1. What are the major growth drivers for the Pipe and Tube Cutters Market market?

Factors such as are projected to boost the Pipe and Tube Cutters Market market expansion.

+1 2315155523

Pipe and Tube Cutters Market

Pipe and Tube Cutters Market

Market Lens IQ is a global market intelligence and strategic consulting firm delivering advanced syndicated research reports, customized industry analysis, competitive intelligence, and data-driven advisory solutions to organizations across international markets. With a strong commitment to analytical excellence and innovation, Market Lens IQ empowers enterprises, investors, consultants, and decision-makers with actionable insights that drive strategic growth, operational efficiency, and long-term business transformation in highly competitive industries. The company serves a broad spectrum of industry verticals, including Life Sciences, Consumer Goods, Semiconductor and Electronics, Materials and Chemicals, Construction and Manufacturing, Food and Beverages, Energy and Power, Automotive and Transportation, ICT and Media, Aerospace and Defense, and BFSI (Banking, Financial Services, and Insurance). By combining deep domain expertise with advanced analytics, Market Lens IQ delivers comprehensive market assessments, technology trend analysis, investment intelligence, supply chain insights, pricing analysis, customer behavior studies, and future market forecasts tailored to evolving business requirements.

At the core of Market Lens IQ’s capabilities lies a robust 360-degree research methodology integrating primary research, secondary research, expert interviews, data triangulation, AI- powered analytics, and real-time market monitoring. Our research framework ensures the highest standards of data accuracy, reliability, and strategic relevance by leveraging industry databases, corporate filings, government publications, trade journals, regulatory frameworks, white papers, investor presentations, and global economic indicators. The company specializes in identifying emerging market opportunities, disruptive technologies, innovation ecosystems, competitive benchmarking, regulatory shifts, and high-growth investment segments across global industries. Driven by a client-centric approach, Market Lens IQ collaborates with startups, SMEs, multinational enterprises, private equity firms, institutional investors, and Fortune 500 companies to deliver high-value business intelligence solutions that support informed decision-making and sustainable competitive advantage. Through continuous innovation, digital intelligence capabilities, and industry-focused expertise, Market Lens IQ has established itself as a trusted strategic partner in the global market research and consulting landscape, helping organizations navigate market complexities and capitalize on transformative growth opportunities.

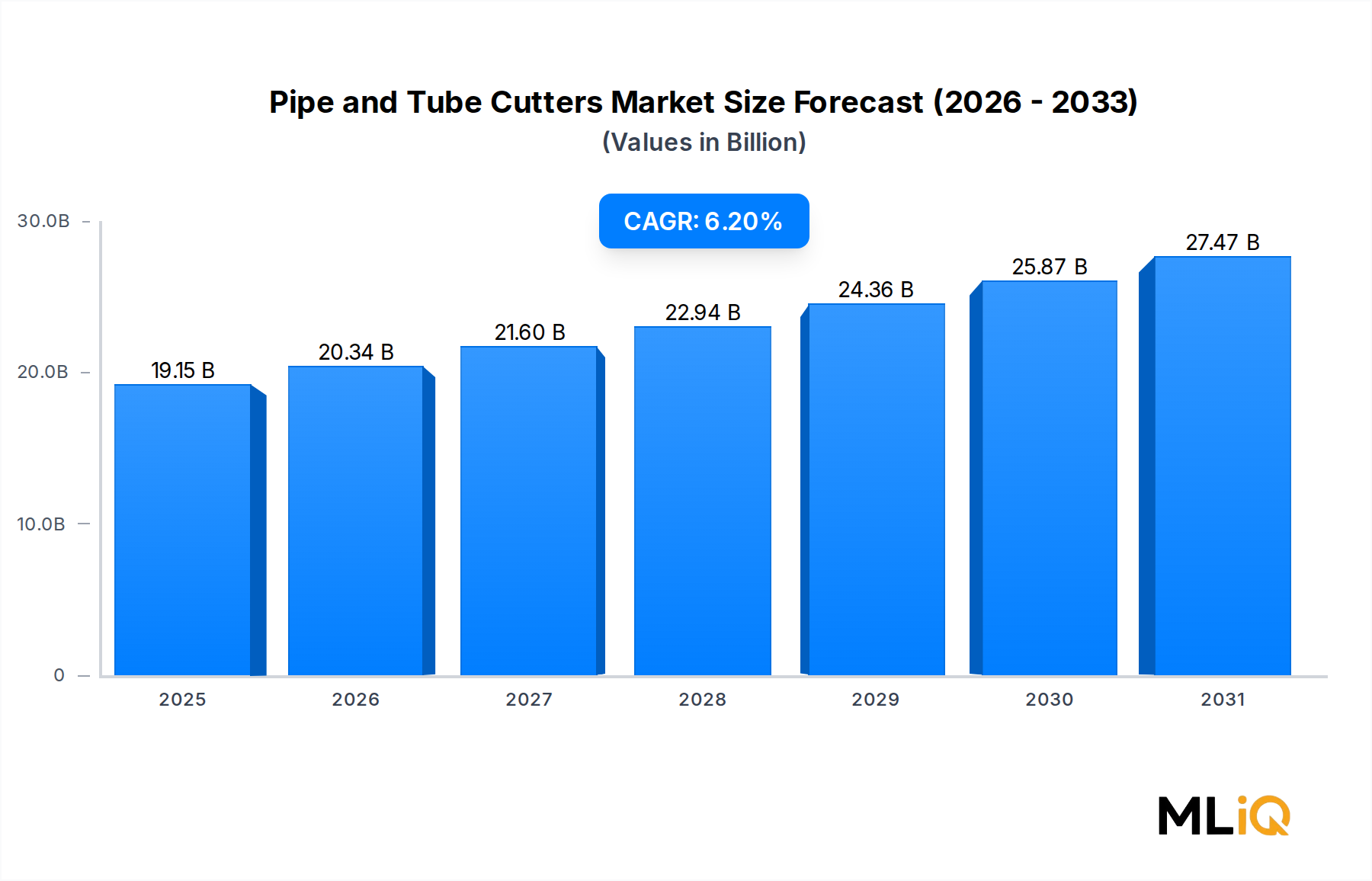

The global Pipe and Tube Cutters Market was valued at $19.15 billion in 2023 and is projected to expand at a compound annual growth rate (CAGR) of 6.2% through the forecast period, driven by accelerating infrastructure investment, rapid urbanization across emerging economies, and a broad shift toward precision-engineered plumbing and industrial piping systems. By 2030, the market is expected to surpass $29 billion, reflecting durable demand across residential construction, commercial infrastructure, and heavy manufacturing verticals.

Key demand drivers include a global surge in water and wastewater infrastructure upgrades, expansion of the oil and gas pipeline network, and rising adoption of automated cutting solutions in high-throughput manufacturing environments. Regulatory mandates around construction safety standards and stricter building codes in North America and Europe are compelling contractors and industrial operators to upgrade legacy manual cutting tools with precision-grade automatic cutters capable of delivering clean, burr-free cuts on tight-tolerance tubing.

Macroeconomic tailwinds—including government-backed stimulus programs for smart city development across Asia Pacific and the Middle East, as well as reshoring of industrial manufacturing capacity in the United States and Europe post-pandemic—are generating sustained procurement activity for both handheld and bench-mounted pipe and tube cutting equipment. The proliferation of HVAC retrofitting projects, combined with rapid expansion of photovoltaic solar farm construction requiring extensive copper and aluminum tubing runs, further reinforces positive market momentum.

On the material segmentation side, metal pipe cutting tools continue to dominate by revenue share due to the prevalence of steel, copper, and aluminum tubing in industrial and commercial applications. Plastic pipe cutters, however, are registering faster unit growth as PVC, CPVC, and PEX piping systems gain traction in residential plumbing and potable water distribution networks.

From a competitive standpoint, the market remains moderately fragmented, with tier-one players such as RIDGID, Milwaukee, and Klein Tools commanding premium positioning through brand equity and distribution scale, while regional manufacturers in China, India, and Eastern Europe compete aggressively on cost. Innovation cycles are shortening, with product launches increasingly centered on ergonomic design improvements, one-handed operation, and compatibility with smart diagnostic systems.

Overall, the Pipe and Tube Cutters Market presents a compelling investment thesis underpinned by durable construction megatrends, technological differentiation, and expanding end-use applications across both mature and high-growth geographies.

The manual segment remains the single largest revenue-generating category within the Pipe and Tube Cutters Market, accounting for an estimated 58–62% of total market revenue in 2023. This dominance is rooted in the segment's versatility, affordability, and suitability across a wide spectrum of job-site environments where portability and ease of use take precedence over throughput speed.

Manual pipe and tube cutters encompass a broad product family including ratchet-style cutters, scissor-action cutters, wheel-type cutters, and compact snap-cut models. Their near-universal applicability across plastic and metal pipe materials—from soft copper and PEX to schedule 40 PVC—makes them the default choice for licensed plumbers, HVAC technicians, and general contractors performing field installation work. The low entry price point, typically ranging from $15 to $150 per unit for professional-grade tools, ensures high-volume procurement by both individual tradespeople and institutional buyers such as construction contractors and municipal utilities.

Key players anchoring the manual segment include RIDGID, a brand synonymous with professional-grade plumbing tools and known for its ratchet pipe cutter lines that deliver smooth, consistent cutting action on copper, aluminum, and thin-wall steel; Klein Tools, whose wide blade and compact-body designs address the demands of electricians and HVAC technicians working in confined spaces; and Husky, a value-oriented brand distributed primarily through home improvement retail channels targeting the residential and DIY segment. Milwaukee has also made notable inroads into the manual segment through ergonomically redesigned ratchet cutters with hardened steel blades, positioning the brand at the premium tier of the professional market. The Plumber's Choice and Imperial round out the competitive landscape with specialized products targeting niche plumbing and refrigeration tubing applications.

The manual segment's share, while dominant, faces moderate consolidation pressure from the automatic segment, which is growing at a faster CAGR of approximately 8.1% as manufacturing and industrial customers seek to reduce labor costs and improve cut consistency at scale. Nevertheless, the manual segment is expected to retain majority share through 2030 for several structural reasons: the global installed base of field-service plumbers and HVAC contractors remains vast, especially in developing markets; manual cutters require no external power source, making them indispensable in off-grid or infrastructure-limited environments; and the total cost of ownership is dramatically lower than powered alternatives, a critical consideration for small and medium-sized contracting firms that dominate the addressable customer base in markets such as India, Southeast Asia, Latin America, and Sub-Saharan Africa.

Within the manual segment, ratchet-style cutters are the fastest-growing sub-category, driven by ergonomic advantages that reduce hand fatigue during repetitive cutting tasks. Manufacturers are responding by introducing models with composite-grip handles, self-adjusting ratchet mechanisms, and replaceable blade systems that extend tool longevity and reduce lifecycle cost. The increasing use of PEX tubing in radiant floor heating and residential plumbing—materials that respond particularly well to sharp-blade scissor-action cutting—is also fueling demand for manual cutters specifically optimized for flexible polymer pipe.

Geographically, North America and Europe represent the most lucrative markets for premium manual cutters, where professional certification requirements and union wage structures incentivize investment in high-quality hand tools. Asia Pacific, led by China and India, dominates unit volume, with cost-competitive domestic manufacturers supplying the bulk of demand in lower price tiers.

Several quantifiable forces are shaping the trajectory of the Pipe and Tube Cutters Market, operating simultaneously as growth accelerators and structural headwinds.

Primary Growth Drivers:

Infrastructure Investment Surge: The United States Infrastructure Investment and Jobs Act committed $55 billion specifically to water infrastructure modernization, directly stimulating demand for pipe cutting tools used in the replacement of aging lead and galvanized steel water mains. Similar programs in the European Union, India's AMRUT 2.0 scheme, and China's 14th Five-Year Plan for urban utilities collectively represent trillions in capital deployment that require extensive piping installation and replacement activity.

HVAC Market Expansion: The global HVAC Equipment Market is projected to grow at a CAGR exceeding 6.5% through 2030, generating parallel demand for copper and aluminum tube cutting tools used in refrigerant line fabrication, condenser coil installation, and ductwork integration. Every new commercial HVAC installation requires multiple cuts of copper refrigerant tubing, directly tying HVAC market volume to pipe cutter unit consumption.

Automation Adoption in Manufacturing: Industrial facilities in automotive, aerospace, and semiconductor fabrication are investing in CNC tube cutting systems and automated orbital cutters to achieve micron-level precision, driving the high-value automatic segment of the market at a CAGR of approximately 8.1%.

Key Constraints:

Raw Material Price Volatility: Fluctuations in high-grade tool steel, tungsten carbide, and hardened alloy prices directly compress manufacturer margins. Steel price indices showed 40–60% swings between 2020 and 2023, creating procurement uncertainty across the supply chain.

Market Fragmentation and Price Erosion: The proliferation of low-cost imports, primarily from Chinese manufacturers, has driven average selling prices downward in value segments, limiting revenue growth even as unit volumes rise. This dynamic is particularly acute in the Construction Equipment Market and adjacent hand tool categories where brand differentiation is difficult to sustain at lower price tiers.

Skilled Labor Shortages: Paradoxically, the construction labor shortage in developed markets reduces overall project activity velocity, dampening the rate of tool procurement cycles even as per-project tool usage increases.

The competitive landscape of the Pipe and Tube Cutters Market is characterized by a mix of multinational tool conglomerates, specialized industrial equipment manufacturers, and regional cost-competitive producers. Below is a strategic profile of the key participants:

Klein Tools: A century-old American hand tool manufacturer with deep penetration in the electrical and plumbing contractor segments. Klein Tools leverages an extensive North American distribution network and a reputation for professional-grade durability to maintain premium pricing on its pipe and conduit cutter lines.

BYSTRONIC: A Swiss precision machinery company with expertise in laser and waterjet tube processing systems. BYSTRONIC targets high-end industrial and automotive manufacturing customers requiring automated, high-precision tube cutting solutions, competing at the upper tier of the automatic segment.

Imperial: A specialist in flaring, swaging, and tube cutting tools for HVAC, refrigeration, and plumbing applications. Imperial's product focus on refrigeration tubing tools positions it favorably amid the global HVAC market expansion.

Milwaukee: A subsidiary of Techtronic Industries, Milwaukee has aggressively expanded its pipe and tube cutter portfolio through ergonomic innovation, hardened blade technology, and integration with its broader cordless power tool ecosystem. The brand commands significant loyalty among professional plumbers and pipefitters.

JSC: A regional manufacturer supplying pipe cutting and threading equipment primarily to industrial and oilfield customers in Eastern Europe and Central Asia, competing on technical robustness and after-sales service depth.

Apollo: Known primarily for valve and fitting systems, Apollo has extended its product range to include pipe preparation tools, leveraging its existing relationships with commercial plumbing contractors and wholesale distributors.

The Eraser Company: A niche manufacturer specializing in tube and cable preparation tools for the electronics and telecommunications industries. The Eraser Company addresses precision cutting applications in thin-wall and specialty material tubing not typically served by mainstream plumbing tool brands.

RIDGID: A flagship brand of Emerson Electric, RIDGID is arguably the most recognized name in professional pipe cutting, threading, and joining equipment globally. Its broad product range spanning manual cutters, powered pipe saws, and press-fit tooling systems makes it a one-stop supplier for the plumbing and mechanical contracting trades.

MISUMI India: The Indian subsidiary of the MISUMI Group, offering a broad catalog of configurable cutting and machining components to industrial OEMs and maintenance procurement departments across South and Southeast Asia.

Husky: A retail-focused tool brand distributed exclusively through The Home Depot in North America. Husky captures significant DIY and light-professional demand through value pricing and wide retail availability.

The Plumber's Choice: A wholesale-oriented brand supplying plumbing professionals with cost-competitive pipe cutters, fittings, and installation accessories, with a distribution model centered on plumbing wholesale houses and e-commerce channels.

January 2023: Milwaukee Tool launched an updated ratchet PVC pipe cutter featuring a reinforced fiberglass handle and a hardened steel blade rated for over 2,000 cuts per blade replacement cycle, targeting professional plumbers in high-volume residential construction projects.

March 2023: RIDGID introduced a new line of press-fit-compatible pipe preparation tools integrating tube cutting, deburring, and end-facing functions in a single portable unit, reducing labor steps for commercial mechanical contractors.

June 2023: BYSTRONIC announced a strategic partnership with a leading German automotive tier-1 supplier to co-develop a next-generation laser tube cutting cell optimized for high-tensile aluminum structural components used in electric vehicle (EV) battery enclosure assemblies.

September 2023: Klein Tools expanded its pipe and conduit cutting portfolio with a new series of compact stainless steel tube cutters designed for tight-clearance applications in data center and semiconductor fabrication facility construction.

November 2023: Imperial Eastman completed certification of its premium refrigeration tube cutter series to updated ASHRAE and EN 378 refrigerant handling safety standards, enabling distribution into the European HVAC market.

February 2024: A major infrastructure contractor in India awarded a multi-year supply contract for industrial pipe cutting and beveling equipment to a consortium of Asian manufacturers, reflecting growing domestic procurement under India's smart city expansion initiative.

April 2024: The Eraser Company introduced a new automated tube stripping and cutting system targeting medical device and semiconductor tubing applications, addressing demand from the rapidly growing precision manufacturing sub-segment.

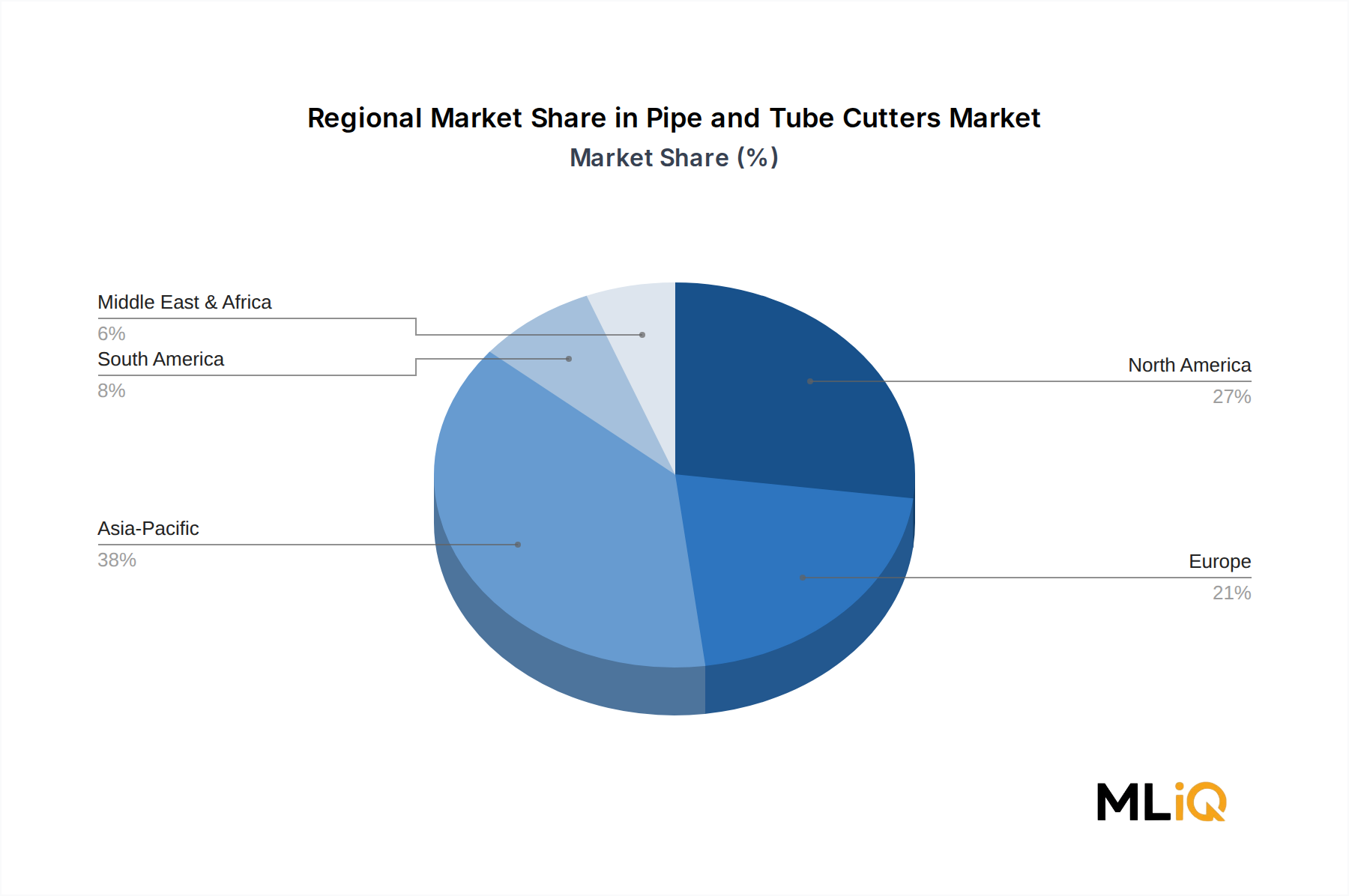

The Pipe and Tube Cutters Market exhibits meaningful regional variation in growth rates, demand composition, and competitive dynamics across its five principal geographies.

North America: North America represented approximately $5.8 billion in market revenue in 2023, anchored by robust commercial construction activity, aging water infrastructure replacement programs, and high penetration of professional-grade tools among licensed plumbing and HVAC contractors. The regional CAGR is estimated at 5.1% through the forecast period. The United States dominates regional demand, with Canada and Mexico contributing meaningfully through oil sands pipeline maintenance and maquiladora manufacturing expansion, respectively. Demand for premium automatic and semi-automatic cutting systems is highest in this region, reflecting elevated labor costs that incentivize productivity-enhancing tool investment.

Europe: Europe accounts for approximately $4.2 billion in market revenue, growing at an estimated CAGR of 4.8%. Germany, the United Kingdom, and France lead regional consumption, driven by building renovation mandates under EU energy efficiency directives, district heating network expansion, and high adoption of press-fit and push-to-connect plumbing systems that require precision tube end preparation. Regulatory quality standards create a favorable environment for premium tool brands and suppress low-cost import penetration relative to other regions.

Asia Pacific: Asia Pacific is both the largest volume market and the fastest-growing region by CAGR, estimated at 7.9% through 2030. China dominates by both production and consumption, with India emerging as the most dynamic growth market as urban infrastructure investment accelerates. Japan and South Korea contribute significantly in the industrial and automotive tube cutting sub-segments. The region benefits from the intersection of massive residential construction pipelines, government-mandated water utility modernization, and a rapidly expanding domestic manufacturing base that is internalizing tube cutting equipment procurement.

Middle East & Africa: This region is recording a CAGR of approximately 6.8%, underpinned by GCC megaproject pipelines—including NEOM, Saudi Vision 2030 infrastructure programs, and UAE industrial zone development—that require extensive plumbing, HVAC, and process piping installation. South Africa and North Africa represent secondary growth pockets tied to mining infrastructure and municipal water system upgrades.

South America: South America represents the smallest regional revenue share at approximately $1.1 billion in 2023, growing at a CAGR of 5.4%. Brazil dominates regional demand through its large residential construction sector and oil and gas pre-salt pipeline network. Argentina and other South American markets remain constrained by macroeconomic volatility but offer long-term opportunity as infrastructure gaps are progressively addressed.

Investment activity within the Pipe and Tube Cutters Market has intensified over the 2022–2024 period, reflecting broader capital flows into the construction tools and industrial equipment ecosystem. The automatic and CNC tube cutting sub-segment has attracted the greatest concentration of venture and private equity interest, given its higher average selling prices, recurring consumable revenue streams, and defensible technology moats built around cutting software, sensor integration, and Industry 4.0 connectivity.

Several strategic acquisitions have reshaped the competitive landscape. Large tool conglomerates have pursued bolt-on acquisitions of specialized pipe processing equipment manufacturers to expand their addressable market in precision industrial cutting, particularly targeting companies with established customer bases in the automotive, aerospace, and semiconductor sectors. These acquisitions are typically valued at 5–8x EBITDA multiples, reflecting premium valuations for technology-differentiated assets

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6.2% from 2020-2034 |

| Segmentation |

|

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Comprehensive validation mechanisms ensuring market intelligence accuracy, reliability, and adherence to international standards.

500+ data sources cross-validated

200+ industry specialists validation

NAICS, SIC, ISIC, TRBC standards

Continuous market tracking updates

Factors such as are projected to boost the Pipe and Tube Cutters Market market expansion.

Key companies in the market include Klein Tools, BYSTRONIC, Imperial, Milwaukee, JSC, Apollo, The Eraser Company, RIDGID, MISUMI India, Husky, The Plumber’s Choice.

The market segments include Type, Pipe Material, End Users.

The market size is estimated to be USD 19.15 billion as of 2022.

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3690, USD 5820, and USD 9870 respectively.

The market size is provided in terms of value, measured in billion and volume, measured in .

Yes, the market keyword associated with the report is "Pipe and Tube Cutters Market," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Pipe and Tube Cutters Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.