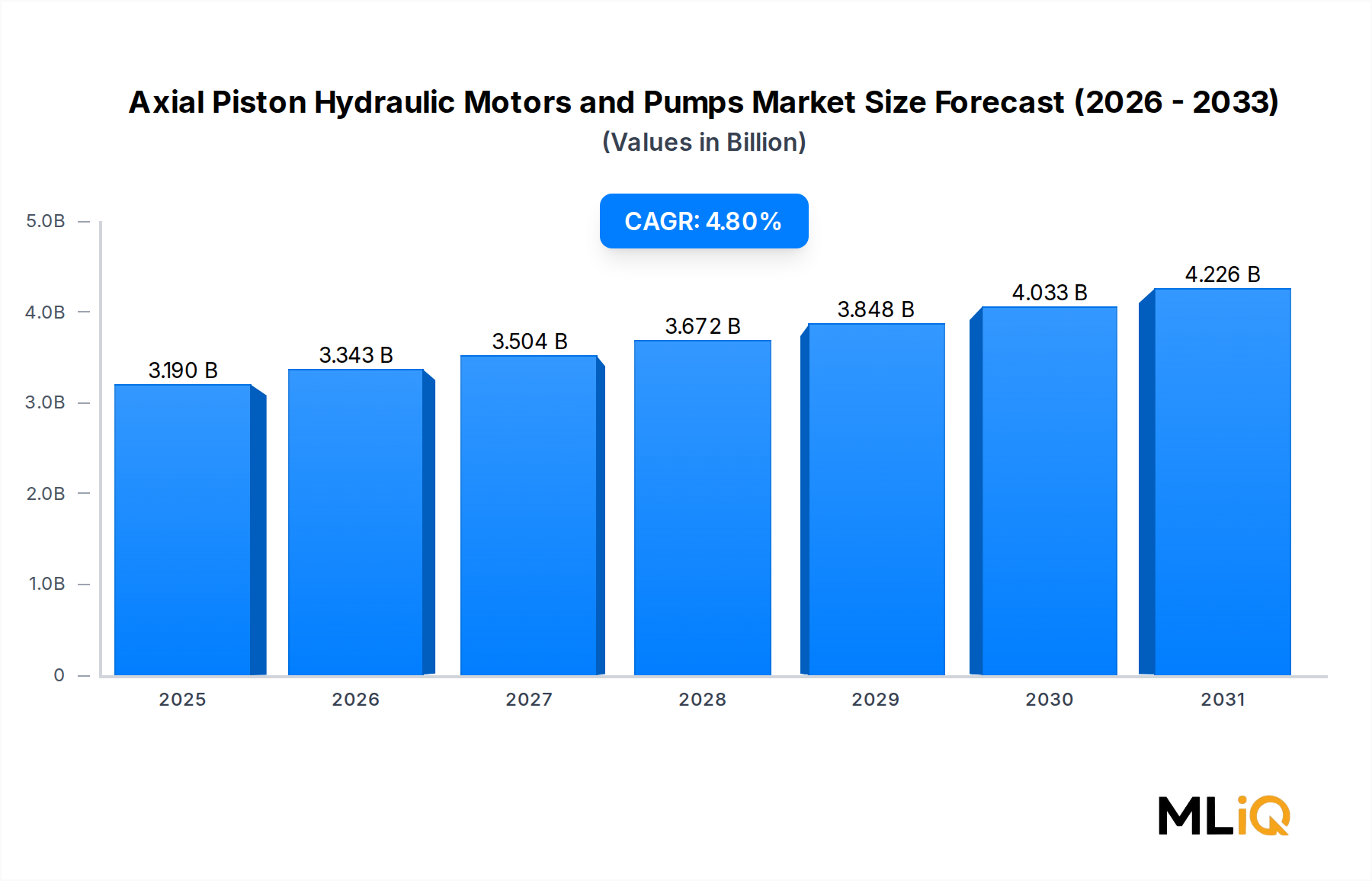

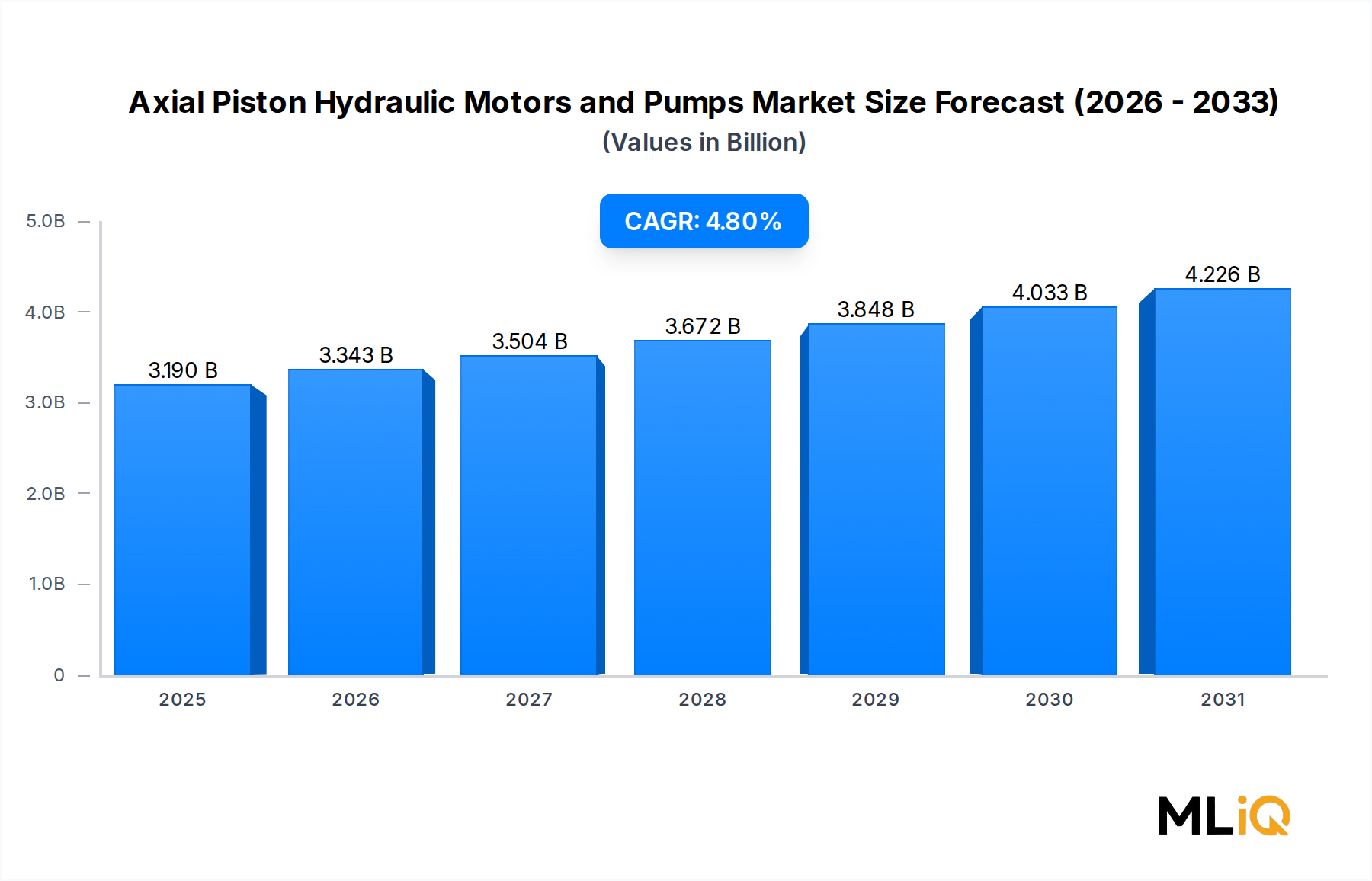

The global Axial Piston Hydraulic Motors and Pumps Market is valued at $3.19 billion as of the base assessment period and is projected to expand at a compound annual growth rate (CAGR) of 4.8% through the forecast horizon. This steady growth trajectory reflects the critical role axial piston technology plays across high-pressure, variable-displacement applications in industries spanning construction, agriculture, oil and gas, and advanced manufacturing.

Axial piston designs — characterized by pistons arranged in a circular pattern parallel to the drive shaft — deliver superior power density, high operating pressures frequently exceeding 400 bar, and efficiency ratings above 95% at peak conditions. These performance attributes position them as the preferred choice in demanding mobile and stationary hydraulic circuits where gear pumps or vane pumps cannot meet duty requirements.

Several macro tailwinds underpin the market's positive outlook. Global infrastructure investment commitments, including the United States Infrastructure Investment and Jobs Act and the European Union's €1.8 trillion NextGenerationEU recovery fund, are driving procurement of heavy construction machinery that relies heavily on axial piston hydrostatic transmissions. Simultaneously, agriculture mechanization in South and Southeast Asia is accelerating adoption of variable-displacement axial piston pumps in combines, tractors, and self-propelled sprayers.

On the industrial side, the reshoring of semiconductor fabrication, automotive assembly, and aerospace manufacturing in North America and Europe is creating sustained demand for precision hydraulic press systems, injection molding machinery, and CNC machine tool circuits — all of which leverage axial piston technology for closed-loop pressure control.

The energy transition also introduces nuanced demand dynamics. While electrification of light mobile equipment creates modest headwinds for small-displacement hydraulic components, large-scale renewable energy infrastructure — including wind turbine blade manufacturing presses and offshore platform hydraulics — reinforces demand for high-pressure axial piston units in the 250–500 bar range.

From a competitive standpoint, the market remains moderately consolidated at the premium end, with Bosch Rexroth AG, Parker Hannifin Corporation, and Kawasaki Precision Machinery commanding significant revenue share. Mid-tier and regional players are gaining traction in price-sensitive Asia Pacific segments. Digital integration — including embedded pressure sensors, IoT-enabled predictive maintenance modules, and electro-hydraulic control interfaces — is emerging as the primary basis of competition moving into the latter half of the decade.

Forward-looking, the market is expected to reach approximately $4.2 billion by the end of the forecast period, driven by continued infrastructure spending, agricultural modernization, and the integration of smart hydraulics into Industry 4.0 manufacturing environments.

Within the Axial Piston Hydraulic Motors and Pumps Market, axial piston hydraulic pumps represent the dominant product segment by revenue contribution, consistently capturing more than 55% of total market value. This dominance stems from the broader range of applications served by hydraulic pumps versus motors, the higher unit average selling prices associated with variable-displacement pump configurations, and the design architecture of most open-circuit hydraulic systems, which require one pump per circuit but may utilize multiple motors.

Axial piston pumps are differentiated primarily by their displacement control mechanism. Fixed-displacement units provide constant flow at a given shaft speed and are widely employed in simple machine tool circuits and agricultural equipment where variable flow is unnecessary. Variable-displacement units — controlled via swashplate angle adjustment — dominate in mobile construction equipment, industrial presses, and hydrostatic transmissions, where load-sensing and pressure-compensating controls dramatically improve system energy efficiency.

The shift toward load-sensing variable-displacement pumps has been one of the most consequential segment trends of the past decade. Traditional fixed-displacement systems operating in throttle-controlled circuits dissipate substantial energy as heat when system demand falls below maximum flow. Variable-displacement load-sensing architectures reduce hydraulic power losses by 20–40% in typical duty cycles, a compelling value proposition as fuel costs and carbon emission regulations tighten globally.

Excavators represent the highest-volume single application for axial piston pumps. A standard 20-ton crawler excavator typically incorporates a tandem axial piston pump arrangement capable of combined displacements between 2×85 cc/rev and 2×130 cc/rev, operating at pressures up to 350 bar. Global excavator production volumes — estimated at over 500,000 units annually prior to supply chain disruptions — translate directly into a high-baseline demand floor for axial piston pump manufacturers.

Key players dominating this segment include Bosch Rexroth AG, which offers the A10V and A4V series; Parker Hannifin Corporation with its PV and P1 series; Kawasaki Precision Machinery with K3V and K5V families; and Danfoss with its H1 series open-circuit pumps. Linde Hydraulics GmbH And Co. KG and HAWE Hydraulik SE maintain strong positions in high-pressure industrial pump applications in Europe.

Chinese manufacturers including Jiangsu Hengli Hydraulic Co., LTD. and THM Huade have made substantial inroads in the domestic Chinese market and are beginning to export competitively priced variable-displacement pumps to Southeast Asia and the Middle East. Jiangsu Hengli in particular reported hydraulic component revenues exceeding CNY 7 billion in recent fiscal years, underscoring the scale competitive Chinese manufacturers have achieved.

Segment revenue share for axial piston pumps is consolidating rather than expanding, as the motors sub-segment grows at a slightly faster pace driven by hydrostatic final-drive adoption in compact construction equipment and agricultural combine harvesters. Nevertheless, the absolute revenue lead of pumps is expected to persist through the forecast period given pump-to-motor ratios in system design and the higher service and replacement revenue associated with pump maintenance intervals.

The growing integration of digital pump controllers — enabling real-time displacement adjustment via CAN bus, IoT telemetry, and cloud-based fleet management platforms — is elevating average selling prices in the premium segment and sustaining revenue growth for technology-leading OEMs.

The growth of the Axial Piston Hydraulic Motors and Pumps Market is governed by a set of quantifiable structural drivers and identifiable constraints that collectively define the risk-adjusted investment case for participants.

Global construction output growth is the single most impactful demand driver. The Global Construction Perspectives research body projects world construction output to grow by $4.5 trillion to reach $15.2 trillion by 2030, with the strongest acceleration in infrastructure and energy-related construction. Axial piston hydraulics are embedded in excavators, cranes, concrete pumps, and drilling rigs — equipment categories with direct correlation to construction spending cycles.

Agricultural mechanization rates in Asia and Africa provide a secondary demand engine. Tractor density in India currently stands at approximately 20 tractors per 1,000 hectares versus 60–80 in mature European markets, indicating substantial mechanization headroom. As combine harvester and precision agriculture equipment penetration increases, so does the installed base requiring high-pressure variable-displacement axial piston pumps and wheel-motor drives.

Oil and gas capital expenditure recovery post-2020 has restored demand for high-pressure axial piston units used in offshore drilling top drives, subsea BOP actuation, and onshore fracturing equipment. Global upstream capex rebounded to approximately $500 billion in 2022–2023, partially restoring the demand lost during the pandemic-era investment freeze.

On the constraint side, the electrification of compact mobile equipment presents a structural headwind. Battery-electric mini-excavators below 6 tons — products commercialized by Volvo, Bobcat, and Komatsu — incorporate electric actuators or reduced-pressure hydraulic circuits that do not require high-efficiency axial piston designs. If electrification adoption accelerates in the 6–20 ton excavator class, it could dampen demand growth by 0.5–1.0 percentage points of CAGR in the medium term.

Raw material cost volatility — specifically for high-grade steel alloys, bearing steel, and precision-ground components — introduces margin pressure. The Hydraulic Pumps Market and broader fluid power suppliers experienced input cost increases of 15–25% during the 2021–2022 supply chain disruption cycle, compressing OEM margins and delaying some customer procurement decisions.

Skilled manufacturing labor scarcity for precision honing, lapping, and assembly operations in Europe and North America adds a capacity constraint that limits the speed at which domestic producers can scale output to meet demand surges.

The competitive landscape of the Axial Piston Hydraulic Motors and Pumps Market features a blend of global technology leaders, diversified industrial conglomerates, and increasingly capable regional challengers:

Bosch Rexroth AG.(ROBERT BOSCH GmbH): The world's leading hydraulic component manufacturer by revenue, offering a comprehensive axial piston portfolio spanning A4V, A10V, A11V, and A2FM series. The company's deep integration with Bosch's IoT and electrification platforms gives it a decisive advantage in smart hydraulics development.

Kawasaki Precision Machinery (Kawasaki Heavy Industries): A dominant supplier to the excavator OEM market, with K3V and K5V pump families standard-specified by major Asian and global construction equipment manufacturers. The company leverages Kawasaki Heavy Industries' robotics and engineering capabilities in developing hybrid hydrostatic systems.

POCLAIN: A specialized manufacturer with particular strength in hydraulic wheel motors for agricultural and material handling applications. POCLAIN is recognized for its cam lobe motor technology alongside axial piston offerings and maintains a strong European and Latin American distributor network.

Parker Hannifin Corporation: A diversified motion and control technology leader whose Hydraulics Division supplies PV, P2 and open-circuit pump series to industrial and mobile markets globally. Parker's aftermarket services network and digital diagnostic tools are key competitive differentiators.

Bucher Group: A Swiss-headquartered precision engineering group with hydraulic divisions serving mobile and industrial markets. Bucher Hydraulics focuses on compact, high-efficiency axial piston designs for agricultural and municipal vehicles.

HAWE Hydraulik SE.: A German specialist in high-pressure compact hydraulics, serving machine tool, semiconductor equipment, and medical device manufacturing sectors. HAWE is known for operating pressures up to 700 bar in its axial piston pump lines.

THM Huade: A leading Chinese hydraulic component manufacturer serving domestic heavy industry, mining, and construction equipment OEMs. THM Huade is expanding export capabilities in Belt and Road Initiative countries.

Bondioli & Pavesi S.p.A.: An Italian driveline and hydraulics specialist with strong positions in agricultural and compact construction equipment hydraulics across European markets.

Liebherr Group: A vertically integrated manufacturer producing axial piston components for internal use in its own construction equipment and cranes, as well as selling externally into industrial markets.

Jiangsu Hengli Hydraulic Co., LTD.: China's largest domestic hydraulic pump and cylinder manufacturer, rapidly closing the technology gap with Western incumbents through sustained R&D investment exceeding 5% of revenue.

HYDAC International GmbH: A German fluid technology specialist with complementary hydraulic filtration, cooling, and accumulator product lines that reinforce its axial piston component sales through system-level value propositions.

Danfoss: Offers the H1 and APP series axial piston pumps and motors, with particular strength in mobile machinery closed-circuit hydrostatic transmissions and marine applications.

Linde Hydraulics GmbH And Co. KG: A subsidiary of Weichai Power, offering premium closed-circuit HPV/HMV axial piston pump and motor systems with strong adoption in heavy mobile equipment and industrial drives.

January 2023: Bosch Rexroth AG unveiled its A1VO series axial piston pump featuring an integrated electronic pressure and flow controller with CAN bus interface, targeting mobile crane and aerial work platform OEMs seeking reduced valve complexity.

March 2023: Danfoss announced a strategic partnership with an undisclosed Tier-1 agricultural equipment OEM to co-develop a next-generation closed-circuit hydrostatic transmission for large-format combine harvesters, incorporating H1 series axial piston units with predictive load-sensing algorithms.

June 2023: Jiangsu Hengli Hydraulic Co., LTD. inaugurated a second precision manufacturing campus in Zhenjiang, China, adding 300,000 square meters of production capacity and targeting annual output of 1 million hydraulic pump units by 2025.

September 2023: Parker Hannifin Corporation completed integration of its Hydraulics Division's digital service platform, enabling real-time pump efficiency monitoring and predictive maintenance scheduling for fleet operators across 45 countries.

November 2023: HAWE Hydraulik SE introduced the V60M series axial piston pump rated to 450 bar continuous operating pressure, addressing demand from precision metal forming press manufacturers replacing aging high-pressure circuits.

February 2024: The European Commission published updated Ecodesign Regulation provisions proposing minimum hydraulic pump efficiency standards, expected to take effect by 2027 and likely to accelerate displacement of fixed-displacement gear pumps by axial piston variable-displacement alternatives in industrial machinery.

April 2024: Kawasaki Precision Machinery announced qualification of its K3VL series for hydrogen fuel cell construction equipment platforms, positioning axial piston hydraulics within next-generation zero-emission heavy machinery architectures.

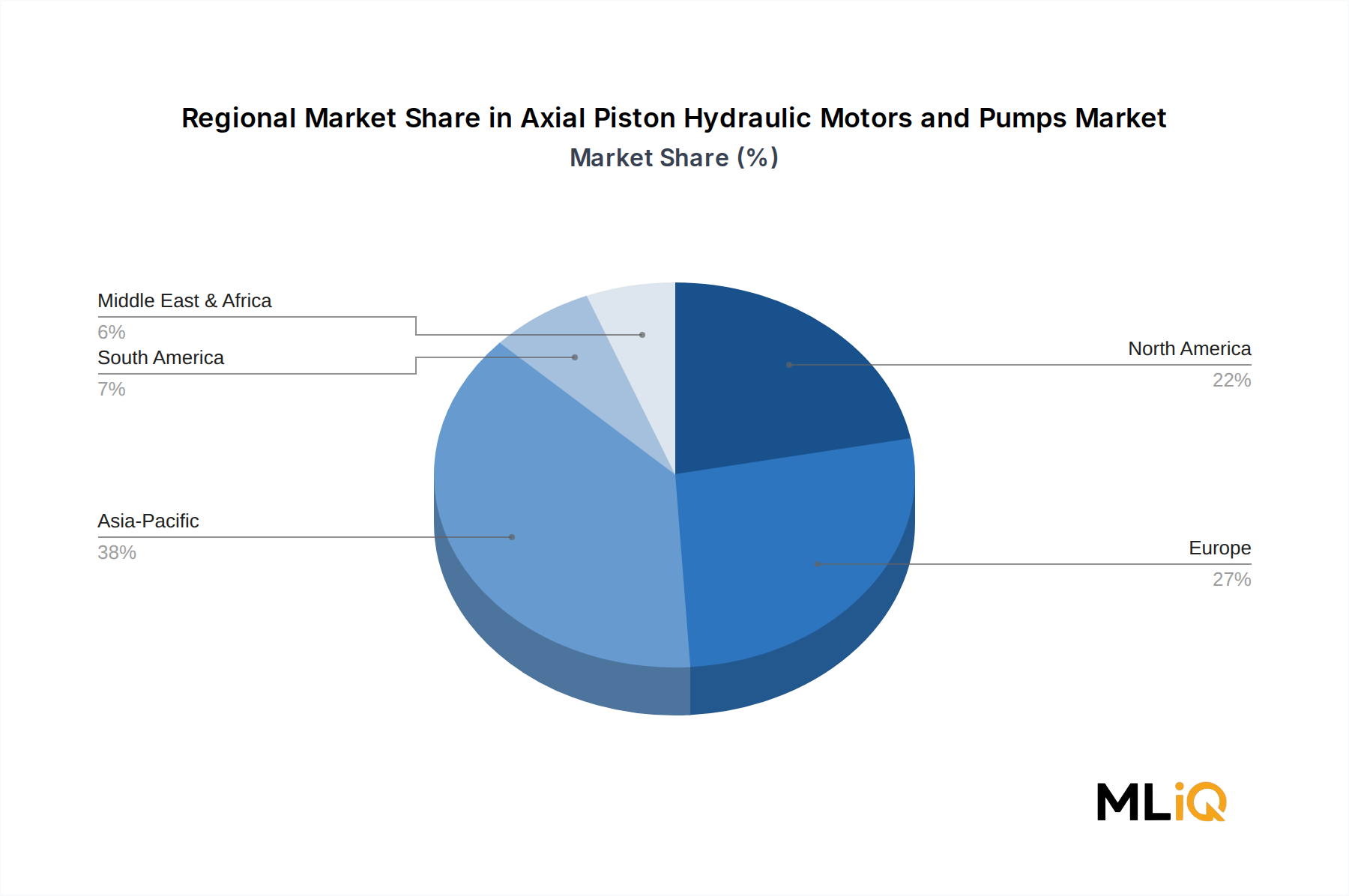

The Axial Piston Hydraulic Motors and Pumps Market displays significant regional variation in growth rates, demand drivers, and competitive dynamics across its five primary geographic segments.

Asia Pacific is the largest and fastest-growing region, accounting for an estimated 42–45% of global market revenue. China alone represents the dominant national market within the region, driven by the world's largest construction equipment fleet, ongoing infrastructure investment under national Five-Year Plans, and the rapid domestic hydraulics industry development. India's market is expanding at a regional CAGR exceeding 6.5%, propelled by the National Infrastructure Pipeline targeting $1.4 trillion in project investment. Japan and South Korea contribute premium demand for high-precision axial piston units in machine tools and robotics. The ASEAN bloc is emerging as a significant secondary growth center as manufacturing investment diversifies away from China.

North America represents the second-largest regional market, with the United States accounting for approximately 20% of global demand. The Infrastructure Investment and Jobs Act, reshoring of industrial manufacturing, and the oil and gas capex recovery in the Permian Basin and offshore Gulf of Mexico are the three primary demand pillars. The North American market is growing at a CAGR of approximately 4.2–4.5%, consistent with overall market average. Canada's mining and oil sands sectors sustain demand for large-format axial piston units in draglines and haul trucks.

Europe is the most mature regional market and home to the highest concentration of premium hydraulics manufacturers. Germany, Italy, France, and the Benelux region together account for the bulk of European demand, driven by precision machine tool manufacturing, agricultural equipment OEM clusters, and industrial automation investment. European regulatory pressure through Ecodesign standards is actively driving substitution toward high-efficiency axial piston designs. The region grows at approximately 3.5–4.0% CAGR.

Middle East and Africa is experiencing accelerated growth at an estimated 5.5–6.0% CAGR, primarily driven by GCC infrastructure megaprojects — including NEOM in Saudi Arabia and UAE urban development programs — as

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.8% from 2020-2034 |

| Segmentation |

|

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Comprehensive validation mechanisms ensuring market intelligence accuracy, reliability, and adherence to international standards.

500+ data sources cross-validated

200+ industry specialists validation

NAICS, SIC, ISIC, TRBC standards

Continuous market tracking updates

Factors such as are projected to boost the Axial Piston Hydraulic Motors and Pumps Market market expansion.

Key companies in the market include Bosch Rexroth AG.(ROBERT BOSCH GmbH), Kawasaki Precision Machinery (Kawasaki Heavy Industries), POCLAIN, Parker Hannifin Corporation, Bucher Group, HAWE Hydraulik SE., THM Huade, Bondioli & Pavesi S.p.A., Liebherr Group, Jiangsu Hengli Hydraulic Co., LTD., HYDAC International GmbH, Danfoss, Linde Hydraulics GmbH And Co. KG.

The market segments include Product Type, Application.

The market size is estimated to be USD 3.19 billion as of 2022.

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3200, USD 4560, and USD 7638 respectively.

The market size is provided in terms of value, measured in billion and volume, measured in .

Yes, the market keyword associated with the report is "Axial Piston Hydraulic Motors and Pumps Market," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Axial Piston Hydraulic Motors and Pumps Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.