1. What are the major growth drivers for the Mechanical Power Transmission Equipment Market market?

Factors such as are projected to boost the Mechanical Power Transmission Equipment Market market expansion.

+1 2315155523

Market Lens IQ is a global market intelligence and strategic consulting firm delivering advanced syndicated research reports, customized industry analysis, competitive intelligence, and data-driven advisory solutions to organizations across international markets. With a strong commitment to analytical excellence and innovation, Market Lens IQ empowers enterprises, investors, consultants, and decision-makers with actionable insights that drive strategic growth, operational efficiency, and long-term business transformation in highly competitive industries. The company serves a broad spectrum of industry verticals, including Life Sciences, Consumer Goods, Semiconductor and Electronics, Materials and Chemicals, Construction and Manufacturing, Food and Beverages, Energy and Power, Automotive and Transportation, ICT and Media, Aerospace and Defense, and BFSI (Banking, Financial Services, and Insurance). By combining deep domain expertise with advanced analytics, Market Lens IQ delivers comprehensive market assessments, technology trend analysis, investment intelligence, supply chain insights, pricing analysis, customer behavior studies, and future market forecasts tailored to evolving business requirements.

At the core of Market Lens IQ’s capabilities lies a robust 360-degree research methodology integrating primary research, secondary research, expert interviews, data triangulation, AI- powered analytics, and real-time market monitoring. Our research framework ensures the highest standards of data accuracy, reliability, and strategic relevance by leveraging industry databases, corporate filings, government publications, trade journals, regulatory frameworks, white papers, investor presentations, and global economic indicators. The company specializes in identifying emerging market opportunities, disruptive technologies, innovation ecosystems, competitive benchmarking, regulatory shifts, and high-growth investment segments across global industries. Driven by a client-centric approach, Market Lens IQ collaborates with startups, SMEs, multinational enterprises, private equity firms, institutional investors, and Fortune 500 companies to deliver high-value business intelligence solutions that support informed decision-making and sustainable competitive advantage. Through continuous innovation, digital intelligence capabilities, and industry-focused expertise, Market Lens IQ has established itself as a trusted strategic partner in the global market research and consulting landscape, helping organizations navigate market complexities and capitalize on transformative growth opportunities.

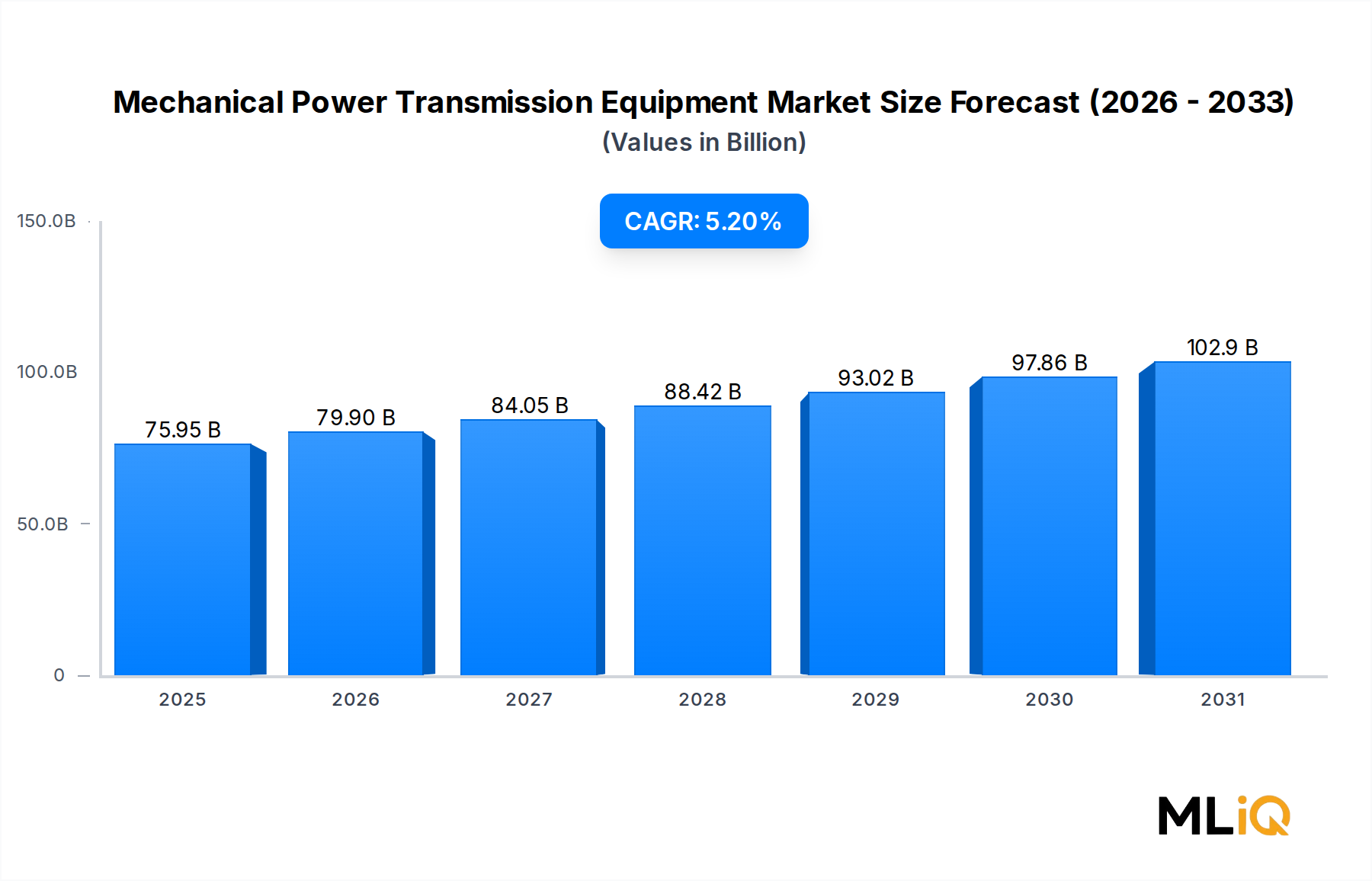

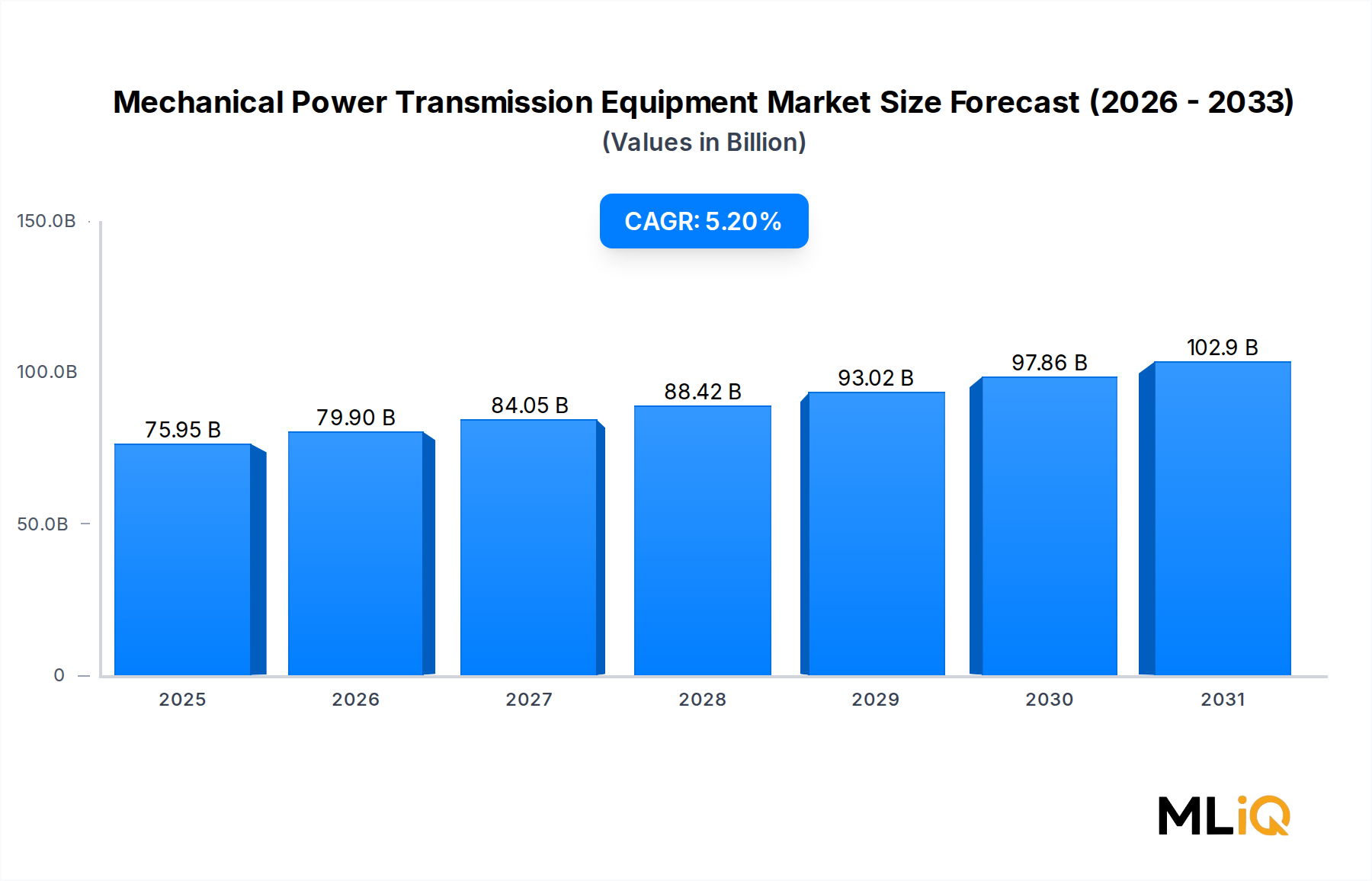

The global Mechanical Power Transmission Equipment Market is valued at $75.95 billion in 2025, projected to expand at a compound annual growth rate (CAGR) of 5.2% through the forecast horizon. This steady expansion reflects the broad-based industrial recovery underway across manufacturing-intensive economies, accelerating capital expenditure in infrastructure, and the persistent modernization of legacy drivetrain and torque-transfer systems across heavy industries.

Mechanical power transmission encompasses a vast array of hardware — from gear drives and chain drives to hydraulic couplings, clutches, and belt-pulley assemblies — all of which serve the singular purpose of converting and transferring rotational force across machinery. The market's resilience stems from its indispensable role in virtually every mechanical system, whether in automotive assembly lines, aerospace ground support equipment, power generation turbines, or mining conveyors.

Key demand drivers include the global push toward factory automation and Industry 4.0 integration, which is prompting original equipment manufacturers (OEMs) to retrofit and upgrade power transmission components with sensor-embedded and IoT-ready variants. Meanwhile, infrastructure megaprojects across Asia Pacific and the Middle East are generating sustained procurement demand for heavy-duty gear drives and hydraulic transmission systems.

On the macroeconomic front, nearshoring trends in North America and Europe are driving domestic manufacturing capacity expansion, directly stimulating demand for power transmission hardware. The automotive sector's ongoing electrification transition presents a nuanced dynamic: while pure electric vehicle platforms reduce reliance on traditional multi-speed transmission systems, hybrid architectures and the continued dominance of internal combustion platforms in commercial vehicles sustain near-term component demand.

The defense and aerospace segment offers incremental tailwinds, particularly as geopolitical tensions elevate defense procurement budgets globally. Power transmission components embedded in actuation, propulsion, and ground mobility platforms remain in high demand.

Looking forward, the market is expected to cross $100 billion by the early 2030s, underpinned by industrial automation proliferation, renewable energy infrastructure buildout (which relies on wind turbine gearboxes and pitch control systems), and the expansion of high-speed rail and logistics networks across emerging economies. Competitive intensity will increase as Asian manufacturers — particularly from China, India, and South Korea — scale up quality standards and challenge incumbent Western OEMs on price-performance metrics.

Among all product segments within the Mechanical Power Transmission Equipment Market, gear drives command the largest revenue share, attributable to their unmatched versatility, torque capacity, and operational reliability across virtually every industrial application. Gear drives — encompassing spur gears, helical gears, bevel gears, worm gears, and planetary gear systems — serve as the cornerstone of mechanical power transmission in industries ranging from automotive manufacturing and mining to wind energy and marine propulsion.

Gear drives dominate due to several structural advantages. First, they are mechanically robust with minimal slippage, making them preferable over belt or chain drives in high-torque, high-load environments. Second, gear drive systems offer precise speed ratios, enabling engineers to tailor output characteristics to exact application requirements. Third, the long service life of properly maintained gear drives — often exceeding 20 years in industrial settings — justifies the higher initial capital outlay, particularly in capital-intensive sectors such as cement, steel, and petrochemicals.

The Industrial Gearbox Market represents the primary sub-segment within gear drives, and it has seen significant investment from major players. ABB, a dominant force in power and automation technologies, integrates advanced gear solutions within its broader drivetrain and motion control product lines. Timken has established itself as a precision-engineering leader, leveraging its metallurgical expertise to produce high-performance gear drives with extended fatigue life. Illinois Tool Works applies its diversified manufacturing capabilities to deliver specialized gear solutions for OEM integration across multiple verticals. Lufkin Industries, with deep roots in oil-field and industrial gearbox manufacturing, commands strong market presence in upstream energy and process industries.

The gear drive segment's market share is not merely holding steady — it is consolidating. Several dynamics are reinforcing this trend. The expansion of wind energy capacity globally has catalyzed demand for large-diameter planetary gear systems used in wind turbine nacelles, where each unit can represent tens of thousands of dollars in component value. Concurrently, the mining sector's push into deeper, more mechanically demanding ore bodies is driving procurement of higher-torque, more durable gear drive configurations.

Digitalization is also transforming the gear drive sub-segment. Leading manufacturers are embedding condition-monitoring sensors and vibration-analysis capabilities directly into gear housings, enabling predictive maintenance integration. This transition from purely mechanical products to "smart" gear systems is elevating average selling prices and creating new service revenue streams for incumbent players.

Geographically, Asia Pacific is the largest consumption zone for gear drives, driven by China's massive industrial base, India's infrastructure expansion, and the region's role as a global manufacturing hub. Europe remains the most technologically advanced market, with German engineering firms setting design benchmarks. North America is experiencing a resurgence in gear drive procurement tied to reshoring manufacturing activity.

The gear drive segment's consolidation is also visible in M&A activity, as larger diversified industrial conglomerates acquire specialized gearbox manufacturers to broaden their drivetrain portfolios. This consolidation is expected to continue, further reinforcing gear drives as the dominant and most structurally significant segment within the broader mechanical power transmission landscape.

Several quantifiable forces are driving expansion across the Mechanical Power Transmission Equipment Market, while a distinct set of structural constraints tempers the pace of growth.

Driver 1: Industrial Automation Acceleration. Global industrial robot installations reached approximately 553,000 units in 2023 (per IFR estimates), each incorporating multiple mechanical power transmission components. As manufacturers pursue automation-driven productivity gains, procurement of gear drives, couplings, and bearings scales commensurately. The Industrial Automation Equipment Market — a directly adjacent space — is itself growing at an estimated CAGR exceeding 8%, creating strong upstream pull for transmission hardware.

Driver 2: Renewable Energy Infrastructure. Wind power capacity additions globally exceeded 117 GW in 2023, with each onshore turbine requiring multi-stage planetary gearboxes and pitch control mechanisms. Offshore wind platforms demand even more robust transmission systems, driving high-value procurement. Solar tracking systems also utilize worm gear drives for panel orientation.

Driver 3: Defense and Aerospace Expenditure. NATO members collectively increased defense spending, with total alliance expenditure surpassing $1.3 trillion in 2024. Aerospace actuation systems, ground vehicle drivetrains, and naval propulsion platforms all incorporate specialized power transmission components, sustaining a high-margin demand stream.

Constraint 1: Raw Material Price Volatility. Steel and specialty alloys — the primary inputs for gears, shafts, and housings — experienced significant price swings between 2021 and 2024, compressing manufacturer margins and complicating long-term contract pricing. The Steel Forgings Market remains susceptible to coking coal price fluctuations and trade policy disruptions.

Constraint 2: Electrification Displacement Risk. The transition toward fully electric vehicles reduces demand for complex multi-ratio transmission systems in passenger cars. While commercial EVs still require reduction gear units, the long-term trajectory points toward simplified drivetrain architectures, posing a structural demand headwind for certain gear drive sub-segments.

Constraint 3: Supply Chain Fragility. Concentrated sourcing of precision-machined components from single-region suppliers — particularly in Asia — creates vulnerability to geopolitical disruption, port delays, and logistics cost spikes, as evidenced during 2021–2022 post-pandemic supply dislocations.

The competitive landscape of the Mechanical Power Transmission Equipment Market is characterized by a mix of diversified industrial conglomerates, specialized OEMs, and regional challengers. Key players are profiled below:

Graham Corporation: A precision-engineered solutions provider focused on energy and defense applications, Graham Corporation supplies specialized heat transfer and fluid handling components that intersect with power transmission in critical process industries.

ABB: A global powerhouse in electrification and automation, ABB integrates mechanical power transmission solutions — including drives, motors, and couplings — within its comprehensive industrial automation portfolio, serving customers across utilities, transportation, and process industries.

Lufkin Industries: Renowned for its oil-field pumping units and industrial gearboxes, Lufkin Industries maintains a strong position in upstream energy and heavy industrial markets, with proprietary gear design capabilities that differentiate its product lines.

Ingersoll-Rand: A diversified industrial manufacturer, Ingersoll-Rand leverages its compressed air and power tool expertise to supply torque and power transmission solutions across manufacturing, energy, and transportation verticals.

Altra: Specializing in precision motion control and power transmission products, Altra serves demanding applications in automation, food and beverage, medical, and industrial markets with an extensive catalog of couplings, clutches, brakes, and gear drives.

Timken: A global leader in engineered bearings and power transmission components, Timken's vertically integrated manufacturing and metallurgical R&D capabilities enable it to deliver premium-performance products with industry-leading fatigue life.

Illinois Tool Works: Operating through multiple business segments, Illinois Tool Works applies its differentiated manufacturing model to produce specialized fasteners, welding systems, and power transmission components for OEM customers globally.

SKF: A Swedish precision engineering company, SKF is a world leader in bearings, seals, and lubrication systems, with significant market share in the Industrial Bearings Market and growing capabilities in condition monitoring and predictive maintenance.

Zebra Technologies: Primarily known for its enterprise visibility and tracking solutions, Zebra Technologies contributes to the smart manufacturing ecosystem that enables real-time monitoring of power transmission equipment performance in logistics and warehouse environments.

Gardner Denver: A producer of industrial machinery and blowers, Gardner Denver supplies compression and fluid transfer solutions that incorporate mechanical power transmission elements across oil and gas, medical, and industrial markets.

Torotrak: A specialist in continuously variable transmission (CVT) and flywheel hybrid technology, Torotrak focuses on developing high-efficiency power transmission innovations for commercial vehicles and off-highway equipment.

January 2024: ABB announced the expansion of its Dresden, Germany, motor and drive manufacturing facility, increasing production capacity for high-efficiency transmission-integrated drive systems by an estimated 25% to meet surging European industrial demand.

March 2024: Timken completed the acquisition of a European precision gearbox manufacturer, strengthening its position in the wind energy and industrial robotics sub-segments and adding approximately $180 million in annualized revenue to its power transmission division.

June 2024: SKF launched its next-generation condition monitoring platform for rotating equipment, integrating AI-driven anomaly detection directly into bearing and gear drive assemblies, targeting predictive maintenance markets in steel, mining, and pulp industries.

August 2024: Altra Industrial Motion announced a strategic partnership with a leading North American automation integrator to co-develop servo-actuated clutch and brake systems optimized for collaborative robot (cobot) applications.

October 2024: The U.S. Department of Energy finalized efficiency standards for electric motors and connected mechanical drive systems, mandating higher minimum efficiency thresholds effective 2027, accelerating OEM product redesign cycles across the sector.

December 2024: Illinois Tool Works divested a non-core power transmission sub-segment to focus capital allocation on higher-margin precision fastening and welding technologies, signaling continued portfolio rationalization among diversified industrial players.

February 2025: Gardner Denver introduced a new line of oil-free screw compressor systems with integrated helical gear drives designed for pharmaceutical and semiconductor cleanroom environments, targeting a market estimated at $2.4 billion globally.

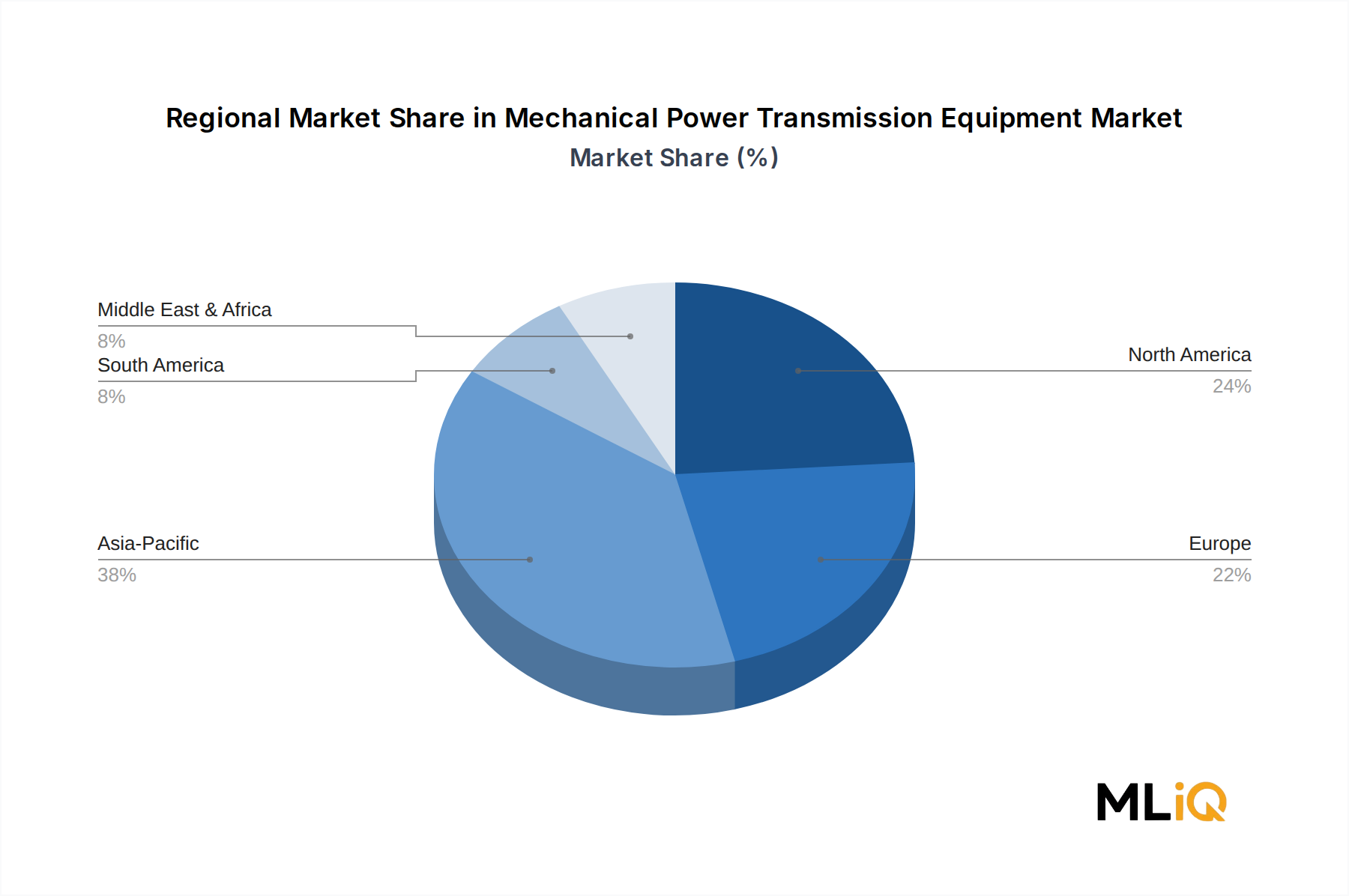

The Mechanical Power Transmission Equipment Market exhibits meaningful regional variation in terms of growth trajectory, maturity, and demand composition.

Asia Pacific is simultaneously the largest and fastest-growing regional market, accounting for an estimated 38–40% of global revenue in 2025. China dominates the regional landscape, driven by its massive industrial base encompassing steel, cement, mining, automotive, and electronics manufacturing. India is the fastest-growing sub-market within the region, expanding at an estimated CAGR of 7.5–8.0%, supported by the government's "Make in India" manufacturing push, infrastructure investment acceleration, and growing automotive OEM activity. Japan and South Korea contribute high-value demand tied to robotics, semiconductor equipment, and precision machine tools. The ASEAN bloc is emerging as a meaningful demand center as manufacturing supply chains diversify away from China.

North America represents the second-largest market, with the United States accounting for the majority of regional revenue. The U.S. market benefits from reshoring-driven manufacturing investment, defense procurement, and energy sector activity — particularly in oil and gas and renewable energy. Canada contributes through its resource extraction industries, while Mexico's expanding automotive manufacturing cluster generates steady transmission component demand. The region's CAGR is estimated at 4.5–5.0%, reflecting its status as a mature but actively reinvesting market.

Europe is the most technologically advanced regional market, characterized by strong demand for high-precision, high-efficiency power transmission components. Germany leads in both consumption and production, anchored by its world-class machine tool and automotive industries. The Nordics contribute through offshore wind and marine applications, while Eastern European manufacturing growth provides incremental demand. The region's CAGR is estimated at 3.8–4.2%, constrained by near-term economic headwinds but supported by green energy transition investments.

Middle East and Africa represent an emerging growth corridor, with GCC nations investing heavily in industrial diversification beyond hydrocarbons. South Africa's mining sector drives regional component demand. The regional CAGR is estimated at 5.5–6.0%.

South America, led by Brazil and Argentina, grows at approximately 4.0–4.5% CAGR, tied to agricultural machinery, mining, and oil exploration activity.

The supply chain architecture underpinning the Mechanical Power Transmission Equipment Market is multi-tiered, with upstream dependencies concentrated in a handful of critical material categories whose price behavior materially impacts manufacturer economics.

Steel — encompassing carbon steel, alloy steel, and case-hardening grades — is the single most significant raw material input, comprising gear teeth, housings, shafts, and structural frames. Between 2020 and 2022, hot-rolled coil prices in North America surged from approximately $500/ton to over $1,900/ton before retreating. This volatility compelled manufacturers to renegotiate long-term supply agreements, dual-source from domestic and import suppliers, and accelerate inventory hedging strategies. The Steel Forgings Market, which supplies precision near-net-shape blanks for gear and shaft production, remains tightly linked to coking coal and iron ore commodity cycles.

Chrome and molybdenum alloys are critical for high-strength, wear-resistant gear steels used in heavy-duty applications. Supply concentration in a small number of producing countries — particularly for molybdenum — creates geopolitical sourcing risk. Price trends for these specialty alloys remained elevated through 2023–2024, sustained by defense and energy sector demand.

Copper is a secondary but meaningful input, primarily in motor windings integrated within electromechanical transmission assemblies. Copper's price trajectory has been upward-biased due to electrification demand globally, adding cost pressure to motor-transmission integrated systems.

Precision bearings — a key sub-component of gear drives and chain drive assemblies — are largely sourced from a concentrated set of manufacturers in Japan, Germany, Sweden, and China. The Industrial Bearings Market demonstrated significant lead time extensions during 2021–2022, with some bearing grades experiencing 40–52 week lead times, directly stalling power transmission equipment assembly lines.

The Roller Chain Market, supplying chain drive sub-systems, depends on cold-drawn steel wire and specialized heat treatment processes, making it susceptible to energy cost inflation — particularly in Europe following the 2022 natural gas price shock.

Man

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.2% from 2020-2034 |

| Segmentation |

|

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Comprehensive validation mechanisms ensuring market intelligence accuracy, reliability, and adherence to international standards.

500+ data sources cross-validated

200+ industry specialists validation

NAICS, SIC, ISIC, TRBC standards

Continuous market tracking updates

Factors such as are projected to boost the Mechanical Power Transmission Equipment Market market expansion.

Key companies in the market include Graham Corporation, ABB, Lufkin Industries, Ingersoll-Rand, Altra, Timken, Illinois Tool Works, SKF, Zebra Technologies, Gardner Denver, Torotrak.

The market segments include Type, Application.

The market size is estimated to be USD 75.95 billion as of 2022.

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3690, USD 5820, and USD 9870 respectively.

The market size is provided in terms of value, measured in billion and volume, measured in .

Yes, the market keyword associated with the report is "Mechanical Power Transmission Equipment Market," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Mechanical Power Transmission Equipment Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.